Internal Finance - Sources of Finance, Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Internal Finance

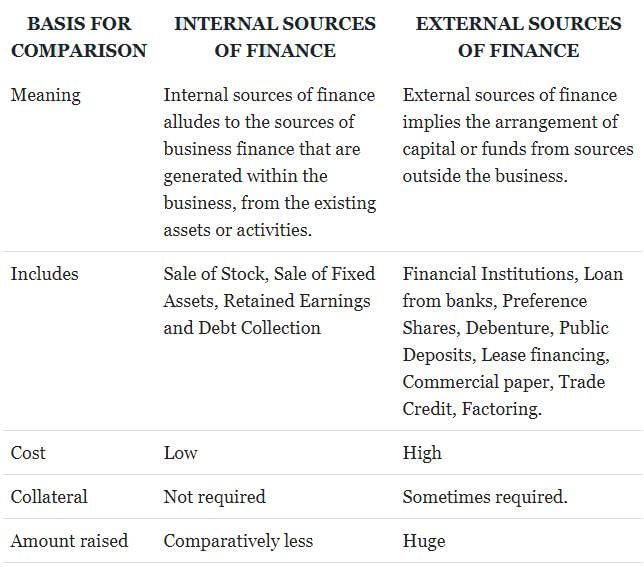

A company can mobilize finance through external and internal sources. A new company may not raise internal sources of finance and they can raise finance only external sources such as shares, debentures and loans but an existing company can raise both internal and external sources of finance for their financial requirements. Internal finance is also one of the important sources of finance and it consists of cost of capital while compared to other sources of finance.

Internal source of finance may be broadly classified into two categories:

A. Depreciation Funds

B. Retained earnings

Depreciation Funds

Depreciation funds are the major part of internal sources of finance, which is used to meet the working capital requirements of the business concern. Depreciation means decrease in the value of asset due to wear and tear, lapse of time, obsolescence, exhaustion and accident. Generally depreciation is changed against fixed assets of the company at fixed rate for every year. The purpose of depreciation is replacement of the assets after the expired period. It is one kind of provision of fund, which is needed to reduce the tax burden and overall profitability of the company.

Retained Earnings

Retained earnings are another method of internal sources of finance. Actually is not a method of raising finance, but it is called as accumulation of profits by a company for its expansion and diversification activities. Retained earnings are called under different names such as; self finance, inter finance, and plugging back of profits. According to the Companies Act 1956 certain percentage, as prescribed by the central government (not exceeding 10%) of the net profits after tax of a financial year have to be compulsorily transferred to reserve by a company before declaring dividends for the year. Under the retained earnings sources of finance, a part of the total profits is transferred to various reserves such as general reserve, replacement fund, reserve for repairs and renewals, reserve funds and secrete reserves, etc.

Advantages of Retained Earnings

Retained earnings consist of the following important advantages:

- Useful for expansion and diversification: Retained earnings are most useful to expansion and diversification of the business activities.

- Economical sources of finance: Retained earnings are one of the least costly sources of finance since it does not involve any floatation cost as in the case of raising of funds by issuing different types of securities.

- No fixed obligation: If the companies use equity finance they have to pay dividend and if the companies use debt finance, they have to pay interest. But if the company uses retained earnings as sources of finance, they need not pay any fixed obligation regarding the payment of dividend or interest.

- Flexible sources: Retained earnings allow the financial structure to remain completely flexible. The company need not raise loans for further requirements, if it has retained earnings.

- Increase the share value: When the company uses the retained earnings as the sources of finance for their financial requirements, the cost of capital is very cheaper than the other sources of finance; Hence the value of the share will increase.

- Avoid excessive tax: Retained earnings provide opportunities for evasion of excessive tax in a company when it has small number of shareholders.

- Increase earning capacity: Retained earnings consist of least cost of capital and also it is most suitable to those companies which go for diversification and expansion.

Disadvantages of Retained Earnings

Retained earnings also have certain disadvantages:

- Misuses: The management by manipulating the value of the shares in the stock market can misuse the retained earnings.

- Leads to monopolies: Excessive use of retained earnings leads to monopolistic attitude of the company.

- Over capitalization: Retained earnings lead to over capitalization, because if the company uses more and more retained earnings, it leads to insufficient source of finance.

- Tax evasion: Retained earnings lead to tax evasion. Since, the company reduces tax burden through the retained earnings.

- Dissatisfaction: If the company uses retained earnings as sources of finance, the shareholder can’t get more dividends. So, the shareholder does not like to use the retained earnings as source of finance in all situations.

Difference Between Internal and External Sources of Finance

|

44 videos|75 docs|18 tests

|

FAQs on Internal Finance - Sources of Finance, Accountancy and Financial Management - Accountancy and Financial Management - B Com

| 1. What are the main sources of internal finance? |  |

| 2. What is the role of accountancy in managing internal finance? | |

| 3. What is financial management and why is it important for internal finance? | |

| 4. How can businesses improve their internal finance management? | |

| 5. How does internal finance impact the overall financial health of an organization? | |

|

4.80/5 Rating |

|

Dec 23, 2024 Last updated |

|

44 videos|75 docs|18 tests

|

|

Explore Courses for B Com exam

|

|

Viva Questions

,practice quizzes

,Exam

,Important questions

,Semester Notes

,MCQs

,Free

,Sample Paper

,ppt

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Internal Finance - Sources of Finance

,Summary

,Previous Year Questions with Solutions

,Extra Questions

,Internal Finance - Sources of Finance

,mock tests for examination

,study material

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,video lectures

,past year papers

,Objective type Questions

,shortcuts and tricks

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Internal Finance - Sources of Finance

,

Internal Finance - Sources of Finance, Accountancy and Financial Management Free PDF Download

Importance of Internal Finance - Sources of Finance, Accountancy and Financial Management

Internal Finance - Sources of Finance, Accountancy and Financial Management Notes

Internal Finance - Sources of Finance, Accountancy and Financial Management B Com Questions

Study Internal Finance - Sources of Finance, Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|