Loan Financing - Sources of Finance, Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Loan Financing

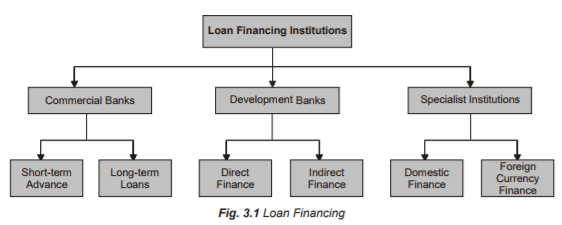

Loan financing is the important mode of finance raised by the company. Loan finance may be divided into two types:

(a) Long-Term Sources

(b) Short-Term Sources

Loan finance can be raised through the following important institutions

Financial Institutions

With the effect of the industrial revaluation, the government established nation wide and state wise financial industries to provide long-term financial assistance to industrial concerns in the country. Financial institutions play a key role in the field of industrial development and they are meeting the financial requirements of the business concern. IFCI, ICICI, IDBI, SFC, EXIM Bank, ECGC are the famous financial institutions in the country.

Commercial Banks

Commercial Banks normally provide short-term finance which is repayable within a year. The major finance of commercial banks is as follows:

Short-term advance: Commercial banks provide advance to their customers with or without securities. It is one of the most common and widely used short-term sources of finance, which are needed to meet the working capital requirement of the company. It is a cheap source of finance, which is in the form of pledge, mortgage, hypothecation and bills discounted and rediscounted.

Short-term Loans Commercial banks also provide loans to the business concern to meet the short-term financial requirements. When a bank makes an advance in lump sum against some security it is termed as loan. Loan may be in the following form:

(a) Cash credit: A cash credit is an arrangement by which a bank allows his customer to borrow money up to certain limit against the security of the commodity.

(b) Overdraft: Overdraft is an arrangement with a bank by which a current account holder is allowed to withdraw more than the balance to his credit up to a certain limit without any securities.

Development Banks

Development banks were established mainly for the purpose of promotion and development the industrial sector in the country. Presently, large number of development banks are functioning with multidimensional activities. Development banks are also called as financial institutions or statutory financial institutions or statutory non-banking institutions. Development banks provide two important types of finance:

(a) Direct Finance

(b) Indirect Finance/Refinance

Presently the commercial banks are providing all kinds of financial services including development-banking services. And also nowadays development banks and specialisted financial institutions are providing all kinds of financial services including commercial banking services. Diversified and global financial services are unavoidable to the present day economics. Hence, we can classify the financial institutions only by the structure and set up and not by the services provided by them.

|

44 videos|75 docs|18 tests

|

FAQs on Loan Financing - Sources of Finance, Accountancy and Financial Management - Accountancy and Financial Management - B Com

| 1. What are the different sources of finance for loan financing? |  |

| 2. What is the role of accountancy in loan financing? | |

| 3. What is the role of financial management in loan financing? | |

| 4. How do banks determine the eligibility for loan financing? | |

| 5. What are the advantages of peer-to-peer lending for loan financing? | |

|

1.6K Views |

|

4.75/5 Rating |

|

Dec 23, 2024 Last updated |

|

44 videos|75 docs|18 tests

|

|

Explore Courses for B Com exam

|

|

Exam

,shortcuts and tricks

,Important questions

,Free

,Loan Financing - Sources of Finance

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Previous Year Questions with Solutions

,past year papers

,Loan Financing - Sources of Finance

,study material

,Sample Paper

,Semester Notes

,Loan Financing - Sources of Finance

,ppt

,Summary

,Extra Questions

,video lectures

,mock tests for examination

,Objective type Questions

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Viva Questions

,practice quizzes

,Accountancy and Financial Management | Accountancy and Financial Management - B Com

,MCQs

;

Loan Financing - Sources of Finance, Accountancy and Financial Management Free PDF Download

Importance of Loan Financing - Sources of Finance, Accountancy and Financial Management

Loan Financing - Sources of Finance, Accountancy and Financial Management Notes

Loan Financing - Sources of Finance, Accountancy and Financial Management B Com Questions

Study Loan Financing - Sources of Finance, Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|