Meaning, Scope & Objectives - Introduction to Cost Accounting, Cost Accounting

Introduction

Cost Accounting is the branch of accounting that deals with recording, classifying, analysing and controlling costs associated with products, services, processes and operations. Its primary purpose is to ascertain the cost of production or service, provide management with information for planning and control, and assist in decision-making to improve profitability and efficiency.

- Cost accounting determines the costs of products or services and shows how cost, price and profit are related.

- It produces regular reports and statements that are useful for cost control, budgeting and managerial decisions.

- This unit covers: the nature and scope of cost accounting, its objectives, the need for costing, differences between cost accounting and financial accounting, the advantages of cost accounting and the essentials required for installation of an effective costing system.

Need for Costing

- Every economic activity, especially those that produce goods or provide services, involves some level of spending.

- This spending can include costs for materials, labor, and other direct or indirect expenses.

- The main goal of these activities in a business is to make a profit.

- Therefore, it is important to clearly identify all three parts of a transaction: cost, profit, and price.

Example:

- A shoe factory produces a new sports shoe. The costs per pair are: Materials = Rs. 20, Labour = Rs. 30, Other expenses (overheads) = Rs. 25.

- Total cost per pair = 20 + 30 + 25 = Rs. 75.

- If the selling price is Rs. 100 per pair, the profit per pair = 100 - 75 = Rs. 25.

- Management requires such product-wise cost and profit information for pricing, budgeting, control and performance evaluation; financial accounting records do not provide this level of detail.

Limitations of Financial Accounting

- Financial accounts provide aggregate information for the enterprise as a whole in terms of income, expenses, assets and liabilities, but do not give detailed operating information for departments, products, processes or other units of activity.

- They do not classify expenses systematically into categories such as direct and indirect, or fixed and variable, so product-wise cost assignment at each stage of production is missing.

- Financial accounting does not establish a control system for the main cost elements (materials and labour); wastages, losses and inefficient use of labour may remain unchecked.

- It does not provide standards or norms against which cost items can be compared for variance analysis and control.

- Financial accounts do not supply adequate costing information required for fixation of selling prices or preparation of detailed quotations and tenders.

- Financial accounting is largely historical and compiled at period ends, making frequent interim compilation of detailed cost data difficult.

- Product-wise profit and loss analysis is generally not possible from financial accounts alone; financial statements act like a thermometer (indicating a symptom) but do not reveal causes or diagnosis.

Costing and the Economy

Modern economies exhibit characteristics that increase the importance and usefulness of costing systems. Key features include:

- Global competition: Firms face competition from domestic and international producers; strict cost control and competitive pricing are essential for survival.

- Limited resources: Resources are scarce and must be used economically; costing helps reduce waste and improve utilisation.

- Complex management: Industrial management has become more complicated; decisions at many stages require reliable cost information.

- Need for fast decisions: Quick and accurate management decisions depend on timely, trustworthy cost data.

- Special responsibilities: Businesses have social duties to ensure consistent quality, fair pricing and steady supply; costing supports these obligations.

- Optimum profit: Profit maximisation depends on effective financial, operational and marketing performance; costing links these areas through cost control and analysis.

Because costing supports pricing decisions, control of wastage, resource management, process improvement, timely information flow and overall efficiency, it has become indispensable for industrial and non-industrial organisations alike.

Definitions and Terminology

- The term Costing refers to the technique or method of determining costs. It comprises the principles and rules applied to ascertain the cost of products and services.

- The term Cost Accounting denotes the process of recording, classifying, analysing and reporting cost data. Cost accounting begins with recording cost-related transactions and ends with the preparation of reports and statements to aid management control.

- Wheldon defined costing as involving classification, recording and appropriate allocation of expenditure to determine the cost of products or services, and presenting the results of operations in a form useful to management.

- The Institute of Cost and Management Accountants (ICMA) (UK) has distinguished historically between terms such as Cost Accounting and Cost Accountancy. In modern usage, Cost Accounting is commonly treated as part of Management Accounting covering budgets, standard costs, actual costs, variance analysis and profitability of operations.

- In summary, cost accounting is a methodical approach to accounting for costs that assists in planning, controlling and decision-making.

Functions of Cost Accounting

- Analysis of cost components and behaviour.

- Recording of cost transactions and maintaining cost ledgers and records.

- Establishing budgets and setting standards for costs and performance.

- Comparison of actual performance with standards and budgets (variance analysis).

- Reporting cost information to various levels of management in suitable formats and at required intervals.

Objectives (Objects) of Cost Accounting

The primary objectives of cost accounting are to:

- Ascertain the cost of products and services.

- Assist in fixation of selling prices and preparation of quotations and tenders.

- Analyse and classify different elements of cost forming the total cost.

- Identify causes of wastage and recommend corrective action to check wastage.

- Control costs by establishing budgets, standards and through analysis and comparison.

- Provide management with cost information to facilitate decision-making.

- Evaluate relative efficiency of departments, branches, products, units, plants and machinery and suggest ways to increase productivity.

- Prepare interim cost statements and reports to review production, sales and profit and to plan future activities.

These objectives show that costing is essential for economic operation and managerial efficiency.

Scope of Cost Accounting

The scope of cost accounting extends across various activities in an organisation. Major areas included are:

- Cost ascertainment: Determining unit costs by job, process, contract or service costing.

- Cost control: Establishing standards, budgets and analysing variances to maintain control over operations.

- Inventory valuation: Valuing work-in-progress, finished goods and stores for internal use and for financial reporting.

- Budgetary and performance control: Preparing budgets and monitoring actual performance against them.

- Pricing decisions: Supplying data for setting selling prices and evaluating special orders.

- Decision support: Providing information for make or buy decisions, product mix, discontinuation, and capital investment choices.

- Cost reduction and efficiency: Identifying opportunities for reducing costs and improving processes and resource utilisation.

- Cost reporting: Preparing periodic internal reports for management at different levels and functional areas.

- Application to services: Extending costing techniques to hospitals, transport, education, banking and other service sectors.

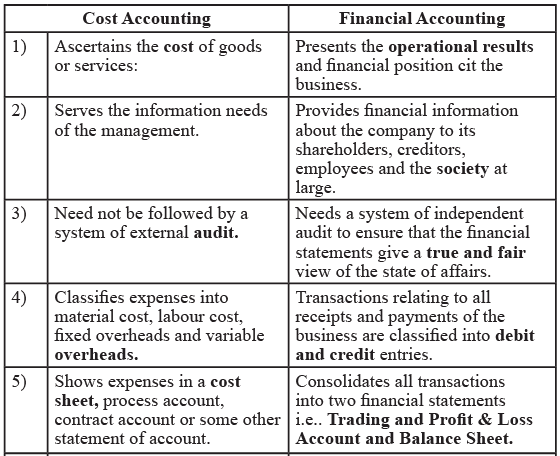

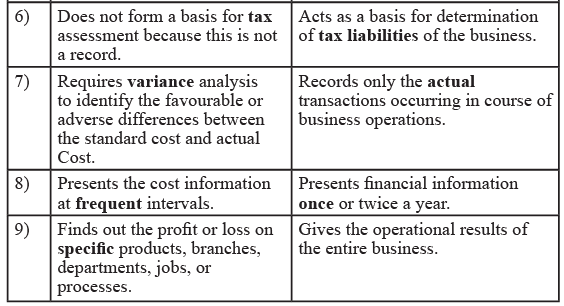

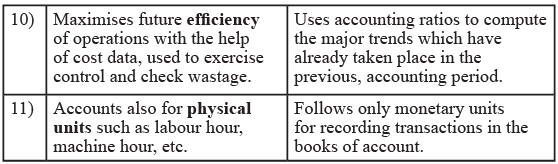

Difference Between Cost Accounting and Financial Accounting

Common goal: Although their purposes and formats differ, cost accounting and financial accounting both assist the organisation in different but complementary ways for its smooth functioning and decision support.

Advantages of Cost Accounting

- A properly organised costing system provides continuous information on production, costs, materials, labour, inventory and plant capacity, aiding effective planning.

- It helps identify unproductive activities, wastage, obsolete machinery and inefficiencies for corrective action.

- Cost accounting ensures the collection of reliable cost data for internal use.

- It supports the preparation of budgets and business forecasts.

- Standard setting and variance analysis enable measurement of operational performance.

- It assists in determining appropriate selling prices and preparing competitive bids.

- Cost comparison across periods, products or departments becomes possible.

- Advance estimates of costs and revenues can be prepared to support planning.

- Costing supports effective inventory control and regular stock verification.

- It highlights unused capacity and the cost consequences of working below installed capacity.

- Frequent determination of cost and profit with cause analysis helps management take timely corrective measures.

- Decisions can be based on factual cost data, improving choices on output levels, make-or-buy, investment in machinery, special orders, product introduction or discontinuation, and labour-machine substitution.

Because of these advantages, costing is used not only in manufacturing but also in service and public sector organisations, benefiting consumers, employees, investors and the broader economy through improved efficiency and pricing.

Installation of a Costing System

There is no one-size-fits-all costing system. Rules and methods must be tailored to the organisation's nature, scale and processes. A well-designed costing system should suit the business and be practical to operate.

- Conduct a preliminary investigation to understand the product range, organisation structure, manufacturing processes and selling and distribution methods.

- Ensure minimal disruption during implementation and introduce the system gradually.

- Design the system to be concise, user-friendly and cost-effective to operate.

- Produce regular reports at appropriate levels of management and integrate costing with the financial accounting system where possible.

- Decide the primary objectives of the costing system (for example, price fixation, cost control, performance measurement or a combination of these).

- Assess practical difficulties and plan to overcome them before full implementation.

Possible Difficulties in Implementation

- Lack of adequate support from top management and resistance from some officers.

- Opposition from staff who currently operate the financial accounting system.

- Resentment at other levels because of additional work arising from costing procedures.

- Shortage of trained and qualified personnel to manage the costing system.

- High initial costs involved in installation of the system.

Factors to be Considered Before Installation

- Clear statement of the objective of the costing system.

- Nature of the business and the suitability of different costing techniques.

- Quality and attitude of management and staff towards change.

- Size and type of organisation, scope of authority and reporting requirements.

- Technical aspects of the production process and its impact on cost measurement.

- Possibility of reconciling cost and financial accounts or integrating them through control accounts.

- Quantum and frequency of information required and the practicability of data collection.

- Extent to which supporting staff appreciate and will cooperate with regular data collection.

Success Factors for a Costing System

- The system must fit the needs and objectives of the business.

- It should be user-friendly, with standard forms and clear purposes for records and reports.

- It must have full support from staff and management at all levels.

- The system should guarantee timely and regular delivery of information for cost reports.

- Integration with the financial accounting system should be possible to reconcile results.

- It should enable effective cost control and comparison between estimates and actuals.

- The system must be flexible to adapt to changing business conditions.

- The cost of installation and operation should be justified by the benefits obtained.

Careful planning, phased introduction and continuous review are essential to ensure that a costing system delivers the intended advantages and supports managerial objectives effectively.

FAQs on Meaning, Scope & Objectives - Introduction to Cost Accounting, Cost Accounting

| 1. What's the exact meaning of cost accounting and how is it different from financial accounting? |  |

| 2. Why do companies need to track costs through cost accounting systems instead of just using regular accounting? | |

| 3. What are the main objectives of cost accounting that B Com students should focus on for exams? | |

| 4. How does the scope of cost accounting cover different business functions and departments? | |

| 5. What practical examples show how cost accounting helps management make better business decisions? | |