Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting | Cost Accounting - B Com PDF Download

Introduction

- Incentive wage systems are considered to be incentive management systems. Traditionally, incentive wage plans have been thought of as payment plans based on the output of the employee, generally considered to be a factory employee. But incentive wage systems of today go far beyond the simple single objective of payment for output. Now-a-days incentive wage systems are so designed that the employee feels satisfied intrinsically as well as extrinsically.

- Incentive wages relate earnings to productivity and may use premiums, bonuses or a variety of rates to compensate for superior performance (Dale Yoder, 1974). Thus, the incentive plans offer an attraction of extra payment for efficiency or more production. They are popular all over the world and are known by different names like variable pay, pay for performance, contingent pay, merit pay etc.

Objectives Of Wage Incentive Plans

- The objectives of incentive wage systems have been made clear by McGregor(1960) when he defines them as “a formal method providing an opportunity for every member of the organization to contribute his brain and ingenuity as well as his physical efforts to the improvement of organizational effectiveness.

- It is the means by which rich opportunities are provided to every member of the organization to satisfy his higher level needs through efforts directed towards the objectives of the enterprise.”

Benefits Of Incentive Compensation

Incentive compensation, also called ‘payment by result’, is essentially a managerial device for increasing workers’ productivity. Simultaneously, it is a method of sharing gains in productivity with workers by rewarding them financially for their increased productivity.

The advantage of incentive plans are as under:

- Alignment between Organization’s Objectives and Employees’ Objectives: The employee tries to increase productivity which is also the aim of the organization.

- Wage Get Related to Output: Differences in employees’ ability, motivation and output are automatically recognized and rewarded accordingly. This understanding by the employees tends to reduce the friction, jealousy, and resentment in the work group.

- Unit Labor Costs are reduced: Incentive wage plans result in reduction of per unit labor, both direct and indirect, costs as the efficiency is emphasized on.

- Need for Less Supervision: Employees need lesser supervision as the employees are disciplined and responsible.

- Good Human Relations: There are good human relations in the firm as the workers are satisfied with higher earnings and management with increased productivity.

Limitations Of Incentives Compensation

Except employee’s attitudes, all other limitations of incentive wage systems centre around situations involving the firm.

These limitations are briefly discussed below:

- Lack of Receptive Attitude on the Part of the Management and the Employees: The proper functioning of the system required existence of mutual trust between labors and management. If workers think that high, unattainable targets have been fixed, and/or management thinks that workers are not putting in their best efforts, the system is going to fail.

- Lack of proper Management Practices: For incentives wages to be equitable, working condition must be as nearly standard, uniform, and dependable as possible. They should be available to all employees. Management must make sure that enough work will be provided to workers so that maximum wages can be earned by them. As most of these sound management practices are absent, wage incentive systems also become less beneficial.

- Leads to Inequities in the Wage Structure: All the jobs in an organization can be divided into two types manual jobs and physical jobs. Performance of physical jobs is not that easily identifiable so they are paid according to straight time basis. Many times, incentive pay systems result in situations where hardworking but low skilled employees working on incentive pay jobs earn more than the more skilled employees working on jobs for which payment is made according to straight time wages. These pay inequities can destroy social relationships, build resentment and animosity among employees.

Types Of Incentive Plans

Following Exhibit shows an overall view of systems of wage payment and incentive plans.

A good incentive plan should encourage the workers to work hard and produce more than the standard production set for them. There are many wage incentive plans which reward the workers for their better performance. The standard output is determined on the basis of time and motion studies by the specialists and the rates of wages are fixed for different jobs on the basis of job evaluation.

Broadly speaking, the various wage incentive plans can classified into two groups:

- Individual incentive Plans,

- Group Incentive Plans

Individual Incentive Plans

Under this, earnings are directly related to the performance of the individual employee. Individual incentives may be based on time or output. In time based plans, a standard time is determined and incentive is paid if any employee completes the job in less than standard time. In output based plans, a standard of output is determined and an employee producing more than standard output is given incentive.

Output linked incentives can lead to:

- Earnings varying in proportion to output; or;

- Earnings varying less proportionately to output; or;

- Earnings varying more proportionately to output; or;

- Earnings varying in different proportions at different levels of output.

Different incentive plans that reward efficiency are discussed here under:

- The Straight Piece Work System.

- Worker is paid at a specified rate per unit of output.

- The standard Hour System.

- A standard time is worked out to complete a job and in case an individual completes the job before time, he earns wages for the time saved.

Halsey Premium Plan

This incentive plan was devised by P.A. Halsey This system is a simple combination of time-speed basis of payment. Under this plan, a minimum time wage is guaranteed to every worker. A standard time is fixed for the completion of a job. If a worker performs his job in less than the standard time, he is rewarded. But there is no penalty for performing the job in more than the standard time fixed. The slow worker is paid the time wages and the efficient worker is paid some bonus in addition to the time wages. The bonus is in proportion to the wage which he could have earned during the time saved.

The working of Halsey Premium Plan is explained with the help of the following illustration:

Standard time (S) = 10 hours

Rate (R) = Rs. 4 per hour

Time (T) = 6 hours

Rate of Bonus (P) = 50%of time saved

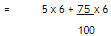

Total Wages = T X R + (S-T) X P X R

= 6 X 4 + (10-6) X ½ X 4

= Rs. 32.00

In the above illustration, the worker gets Rs. 8 extra than he would have earned under the time wage system.

The merits of Halsey plan are as under:

- Halsey premium plan is very simple to understand. The amount of wages can be calculated very easily.

- Both the workers and the employer get the benefit of time saved.

- Halsey plan gives due importance to the efficient workers by paying them bonus for the time saved by them in doing a particular job.

- Minimum wage is assured to each worker. Every worker gets wages for the time he has actually devoted at the fixed rate irrespective of his output.

Halsey plan suffers from the following limitations:

- Workers may not like the sharing of the benefit of their efficiency with the employers. Under this plan, the worker get wages for 50% of the time saved only.

- There may be deterioration in the quality of work because the worker may just rush through not caring for the quality of the product or the amount of waste of raw materials.

- The standard time may not have been properly fixed.

Rowan Bonus Plan

Rowan Plan is a modification of Halsey Plan. It guarantees the minimum time wages and does not penalize the slow worker. A standard time as fixed for the completion of a job and the bonus is paid on the basis of time saved. Bonus is a proportion of the wages earned by the worker for the time taken by him and the proportion is the ratio of time saved to standard time. It implies that as the time saved increases, time taken will be reduced and as such the bonus would increase at a diminishing rate. This will check over speeding and overcome a major drawback of Halsey Plan.

The working of this plan is explained with the help of the following illustration:

Standard time(S) = 10 hours

Time taken (T) = 6 hours

Rate ( R) = Rs. 4 per hour

Total wages = T * R * [ T * R * Time saved__]

Standard time

= 6 * 4 + (6 * 4 * 4/10)

= Rs. 33.60

The advantages of Rowan plan are as follows:

- As under Halsey plan, the minimum wages are assured in Rowan plan also.

- Employer are also benefited when the efficient workers get bonus.

- The efficient workers get bonus at a diminishing rate if they save more than 50 percent of the standard time. This checks them to overstrain themselves and compels them to maintain quality.

The limitations of Rowan plan are as under:

- Where time saved is more than 50 percent of standard time, employees get bonus at a diminishing rate. Thus, a worker is discouraged to achieve saving in time more than 50 percent of the standard time.

- Calculation of wages is difficult and the workers may not be able to understand this system.

- The workers do not like sharing of the benefits of time saved by them.

Emerson Efficiency Plan

- Under this plan, a minimum time wage is guaranteed to the workers. Conditions of work are standardized and standard output is fixed which is to be completed within a specified period of time .This plan is similar to Gantt’s Task and Bonus Plan and is an improvement over the Taylor’s Differential Piece Rate Plan.

- Under this plan, a worker is entitled to bonus if he is able to achieve 66.67 percent or more of the standard. If a worker’s output is less than 66.67 percent of the standard output, he does not get any bonus, but he gets the minimum time wages. The workers whose output exceeds 66.67 percent of the standard get incentives at a differential piece rate, a small bonus is paid for increases in efficiency from 66.67 percent upwards, until at 80 percent efficiency the bonus payable is 4 percent, at 90 percent efficiency, it is 10 percent and at 100 percent, 1 percent bonus is given for every additional 1 percent efficiency.

- For instance, if the standard output is 25 units and a worker produces 18 units, he is 90 percent efficient. He will get wages for the day plus 10 percent bonus. But if he produces 25 units, his efficiency will be 125 percent and his remuneration will be day’s wages plus 45 percent bonus (20per cent of 100 per cent and 25 per cent for efficiency above 100 percent.).

- The chief advantage of this plan to the workers is that their minimum wages for the day are secured. If a worker is unable to produce 66.67 per cent of the standard output, he is not deprived of his daily wage. Secondly, there is enough scope for earning more and more for the efficient workers.

- The rate of bonus increases at an increasing rate. This plan is very beneficial to the extraordinary workers. This plan is criticized by some people because the bonus rates are not uniform. Below 100 per cent efficiency 20 per cent bonus is to be distributed among the additional 33.33 efficiency. But after 100 per cent efficiency, bonus rate increases exactly in proportion to increase in efficiency.

Bedeaux Point Plan

- Under this plan, the minute is the time unit described as the standard minute and accounted as Bedeaux point B. In determining the Bs, the time of operation and the time of rest taken into account. Thus, B may be defined as a fraction of a minute of effort plus a fraction of compensation rest always aggregating unity. The standard time for each job is fixed after undertaking time and motion study and expressed in terms of Bs. The standard time for a job is the number of Bs allowed to complete it. Thus, if the standard time required for a job is five hours, it will be expressed as 300 Bs.

- The workers who are not able to or are just able to complete the work within standard time are paid at the normal time rate. Those who are able to complete their work earlier are paid bonus equal to the wages for time saved as indicated by the excess of B point over the actual time taken.

- Generally, the bonus paid to the worker is 75% of the wages for time saved. The remaining 25% goes to the foreman. The working of the Bedeaux plan is explained with the help of the following illustration:

Standard time (S) = 300 Bs (5 hours)

Actual time (T) = 240 Bs (4hours)

Rate of wages (R ) = Rs. 6 per hour

60 Bs = 1 hour

Value of time saved

=

= Rs.6.00

Total wages (W) = S x R + 75% of value of time saved

= Rs. 34.50

The merits of Bedeaux plan are as under:

- In industrial units where conditions are standardized and where facilities exists for measuring the task and the output with a fair degree of accuracy through time and method studies Bedeaux plan can be useful as a bases for scientific production control particularly for purpose of estimating, planning and controlling machine capacities and for determining standard production costs.

- The Bedeaux premium plan is mostly used in those units where the performance by individuals machines or workers has to be constantly watched and kept under control by comparing the number of B’s actually produced with the number of B’s standard.

- Minimum wages are guaranteed to the workers, even if the are not able to complete their job within the standard time.

- Since 25% of the wages for time saved goes to the foreman, he is motivated to get higher productivity from the workers.

The demerits of this plan are as under:

- Much clerical work is involved in maintaining record and in preparing wages accounts etc. So in this respect, Bedeaux plan is costlier than many other incentive plans .

- Though the earnings of a worker increase as his efficiency rises, the rate of increment in the earning is less than in a straight piece rate plan.

- Some employers considers that this plan is not easily intelligible to many workers.

- Like all other incentive plan, the success of this plan depends on the reaction of the workers to the plan. Therefore, before adoption this plan may need a certain amount of modification.

Taylor’s Differential Piece Rate System

Tailor’s plan is based on piece rate method and does not guarantee a minimum time wage. Under this plan, standard output per hour or per day of worker is fixed. There are two piece rates ; one for those who do not attain the standards fixed and the other for those who attain or exceed the standard. In the second case, the piece rate is higher. This system provides an incentive to the efficient worker and at the same time penalises the inefficient ones. Let us suppose that the standard output per worker has been fixed at 8 units per day and the rate per unit for this standard output or above is Rs.6 per unit. The worker producing 7 units will get Rs.37.50 and the one producing 8 units will get Rs.48. Thus, the first worker is penalised at the rate of Rs.0.50 per unit if he does not achieve the target output.

The benefits of Taylor’s plan are as follows:

- The system not only provides the incentive to efficient workers but also at the same time penalises the inefficient ones. An efficient worker gets full piece rate per unit of production and an inefficient worker (i.e., whose output is less than standard output) is paid at a lower rate per unit.

- There is increase in production because every worker tries to increase his productivity in order to get higher piece rate.

- It is simple and easy to understand by the workers.

The drawbacks of Taylor’s plan are as follows:

- Minimum wages are not assured to the workers. So it is vehemently opposed by the Workers.

- The existence of lower piece rate in Taylor’s plan does not act as incentive force, but is a sort of punishment to those who produce below the standard output.

- This plan fails to attract workers who are accustomed to receiving time rate wages or piece rate wages back by guarantied wage.

On the whole, the scheme is very harsh for those whose productivity is less than the standard laid down. This plan may bring about disunity among the workers because it divides them into two groups, viz., efficient and inefficient, the inefficient workers may feel jealous of efficient ones as the letter get wages at higher rates.

Merrick’s Multiple Piece Rate Plan

M. Dwight V. Merrick realized that it is unreasonable and unrealistic to classify all workers into two categories only, viz., workers of high efficiency and those who lower efficiency because there are various degrees of efficiency and there are many workers who actually work in their effort to produce more and for their own progress. These persons deserve to be encouraged. Merrick, therefore, introduced three piece rates and made the lowest piece rate equal to the ordinary piece rate which became the ‘Basic Piece Rate’.

The rates introduced by Merrick are usually as follow:

( % of task) | Piece Rate wage |

1. less than 83% | Basic Piece Rate |

2. From 83% to 100% | 110 % of Basic Piece Rate |

3. Over 100% | 120% of Basic Piece Rate |

To the workers who are potentially high producer, Merrick plan is good incentive system. It seems reasonable to pay production bonus at 110% of the basic piece rate to the workers when they reach 83% task because many workers should be able to reach 83 % task with a little extra effort. When they do so, they will be encouraged to reach the 100% task

By introducing the basic piece rate for low output, Merrick removed the punitive wage rate originated by Taylor. In fact, Merrick’s plan is only a modified form of Taylor’s plan. Like Taylor’s plan, Merrick’s plan also does not guarantee minimum wages for the workers. Another drawback of the system is the existence of a wide gap in slabs. As is obvious from the plan, all workers producing 1% to 82% of the standard output are considered as sub-standard workers and are paid the same piece rate.

Gantt’s Task and Bonus Wage Plan-

It was developed by Henry L. Gantt, a close associate of F.W. Taylor. Under it, standard time for every task is fixed through time and motion study. Minimum time wage is guaranteed to all workers. A worker who fails to complete the task within the standard time receives wages for actual time spent at the specified rate. Workers who achieve or exceed the standard get extra bonus varying between 20% to 50% of the hourly rate for the time allowed for the task. Suppose, the standard time fixed for the job 8 hours and the time rate is Rs 10 per hour and the rate of bonus is 25 per cent. A worker who completes the task in 10 hours he will be paid Rs. 80( 8 * Rs. 10) only. On the other hand, the worker who completes the task in 6 hours will receive Rs. 100 (Rs. 80 + 25 % of Rs. 80). Therefore, the actual rate comes out to be Rs.100 / 6 =Rs. 16.67 per hour.

Under this method, minimum wage is assured to all workers, wages increases progressively with increase in efficiency, and at the same time inefficient workers are not penalized severally.

Merits

- Minimum wages to every worker.

- Incentive for the efficient workers.

- Motivates the employees to increase their efficiency

Group Incentive Plans

Under these plans, bonus is calculated for a group of workers and the total amount is distributed among the group members on one of the following bases:

- If the group members possess similar skills and abilities, group bonus may be distributed among them on an equal basis; or

- If the group members have different basic rates of wages, the bonus may be distributed in proportion to the basic rates as under priestman’s output bonus plan; or

- Group members may be paid bonus on a specified percentage basis.

Such percentage may be determined on the basis of skill, experience and basis rate of pay of each individual worker.

These methods are suitable in the following situations:

- Where it is not possible to measure the performance of each individual employee:

- Where the workers constituting a group possess similar skills, abilities, experience: and

- Where the finished product is the result of collective efforts of group members.

Priestman’s Plan

- Under this plan productivity of the group as a whole is the starting point. Standard output is laid down for the group. However, a minimum wage is assured to each group member. The group members become entitled to the bonus if their output exceeds the standard. The bonus is paid in proportion to the excess of actual output over the standard output. For example, if the actual production is 20 per cent higher than the standard output, the wages of each group member will rise by 20 per cent. The additional wage of each member is his bonus.

- The main benefit of Priestman’s Plan is that it brings about a team spirit among the group members. This scheme can be successful only if the number of workers in the group is small. However, as no distinction is made between efficient and inefficient workers, no regard is paid to efficiency of the individual.

Gain Sharing Plan

Towne devised this plan. Under this plan, half of the savings in labor cost as a result of output in excess of the standard is distributed among workers and foreman and bonus is paid half yearly. The percentage of the foreman is fixed in advance.

Goal Sharing Plan or Work Team’s Results

It rewards employees for meeting specific goals in terms of quality, service and job performance e.g., an employee may be paid Rs. 20 extra for each one per cent improvement over baseline (minimum performance). Suppose the baseline is 90% and the group achieves 93% performance, this would mean each group member would receive Rs. 60 bonus based on group performance.

Methods

Method # 1. Time Rate System

Time rate system is the simplest and oldest method of wage payment. According to this system, the workers are paid in accordance with the time spent on the job. The time may be on hourly, daily, weekly, fortnightly or monthly basis. The work or production done by an employee is not taken into consideration.

For example,

If the worker is paid at the rate of Rs.20 per hour and he spends 50 hours during a week, the weekly payment is:

Weekly wages = (Number of hours worked during the week) x (Rate per hours) = 50 x 20 = Rs.1000 per week.

Advantages

- This method of wage payment is very simple. The workers will not find any difficulty in calculating the wages.

- This method is acceptable to trade unions because it does not distinguish between workers on the basis of their performance.

- The quality of goods will be better as workers are assured of wages on time basis.

- This system is good for the beginners because they may not be able to reach a particular level of production in the beginning.

- There will be less wastage, as workers will not be in a hurry to push through production.

Disadvantages

- This method does not distinguish between efficient and inefficient workers. The payment of wages is related to time and not output. Thus, the method gives no incentive for producing more.

- There will be wastage of time, as the workers are not following a target of production.

- Because wages are not related to output, employees find it difficult in determining labour cost per unit.

- Work needs supervision. Thus, cost of supervision increases.

Method 2. Piece Rate System

Piece rate system is a system in which wages are paid in accordance with the number of units of work produced. This is independent of time spent on the job. A fixed rate of wage is paid for each piece of unit produced.

For example,

If a worker produces 100 pieces per day and he is paid at the rate of Rs.1.2 per piece, the daily wage is 100 x 1.2 = Rs.120.

Advantages

- This system is simple in working and the workers can easily calculate their wages.

- This system helps in distinguishing efficient and inefficient workers.

- Strict supervision is not required in this system.

- This system is fair to employee and employer both.

- There will be no dispute for wages, as workers will be rewarded satisfactory for their work.

Disadvantages

- This system does not guarantee a fixed minimum wage to a worker.

- The quality of goods will be poor as workers try to speed up their work in order to produce more.

- There will be increase in wastage of materials.

- Workers intentionally ignore safety rules, inviting accidents.

- Workers neglect their health in order to put their maximum efforts.

- The wages of beginners will be less, as their output cannot be equal to the experienced workers.

Method 3. Combination of Time and Piece Rate System

In this system, both time and product are taken into consideration. The minimum weekly wages are fixed for every worker, which are to be paid irrespective of his output during the week, provided he has worked for full working hours required in a week. The wages for the period of his absence are deducted from the total amount of his wages.

The piece rate system is also combined with time rate system as follows:

- A job card of each worker is maintained which clearly shows the number of jobs completed by the worker during a week.

- Payment for each job is fixed in advance.

- If the piece rate wages earned by the worker are more than time rate wages, the balance is paid to the worker.

- On the other hand, if piece rate wages are less than time rate wages, then the worker will have to compensate the same by making more pieces during next week.

Advantages

- This system provides incentives to workers to produce more.

- It is simple in its working and the workers can easily calculate their wages.

Disadvantages

- It needs check on quality.

- It needs careful piece rate fixing.

- The entire benefit of extra payment goes to worker.

|

106 videos|173 docs|18 tests

|

FAQs on Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting - Cost Accounting - B Com

| 1. What are incentive plans in labor cost accounting? |  |

| 2. What are the different types of incentive plans? | |

| 3. How do incentive plans help control labor costs? | |

| 4. How are incentive plans beneficial for employees? | |

| 5. What factors should be considered when designing an effective incentive plan? | |

|

7.5K Views |

|

4.79/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for B Com exam

|

|

Free

,Previous Year Questions with Solutions

,Methods of Wage Payment and Incentive Plans - Labour Cost

,mock tests for examination

,Methods of Wage Payment and Incentive Plans - Labour Cost

,Methods of Wage Payment and Incentive Plans - Labour Cost

,Cost Accounting | Cost Accounting - B Com

,Important questions

,Cost Accounting | Cost Accounting - B Com

,Objective type Questions

,Sample Paper

,study material

,MCQs

,Summary

,Semester Notes

,practice quizzes

,video lectures

,past year papers

,Viva Questions

,Cost Accounting | Cost Accounting - B Com

,shortcuts and tricks

,ppt

,Extra Questions

,Exam

;

Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting Free PDF Download

Importance of Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting

Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting Notes

Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting B Com Questions

Study Methods of Wage Payment and Incentive Plans - Labour Cost, Cost Accounting on the App

|

© EduRev

|

Education Revolution

|

|