ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1 - CA Foundation PDF Download

| Table of contents |

|

| Introduction |

|

| Meaning of Accounting |

|

| Evolution of Accounting as a Social Science |

|

| Objectives of Accounting |

|

| Functions of Accounting |

|

| Book-Keeping |

|

Introduction

- Every individual performs some kind of economic activity. A salaried person gets salary and spends to buy provisions and clothing, for children’s education, construction of house, etc.

- A sports club formed by a group of individuals, a business run by an individual or a group of individuals, a local authority like Calcutta Municipal Corporation, Delhi Development Authority, Governments, either Central or State, all are carrying some kind of economic activities.

- Not necessarily all the economic activities are run for any individual benefit; such economic activities may create social benefit i.e. benefit for the public, at large.

- Anyway such economic activities are performed through ‘transactions and events’. Transaction is used to mean ‘a business, performance of an act, an agreement’ while event is used to mean ‘a happening, as a consequence of transaction(s), a result.’

Example:

An individual invests  2,00,000 for running a stationery business. On 1st January, he purchases goods for 1,15,000 and sells for 1,47,000 during the month of January. He pays shop rent for the month 5,000 and finds that still he has goods worth 15,000 in hand. The individual performs an economic activity. He carries on a few transactions and encounters with some events. Is it not logical that he will want to know the result of his activity?

2,00,000 for running a stationery business. On 1st January, he purchases goods for 1,15,000 and sells for 1,47,000 during the month of January. He pays shop rent for the month 5,000 and finds that still he has goods worth 15,000 in hand. The individual performs an economic activity. He carries on a few transactions and encounters with some events. Is it not logical that he will want to know the result of his activity?

We see that the individual, who runs the stationery business, earns a surplus of 42,000.

Earning of 42,000 surplus is an event; also having the inventories in hand is another event, while purchase and sale of goods, investment of money and payment of rent are transactions.

Similarly, a municipal corporation got government grant 500 lakhs for adult education; it spent 250 lakhs for purchasing literacy kits, paid 200 lakhs to the tutors and is left with a balance of 50 lakhs. These are also transactions and events. Similarly, the Central Government raised money through taxes, paid salaries to the employees, and spent on various developmental activities. Whenever receipts of the Government are more than expenses it has surplus, but if expenses are more than receipts it runs in deficit. Here raising money through various sources can be termed as transaction and surplus or deficit at the end of the accounting year can be termed as an event.

So, everybody wants to keep records of all transactions and events and to have adequate information about the economic activity as an aid to decision-making. Accounting discipline has been developed to serve this purpose as it deals with the measurement of economic activities involving inflow and outflow of economic resources, which helps to develop useful information for decision-making process.

Accounting has universal application for recording transactions and events and presenting suitable information to aid decision-making regarding any type of economic activity ranging from a family function to functions of the national government. But hereinafter we shall concentrate only on business activities and their accounting because the objective of this study material is to provide a basic understanding on accounting for business activities. Nevertheless, it will give adequate knowledge to think coherently of accounting as a field of study for universal application.

The growth of accounting discipline is closely associated with the development of the business world. Thus, to understand accounting as a field of study for universal application, it is best identified with recording of business transactions and communication of financial information about business enterprise to facilitate decision-making. The aim of accounting is to meet the information needs of the rational and sound decision-makers, and thus, called the language of business.

Meaning of Accounting

- The Committee on Terminology set up by the American Institute of Certified Public Accountants formulated the following definition of accounting in 1961: “Accounting is the art of recording, classifying, and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of a financial character, and interpreting the result thereof.”

- As per this definition, accounting is simply an art of record keeping. The process of accounting starts by first identifying the events and transactions which are of financial character and then be recorded in the books of account. This recording is done in Journal or subsidiary books, also known as primary books.

- Every good record keeping system includes suitable classification of transactions and events as well as their summarization for ready reference. After the transactions and events are recorded, they are transferred to secondary books i.e. Ledger.

- In ledger transactions and events are classified in terms of income, expense, assets and liabilities according to their characteristics and summarized in profit & loss account and balance sheet.

- Essentially the transactions and events are to be measured in terms of money. Measurement in terms of money means measuring at the ruling currency of a country, for example, rupee in India, dollar in U.S.A. and like.

- The transactions and events must have at least in part, financial characteristics.

Example: The inauguration of a new branch of a bank is an event without having financial character, while the business disposed of by the branch is an event having financial character. - Accounting also interprets the recorded, classified and summarized transactions and events.

- However, the dimension of accounting is much broader than that described in the above definition.

- According to the above definition, accounting ends with interpretation of the results of the financial transactions and events but in the modern world with the diversification of management and ownership, globalization of business and society gaining more interest in the functioning of the enterprises, the importance of communicating the accounting results has increased.

- Therefore, this requirement of communicating and motivating informed judgement has also become the part of accounting as defined in the widely accepted definition of accounting, given by the American Accounting Association in 1966 which treated accounting as “The process of identifying, measuring and communicating economic information to permit informed judgments and decisions by the users of accounts.”

- In 1970, the Accounting Principles Board (APB) of American Institute of Certified Public Accountants (AICPA) enumerated the functions of accounting as follows: “The function of accounting is to provide quantitative information, primarily of financial nature, about economic entities, that is needed to be useful in making economic decisions.” Thus, accounting may be defined as the process of recording, classifying, summarizing, analyzing and interpreting the financial transactions and communicating the results thereof to the persons interested in such information.

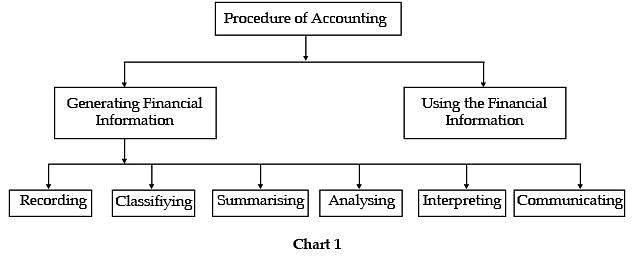

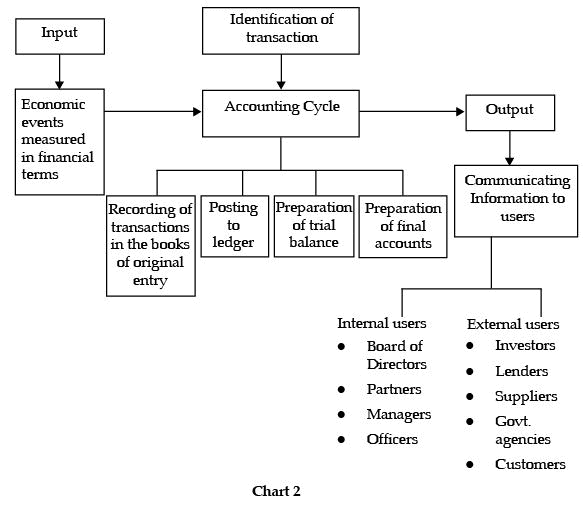

Procedural Aspects of Accounting

On the basis of the above definitions, procedure of accounting can be basically divided into two parts:

(i) Generating financial information.

(ii) Using the financial information.

The procedural aspects of accounting can be explained with the help of the following chart:

Generating Financial Information

- Recording: This is the basic function of accounting. All business transactions of a financial character, as evidenced by some documents such as sales bill, pass book, salary slip etc. are recorded in the books of account. Recording is done in a book called “Journal.” This book may further be divided into several subsidiary books according to the nature and size of the business.

- Classifying: Classification is concerned with the systematic analysis of the recorded data, with a view to group transactions or entries of one nature at one place so as to put information in compact and usable form. The book containing classified information is called “Ledger”. This book contains on different pages, individual account heads under which, all financial transactions of similar nature are collected. For example, there may be separate account heads for Salaries, Rent, Printing and Stationeries, Advertisement etc. All expenses under these heads, after being recorded in the Journal, will be classified under separate heads in the Ledger. This will help in finding out the total expenditure incurred under each of the above heads.

- Summarizing: It is concerned with the preparation and presentation of the classified data in a manner useful to the internal as well as the external users of financial statements.

This process leads to the preparation of the following financial statements:

(a) Trial Balance

(b) Profit and Loss Account

(c) Balance Sheet

(d) Cash-flow Statement - Analyzing: The term ‘Analysis’ means methodical classification of the data given in the financial statements. The figures given in the financial statements will not help anyone unless they are in a simplified form. For example, all items relating to fixed assets are put at one place while all items relating to current assets are put at another place. It is concerned with the establishment of relationship between the items of the Profit and Loss Account and Balance Sheet i.e. it provides the basis for interpretation.

- Interpreting: This is the final function of accounting. It is concerned with explaining the meaning and significance of the relationship as established by the analysis of accounting data. The recorded financial data is analyzed and interpreted in a manner that will enable the end users to make a meaningful judgement about the financial condition and profitability of the business operations. The financial statement should explain not only what had happened but also why it happened and what is likely to happen under specified conditions.

- Communicating: It is concerned with the transmission of summarized, analyzed and interpreted information to the end-users to enable them to make rational decisions. This is done through preparation and distribution of accounting reports, which include besides the usual profit and loss account and the balance sheet, additional information in the form of accounting ratios, graphs, diagrams, fund flow statements etc. Students will learn this aspect of financial statements in the later stages of the Chartered Accountancy Course. The first two procedural stages of the process of generating financial information along with the preparation of trial balance are covered under book-keeping while the preparation of financial statements and its analysis, interpretation and also its communication to the various users are considered as accounting stages.

Using the Financial Information

- There are certain users of accounts. Earlier it was viewed that accounting is meant for the proprietor or owner of the business, but changing social relationships diluted the earlier thinking.

- It is now believed that besides the owner or the management of the business enterprise, users of accounts include the investors, employees, lenders, suppliers, customers, government and other agencies and the public at large.

- Accounting provides the art of presenting information systematically to the users of accounts. Accounting data is more useful if it stresses economic substance rather than technical form. Information is useless and meaningless unless it is relevant and material to a user’s decision. The information should also be free of any biases. The users should understand not only the financial results depicted by the accounting figures, but also should be able to assess its reliability and compare it with information about alternative opportunities and the past experience.

- The owners or the management of the enterprise, commonly known as internal users, use the accounting information in an analytical manner to take the valuable decisions for the business. So the information served to them is presented in a manner different to the information presented to the external users. Even the small details which can affect the internal working of the business are given in the management report while financial statements presented to the external users contains key information regarding assets, liabilities and capital which are summarized in a logical manner that helps them in their respective decision-making.

The entire procedure of accounting can be explained with the help of chart given below:

Evolution of Accounting as a Social Science

Social Science study man as a member of society; they concern about social processes and the results and consequences of social relationships. The usefulness of accounting to society as a whole is the fundamental criterion to treat it as a social science. Although individuals may benefit from the availability of accounting information, the accounting system generates information for social good. It serves social purposes, it contributes for social progress; also it is being adapted to keep pace with social progress. So, accounting is treated as a social science.

- In its oldest form accounting aided the stewards to discharge their stewardship function. The wealthy men employed stewards(a person employed to look after one's property); the stewards in turn rendered an account periodically of their stewardship.

- This ‘Stewardship Accounting’ was the root of financial accounting system. The presently followed system of double-entry book-keeping has been developed only in the 15th Century. However, historians found records of debit and credit dating back to the 12th Century.

- Although double-entry system was followed, ‘stewardship accounting’ served the purpose of businessmen and wealthy persons at that time. In India too, stewardship accounting was prevalent till the emergence of large-scale enterprises in the form of public limited companies.

- In the second phase, the idea of financial accounting emerged with the concept of joint stock company and divorce of ownership from the management.

- To safeguard the interest of the shareholders and investors, disclosure of financial statements (mainly, profit and loss account and balance sheet) and other accounting information was molded by law. Financial statements give periodic performance report by way of profit and loss account and financial position at the end of the period by way of Balance Sheet. It got the legal status due to changing relationships between the owners, economic entity and the managers.

- With the democratization of society, the relationships between the enterprise on the one hand, the investors, employees, managers and governments on the other, have also undergone a sea-change. Also the prospective investors and other business contact groups want to know a lot about the business before entering into transactions.

- Thus, financial accounting emerged as an information system to identify, measure and communicate useful information for informed judgements and decisions by a broad group of users.

- In the third phase, accounting information was generated to aid management decision- making in particular. It contributed a lot to improve the quality of management decisions. This new dimension of accounting is called Management Accounting and it is the development of 20th Century only. It is pervasive enough to cover all spheres of management decisions.

- Lastly, Social Responsibility Accounting is in the formative process, which aims at accounting for the social cost incurred by business as well as the social benefit, created by it.

- It emerges from the growing social awareness about the undesirable by-products of economic activities. While earning profit, an enterprise incurs numerous social costs like pollution, using the resources of society like materials, land, labour etc. To compensate for this social cost, in today’s world, an enterprise is expected to generate some social benefits also like employment opportunities, recreation activities, more choice to customers at reasonable price, better quality products etc.

- Therefore, it is demanded that the accounting system should produce a report measuring the social cost incurred and social benefits generated.

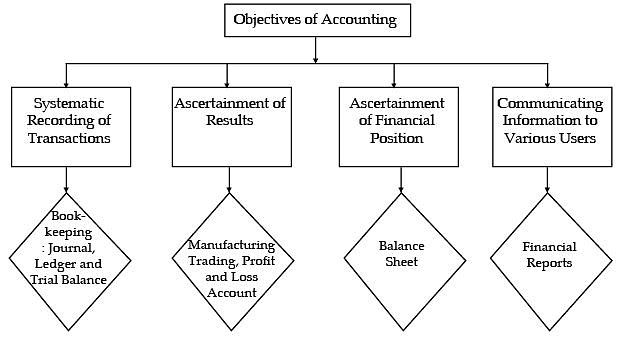

Objectives of Accounting

The objectives of accounting can be given as follows:

- Systematic recording of transactions: Basic objective of accounting is to systematically record the financial aspects of business transactions i.e. book-keeping. These recorded transactions are later on classified and summarized logically for the preparation of financial statements and for their analysis and interpretation.

- Ascertainment of results of above recorded transactions: Accountant prepares profit and loss account to know the results of business operations for a particular period of time. If revenue exceed expenses then it is said that business is running profitably but if expenses exceed revenue then it can be said that business is running under loss. The profit and loss account helps the management and different stakeholders in taking rational decisions.

Example: If business is not proved to be remunerative or profitable, the cause of such a state of affair can be investigated by the management for taking remedial steps. - Ascertainment of the financial position of the business: Businessman is not only interested in knowing the results of the business in terms of profits or loss for a particular period but is also anxious to know that what he owes (liability) to the outsiders and what he owns (assets) on a certain date. To know this, accountant prepares a financial position statement popularly known as Balance Sheet. The balance sheet is a statement of assets and liabilities of the business at a particular point of time and helps in ascertaining the financial health of the business.

- Providing information to the users for rational decision-making: Accounting as a ‘language of business’ communicates the financial results of an enterprise to various stakeholders by means of financial statements. Accounting aims to meet the information needs of the decision-makers and helps them in rational decision-making.

- To know the solvency position: By preparing the balance sheet, management not only reveals what is owned and owed by the enterprise, but also it gives the information regarding concern’s ability to meet its liabilities in the short run (liquidity position) and also in the long-run (solvency position) as and when they fall due.

An overview of objectives of accounting is depicted in the chart given below:

Functions of Accounting

The main functions of accounting are as follows:

- Measurement: Accounting measures past performance of the business entity and depicts its current financial position.

- Forecasting: Accounting helps in forecasting future performance and financial position of the enterprise using past data.

- Decision-making: Accounting provides relevant information to the users of accounts to aid rational decision-making.

- Comparison & Evaluation: Accounting assesses performance achieved in relation to targets and discloses information regarding accounting policies and contingent liabilities which play an important role in predicting, comparing and evaluating the financial results.

- Control: Accounting also identifies weaknesses of the operational system and provides feedbacks regarding effectiveness of measures adopted to check such weaknesses.

- Government Regulation and Taxation: Accounting provides necessary information to the government to exercise control on the entity as well as in collection of tax revenues.

Book-Keeping

- Book-keeping is an activity concerned with the recording of financial data relating to business operations in a significant and orderly manner. It covers procedural aspects of accounting work and embraces record keeping function.

- Obviously book-keeping procedures are governed by the end product, the financial statements.

- In India, the term ‘financial statements’ means Profit and Loss Account and Balance Sheet including Schedules and Notes forming part of Accounts. As discussed earlier, Profit and Loss Account gives result of economic activities for a period and Balance Sheet states the financial position at the end of the period. Book-keeping also requires suitable classification of transactions and events. This is also determined with reference to the requirement of financial statements.

- A book-keeper may be responsible for keeping all the records of a business or only of a minor segment, such as position of the customers’ accounts in a departmental store. A substantial portion of the book-keeper’s work is of a clerical nature and is increasingly being accomplished through the use of a mechanical and electronic devices. Accounting is based on a careful and efficient book-keeping system.

- The essential idea behind maintaining book-keeping records is to show correct position regarding each head of income and expenditure. A business may purchase goods on credit as well as in cash.

Example: When the goods are bought on credit, a record must be kept of the person to whom money is owed. The proprietor of the business may like to know, from time to time, what amount is due on credit purchase and to whom. If proper record is not maintained, it is not possible to get details of the transactions in regard to the expenses. At the end of the accounting period, the proprietor wants to know how much profit has been earned or loss has been incurred during the course of the period. For this lot of information is needed which can be gathered from a proper record of the transactions. - Therefore, in book-keeping, the proper maintenance of books of account is indispensable for any business.

- Book-keeping and preparation of financial statements have legal implications also. Maintenance of books of accounts and the preparation of financial statements of a company are guided by the Companies Act, 1956,* Cooperative society by Co-operative Societies Act, banks and insurance companies by special Acts governing these institutions and so on.

- However, for sole-proprietorship and partnership business, there is no specific legislation regarding maintenance of books of accounts and preparation of financial statements. But, the Income-tax Act, 1961 requires maintenance of books of accounts in some cases.

Objectives of Book-Keeping

- Complete Recording of Transactions: It is concerned with complete and permanent record of all transactions in a systematic and logical manner to show its financial effect on the business.

- Ascertainment of Financial Effect on the Business: It is concerned with the combined effect of all the transactions made during the accounting period upon the financial position of the business as a whole.

FAQs on ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1 - CA Foundation

| 1. What is the meaning of accounting? |  |

| 2. How did accounting evolve as a social science? | |

| 3. What are the objectives of accounting? | |

| 4. What are the functions of accounting? | |

| 5. What is book-keeping? | |

|

49.3K Views |

|

4.83/5 Rating |

|

Dec 28, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

video lectures

,Important questions

,Viva Questions

,ICAI Notes 1.1

,Semester Notes

,Meaning & Scope: Accounting Introduction- 1 - CA Foundation

,Summary

,Meaning & Scope: Accounting Introduction- 1 - CA Foundation

,practice quizzes

,study material

,Extra Questions

,Previous Year Questions with Solutions

,ICAI Notes 1.1

,Sample Paper

,Meaning & Scope: Accounting Introduction- 1 - CA Foundation

,shortcuts and tricks

,ppt

,Free

,MCQs

,Objective type Questions

,ICAI Notes 1.1

,Exam

,past year papers

,mock tests for examination

;

ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1 Free PDF Download

Importance of ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1

ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1

ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1 CA Foundation Questions

Study ICAI Notes 1.1, Meaning & Scope: Accounting Introduction- 1 on the App

|

© EduRev

|

Education Revolution

|

|