ICAI Notes 7.2: Consignment Accounting - 2

Simultaneous Normal Loss and Abnormal Loss

Illustration 17.

Lubrizols Ltd. of Mumbai consigned 1,000 barrels of lubricant oil costing  800 per barrel to Central Oil Co. of Kolkata on 1.1.2013. Lubrizols Ltd. paid 50,000 as freight and insurance. 25 barrels were destroyed on 7.1.2013 in transit. The insurance claim was settled at 15,000 and was paid directly to the consignor.

800 per barrel to Central Oil Co. of Kolkata on 1.1.2013. Lubrizols Ltd. paid 50,000 as freight and insurance. 25 barrels were destroyed on 7.1.2013 in transit. The insurance claim was settled at 15,000 and was paid directly to the consignor.

Central Oil took delivery of the consignment on 19.1.2013 and accepted a bill drawn upon them by Lubrizols Ltd., for 5,00,000 for 3 months. On 31.3.2013 Central Oil reported as follows:

(i) 750 barrels were sold as 1,200 per barrel.

(ii) The other expenses were:

Clearing cha rges Godown Rent Wages Printing, Stationery, Advertisement | ( 11,250 10,000 30,000 20,000 |

25 barrels of oil were lost due to leakage which is considered to be normal loss.

Central Oil Co. is entitled to a commission of 5% on all the sales affected by them. Central Oil Company paid the amount due in respect of the consignment on 31st March itself.

Show the Consignment Account, the Account of Central Oil Co., and the Lost -in-Transit Account as they will appear in the books of Lubrizols Ltd.

Solution:

In the books of Lubrizols Ltd.

Consianmertt to Kolkata Account

| Dr. | Cr. | |||||

Date | Particulars | Amount | Amount | Date | Particulars | Amount (Rs) |

2013 | To Goods sent on C onsig nment A/c |

| 8,00,000 | 2013 | By, Abnormal Loss A/c | 21,250 |

Jan. 1 | (1,000 x Rs 800) |

|

| Jan. 7 | By, Central Oil Co. A/c |

|

Mar.31 | To, Bank A/c - Expenses |

| 50,000 | Mar.31 | Sale proceeds (750 x Rs 1,200) | 9,00,000 |

| To, Central Oil Co. A/c : |

|

|

| By, Stock on | 1,76,842 |

| Clearing charges God own Rent | 11,250 10,000 |

|

| Consignment A/c |

|

| Wages | 30,000 |

|

|

|

|

| Printing | 20,000 | 71,250 |

|

|

|

| To, Central Oil Co. A/c : Commissions @5% |

| 45,000 |

|

|

|

| To, Profit on Consignment A/c: (Transferred to Profit & Loss A/c) |

| 1,31,842 |

|

|

|

|

|

| 10,98,092 |

|

| 10,98,092 |

Central Oil Co. Ltd. Account

Dr. | Cr. | ||||

Date | Particulars | Amount (Rs) | Date | Particulars | Amount (Rs) |

2013 Mar.31 | To, Consignment to Kolkata A/c -Sale Proceeds | 9,00,000 | 2013 Jan,7 Mar.31 | By, Bills Receivable A/c By, Consignment to Kolkata A/c Expenses Commission By, Bank (amount due) | 5,00,000 71,250 45,000 2,83,750 |

|

| 9,00,000 |

|

| 9,00,000 |

Abnormal Loss Account

Dr. Cr. | |||||

Date | Particulars | Amount (Rs) | Date | Particulars | Amount (Rs) |

2013 Jan. 7 | To, Consignment to Kolkata A/c | 21,250 | 2013 Jan.7 Mar.31 | By Bank-Insurance Claim A/c By, Profit and Loss A/c (bal. fig.) | 15,000 6,250 |

21,250 | 21,250 | ||||

Workings:

Valuation of Goods Lost-in-transit and Unsold Stock:

| (Rs) |

Total Cost (1,000 x Rs 800) | 6,00,000 |

Add: Consignor's Expenses | 50,000 |

Value of 1,000 barrels | 8,50,000 |

| 21,250 |

Add: Non-recurring expenses of Consignee | 11,250 |

Value of (1,000-25-25) = 950 Kg. | 8.40,000 |

Invoice Price Method

Generally, the method is used where the consignor does not want to disclose the real price of the goods which are sent to the consignee for a number of reasons. For this purpose, he sends goods at invoice price. It means, certain amount of profit is added to the cost price of goods. Profit/ Loading is calculated after charging certain percentage either on Cost or Sale/ Invoice price.

Naturally, for finalization of accounts, such loading should be adjusted accordingly. Loading is usually calculated on:

(a) Goods Sent on Consignment; (b) Any Abnormal Cost; or (c) Unsold Stock.

Entries to be Recorded in the Books of Consignor

a. For Goods Sent on Consignment -

Note: Other entries are as usual.

Illustration 18.

Mr. X , the consignor , consigned goods to Mr. Y 100 Radio sets valued Rs 50,000. This was made by adding 25% on cost. Mr. X paid Rs 5,000 for freight and insurance. 20 sets are lost - in- transit for which Mr. X received Rs 5,000 from the Insurance company.

Mr. Y received remaining goods in good condition. He incurred Rs 4,000 for freight and miscellaneous expenses and Rs3,000 for godown rent. He sold 60 sets for Rs 50,000. Show the necessary ledger account in the books of Mr. X assuming that Mr. Y was entitled to an ordinary Commission of 10% on sales and 5% Del Credere Commission on sales. He also reported that Rs 1,000 were provide bad .

Solution:

In the books of Mr.X

Consignment Account

Dr. | Cr, | ||

Particulars | Amount | Particulars | Amount |

To, Goods Sent on Consignment A/c | 50,000 | By, Goods Sent on Consignment A/c | 10,000 |

|

| (Loading) (Rs 50,000x100/125) |

|

To, Bank A/c - Expenses | 5,000 | By, Y A/c - Sale Proceeds | 50,000 |

To, Y A/c |

| By, Abnormal Loss A/c | 11,000 |

- Freight and Misc. Expenses | 4,000 |

|

|

- Godown Rent | 3,000 |

|

|

To, Abnormal Loss A/c (Loading) | 2,000 | By, Stock on Consignment A/c | 12,000 |

To, Stock surplus A/c | 2,000 |

|

|

To, YA/c |

|

|

|

- Commission (ordinary) @ 1096 | 5,000 |

|

|

- Del credere Commission @ 5% | 2,500 |

|

|

To, Profit and Loss A/c |

|

|

|

- Profit on Consignment | 9,500 |

|

|

| 83,000 |

| 83,000 |

Y Account

Dr. |

| Cr. | |

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Consignment A/c - Sole proceeds | 50,000 | By, Consignment A/c

| 7,000 7,500 |

|

| By, Balance c/d | 35,500 |

| 50,000 |

| 50,000 |

Abnormal Loss Account

Dr. | Cr. | ||

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Consignment A/c | 11,000 | By, Consignment A/c (Loading) By, Bank A/c - Insurance Claim | 2,000 5,000 |

|

| By, Profit and Loss A/c Loss transferred | 4,000 |

| 11,000 |

| 11,000 |

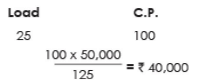

∴ Loading = Rs(50,000 - 40,000) = Rs 10,000

Loading Per Set = Rs 10,000 ÷ 100 = Rs 100

(2) Valuation of Goods Lost - in - transit and Unsold stock

| Rs |

Total Invoice Price | 50,000 |

Add: Consignor's Expenses | 5,000 |

Invoice Price of 100 sets | 55,000 |

Less: Lost In Transit - | 11,000 |

| 44,000 |

Add: Non recurring Expenses of Mr. Y | 4,000 |

1. P. of 50 sets | 48,000 |

∴ For Unsold Stock of f 100 -20 - 60) = 20 sets

= Rs 12,000

= Rs 12,000

(3) Loading on Abnormal Loss = 20 x 100 = 2,000

(4) Stock suspense = 20sets x 100 = 2,000

(5) Since Del Credere Commission is given that will not be any entry for bad debts.

Illustration 19.

On 1.7.2012, Mantu of Chennai consigned goods of the value of 50,000 to Pandey of Patna. This was made by adding 25% on cost. Mantu paid that on 2,500 for freight and 1,500 for insurance. During transit 1/10 th of the goods was totally destroyed by fire and a sum of 2,400 was realised from the insurance company. On arrival of the goods, Pandey paid 1,800 as carriage to godown. During the year ended 30th June 2013, Pandey paid 3,600 for godown rent and 1,900 for selling expenses. 1/9 th of the remaining goods was again destroyed by fire in godown and nothing was recorded from the insurance company. On 1.6.2013, Pandey sold half 1/2 the original goods for 30,000 and changed a commission of 5% on sales. As on 30.6.2013, Pandey sent a bank draft to Mantu for the amount so far due from him.

You are required to prepare the following ledger accounts in the books of Mantu of Chennai for the year ended 30.6.2013.

(a) Consignment to Patna Account; (b) Goods Destroyed by Fire Account; and (c) Personal Account of Pandey.

Solution:

In the books of Mcmfu of Chennai

Consignment to Patna Account

Dr. | Cr. | |||

Particulars |

| Amount | Particulars | Amount |

To Goods Sent on Consignment A/c |

| 50,000 | By, Goods Sent on Consignment A/c. | 10,000 |

To, Bank A/c : |

|

| - Loading |

|

Freight | 2,500 |

|

|

|

Insurance | 1,500 | 4,000 | By, Pandey A/c : | 30,000 |

To, Pandey A/c : |

|

| Sale Proceeds |

|

Carriage Inward | 1,800 |

| By, Goods Destroyed by Fire A/c | 11,000 |

Godown Rent | 3,600 |

| By, Stock on Consignment A/c | 1 6,800 |

Selling Expenses | 1,900 | 7,300 |

|

|

To, Pandey A/c : |

|

|

|

|

Commission (5% on ? 30,000) |

| 1,500 |

|

|

To, Goods Destroyed by Fire A/c : |

| 2,000 |

|

|

Loading |

|

|

|

|

To, Stock Suspense A/c : |

| 3,000 |

|

|

Loading on unsold stock |

|

|

|

|

|

| 67,800 |

| 67,800 |

Goods Destroyed by Fire Account

Dr. | Cr. | ||

Partic ulars | Amount | Particulars | Amount |

To, Consignment to Patna A/c - In transit | 5,400 | By, Consignment to Patna A/c : Loading | 2,000 |

- In God own | 5,600 | By, Bank A/c - Insurance claim | 2,400 |

|

| By, Profit & Loss A/c | 6,600 |

| 11,000 |

| 11,000 |

Pandey Account

Dr. | Cr. | ||

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Consignment to Patna A/c Sale proceeds | 30,000 | By, Consignment to Patna A/c : By, Draft A/c |

1,500 21,200 |

| 30,000 |

| 30,000 |

Valuation of goods destroyed by fire and unsold stock

Particulars | Amount (Rs) |

Total Insurance Claim Add: Consignor's Expenses | 50,000 4,000 |

| 54,000 |

| 5,400 |

Goods received (9/10 th of Rs 54,000) Add: Non- recurring expenses of Pandey | 48,600 1,800 |

Less: Value of goods destroyed by fire in godown | 50,400 5,600 |

(1/9 th of Rs 50,400) |

|

| 44,800 |

∴ Value of unsold stock

Goods sold

∴ Value of unsold stock

Loading on goods destroyed

Loading on unsold stock

Illustration 20.

Usha sent goods costing 75,50,000 on consignment basis to Gayatri on 1st Feb 2012 @ 8.5% commission. Usha spent 8,25,000 on transportation. Gayatri spent 5,25,000 on unloading. Gayatri sold 88% of the goods for 90,00,000, 10% of the goods for 10,00,000 and the balance are taken over by her at 10% below the cost price. She sent a cheque to Usha for the amount due after deducting commission.

Show Consignment to Gayatri Account and Gayatri's Account in the books of Usha.

Solution:

Calculation of sales | Cost (Rs) | Invoice (Rs) |

Goods sent | 75,50,000 |

|

88% of the goods | 66,44,000 | 90,00,000 |

10% of goods | 7,55,000 | 10,00,000 |

Total sales | 73,99,000 | 1,00,00,000 |

Goods taken over by Gayatri | 1,51,000 | 1,35,900 |

There is no closing stock here as all unsold goods were taken over by Gayatri. The commission is payable only on sales to outsiders and not on goods taken over by Gayatri.

Thus, commission is 8.5% on 10,000,000 i.e. 8,50,000

The required ledger Accounts are shown below.

Consignment to Gayatri Account

Dr, | Cr. | ||

Particulars | Amount (Rs) | Particulars | Amount (RS) |

To Goods Sent on Consignment A/c | 75,50,000 | ByGayatri's A/c (sales) | 1,00,00,000 |

To Bank A/c (transportation) | 8,25,000 | By Gayatri's A/c (goods taken over) | 1,35,900 |

To Gayatri's A/c : |

|

|

|

- Unloading charges | 5,25,000 |

|

|

- Commission | 8,50,000 |

|

|

To P & L A/c | 3,85,900 |

|

|

| 1,01,35,900 |

| 1,01,35,900 |

Gayatri's Account

Dr, |

| Cr. | |

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To Consignment A/c | 1,01,35,900 | By Consignment A/c (expenses) | 5,25,000 |

|

| By Consignment A/c (commission) | 8,50,000 |

|

| By Bank A/c | 87,60,900 |

| 1,01,35,900 |

| 1,01,35,900 |

Advance from Consignee as Security Money:

Usually the consignor takes certain some of money as advance by way of cash/draft/bill etc from the consignee against the goods that are sent for sale to the consignee. The so called advance money is automatically adjusted against the total dues in order to determine the net amount payable. If the advance money is not treated as security money, then the entire amount of advance money may be adjusted even if a part of goods are sold. But if the advance money is treated as security money, in that case, the proportionate amount of such advance money will be carried forward as the same is treated to the unsold stock. The entries in the books of both companies and consignor will be:

In The books of Consignor | In fhe books of Consignee |

Cash/ Draft/Bill Receivable A/c Dr, To, Consignee's Personal A/c | Consignor A/c Dr, To, Cash/ Draft/B/P A/c |

Illustration 21.

Ram of Patna consigns to Shyam of Delhi for sale at invoice price or over. Shyam is entitled to a commission @ 5% on invoice price and 25% of any surplus price realized. Ram draws on Shyam at 90 days sight for 80% of the invoice price as security money. Shyam remits the balance of proceeds after sales, deducting his commission by sight draft.

Goods consigned by Ram to Shyam costing 20,900 including freight and were invoiced at 28,400. Sales made by Shyam were 26,760 and goods in his hand unsold at 31st Dec, represented an invoice price of 6,920. ( Original cost including freight 5,220). Sight draft received by Ram from Shyam upto 31st Dec was 6,280. Others were in- transit.

Prepare necessary any Ledger Accounts.

Solution:

In the books of Ram

Consignment to Delhi Account

Dr. Cr. | |||

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Goods Sent on Consignment A/c | 28,400 | By, Goods Sent on Consignment A/c (Loading) Rs (28,400- 20,900) | 7,500 |

To, Y A/c - Commission | 2,394 | By, Shyam A/c - Sale proceeds | 26,760 |

To, Stock Reserve A/c Rs(6,920-5,220) | 1,700 | By, Stock on Consignment A/c | 6,920 |

To, Profit and Loss A/c- Profit on consignment transferred | 8,686 |

|

|

| 41,180 |

| 41,180 |

Shyam Account

Dr. Cr. | |||

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Consignment to Delhi A/c To, Balance c/d (Rs 6,920 x 80%) | 26,760 5,536 | By, Bills Receivable A/c By, Consignment to Delhi A/c By, Draft A/c By, Draft- in- Transit A/c | 22,720

6,280 902 |

32,296 | 32,296 | ||

Goods sent on Consignment Account

Dr. | Cr. | ||

Particulars | Amount (Rs) | Particulars | Amount (Rs) |

To, Consignment to Delhi A/c To, Trading A/c (bal.fig) | 7,500 20,900 | By, Consignment to Delhi A/c | 28,400 |

| 28,400 |

| 28,400 |

Workings:

Calculation of Commission: | Rs |

invoice value of goods | 28,400 |

Less: Unsold stock | 6,920 |

Invoice value of goods sold | 21,480 |

Total sale proceeds | 26,760 |

Less: Invoice value of goods sold | 21,480 |

Surplus price | 5,280 |

Commission ® 5% on Rs 21,480 | 1,074 |

Add: @ 25% on Rs 5,280 | 1,320 |

| 2,394 |

FAQs on ICAI Notes 7.2: Consignment Accounting - 2

| 1. What is consignment accounting? |  |

| 2. What is the difference between consignment and sale? | |

| 3. What is the journal entry for goods sent on consignment? | |

| 4. How is consignment inventory valued in the balance sheet? | |

| 5. What is the consignee's role in consignment accounting? | |