Chapter Notes: Issue and Redemption of Debentures

Introduction

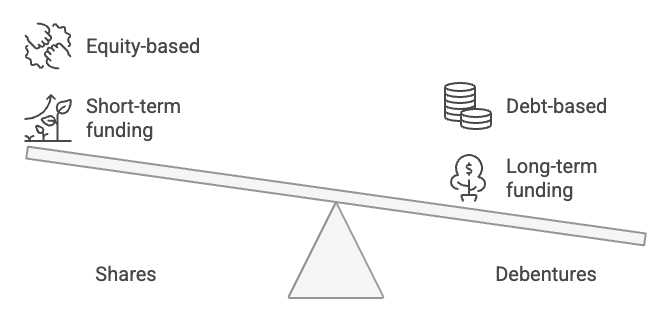

- Companies raise long-term funds not only by issuing shares but also by issuing debentures to meet long-term financial requirements.

- Debentures may be issued by private placement or by a public offer.

- Money raised through debentures is treated as long-term debt in the financial statements.

- This chapter explains the accounting treatment for the issue and redemption of debentures, and related aspects such as types, terms, interest, and reserve requirements.

Debenture: Meaning and Distinction from Shares

Meaning of Debentures:

- The word debenture is derived from the Latin debere meaning "to borrow".

- A debenture is a written instrument issued under a company's common seal which acknowledges a debt and the company's obligation to repay the principal with interest.

- Debentures carry a specified rate of interest payable at stated intervals (commonly half-yearly or yearly).

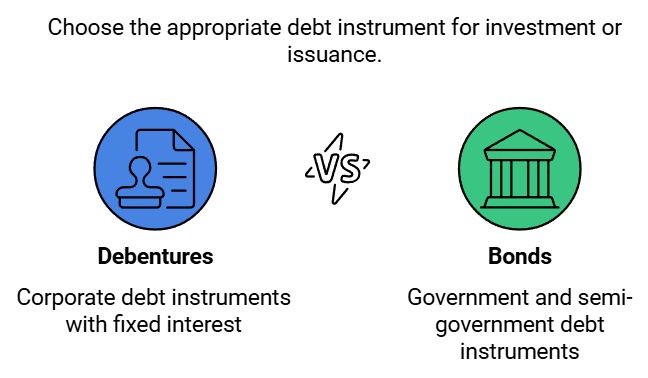

- Under The Companies Act, 2013, the term debentures includes bonds and other securities of a company, whether they create a charge on the assets of the company or not.

Bonds are also instruments acknowledging a debt. Traditionally issued by governments, bonds are now also issued by semi-government and private organisations. The terms debentures and bonds are often used interchangeably in practice.

Distinction between Shares and Debentures

- Ownership: Shares represent ownership in the company; debentures represent a loan to the company (creditor relationship).

- Return: Shareholders receive dividends which depend on profits and are discretionary; debenture holders receive a fixed interest, a charge against profits and payable even when there are no profits.

- Repayment: Share capital is generally not repayable during the life of the company; debentures are usually repayable after a specified period.

- Voting Rights: Shareholders usually have voting rights; debenture holders normally do not.

- Security: Shares are usually unsecured; debentures are commonly secured by a fixed or floating charge on company assets.

- Convertibility: Shares are not convertible into debentures; debentures may be convertible into shares if the terms permit (called convertible debentures).

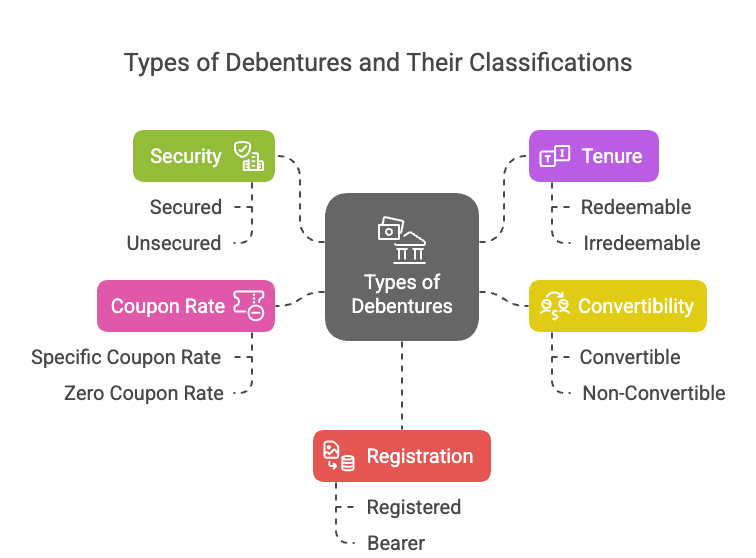

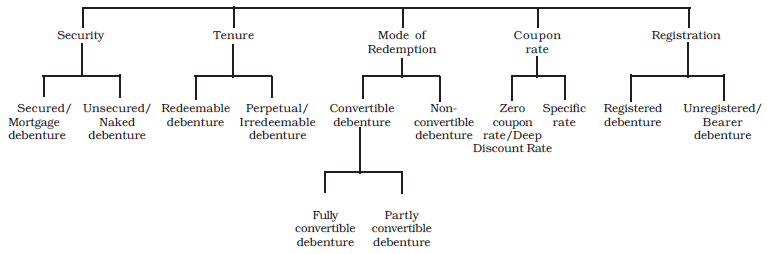

Types of Debentures

A company may issue different kinds of debentures. They can be classified as follows:

From the Point of View of Security

- Secured Debentures: These carry a charge on specified assets of the company to secure payment in case of default.

- Fixed charge - attaches to specific assets (e.g., land, plant) and remains until discharged.

- Floating charge - covers a class of assets (e.g., stock, debtors) which may change over time; it "floats" until crystallised on default.

- Unsecured Debentures (also called naked debentures): No specific charge on assets. They rank with other unsecured creditors.

From the Point of View of Tenure

- Redeemable Debentures: Repayable after a specified period or in instalments during the company's life. Redemption can be at par or at a premium.

- Irredeemable (Perpetual) Debentures: No obligation to redeem during the life of the company; repayable only on winding up or after a very long period.

From the Point of View of Convertibility

- Convertible Debentures: Can be converted into equity shares or other securities, fully or partly, according to the terms of issue.

- Non-convertible Debentures: Cannot be converted into shares; most corporate debentures are non-convertible.

From the Point of View of Coupon Rate

- Specific Coupon Rate Debentures: Carry a stated interest rate (fixed or floating). Floating rates may be linked to a reference rate such as the bank rate.

- Zero Coupon Debentures: Issued without periodic interest; issued at a deep discount and the difference between face value and issue price constitutes the effective interest over the life of the debenture.

From the Point of View of Registration

- Registered Debentures: The company records the details (name, address, holdings) of holders in a register. Transfer requires execution of transfer documents and registration.

- Bearer Debentures: Transferable by delivery. The company does not maintain a register for bearer debentures; interest is paid to the bearer presenting the coupon.

Types of Debenture/Bond

Types of Debenture/BondIssue of Debentures

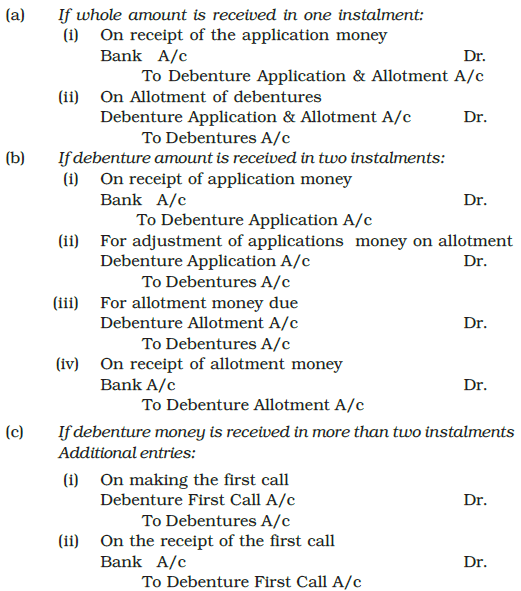

The procedure for issuing debentures is broadly similar to that for issuing shares. A prospectus or offer document states the terms, and applicants apply for debentures. The company may ask for payment in full on application or in instalments (application, allotment, calls). Debentures may be issued at par, at a premium or at a discount. They may also be issued as consideration for non-cash assets or as collateral security.

Issue of Debentures for Cash

- When debentures are issued at par the issue price equals the face value. Appropriate journal entries are made to record application money, allotment, calls and receipt of cash.

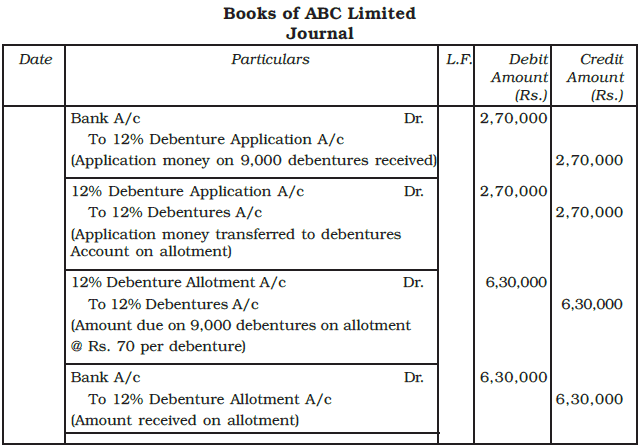

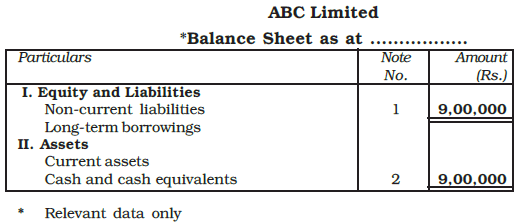

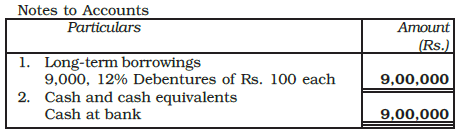

Example: ABC Limited issued 10,000, 12% debentures of Rs. 100 each payable Rs. 30 on application and remaining amount on allotment. The public applied for 9,000 debentures which were fully allotted, and all the relevant allotment money was duly received. Give journal entries in the books of ABC Ltd., and exhibit the relevant information in the balance sheet.

Ans:

Issue of Debentures at a Discount

- Definition: Debentures are issued at a discount when the issue price is less than nominal (face) value. E.g., Rs. 100 debenture issued at Rs. 95: discount Rs. 5.

- Writing off Discount: Discount on issue is a capital loss and is written off in the year of issue. It may be written off from Securities Premium Reserve if available; otherwise from revenue profits.

- Presentation in Balance Sheet: The portion of discount to be written off within 12 months is shown under Other Current Assets, and the portion beyond 12 months under Other Non-Current Assets.

- Regulatory Position: The Companies Act, 2013 does not prohibit issue of debentures at a discount.

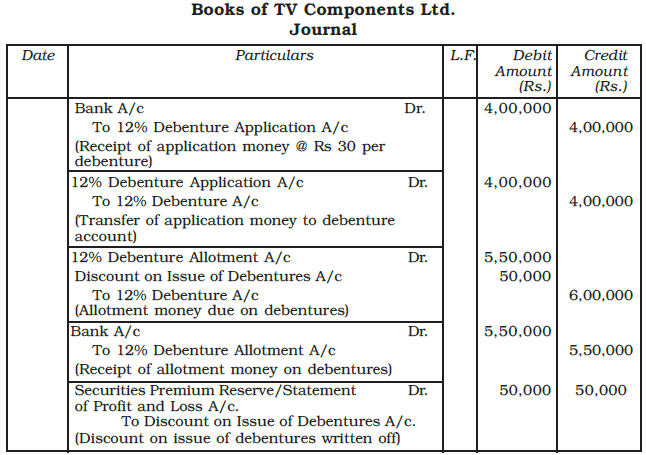

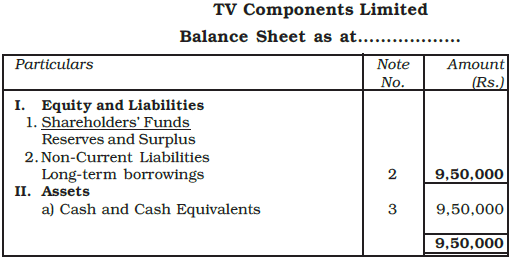

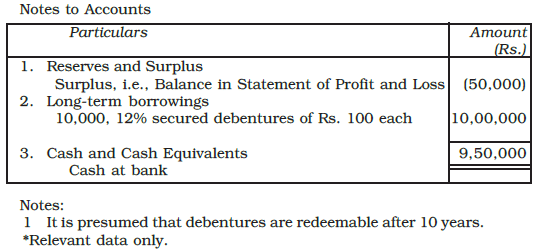

Example: TV Components Ltd., issued 10,000, 12% debentures of Rs. 100 each at a discount of 5% payable as follows:

On application - Rs. 40

On allotment - Rs. 55

Show the journal entries including those for cash, assuming that all the instalments were duly collected. Also show the relevant portion of the balance sheet.

Ans:

Debentures Issued at a Premium

- Debentures are issued at a premium when the issue price exceeds face value. E.g., Rs. 100 debenture issued at Rs. 110: premium Rs. 10.

- Premium received is credited to the Securities Premium Reserve and disclosed under Reserves and Surplus on the liabilities side of the balance sheet.

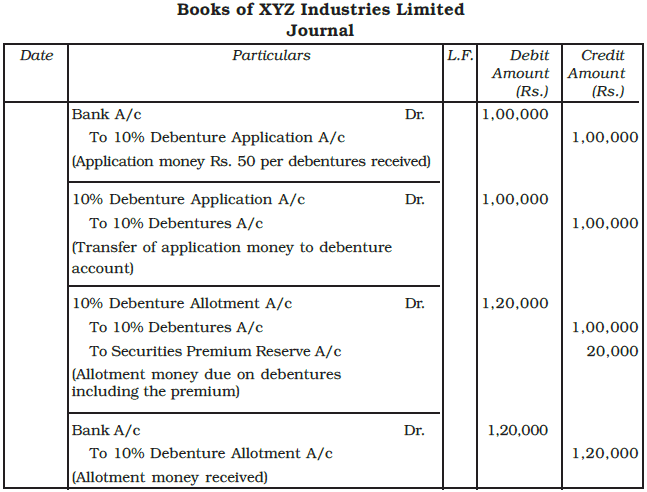

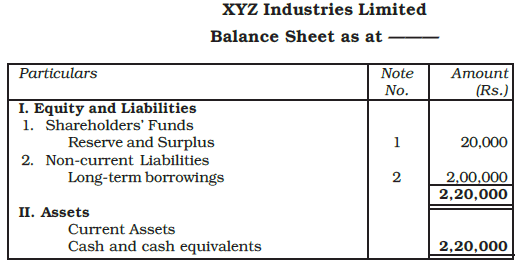

Example: XYZ Industries Ltd., issued 2,000, 10% debentures of Rs. 100 each, at a premium of Rs. 10 per debenture payable as follows:

On application - Rs. 50

On allotment - Rs. 60

The debentures were fully subscribed and all money was duly received. Record the journal entries in the books of a company. Show how the amounts will appear in the balance sheet.

Ans:

Over Subscription

- Over-subscription occurs when applications exceed the number of debentures offered.

- A company cannot allot more debentures than issued. Excess application money may be adjusted against allotment or future calls where appropriate.

- Applicants not allotted any debentures must have their application money refunded.

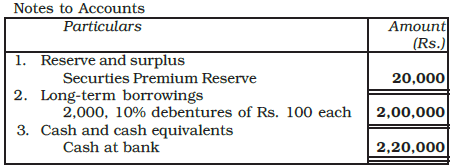

Example: X Limited issued 10,000, 12% debentures of Rs. 100 each payable Rs. 40 on application and Rs. 60 on allotment. The public applied for 14,000 debentures. Applications for 9,000 debentures were accepted in full; applications for 2,000 debentures were allotted 1,000 debentures and the remaining applications were rejected. All money was duly received. Journalise the transactions.

Ans:

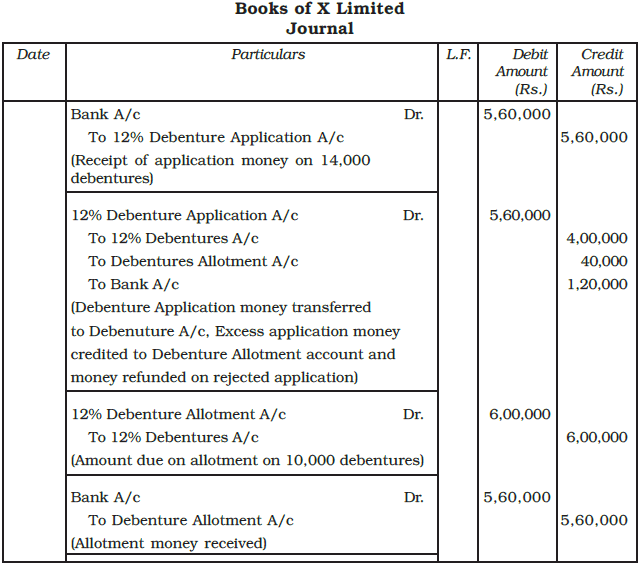

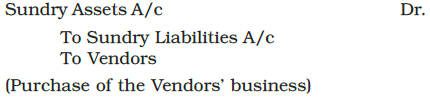

Issue of Debentures for Consideration other than Cash

Sometimes companies acquire assets or entire businesses and pay the vendor by issuing debentures instead of cash. Such debentures may be issued at par, at a premium, or at a discount. The accounting treatment resembles that for shares issued for non-cash consideration: the vendor's account is credited and debentures are shown as consideration payable.

Purchase of Business (Assets and Liabilities)

- When a company acquires a whole business, it takes over both assets and liabilities of the vendor.

- Purchase consideration equals the value of net assets acquired: Net Assets = Assets - Liabilities.

- If debentures are issued as full consideration, the journal entries record assets taken over, liabilities assumed and debentures issued.

- If debentures issued exceed net assets taken over, the excess represents goodwill and is debited accordingly.

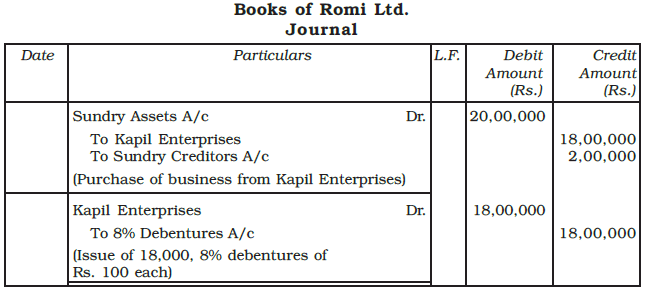

Example: Romi Ltd. acquired assets of Rs. 20 lakh and took over creditors of Rs. 2 lakh from Kapil Enterprises. Romi Ltd., issued 8% debentures of Rs 100 each at par as purchase consideration. Record necessary journal entries in the books of Romi Ltd.

Ans:

- If the consideration by debentures exceeds the net assets acquired when an entire business is taken over, the difference is treated as goodwill and debited in the purchase entries.

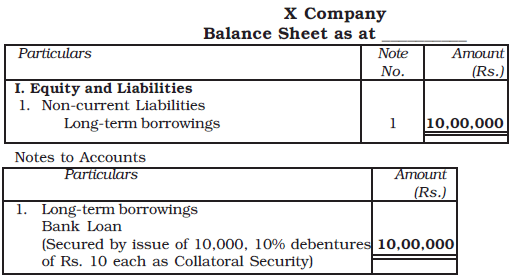

Issue of Debentures as a Collateral Security

- Where a company obtains a loan or overdraft from a bank, the lender may ask for additional protection called collateral security besides primary security (e.g., a mortgage).

- Debentures issued as collateral provide extra security for the lender. If the borrower defaults and primary security sale is insufficient, the lender can realise the collateral debentures to meet the debt.

- Accounting treatment has two common approaches:

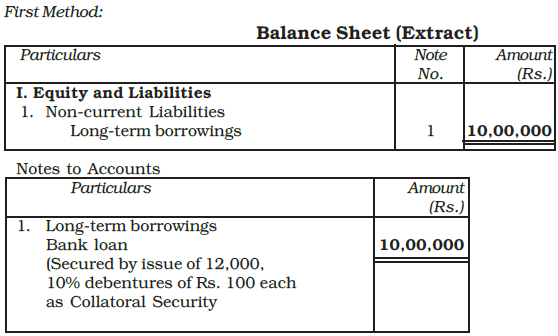

First method: No journal entry is passed on issuing debentures as collateral security because no actual liability arises. A disclosure note is made in the notes to accounts under long-term borrowings specifying that the loan is secured by debentures issued as collateral security.

- Example: If X Company issues 9%, 10,000 debentures of Rs. 100 each as collateral for a bank loan of Rs. 10,00,000, the balance sheet shows a note about the collateral issue without adding an extra liability.

This may be shown in the balance sheet by a note beneath the relevant loan item.

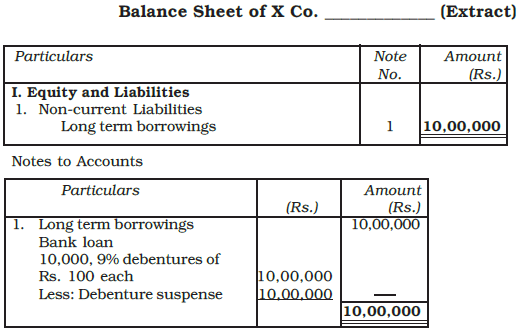

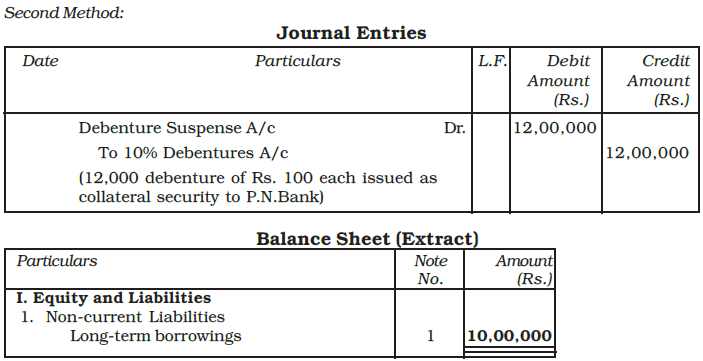

Second method: Record the issue in the books by passing appropriate journal entries-often by crediting a Debenture Suspense Account (or a similar off-balance sheet note) and disclosing it as a deduction from debentures until the collateral is released. On repayment of the loan, the suspense entry is reversed and debentures are cancelled if required.

- At times a Debenture Suspense Account is created to reflect debentures held as collateral; this is shown as a detailed deduction from total debentures in the notes to accounts under long-term borrowings. On repayment of the loan, the suspense entry is reversed.

Example: A company took a loan of Rs. 10,00,000 from Punjab National Bank and issued 10% debentures of Rs. 12,00,000 of Rs. 100 each as a collateral security. Explain how you will deal with the issue of debentures in the books of the company.

Ans:

Terms of Issue of Debentures

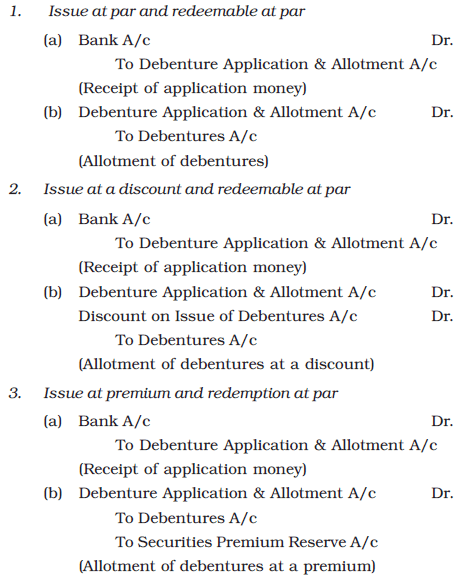

Debenture terms specify redemption conditions. Redemption means repayment of the debenture principal and discharge of the liability. Common combinations of issue and redemption prices include:

- Issued at par and redeemable at par.

- Issued at a discount and redeemable at par.

- Issued at a premium and redeemable at par.

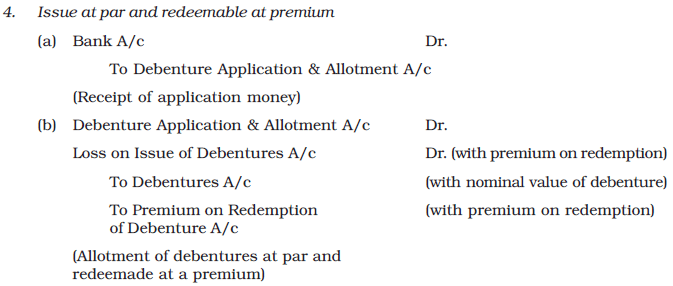

- Issued at par and redeemable at a premium.

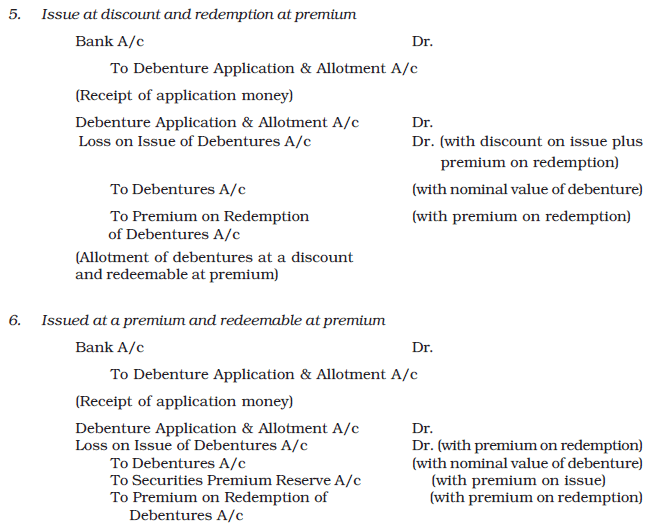

- Issued at a discount and redeemable at a premium.

- Issued at a premium and redeemable at a premium.

Irrespective of the case, the accounting for issue, receipt of money and redemption follows standard journal entries: allotment & receipt, interest recognition and payment, write-off of discount and transfer to/from securities premium as permitted. Typical illustrative journal entry formats for these events are commonly shown in textbooks.

Interest on Debentures

- Obligation to pay interest: Debentures normally carry a fixed rate of interest (e.g., 8%, 10%) payable periodically (often half-yearly or annually) on the face value of debentures.

- Charge against profit: Interest on debentures is a charge against profit and must be paid even if the company has not made a profit.

- TDS (Tax Deducted at Source): Under the Income Tax Act, a company may be required to deduct tax at source when paying interest on debentures beyond specified limits. The deducted tax is deposited with the tax authorities and is adjustable in the hands of debenture holders.

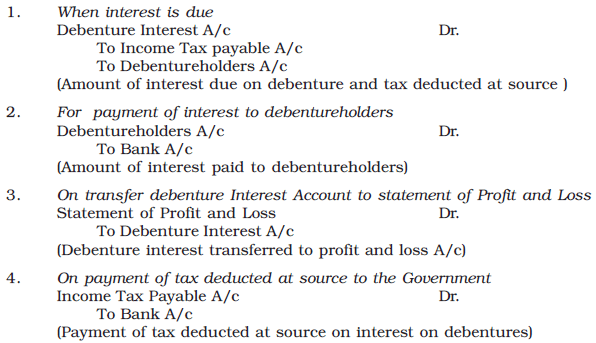

Accounting treatment (typical entries):

The company records interest accrued and paid with entries for Interest on Debentures account (expense), Interest Payable (liability) and Bank (payment). If tax is deducted, a TDS receivable / current asset entry is recorded for the amount to be remitted to tax authorities.

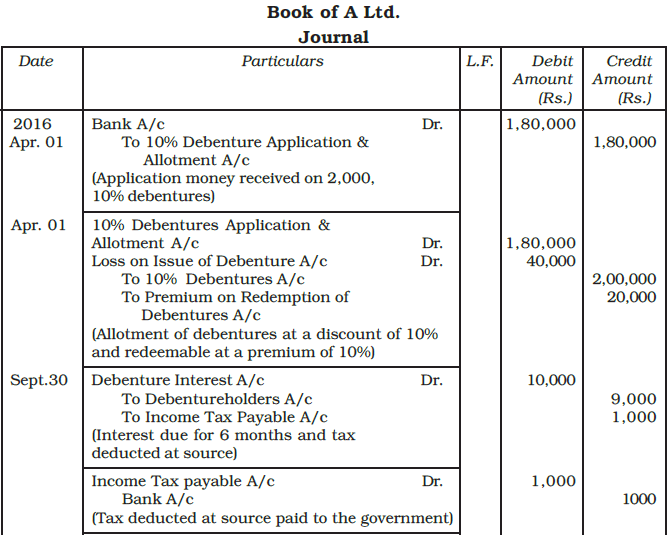

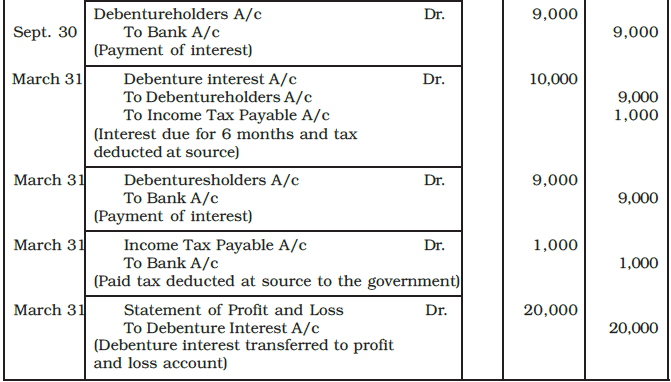

Example: A Ltd., issued 2,000, 10% debentures of Rs. 100 each on April 01, 2016 at a discount of 10% redeemable at a premium of 10%.

Give journal entries relating to the issue of debentures and debenture interest for the period ending March 31, 2017 assuming that interest was paid half yearly on September 30 and March 31 and tax deducted at source is 10%.

Ans:

Writing Off Discount / Loss on Issue of Debentures

- Discount on issue is treated as a capital loss and is written off in the year of issue.

- It may be written off against the Securities Premium Reserve under the provisions of the Companies Act, when available; otherwise it is charged to revenue.

The journal entry for writing off discount is recorded as appropriate in the books (for example: transfer from Securities Premium Reserve or charge to Profit & Loss).

Illustration: On July 01, 2019 a company issued 15,000, 9% debentures of Rs. 100 each at 10% discount. It had a balance of Rs. 1,00,000 in the Securities Premium Reserve. The total discount of Rs. 1,50,000 will be written off in the year ending March 31, 2020 as follows:

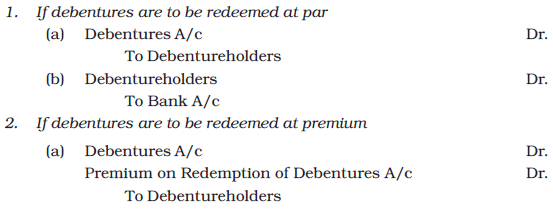

Redemption of Debentures

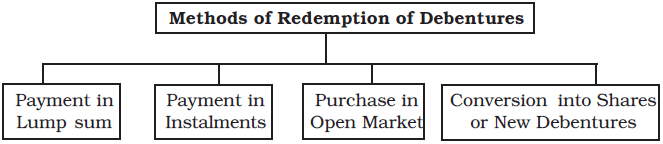

Redemption means repaying debenture holders and discharging the debenture liability as per issue terms. Debentures may be redeemed by:

- Payment in lump sum at maturity.

- Payment in instalments over specified years.

- Purchase in the open market and cancellation.

- Conversion into shares or new debentures (applicable for convertible debentures).

- Payment in Lump Sum: The company pays the full principal to debenture holders on maturity.

- Payment in Instalments: Redemption made in fixed instalments on specified dates. Debentures to be redeemed are usually selected by draw of lots.

- Purchase in Open Market: Company buys debentures from the market and cancels them immediately.

- Conversion into Shares/New Debentures: Convertible debentures may be converted into equity shares or new debentures. The number of shares issued takes into account the actual proceeds originally received for the debentures (i.e., issue price actually realised).

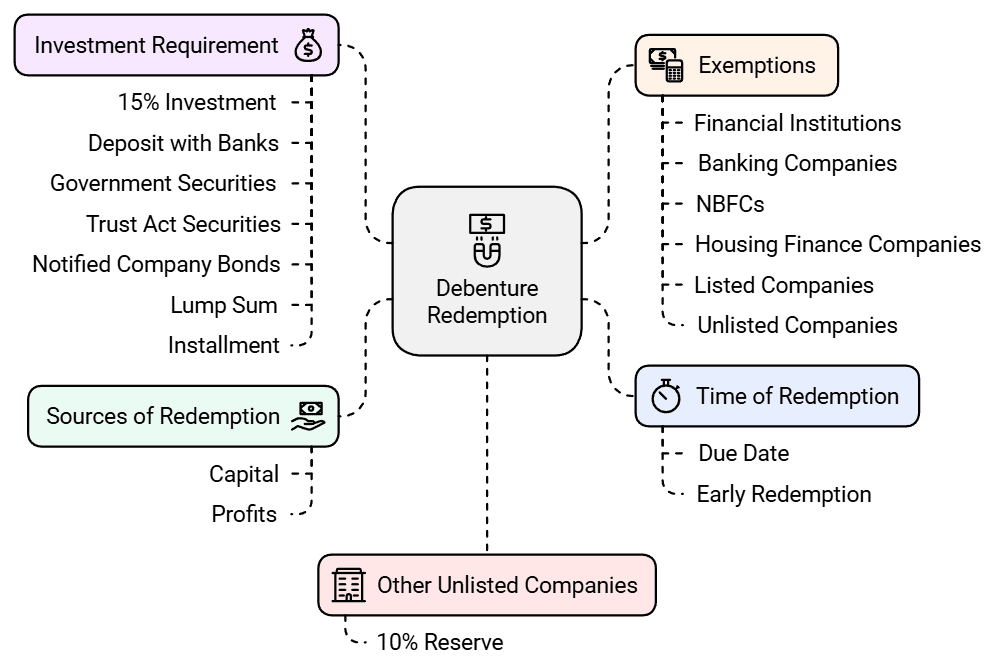

Factors to Consider for Debenture Redemption

- Time of redemption: Debentures are redeemed on the due date; early redemption is allowed only if articles of association permit it.

- Source of redemption: Debentures can be redeemed out of profits or capital subject to Companies Act provisions.

- Exemptions: Certain entities (all-India financial institutions, banking companies, NBFCs, housing finance companies, listed companies and some unlisted companies) are exempt from creating a Debenture Redemption Reserve (DRR) and may redeem out of capital as permitted.

- DRR for other unlisted companies: Such companies must create a DRR equal to 10% of outstanding debentures.

- Investment requirement: Companies must invest or deposit at least 15% of the debentures maturing during the year by April 30 in specified forms (e.g., deposits with scheduled banks, central/state government securities, notified bonds, or specified securities under Indian Trusts Act).

- Lump sum vs instalment redemption: For lump sum redemption 15% of the value must be invested by April 30. For instalment redemption the requirement is carried forward appropriately to meet subsequent year obligations.

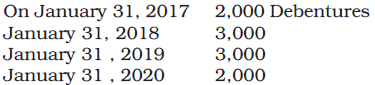

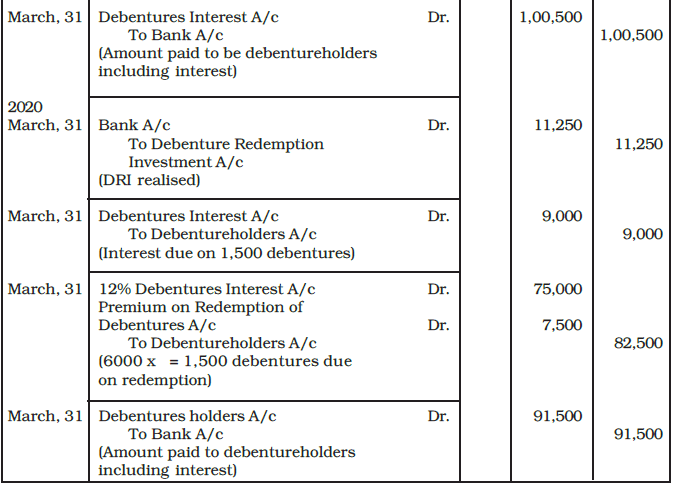

Illustration: Kays Ltd. has 10,000 debentures to be redeemed on various dates. The company must invest 15% of the value maturing in the year by April 30, and follow the schedule of investments and realisations as each redemption date arrives.

- Kays Ltd. invests Rs. 30,000 by April 30, 2016 for redemptions due on 31 Jan 2017 (2,000 debentures).

- By April 30, 2017 an additional Rs. 15,000 is invested so total investments reach Rs. 45,000 (=15% of the next year's redemptions).

- On realisation and subsequent redemptions the invested sums are realised and applied towards payment of debentures as per the redemption schedule.

Redemption by Payment in Lump Sum

When debentures are redeemed in one lump sum at maturity, journal entries reflect transfer of cash to debenture holders and cancellation of debenture capital.

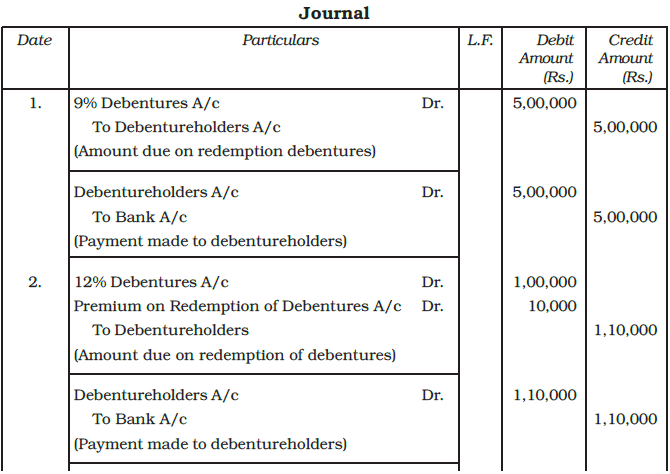

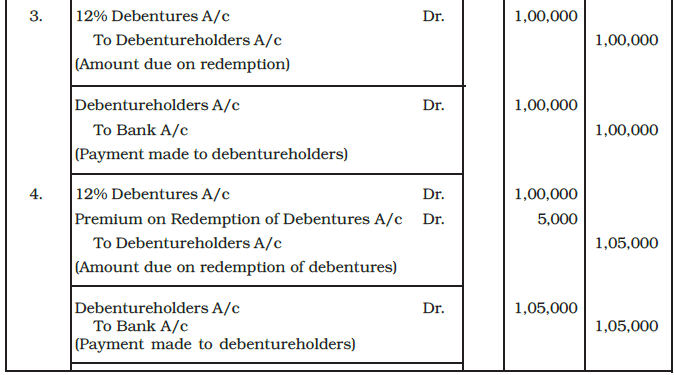

Example: Give the necessary journal entries at the time of redemption of debentures in each of the following cases.

1. X Ltd. issued 5,000, 9% debentures of Rs. 100 each at par and redeemable at par at the end of 5 years out of capital.

2. X Ltd. issued 1,000, 12% debentures of Rs. 100 each at par. These debentures are redeemable at 10% premium at the end of 4 years.

3. X Ltd. issued 12% debentures of the total face value of Rs. 1,00,000 at premium of 5% to be redeemed at par at the end of 4 years.

4. X Ltd. issued Rs. 1,00,000, 12% debentures at a discount of 5% but redeemable at a premium of 5% at the end of 5 years.

Ans:

Redemption by Payment in Instalments

- When debentures are to be redeemed in instalments, debentures to be redeemed in a particular year are usually selected by draw of lots.

- Appropriate journal entries are passed at the time of each instalment redemption, including payment of principal, cancellation of debenture capital and settlement of premium (if any).

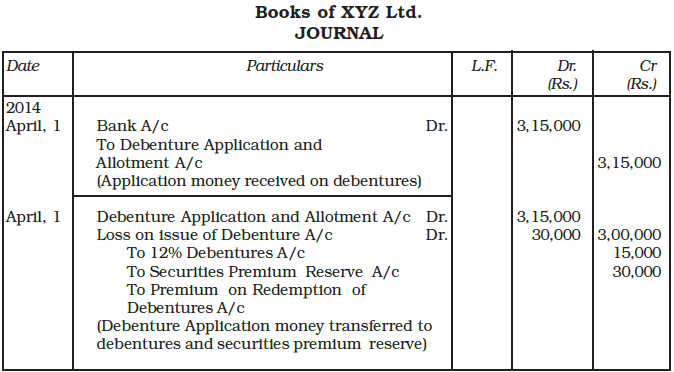

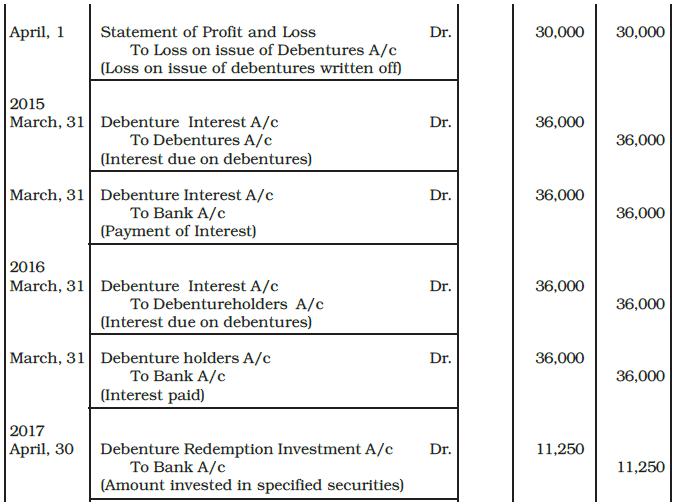

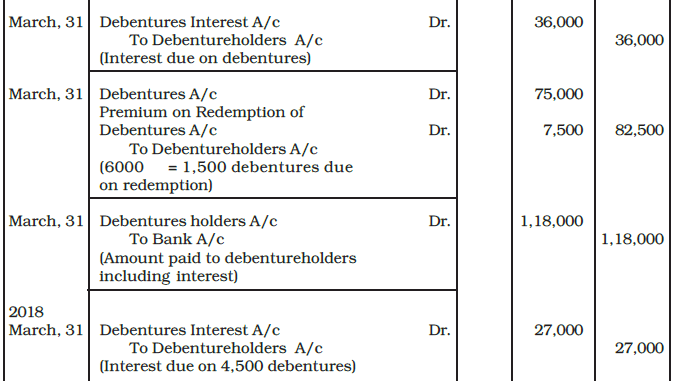

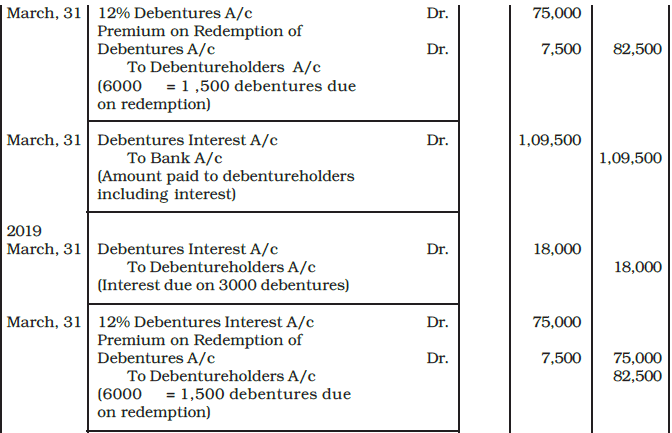

Example: XYZ Ltd. (a listed company) issued 6,000, 12% Debentures of Rs. 50 each at a premium of 5% on April 1, 2014. Interest on these debentures is payable annually on 31st March each year. The debentures are redeemable in four equal instalments at the end of third, fourth, fifth and sixth year at a premium of 10%. The company invested in specified securities as investment for the redemption of debentures.

You are required to pass journal entries at the time of issue and redemption of debentures in the books of the company.

Ans:

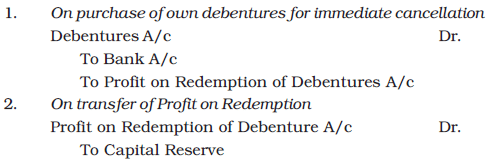

Redemption by Purchase in Open Market

- When a company buys its own debentures from the market and cancels them immediately, it is redemption by purchase in the open market.

- Advantages:

- Convenience - company redeems when surplus funds are available.

- Cost saving - company may buy back at a discount if market price is below face value.

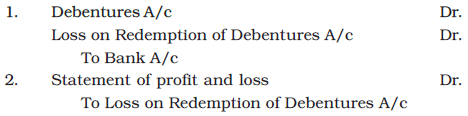

- If purchased at a discount, the difference reduces the debenture liability and is treated as a gain; if purchased above face value, the excess is treated as loss on redemption of debentures.

Typical journal entry when debentures are purchased from the market at a price lower than face value records the purchase and cancellation; if purchased above face value, the excess is debited to Loss on Redemption of Debentures.

- If debentures are bought at a price higher than face value, the extra amount paid is recorded as a loss on redemption of debentures.

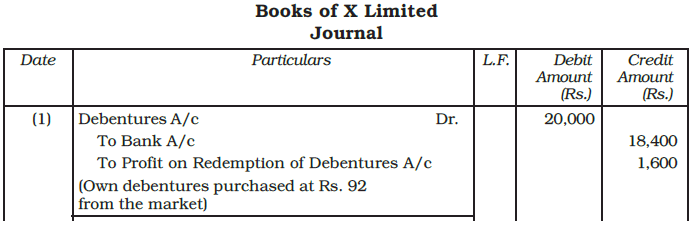

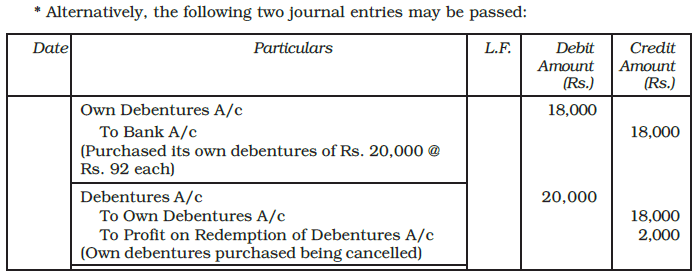

Example: X Ltd. purchased its own debentures of Rs. 100 each of the face value of Rs. 20,000 from the open market for cancellation at Rs. 92. Record necessary journal entries.

Ans:

Redemption by Conversion

- Convertible debentures can be redeemed by converting them into equity shares or new debentures in accordance with the terms of issue.

- Debenture holders may accept conversion if the terms are favourable. The new securities issued on conversion may be at par, discount, or premium depending on terms.

- When calculating the number of shares to be issued on conversion, the computation is based on the actual amount realised on issue of debentures (i.e., issue proceeds after discount, not face value) when debentures were originally issued at a discount.

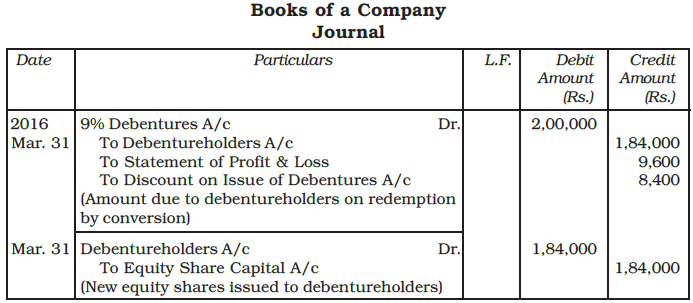

Example: On April 01, 2013, a company made an issue of 10,000, 9% Debentures of Rs. 100 each at Rs. 92 per debenture. The terms of issue provided for the redemption of 2,000 debentures every year starting from March 31, 2016 either by conversion into equity shares of Rs. 20 each or by draw of lot at par at the company's option. On March 31, 2016, company redeemed 2,000, 9% debentures by converting them into Equity shares of Rs. 20 each. Give the necessary Journal entries.

Ans:

FAQs on Chapter Notes: Issue and Redemption of Debentures

| 1. What's the difference between debentures issued at par, premium, and discount? |  |

| 2. How do I record the journal entries when a company redeems debentures before maturity? | |

| 3. What happens to debenture discount when you amortise it over the debenture period? | |

| 4. Why do companies issue debentures at a premium instead of at par value? | |

| 5. Can debenture redemption reserves be used for purposes other than redemption in CBSE Accountancy Class 12? | |