Chapter Notes: Financial Statements of a Company

Introduction

- Once we understand how a company secures its capital, the next step is to study the nature, objectives and types of financial statements that a company is required to prepare, including their contents, formats, uses and limitations.

- Financial statements are the final output of the accounting process. Their preparation is guided by accounting policies, applicable accounting standards, provisions of the Companies Act and fundamental accounting concepts and conventions. They must also comply with relevant legal and regulatory requirements.

- Financial statements summarise monetary information and thus do not capture qualitative aspects such as industrial relations, labour climate or quality of work. They form the basic formal annual report through which management communicates financial information to owners and external parties - investors, creditors, tax authorities, regulators and employees. The Statement of Profit and Loss reports results for a specified period and is therefore an interim report of performance.

- Financial statements form a key part of a company's annual report, together with the directors' report, auditors' report, corporate governance report and management discussion and analysis.

Meaning of Financial Statements

- Financial statements are the end products of the accounting process. They present, for a specified period and date, the financial results and the financial position of an enterprise by summarising accounting data recorded during the period.

- Typically, financial statements of a company include the Balance Sheet (statement of financial position), the Statement of Profit and Loss (income statement) and the Cash Flow Statement. Together with accompanying notes, disclosures and schedules they provide information necessary for economic decision-making.

- The main purpose of financial statements is to provide relevant, reliable and comparable information to users so that they can form judgements about the entity's profitability, liquidity, solvency and financial performance.

Limitations of Financial Statements (summary)

- They provide aggregate information intended for general user needs and therefore may not satisfy specialised requirements.

- Understanding financial statements requires basic accounting knowledge; they are technical documents.

- They are primarily historical: figures are generally based on historical cost and therefore may not represent current market values.

- They quantify financial performance but omit many qualitative factors such as employee relations, management quality, innovation and market reputation.

- Some amounts reflect estimates and judgements (for example, depreciation and provisions), so the figures are subject to managerial judgement and may be influenced by bias.

- Careful analysis and interpretation are necessary before using financial statements for decision-making.

Try yourself: What are the main financial statements that a company is required to prepare annually?

Nature of Financial Statements

- Financial statements are prepared from recorded monetary transactions for a specified period and present two complementary views: the financial position at a specific date (Balance Sheet) and the financial results over a period (Statement of Profit and Loss).

- The American Institute of Certified Public Accountants describes financial statements as instruments for periodically reviewing management's stewardship of resources and disclosing results of operations and financial position to stakeholders.

- They integrate recorded facts, accounting principles and procedures, and the legal/regulatory environment that governs business operations.

- Companies prepare and publish financial statements to communicate formally with shareholders and external parties; these statements are part of statutory reporting and corporate transparency.

- Financial statements do not directly communicate qualitative information such as industrial relations or staff motivation; such matters are discussed in non-financial sections of the annual report (for example, management discussion and analysis).

Recorded Facts

- Financial statements rely on recorded transactions and balances, normally measured at historical cost in the accounting records.

- Account balances such as cash, trade receivables and fixed assets are taken from the accounting ledger and supporting records.

- Assets acquired at different times and prices remain recorded at their historical costs; they are not automatically updated to current market prices. Therefore, a balance sheet may not indicate the present market value of assets.

Accounting Conventions

- Certain generally accepted accounting conventions and policies are followed when preparing financial statements.

- Inventories are valued at the lower of cost and net realisable value (market value) following conservative practice.

- Assets are shown at cost less accumulated depreciation (for depreciable assets).

- The materiality convention allows small or immaterial items (for example, stationery) to be expensed when purchased rather than capitalised.

- Adherence to conventions and standards promotes comparability, relevance and reliability of financial statements.

Postulates

- Financial statements are based on certain fundamental assumptions or postulates:

- The going concern postulate assumes the enterprise will continue to operate for the foreseeable future; consequently, assets are valued on a historical cost basis rather than liquidation value.

- The money measurement postulate assumes that transactions are recorded in monetary terms and that money is a common denominator, despite changes in purchasing power over time.

- The realisation postulate recognises revenue when goods are sold or services rendered, not necessarily when cash is received.

Personal Judgments

- Preparation of financial statements often requires estimates and personal judgements by management and accountants.

- Examples include estimation of useful life for computing depreciation, making provisions for doubtful debts, and selecting inventory valuation methods where cost and market differ.

- Such judgements are intended to present a fair view and to avoid overstatement of assets, liabilities, income or expenses; disclosures of significant accounting policies help users understand these choices.

Objectives of Financial Statements

Financial statements provide essential information to shareholders and other external users to understand the profitability and financial position of an enterprise. Their primary objective is to supply information useful for economic decision-making. Specific objectives comprise:

- Information on economic resources and obligations: To provide reliable, relevant and periodic information about the company's assets, liabilities and equity to users who do not have direct access to internal records.

- Earning capacity assessment: To provide information that helps predict, compare and evaluate the company's capacity to generate earnings in future periods.

- Cash flow information: To assist investors and creditors in assessing the timing, amount and uncertainty of future cash flows.

- Management effectiveness evaluation: To provide a basis for assessing how effectively management has used the company's resources.

- Societal impact reporting: To disclose measurable activities of the enterprise that impact society and the environment where those items are significant and measurable.

- Disclosure of accounting policies: To disclose significant accounting policies, assumptions and changes therein so that users may understand how the figures have been prepared and are to be interpreted.

Types of Financial Statements

- The principal financial statements are the Balance Sheet (statement of financial position) and the Statement of Profit and Loss (income statement). These are used for external reporting and internal management purposes such as planning, control and decision making.

- To explain movements in funds and to show changes in the financial position during a period, a Cash Flow Statement is prepared. The Cash Flow Statement classifies cash receipts and payments into operating, investing and financing activities (AS-3).

- Under the Companies Act, 2013, companies must prepare the Balance Sheet, Statement of Profit and Loss and notes in accordance with the revised Schedule III, which prescribes presentation and disclosure requirements to ensure consistency with accounting standards and regulatory reforms.

Balance Sheet as of 31st March, 20.....

Important Features of Presentation (Schedule III)

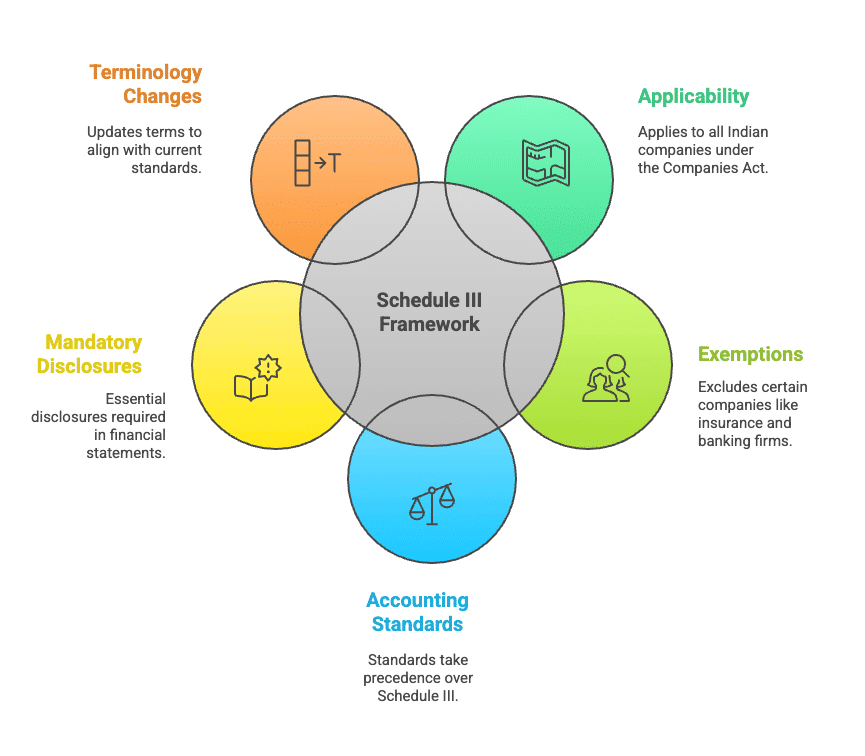

- Applicability: Schedule III applies to companies preparing financial statements under the Companies Act, 2013 in India.

- Exemptions: It does not apply to entities such as banking and insurance companies which have specialised formats prescribed by other statutes or regulators.

- Accounting standards precedence: Applicable accounting standards take precedence over Schedule III; Schedule III complements standards with required presentation and disclosures.

- Mandatory disclosures: Disclosures both on the face of financial statements and in the notes to accounts are required where specified.

- Terminology: Terms used in Schedule III carry meanings as defined in applicable accounting standards.

- Balance of detail: A useful balance must be struck between excessive detail and adequate disclosure of material items.

- Current/non-current bifurcation: Assets and liabilities are required to be classified into current and non-current categories (with prescribed criteria).

- Rounding off: Rounding off conventions are specified and must be followed.

- Presentation format: A vertical format (items arranged down the page) is prescribed for main statements.

- Profit and loss statement: Debit balances in the statement of profit and loss are shown as negative figures under Surplus where applicable.

- Share application money: Money received against share applications pending allotment must be disclosed.

- Terminology change: Old terms such as 'Sundry Debtors' and 'Sundry Creditors' are replaced by Trade Receivables and Trade Payables.

Shareholders' Funds and Related Disclosures

The shareholders' funds section on the face of the balance sheet is sub-classified and supported by detailed disclosures in the Notes to Accounts.

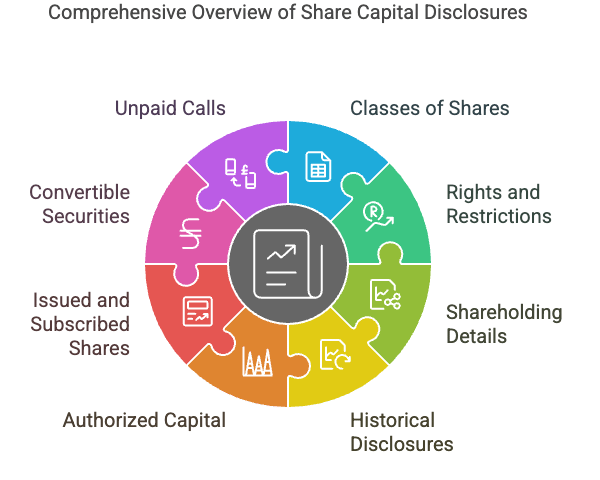

- Components on the face of balance sheet: Share Capital; Reserves and Surplus; Money received against Share Warrants.

- Share capital disclosures: For each class of share, the company must disclose the number of shares outstanding at the beginning and at the end of the reporting period, rights and restrictions attached to each class and par value per share.

- Major shareholder disclosures: Aggregate shares held by the holding/ultimate holding company, subsidiaries or associates; details of shareholders holding more than 5% of shares must be disclosed.

- Five-year disclosures: Aggregate number and class of shares allotted as fully paid without cash consideration, allotted as bonus shares and bought back during the last five years must be disclosed.

- Other required disclosures: Shares reserved for issue under options, terms and amounts of convertible securities, aggregate calls unpaid and amount originally paid on forfeited shares must be disclosed in the Notes to Accounts.

Reserve and Surplus - Main Categories

- Capital Reserve

- Capital Redemption Reserve

- Securities Premium Reserve

- Debenture Redemption Reserve

- Revaluation Reserve

- Share Options Outstanding Account

- Other Reserves (nature and purpose to be specified)

- Surplus: Balance in the statement of profit and loss after appropriation; disclosures must show transfers such as dividends, bonus issue, transfer to/from reserves etc.

- A reserve represented by earmarked investments is often called a Fund.

- A debit balance in the statement of profit and loss is shown as a negative figure under Surplus. Even if Reserve and Surplus becomes negative after adjusting a negative Surplus, it shall still be presented as Reserve and Surplus (which may be a negative amount).

- The Stock Options Outstanding Account is now recognised separatel y under shareholders' funds and, per ICAI guidance, is shown between share capital and reserves and surplus where applicable.

- Share application money pending allotment requires mandatory disclosure.

Money Received Against Share Warrants

- Amount received by a company against share warrants (to be converted into shares at a specified date and rate) is disclosed as a separate line item under shareholders' funds.

Example: Dinkar Ltd. has an authorised capital of Rs. 50,00,000 divided into equity shares of Rs. 100 each. The company invited applications for 40,000 shares, applications for 36,000 shares were received. All calls were made and duly received except for 500 shares on which the final call of Rs. 20 was not received. The company forfeited 200 shares on which final call was not received. Show how share capital will appear in the balance sheet of the company. Also prepare 'Notes to Accounts' for the same.

Ans:

Current and Non-current Classification

- In a classified balance sheet, assets and liabilities are presented as current and non-current. This enhances clarity about liquidity and maturity profiles.

- Classification criteria for an item to be treated as current include:

- It is part of the company's operating cycle.

- It is expected to be realised, sold or consumed within twelve months after the reporting date.

- It is held primarily for trading.

- It is cash or cash equivalent.

- For liabilities, if the company does not have an unconditional right to defer settlement for at least twelve months after the reporting date, it is current.

- Items not meeting these criteria are classified as non-current.

Important Points

- Preliminary expenses should be written off fully in the year incurred. They should first be deducted from securities premium, and any remaining balance written off to the profit and loss statement.

- Borrowing costs such as discount on debentures should be written off in the year they arise unless accounting standards require otherwise.

- Disclosure of share application money pending allotment is mandatory.

- Terminology: 'Sundry Debtors' and 'Sundry Creditors' are replaced by Trade Receivables and Trade Payables respectively.

Borrowings

Total borrowings are classified into long-term borrowings, short-term borrowings and current maturities of long-term debt.

- Loans repayable after more than twelve months (or operating cycle if longer) are classified as long-term borrowings on the face of the balance sheet.

- Loans repayable on demand or with original tenure not exceeding twelve months (or operating cycle) are classified as short-term borrowings on the face of the balance sheet.

- Current maturities of long-term loans (amounts payable within twelve months) are shown under other current liabilities with a note specifying the total long-term borrowing and the current maturities component.

- Deferred tax assets and liabilities are classified as non-current in accordance with Schedule III.

- Trade payables are shown under current liabilities. Amounts payable after 12 months or beyond the operating cycle are classified as other long-term liabilities with explanatory notes.

Proposed Dividend

- The proposed (final) dividend is recommended by the Board of Directors and is subject to approval by shareholders in the Annual General Meeting (AGM).

- The Board proposes the dividend after preparing the annual accounts; shareholders approve it subsequently (typically in the next financial year).

- Shareholders may reduce the proposed dividend but cannot increase it.

- Until approved by shareholders, the proposed dividend is a contingent liability and must be disclosed in the Notes to Accounts in accordance with AS-4 (Contingencies and Events Occurring after the Balance Sheet Date).

- Once the dividend is declared by shareholders, it becomes a legal liability and is recorded in the company's accounts.

- Provisions expected to be settled within twelve months (or operating cycle) are classified as short-term provisions under current liabilities; otherwise they are long-term provisions under non-current liabilities.

Fixed Assets

- Tangible and intangible fixed assets are treated as non-current assets. Even if an asset's useful life is less than twelve months, it is still described as a non-current asset given its nature as a fixed asset.

Investments

- Investments are classified as current or non-current depending on management's intention and whether they are expected to be realised within twelve months.

- Current investments are shown under current assets; non-current investments are presented under non-current assets. Both categories are displayed on the face of the balance sheet with appropriate notes.

Inventories

- Inventories are treated as current assets.

Trade Receivables

- Trade receivables expected to be realised beyond twelve months from the reporting date (or beyond operating cycle) are classified as other non-current assets with a note to accounts.

- Trade receivables expected to be realised within twelve months are classified as current assets and shown on the face of the balance sheet.

Cash and Cash Equivalents

- Cash and cash equivalents are always classified as current assets. Disclosure of cash and cash equivalents follows AS-3 (Cash Flow Statements) which takes precedence over Schedule III where relevant.

Example: Show the following items in the balance sheet of Sunfill Ltd. as at March 31, 2017:

Ans:

Form and Content of Statement of Profit and Loss

Statement of Profit and Loss for the year ended ______________

Principal items included in the Statement of Profit and Loss

1. Revenue from Operations

- Sale of products.

- Sale of services.

- Other operating revenues.

- For finance companies, revenue from operations includes interest, dividends and other income arising from financial services.

2. Other Income

- Interest income (for non-finance companies).

- Dividend income.

- Net gain or loss on sale of investments.

- Other non-operating income (net of direct expenses attributable to such income).

3. Expenses

Example: From the following particulars, prepare Statement of profit and loss for the year ending March 2017, showing profit before tax as per Schedule III of the Companies Act, 2013.

Solution:

Uses and Importance of Financial Statements

Financial statements are essential to a wide range of users - management, investors, shareholders, creditors, government, bankers, employees and the public. They provide financial information that assists these users in making informed economic decisions. Financial statements are also a key component of the company's annual report, along with directors' and auditors' reports and management discussion and analysis.

- Report on stewardship: Financial statements show how management has performed in utilising shareholders' resources and achieving targets.

- Basis for fiscal policies: The government uses aggregated corporate financial information to frame taxation and economic policies.

- Basis for granting credit: Banks and financial institutions assess creditworthiness and decide loan terms using financial statements.

- Guide for prospective investors: Short-term and long-term investors rely on financial statements to evaluate security, liquidity, profitability and solvency of investment choices.

- Valuation of existing investment: Shareholders use financial statements to assess the safety and returns on their investments and to decide whether to hold, buy or sell shares.

- Support for trade associations: Trade bodies analyse financial statements to develop benchmarks, set industry norms and assist members in accounting and financial matters.

- Assistance to stock exchanges: Stock exchanges, brokers and analysts use financial statements to ensure transparency, protect investors and support valuation and trading decisions.

Limitations of Financial Statements (detailed)

- Financial statements are prepared with care, but they have inherent limitations:

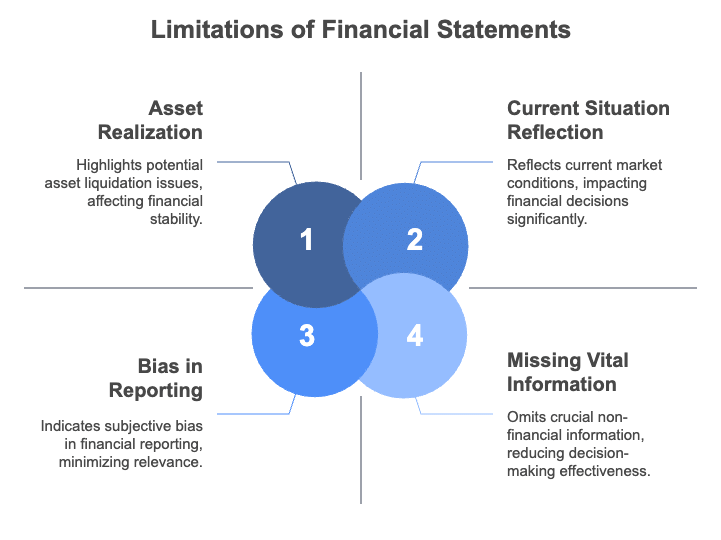

- Historical nature: Most figures are based on historical cost and therefore may not reflect current market conditions as purchasing power changes over time.

- Realisation uncertainty: Some assets shown on the balance sheet may not realise their stated amounts if the company is compelled to liquidate; the balance sheet shows unexpired costs rather than guaranteed recoverable amounts.

- Bias and judgement: Figures are influenced by accounting concepts, conventions and management's estimates, which may introduce bias.

- Aggregate presentation: Financial statements present summary information and may omit detailed transactional or contextual information required for certain decisions.

- Missing vital information: Events such as impending contract terminations, market losses or contingent liabilities may not be fully apparent on the face of the statements.

- Absence of qualitative data: Non-financial aspects such as management quality, employee morale and competitive strategy are not quantified within financial statements.

- Interim perspective: The Statement of Profit and Loss reports performance over a period but does not by itself guarantee future earning capacity; the Balance Sheet is accurate at one date only and does not predict future changes.

FAQs on Chapter Notes: Financial Statements of a Company

| 1. What's the difference between a Balance Sheet and an Income Statement in company accounts? |  |

| 2. How do I identify fixed assets and current assets on a company's Balance Sheet? | |

| 3. Why do companies prepare notes to financial statements and what information do they contain? | |

| 4. What does depreciation mean and how does it affect a company's financial statements? | |

| 5. How can I calculate a company's profitability and solvency using its financial statements? | |