NCERT Solution: Accounting for Not for Profit Organisation - 2

PAGE NO. 51

NUMERICAL QUESTIONS:

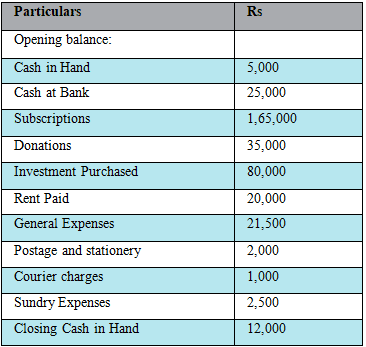

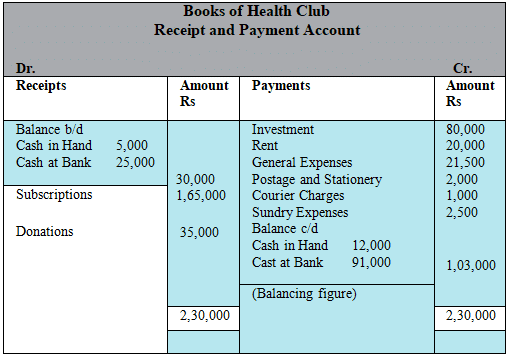

Q.1. From the following particulars taken from the Cash Book of a health club, prepare a Receipts and Payments Account.

Ans.

Working/Explanation: The Receipts and Payments Account is a summary of all cash and bank transactions for the period. Present receipts under appropriate heads (subscriptions, donations, sale proceeds, interest, etc.) and payments under their heads (salaries, rent, repairs, etc.). Ensure closing cash and bank balances are shown at the foot as they represent the opening balances for the next period. Any cash discounts or bank charges are recorded on the payments side. The image above shows the column-wise totals and the balancing figure which is the closing cash/bank balance.

PAGE NO. 52

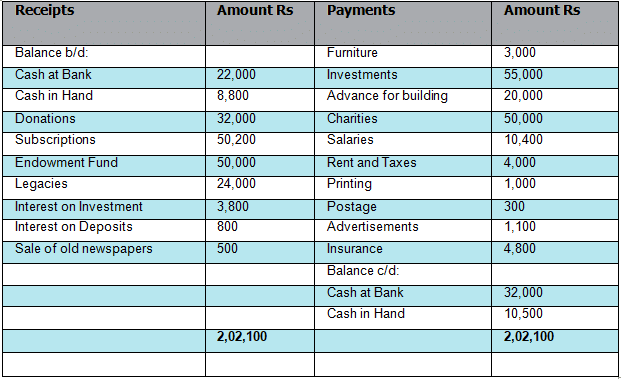

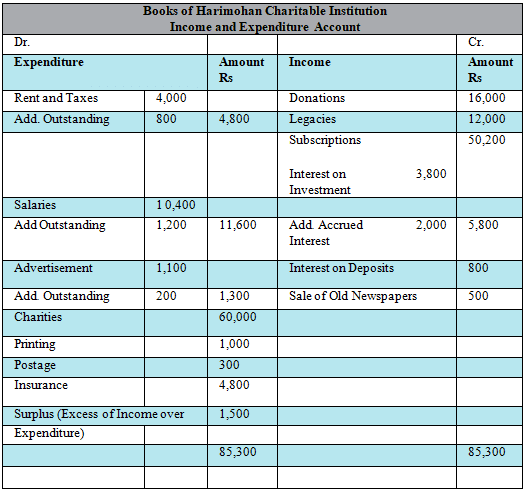

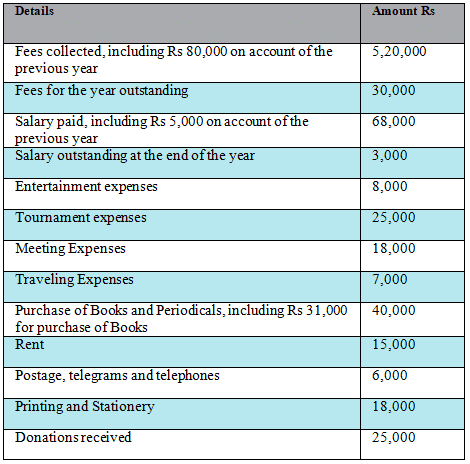

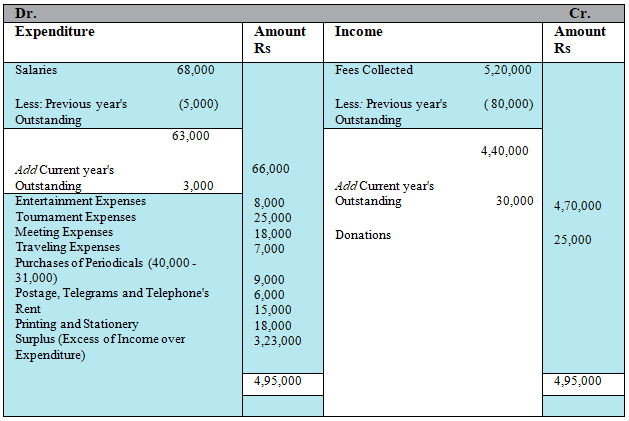

Q.2. The Receipt and Payment Account of Harimohan charitable institution is given:

Receipt and Payment Account for the year ending March 31, 2015

Prepare the Income and Expenditure Account for the Year ended on March 31, 2007 after considering the following:

(i) It was decided to treat Fifty per cent of the amount received on account of Legacies and Donations as income.

(ii) Liabilities to be provided for are:

Rent Rs 800; Salaries Rs 1,200; advertisement Rs 200.

(iii) Rs 2,000 due for interest on investment was not actually received.

Ans.

Working/Explanation: Prepare the Income and Expenditure Account by: (a) Taking fifty per cent of legacies and donations to the income side and the remaining fifty per cent to the capital/fund (as per instruction); (b) Including accruals and outstanding items - provide for Rent Rs 800, Salaries Rs 1,200 and Advertisement Rs 200 as expenses in the Income and Expenditure Account though not paid; (c) Recognise accrued interest of Rs 2,000 as income even if not received (but if it was not to be received at all, then it should be shown as accrued income - per given instruction it was due but not received so it should be included as income and shown as receivable on the asset side). The image displays the complete ledger-style presentation and the resulting Excess of Income over Expenditure. Note provided shows a minor discrepancy with the book; recheck arithmetic and treatment of legacies while reconciling.

Q.3. From the following particulars, prepare Income and Expenditure account:

From the following particulars, prepare Income and Expenditure account:

Ans.

Working/Explanation: Convert the Receipt & Payment items into accrual basis. Include income earned during the year (subscriptions less opening outstanding plus closing outstanding and adjust advance receipts). Provide for depreciation where required and for outstanding expenses. The image shows the detailed transfer of relevant receipts to the income side and payments that are revenue in nature to the expenditure side, culminating in Excess of Income over Expenditure. The note indicates a difference between solution and book figures; verify inclusion/exclusion of any capital receipts or prior year amounts that could cause the difference.

PAGE NO. 53

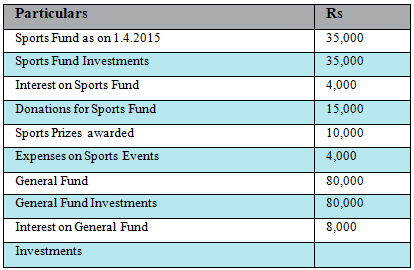

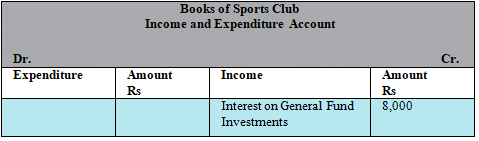

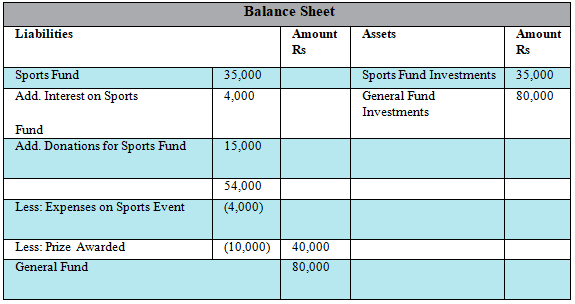

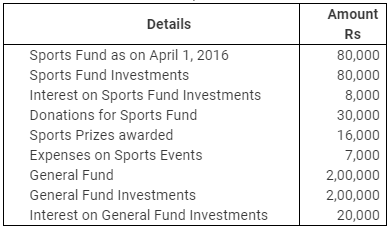

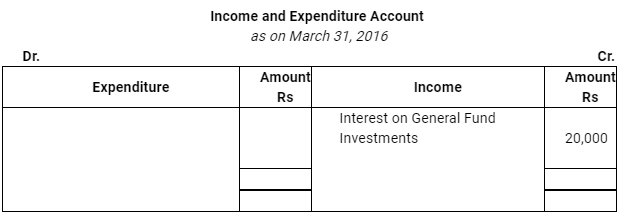

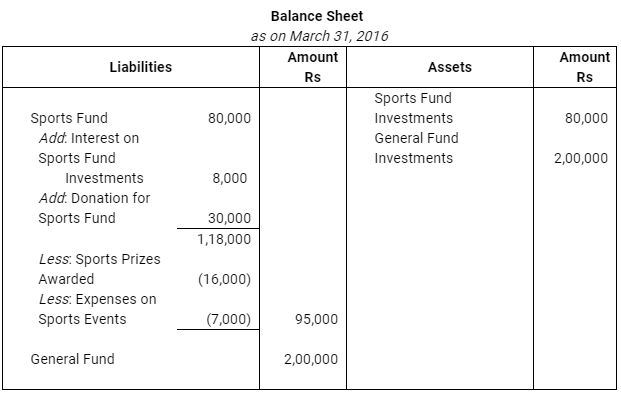

Q.4. Following is the information given in respect of certain items of a Sports Club. Show these items in the Income and Expenditure Account and the Balance Sheet of the Club:

Ans.

Explanation: Classify each item as either revenue or capital. Items that relate to day-to-day operations (e.g., subscriptions, salaries, repair charges) are shown in the Income and Expenditure Account, while capital items (e.g., donations for pavilion, construction costs, purchase of assets) are shown on the liabilities (funds) and assets side of the Balance Sheet. Provide depreciation on fixed assets where applicable. The images above show the Income & Expenditure treatment and the Balance Sheet presentation with each item placed in its correct head.

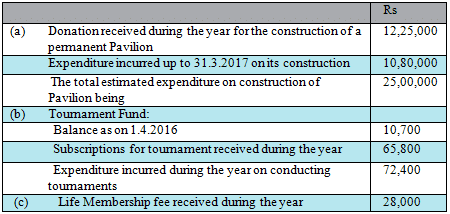

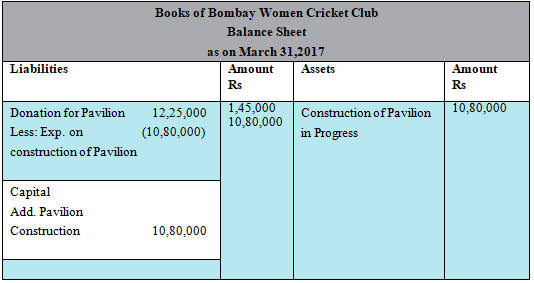

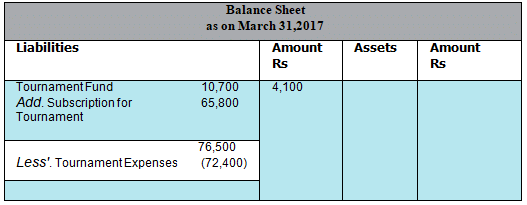

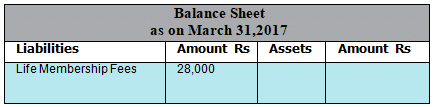

Q.5. How will you deal with the following items while preparing for the Bombay Women Cricket Club its income and expenditure account for the year ending 31.3.2017 and its Balance Sheet as on 31.3.2017:

Give reasons for your answers

Ans.

(a)

Reason

Donation for construction of Pavilion is a donation for specific purpose.

Expenses on construction on Pavilion is a capital expenditure.

(b)

Reason

All funds received are treated as capital receipts and expenses related to any fund are deduced from the concerned funds.

(c)

Reason

Life Membership Fees are considered as capital receipts and are shown on the Liabilities side of the Balance Sheet, if nothing is specified about its treatment. But if it is to be treated as revenue item, then it is shown on the credit side of the Income and Expenditure Account.

Further Explanation: For (a) record the donation received for pavilion under a specific fund (capital fund) and show pavilion as fixed asset under assets; the construction cost reduces that specific fund. For (b) when a fund is created for a purpose, receipts are credited to that fund and any related expenditure is debited to the same fund. For (c) unless explicitly stated that life membership fees should be treated as income, they are treated as capital (so shown on the liabilities side under Capital/Endowment Fund). If the governing body decides to treat a portion as revenue (e.g., transfer to income over several years), follow that policy consistently.

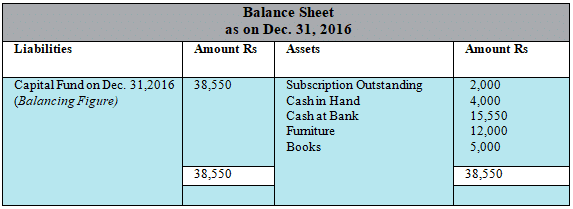

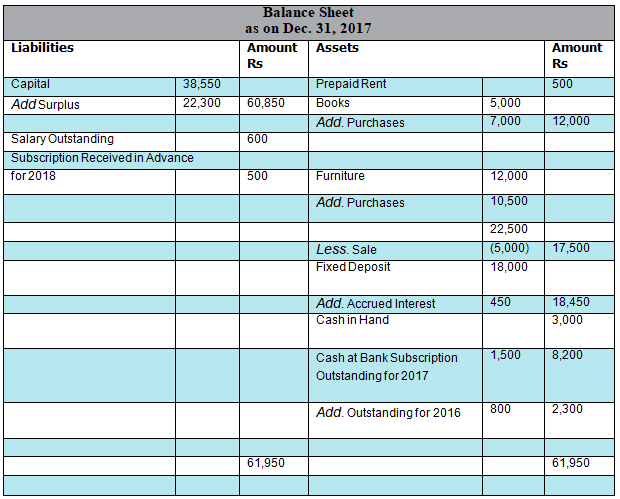

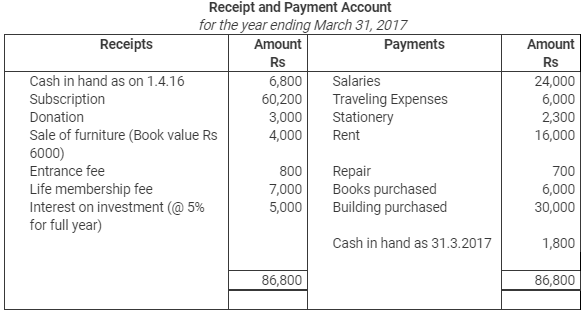

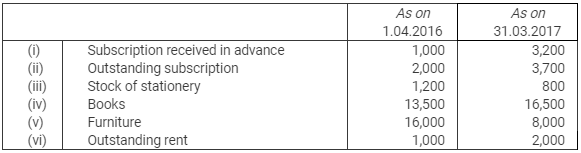

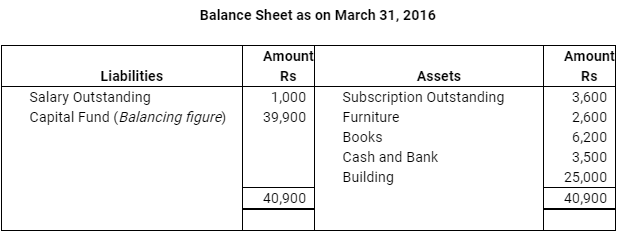

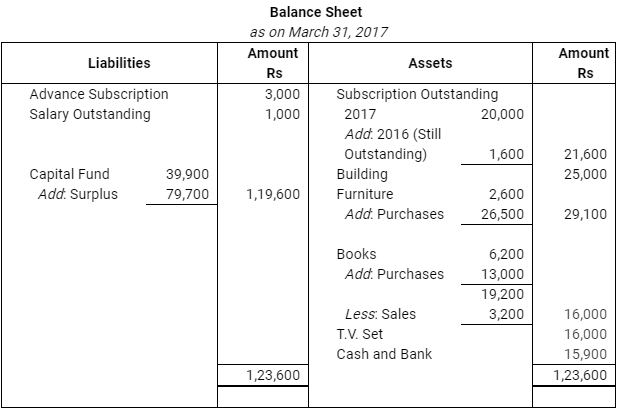

Q.6. From the following receipts and payments and information given below, Prepare Income and Expenditure Account and opening Balance Sheet of Adult Literacy Organisation as on December 31, 2013.

Information:

(i) Subscription outstanding as on 31.12.2016 Rs 2,000 and on December 31, 2017 Rs 1,500.

(ii) On December 31, 2017 Salary outstanding Rs 600, and one month Rent paid in advance.

(iii) On Jan. 01, 2016 organisation owned Furniture Rs 12,000, Books Rs 5,000.

Ans.

Books of Adult Literacy Organisation

Income and Expenditure Account

as on Dec. 31, 2017

Explanation: Convert the cash figures into accrual basis. Add subscriptions outstanding (closing) to subscription receipts and deduct opening outstanding and any advance received. Include outstanding salary as an expense and treat one month's rent paid in advance as a prepaid expense (asset). Opening fixed assets (Furniture, Books) are shown in the Balance Sheet at their book value and depreciation (if to be provided) should be charged in the Income & Expenditure Account. The images present the detailed Income & Expenditure Account and the opening Balance Sheet showing how closing balances and adjustments are reflected.

PAGE NO. 54

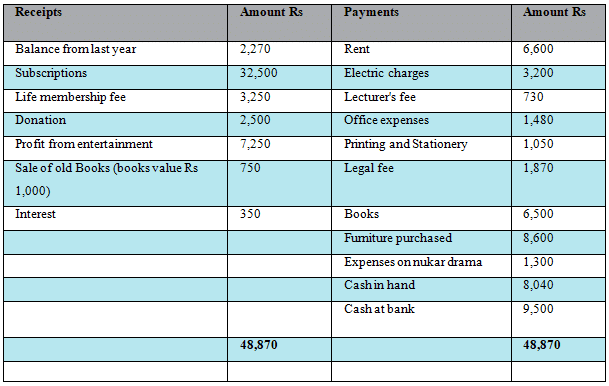

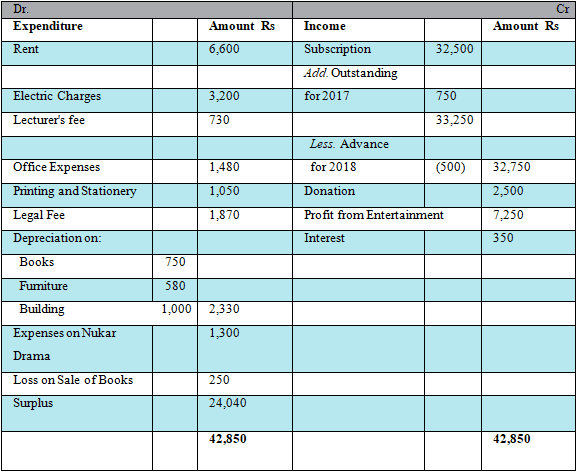

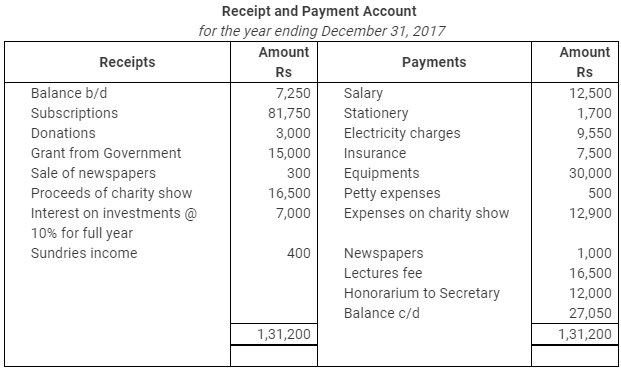

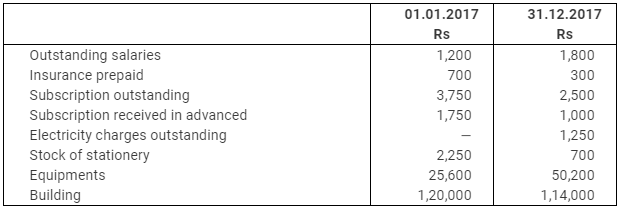

Q.7. The following is the account of cash transactions of the Nari Kalayan Samittee for the year ended December 31, 2017:

You are required to prepare an Income and Expenditure Account after the following adjustments:

(a) Subscription still to be received are Rs 750, but subscription include Rs 500 for the year 2018.

(b) In the beginning of the year the Sangh owned building Rs 20,000 and furniture Rs 3,000 and Books Rs 2,000.

(c) Provide depreciation on furniture @ 5% (including purchase), books @ 10% and building @ 5%.

Ans.

Explanation: Adjust subscription receipts for next year's portion by deducting Rs 500 (advance for 2018) and add outstanding Rs 750 to the subscription income. Show opening assets (building, furniture, books) in the Balance Sheet and charge depreciation at the rates given: Furniture 5%, Books 10%, Building 5%. Depreciation is an expense in the Income & Expenditure Account and reduces the book value of the respective assets in the Balance Sheet. The images show the computations and final presentation.

PAGE NO. 55

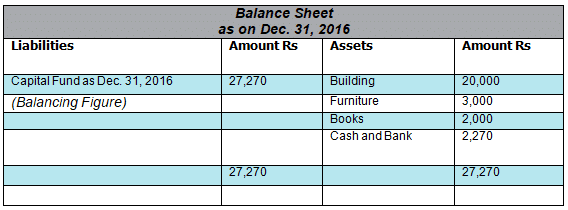

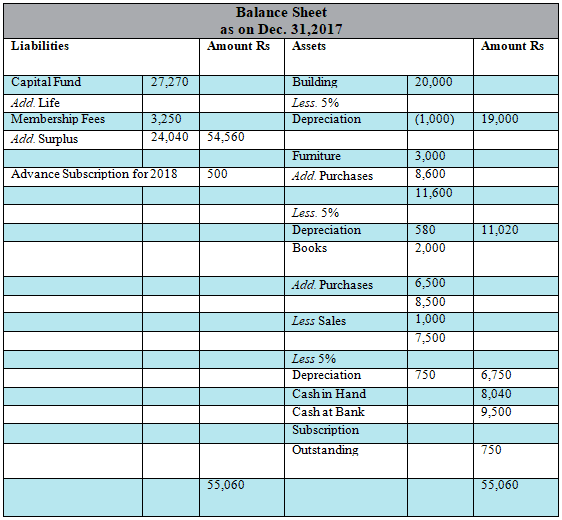

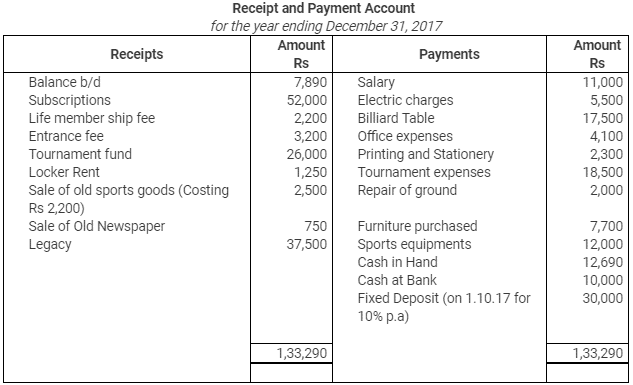

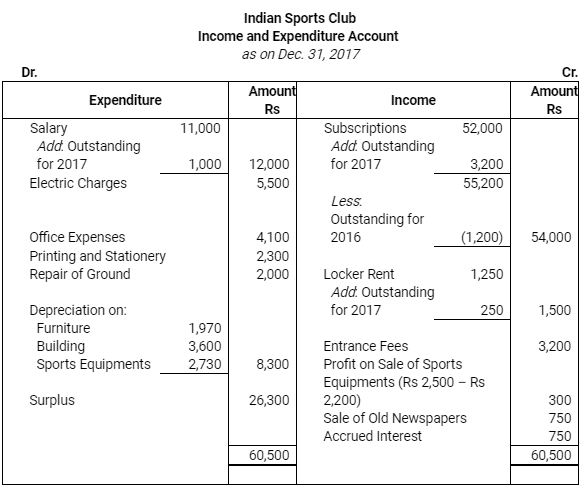

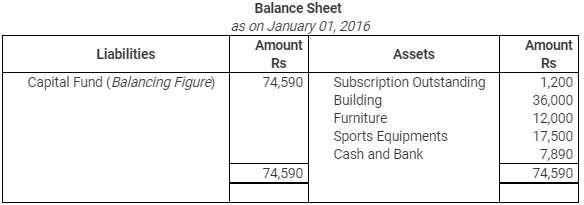

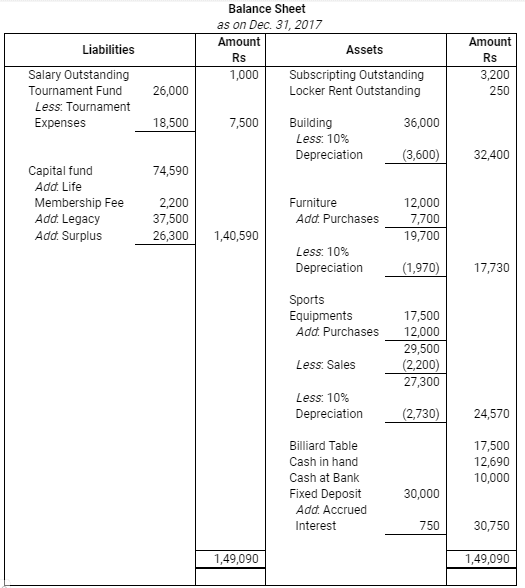

Q.8. Following is the Receipt and Payment Account of Indian Sports Club, prepared Income and Expenditure Account, Balance Sheet as on December 31, 2017:

Other Information:

Subscription outstanding was on December 31, 2016 Rs 1,200 and Rs 3,200 on December 31, 2017. Locker rent outstanding on December 31, 2013 Rs 250. Salary outstanding on December 31, 2013 Rs 1,000.

On January 1, 2017, club has Building Rs 36,000, furniture Rs 12,000, Sports equipments Rs 17,500. Depreciation charged on these items @ 10% (including Purchase).

Ans.

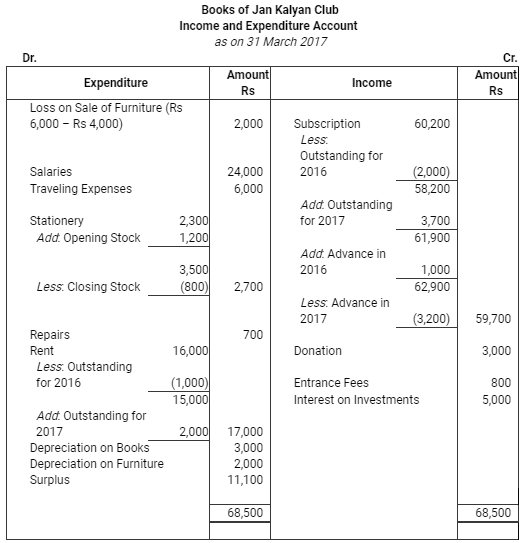

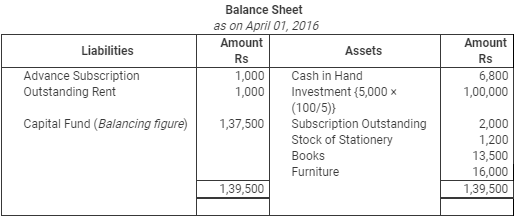

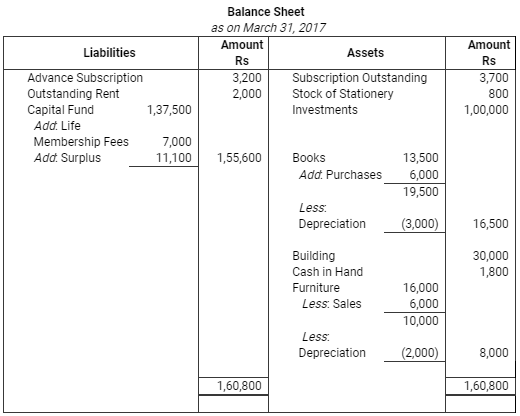

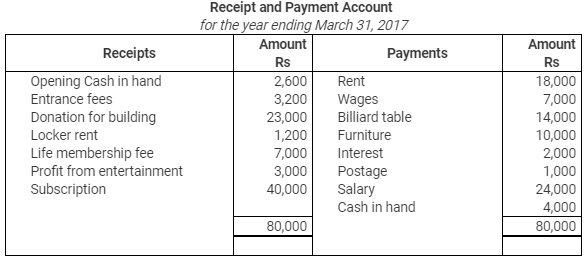

Q.9. From the following Receipt and Payment Account of Jan Kalyan Club, prepare Income and Expenditure Account and Balance Sheet for the year ending March 31, 2017.

Additional Information:

Ans.

Explanation: Use the additional information to convert cash receipts and payments into accrual basis: adjust subscriptions for outstanding and advance, include outstanding expenses, account for opening fixed assets and provide depreciation as required. The images include the stepwise transfer of items to Income & Expenditure Account and the resulting Balance Sheet figures.

PAGE NO. 56

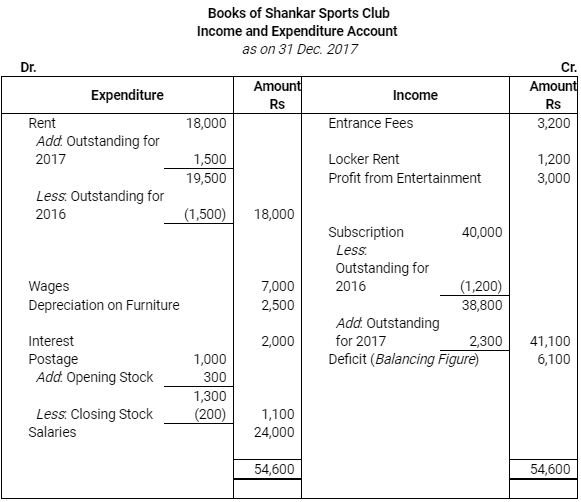

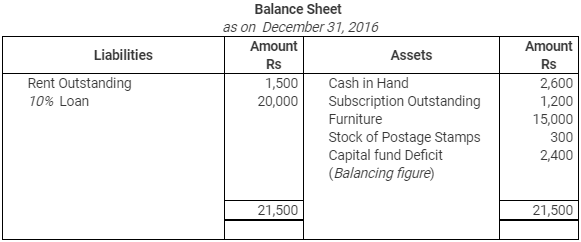

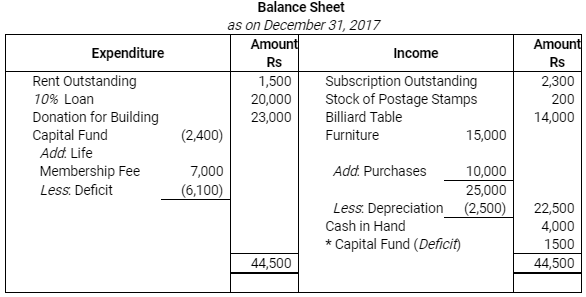

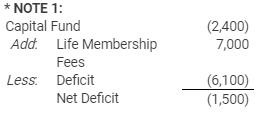

Q.10. Receipt and Payment Account of Shankar Sports club is given below, for the year ended March 31, 2017

On March 31, 2017. The club took a loan of Rs 20,000 (@ 10% p.a.) in 2017*.

Ans.

Explanation: Adjust subscriptions by adding opening outstanding Rs 1,200 and subtracting closing outstanding Rs 2,300 from cash receipts to get subscription income for the year. Account for opening and closing stamp stocks - treat consumption as postage expense equal to opening stock plus purchases minus closing stock. Include rent due for prior year as an outstanding expense and record the current unpaid rent as outstanding liability. Show the loan of Rs 20,000 as a liability in the Balance Sheet and account for interest on loan for the period if due. The images show the Income & Expenditure Account, Balance Sheet and calculations of these adjustments.

PAGE NO. 57

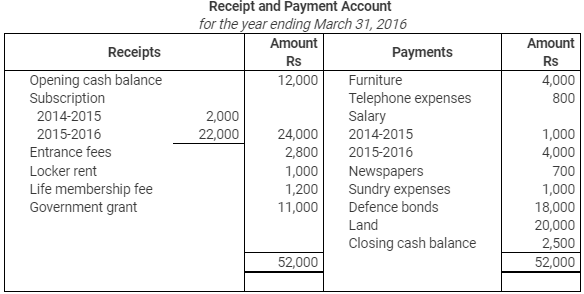

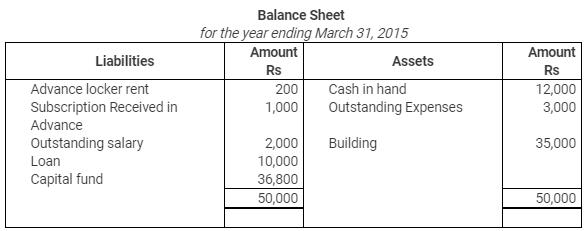

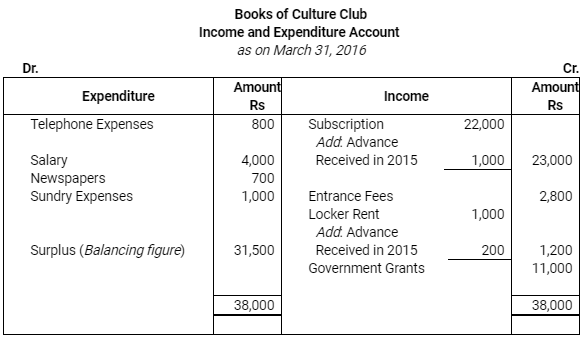

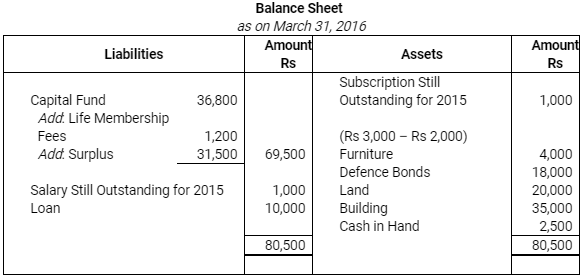

Q.11. Prepare Income and Expenditure Account and Balance Sheet for the year ended December 31, 2006 from the following Receipt and Payment Account and Balance Sheet of culture club:

Explanation: Transfer revenue items from the Receipt & Payment account to the Income & Expenditure Account and capital items to the Balance Sheet. Reconcile opening balances from the given Balance Sheet and adjust for receipts/payments impacting funds and assets. Provide depreciation on assets as necessary and include outstanding or accrued items. The images above give the full prepared Income & Expenditure Account and the Balance Sheet after adjustments.

PAGE NO. 58

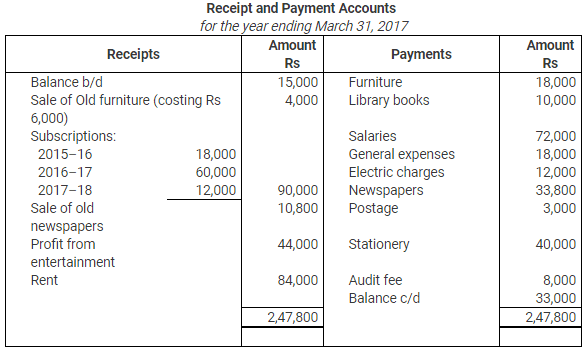

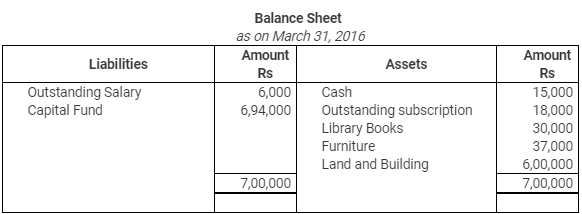

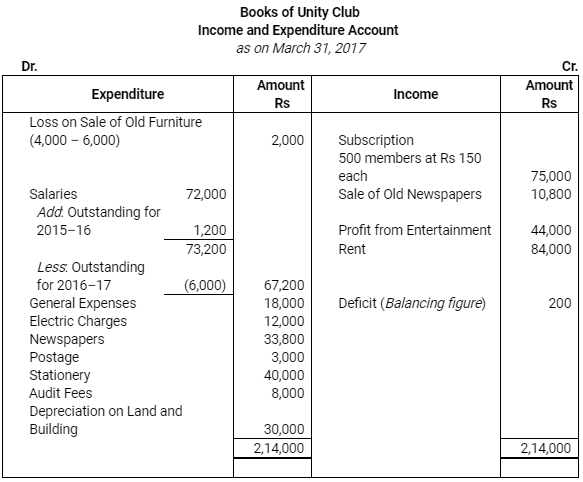

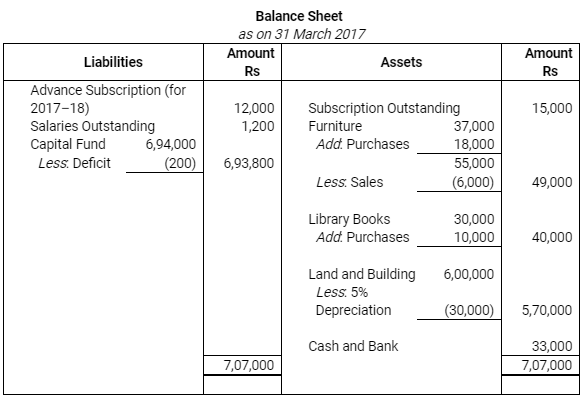

Q.12. From the following Receipt and Payment Account prepare final accounts of a Unity Club for the year ended March 31, 2017.

Additional Information:

1. The Club had 500 members each paying an annual subscription of Rs 150.

2. On 31.3.2016 salaries outstanding amounted to Rs 1,200 and salaries paid included Rs 6,000 for the year 2015-16.

3. Provide 5% depreciation on Land and Building.

Ans.

Explanation: Compute subscription income by comparing the expected total (500 × 150) with amounts received and adjust for opening and closing outstanding/advance subscriptions. Remove any salary payments that relate to prior year (Rs 6,000) from current year expense, and add salaries outstanding as an expense. Depreciate Land and Building at 5% and show depreciation as an expense and reduce asset value in the Balance Sheet. The images show the final Income & Expenditure Account and Balance Sheet.

PAGE NO. 58

Q.13. Following is the information in respect of certain items of a Sports Club. You are required to show them in the Income and Expenditure Account and the Balance Sheet.

Explanation: Classify each item as revenue or capital and place it accordingly. For example, sponsorships or donations for recurring activities are income, while donations for construction or specific assets are capital and shown under funds. Depreciation, outstanding liabilities and accruals must be adjusted. The images provide the correct placement of each item in Income & Expenditure and Balance Sheet formats.

PAGE NO. 59

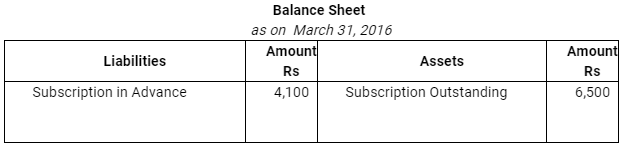

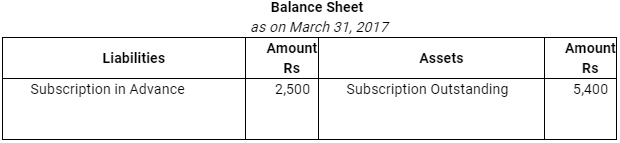

The additional information was as under:

1. Subscription Outstanding as on March 31, 2016 were Rs 6,500,

2. Subscription received in advance as on March 31, 2016 were Rs 4,100,

3. Subscription Outstanding as on March 31, 2017 were Rs 5,400,

4. Subscription received in advance as on March 31, 2017 were Rs 2,500.

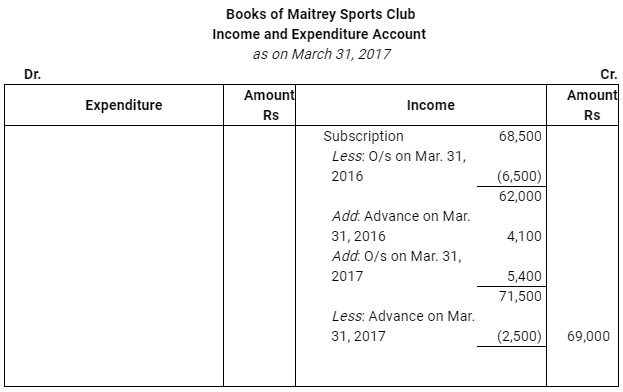

Show how that above information would appear in the final accounts for the year ended on March 31, 2017 of Maitrey Sports Club.

Ans.

Working/Explanation: Determine subscription income for the year as: Cash receipts Rs 68,500 + Opening outstanding Rs 6,500 - Opening advance Rs 4,100 - Closing outstanding Rs 5,400 + Closing advance Rs 2,500. Present subscription income in the Income & Expenditure Account and show closing outstanding as current asset and closing advance as current liability in the Balance Sheet. The images display the calculations and how the amounts appear in final accounts.

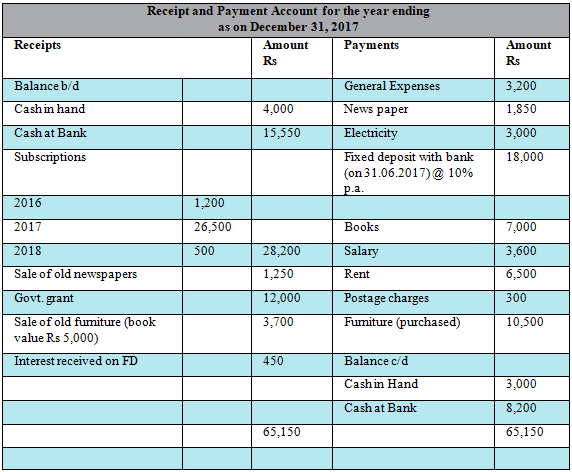

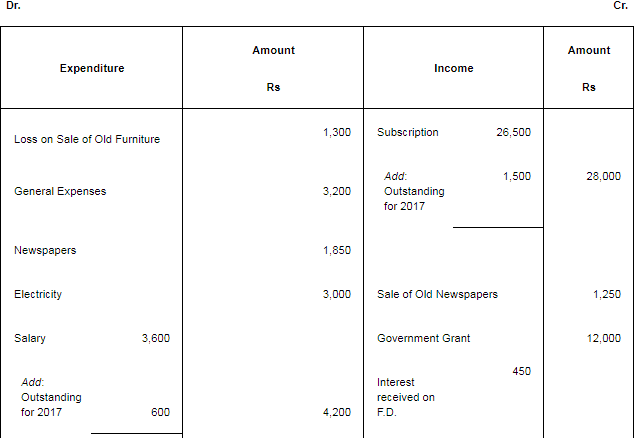

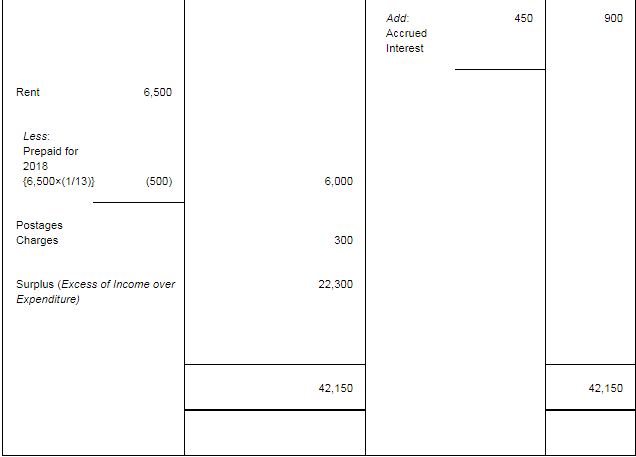

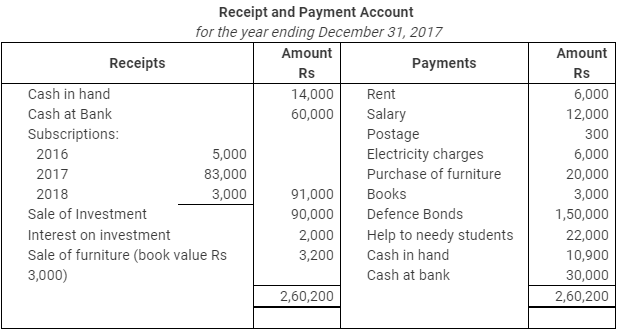

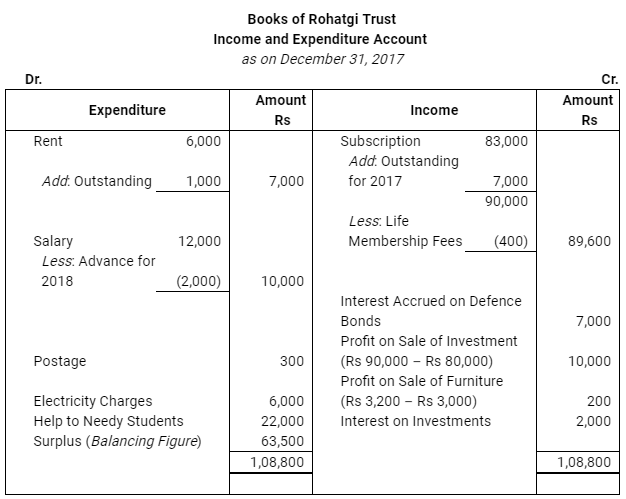

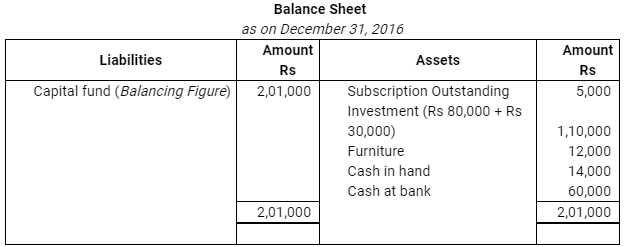

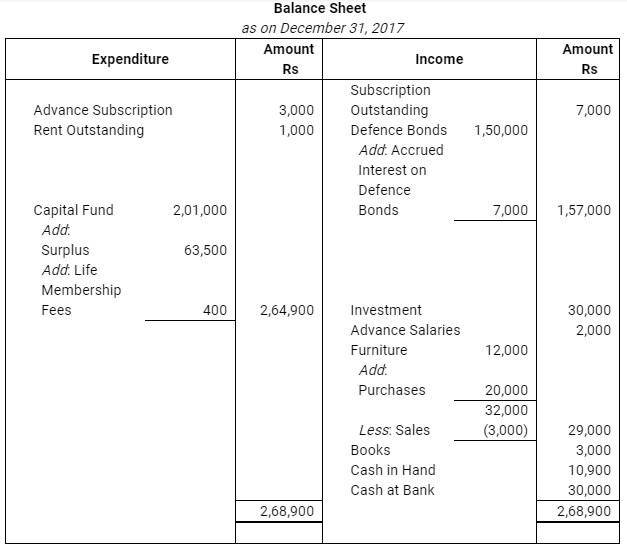

Q.15. Following is the Receipt and Payment account of Rohatgi Trust :

Prepare Income and expenditure account for the year ended December 31, 2017, and a balance sheet as on that date after the following adjustments: Subscription for 2017, still owing were Rs 7,000. Interest due on defence bonds was Rs7,000, Rent still owing was Rs 1,000. The Book value of investment sold was Rs 80,000, Rs 30,000 of the investment were still in hand. Subscription received in 2017 included Rs 400 from a life member. The total furniture on January 1, 2017 was worth Rs 12,000. Salary paid for the year 2018 is Rs 2,000.

Ans.

Explanation: Adjust subscription receipts for outstanding subscriptions (Rs 7,000) and exclude life membership receipt (Rs 400) from subscription income if life fee is to be treated as capital. Include accrued interest on defence bonds (Rs 7,000) though not received. Show rent and salary outstanding as expenses. For investments, remove the book value of investments sold (Rs 80,000) from investments and show any gain or loss on sale in Income & Expenditure Account if necessary; remaining investments include Rs 30,000 still in hand. Furnish opening furniture under fixed assets and account for depreciation. The provided images show the complete Income & Expenditure Account and the Balance Sheet after these adjustments.

PAGE NO. 60

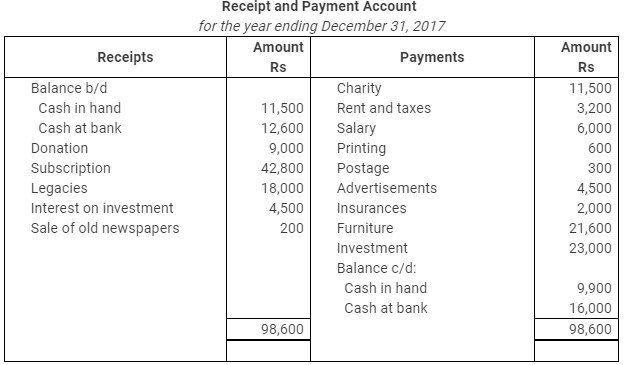

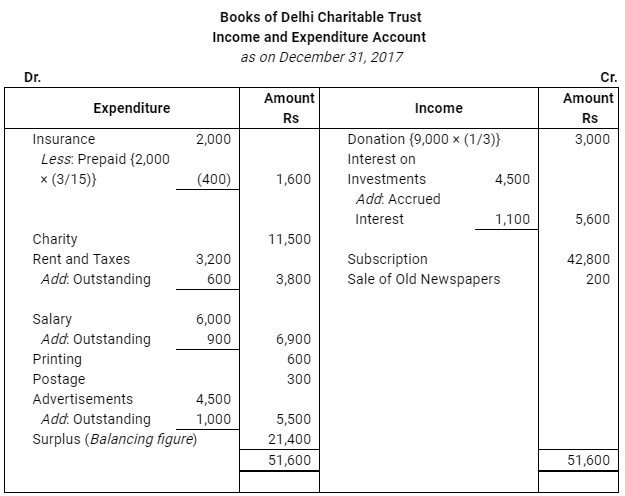

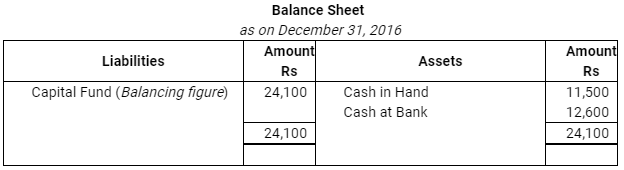

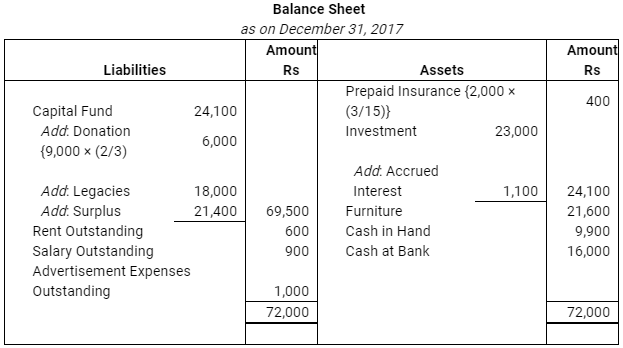

(a) It was decided to treat one-third of the amount received on account of donation as income.

(b) Insurance premium was paid in advance for three months.

(c) Interest on investment Rs1,100 accrued was not received.

(d) Rent Rs600: salary Rs900 and advertisement expenses Rs1,000 outstanding as on December 31, 2017.

Ans.

Explanation: Treat one-third of donations as income and the remaining two-thirds as capital (or fund) as instructed. Record prepaid insurance (three months) as an asset (prepaid expense) and allocate only the portion relating to current year as expense. Include accrued interest Rs 1,100 as income receivable. Provide for outstanding rent, salary and advertisement expenses as liabilities and recognise them in the Income & Expenditure Account. The images show the detailed workings and final statements.

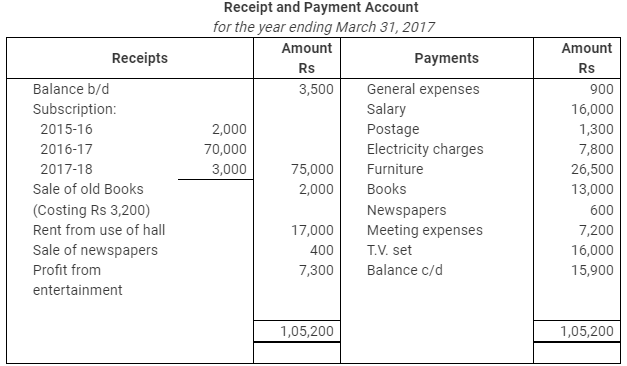

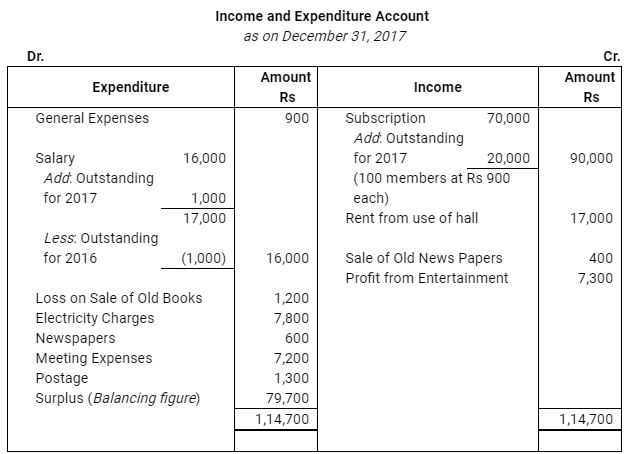

Q.17. From the following Receipt and Payment Account of a club, prepare Income and Expenditure Account for the year ended December 31, 2017 and the Balance Sheet as on that date.

(a) The club has 100 members each paying an annual subscription of Rs 900. Subscriptions outstanding on March 31, 2016 were Rs 3,600.

(b) On March 31, 2017, salary outstanding amounted to Rs 1,000, Salary paid included Rs 1,000 for the year 2012.

(c) On April 1, 2017 the club owned land and building Rs 25,000, furniture Rs 2,600 and books Rs 6,200.

Ans.

Explanation: Calculate subscription income using 100 members × Rs 900 and adjust for opening outstanding and any advance amounts. Remove salary amount that relates to an earlier year (Rs 1,000) from current year's expense, and add salary outstanding as current liability. Show fixed assets (Land & Building, Furniture, Books) at opening book values and provide depreciation if required. The images present the Income & Expenditure Account and Balance Sheet after making these adjustments.

PAGE NO. 61

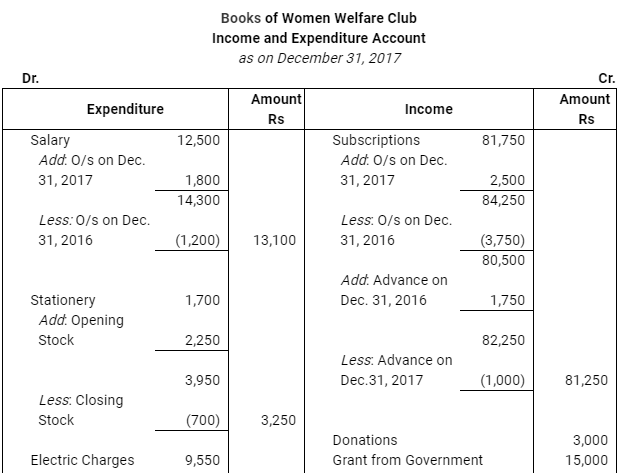

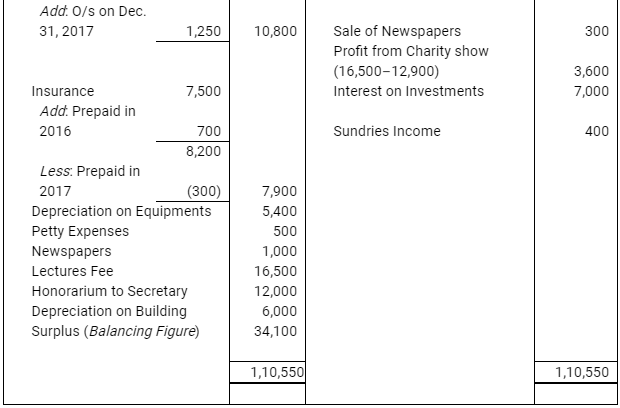

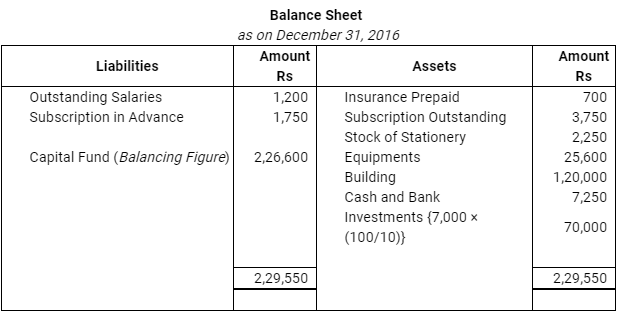

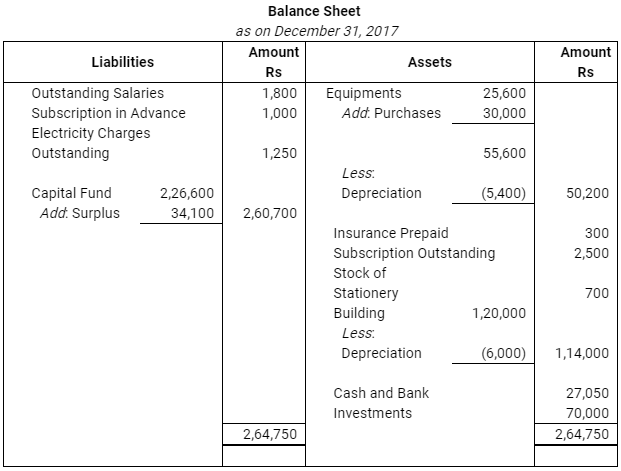

Q.18. Following is the Receipt and Payment Account of Women's Welfare Club for the year ended December 31, 2017:

Prepare Income and Expenditure Account for the year ended December 31, 2017 and Balance Sheet as on that date.

Ans.

Explanation: Apply accrual adjustments: include subscriptions and other incomes earned in the year after adjusting outstanding/advance; include outstanding expenses; charge depreciation on fixed assets; and present reserves and funds correctly in the Balance Sheet. The images contain the completed Income & Expenditure Account and the Balance Sheet with all adjustments applied.

PAGE NO. 62

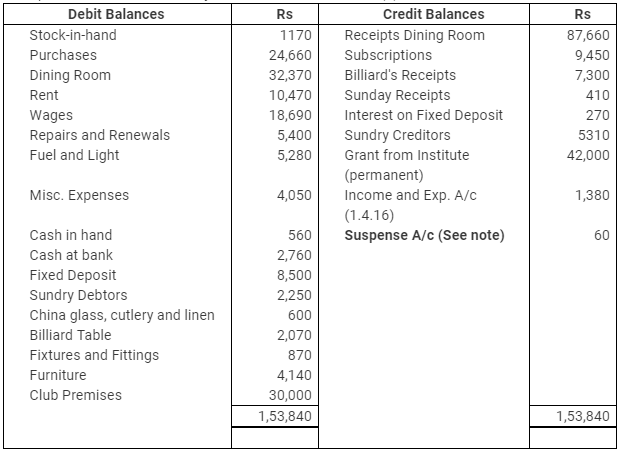

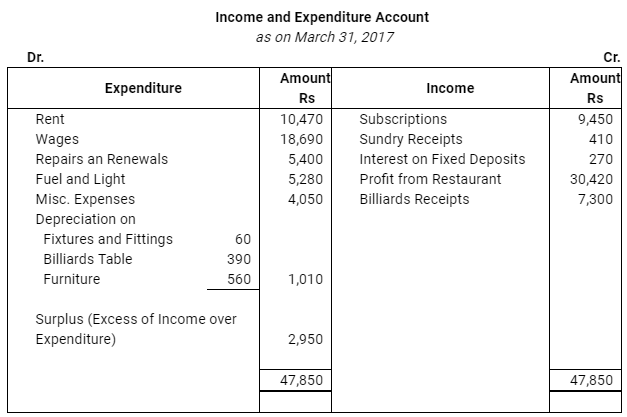

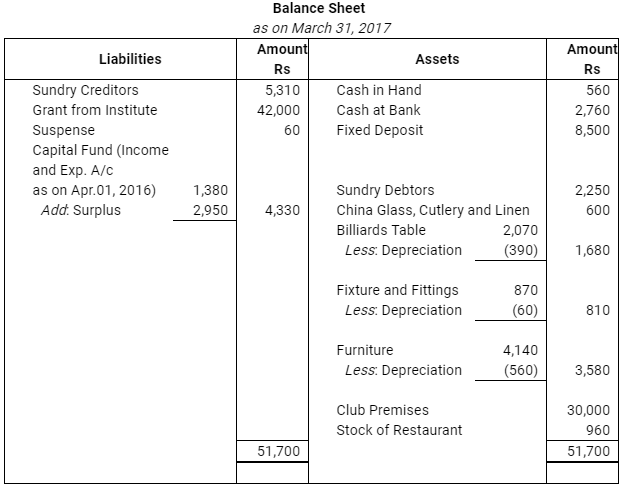

Q.19. As at March 31,2017 the following balances have been extracted from the books of the Indian Chartered Accountants Recreation Club and you are asked to prepare (1) Trading Account for ascertaining gross profit derived from running restaurant and dining room and (2) Income and Expenditure Account for the year ended March 31, 2017 (3) and a Balance Sheet as at that date.

On March 31,2016 stock of restaurant consisted of Rs 900 and Rs 60 respectively. Provide depreciations Rs 60 on fixtures and fittings, Rs 390 on billiard table and Rs 560 on furniture.

Ans.

Important Note:

1. Credit side of the Trial Balance of the question is short by Rs 60. Thus, in order to tally both sides of the Trial Balance, Suspense Account will be opened with the difference amount of Rs 60.

2. In the adjustment, Closing Stock should be Rs 960 instead of Rs 900.

Books of Indian Chartered Accountants Recreation Club

Restaurant Trading Account

Explanation: Prepare a Trading Account for the restaurant by taking opening stock, adding purchases, less closing stock to arrive at cost of goods sold and then compute gross profit. Transfer restaurant gross profit to the Income & Expenditure Account. Provide depreciation on fixtures & fittings, billiard table and furniture as given, and include these depreciation charges in the Income & Expenditure Account. Open a Suspense Account only to rectify the Trial Balance discrepancy of Rs 60 and disclose it until the error is located. The images show the Trading Account, Income & Expenditure Account and Balance Sheet with these adjustments applied.

FAQs on NCERT Solution: Accounting for Not for Profit Organisation - 2

| 1. What is meant by not for profit organization? |  |

| 2. What are the sources of income for not for profit organizations? | |

| 3. What is the accounting treatment for donations received by a not for profit organization? | |

| 4. What is the difference between a not for profit organization and a for-profit organization? | |

| 5. What is the importance of maintaining proper accounting records for not for profit organizations? | |