Partnership Deed | Crash Course of Accountancy - Class 12 - Commerce PDF Download

Partnership Deed

Partnership comes into existence as a result of agreement among the partners. The agreement can be either oral or written. The Partnership Act does not require that the agreement must be in writing. But wherever it is in writing, the document, which contains terms of the agreement is called ‘Partnership Deed’. It is also called ‘Articles of Partnership’

• Names and Addresses of the firm and its main business;

• Names and Addresses of all partners;

• Amount of capital to be contributed by each partner;

• The accounting period of the firm;

• The date of commencement of partnership;

• Profit and loss sharing ratio;

• Rate of interest on capital, loan, drawings, etc;

• Salaries, commission, etc, if payable to any partner

Importance of Partnership Deed :

Though, the law does not make it mandatory (compulsory) for every firm to have a partnership deed, it is desirable to have it due to the following reasons :

(i) It regulates the rights, duties and liabilities of each partner.

(ii) It helps to avoid any misunderstanding amongst the partners because all the terms and conditions of partnership have been laid down before hand in the deed.

(iii) Any dispute amongst the partners may be settled easily as the partnership deed may be readily referred to.

Hence, it is always the best course to have a written partnership deed duly signed by all the partners and registered under the Act.

Rules in absence of Partnership Deed

1. profits and losses of the firm are to be shared equally

2. no Interest on Capital

3. no Interest on Drawings

4. Interest on Advances or on partner loan will be @ 6%p.a.

5. No partner is entitled to get salary or other remuneration

6. Without the consent of all existing partners no new partner can be admitted to the firm. 7. Each partner can participate in the conduct of business 8. Each partner can inspect the books of firm and can take a copy of the same.

Final accounts of a partnership firm

1. Trading and P&L a/c (not in syllabus) - profits will be given

2. P&L Appropriation A/c

3. Balance sheet (not in syllabus)

4. Partner’s capital a/c

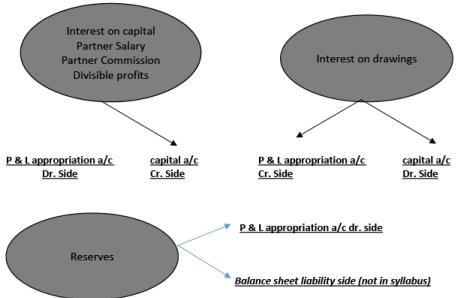

P&L Appropriation A/c

Meaning – Profit and Loss Appropriation Account’ records all the entries for interest on capital, interest on drawing, salary to partners and division of profits among the partners

Nature of Profit and Loss Appropriation Account’-

Nominal account

Purpose of preparing of P&L Appropriation A/c

1. Records all the expenses related to the partners-

Partner salary (remuneration)

Partner commission

Interest on capital

2. Records all the incomes related to the partners

Interest on drawings

3. Record all adjustments on profits

Transfer money to Reserves

Distribution of profits on the basis of profit sharing ratio.

Specimen of P&L Appropriation A/c

P&L Appropriation A/c | |||

Particulars | Rs. | Particulars | Rs. |

To salary | XXXX | By NP or P & L a/c (transferred from P&L -a/c) - IPL - M.COMM - RENT(OTHER P& LEXPENSES) | |

To partners commission | XXXX | By interest on drawings | XXXX |

To interest on capital a/c - | XXXX | ||

To reserves | |||

To divisible profits A XXXX B XXXX | XXXX | ||

All XXXX items shows that these will be transferred to the cross i.e. opposite side of capital a/c.

Important points for P&L Appropriation a/c

1. Prepared only at the time of profits (so in-case of losses this account will not be prepared)

2. Follow the rule of nominal a/c

3. The profits should be after deducting all the items of P&L a/c – mainly interest on partner loan, manager commission & rent.

Journal entries that are passed for various items shown in the above Profit and Loss Appropriation Account are as | |

follows- | |

1. Entry for Interest on Capital :— | |

(i) On allowing Interest on Capital : | |

Interest on Capital A/c | Dr. |

To Partner's Capital A/c | |

(Interest on Capital at ....% p.a.) | |

(ii) On closure of Interest on Capital A/c : | |

Profit & Loss Appropriation A/c | Dr. |

To Interest on Capital A/c | |

2. Entry for Interest on Drawings :— | |

zew | |

3. Entry for Salary or Commission Payable to a Partner :— | |

(i) On allowing salary or Commission to a partner : Partner's Salary/Commission A/c | Dr. |

To Partner's Capital A/c | |

(ii) On closure of salary or commission account : | |

Profit & Loss Appropriation A/c | Dr. |

To Partner's Salary/Commission A/c | |

4. Entry for transferring a part of profit to Reserve : | |

Profit & Loss Appropriation A/c To Reserve A/c | Dr. |

5. Entry for transfer of Credit balance of Profit & Loss Appropriation A/c (being profit) :- | |

Profit & Loss Appropriation A/c | Dr. |

To Partner's Capital or Current A/c's ( to be distributed in the ratio) | _ |

Accounting treatment of various items of P&L appropriation a/c

Distinction between Profit & Loss Account and Profit & Loss Appropriation Account:

| Profit & Loss Account | Profit & Loss Appropriation Account |

| 1. It is prepared after Trading Account and hence starts with the gross profit disclosed by Trading Account. | 1. It is prepared after Profit and Loss Account and hence starts with the net profit disclosed by Profit & Loss Account. |

| 2. It is prepared to ascertain net profit or net loss. | 2. It is prepared to distribute, the net profit of the year among the partners. |

| 3. This account has neither opening balance nor closing balance. | 3. This account may have opening as well as closing balances. |

| 4. Expenses debited to this account are charge against profits. | 4. Items debited to this account are appropriation of profits. |

| 5. This account is not prepared on the basis of partnership agreement, except for interest on loan from partners. | 5. This account is prepared on the basis of partnership agreement. |

| 6. Matching principle (i.e. matching of revenue against expenses) is followed while preparing this account. | 6. Matching principle is not followed while preparing this account. |

All adjustments of Profit & Loss Appropriation Account are an Appropriation out of Profit and are not a Charge Against Profit

Meaning of an Appropriation

Appropriations are made only when there is profit and is debited to Profit and Loss Appropriation Account. ExInterest on capital, partner’s salary etc.

Meaning of charge Against Profit –

Charge means the expenses which will be deducted from profits while calculating net profit or loss and is debited to Profit and Loss Account. Ex- Interest on partner’s loan and rent paid to a partner It is necessary to make charges against profits even if there is loss.

Distinction between Charge Against Profit and Appropriation out of Profit

| Basis of Distinction | Charge Against Profit | Appropriation Out of Profit | |

| 1. | Nature | It indicates expenses to be deducted from profits while calculating net profit or loss. | It indicates distribution of net profit to various heads. |

| 2. | Recording | It is debited to Profit and Loss Account | It is debited to Profit and Loss Appropriation Account. |

| 3. | Necessary or not | It is necessary to make charges against profits even if there is loss. | Appropriations are made only when there is profit. |

| 4. | Example | Interest on partner’s loan and rent paid to a partner. | Interest on capital, partner’s salary etc. |

|

79 docs|41 tests

|

FAQs on Partnership Deed - Crash Course of Accountancy - Class 12 - Commerce

| 1. What is a partnership deed in commerce? |  |

| 2. Why is a partnership deed important in commerce? | |

| 3. How can one create a partnership deed in commerce? | |

| 4. Can a partnership deed be modified or amended? | |

| 5. What happens if a partnership deed is not in place in a commerce partnership? | |

|

1.5K Views |

|

4.69/5 Rating |

|

Dec 26, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

video lectures

,Viva Questions

,MCQs

,study material

,past year papers

,Partnership Deed | Crash Course of Accountancy - Class 12 - Commerce

,Sample Paper

,Important questions

,Summary

,Exam

,shortcuts and tricks

,mock tests for examination

,Semester Notes

,ppt

,Objective type Questions

,practice quizzes

,Extra Questions

,Partnership Deed | Crash Course of Accountancy - Class 12 - Commerce

,Partnership Deed | Crash Course of Accountancy - Class 12 - Commerce

,Previous Year Questions with Solutions

,Free

;

Partnership Deed Free PDF Download

Importance of Partnership Deed

Partnership Deed Notes

Partnership Deed Commerce Questions

Study Partnership Deed on the App

|

© EduRev

|

Education Revolution

|

|