Basic Concepts: Profit, Loss & Discount

Introduction

- The profit and loss formula is used in mathematics to determine the price of a commodity in the market and to understand how profitable a business is.

- Every product has a cost price and a selling price.

- Based on these prices, we calculate the profit gained or the loss incurred on a particular product.

- Problems typically involve applying percentage concepts, successive changes, and sometimes special cases such as dishonest dealers or false weights.

Basic Terms

Cost Price (CP)

The amount paid by a seller to purchase or produce a product or commodity is called the cost price, denoted as CP. Costs can be classified:

- Fixed cost: Remains constant and does not vary with the quantity produced or sold (for example, rent, salaried wages).

- Variable cost: Varies with the level of production or sales (for example, raw materials, piece-rate wages).

Selling Price (SP)

The amount for which a product is sold is called the selling price, denoted as SP. It is also called the sale price.

Profit and Loss

Profit: When an article is sold for more than its cost price, the difference is called profit or gain.

- Profit or Gain = S.P - C.P

Loss: When an article is sold for less than its cost price, the difference is called loss.

- Loss = C.P - S.P

The percentage measures are taken on the cost price unless otherwise stated:

- Profit percentage = (Profit / Cost price) × 100

- Loss percentage = (Loss / Cost price) × 100

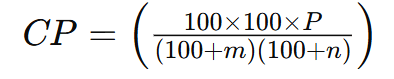

Important: If the selling price of X articles is equal to the cost price of Y articles, then the net profit percentage is given by

Solved Examples

Example 1: Brijesh purchased a book for Rs.1260 and sold it to Rakesh for Rs.1320. Rakesh sold it to Kishore for Rs.1400. Who gained more and by how much?

Sol:

For Brijesh:

Cost Price = Rs. 1260.

Selling Price = Rs. 1320.

Profit = Rs. 1320 - Rs. 1260 = Rs. 60.For Rakesh:

Cost Price = Rs. 1320.

Selling Price = Rs. 1400.

Profit = Rs. 1400 - Rs. 1320 = Rs. 80.Rakesh gained more by Rs. 80 - Rs. 60 = Rs. 20.

Therefore, Rakesh gained Rs. 20 more than Brijesh.

Example 2: If the selling price of 10 articles is the same as the cost price of 11 articles, find the profit or loss percent.

Sol:

Let the cost price of 1 article be Re. 1.

Cost Price of 10 articles = Rs. 10.

Cost Price of 11 articles = Rs. 11.

Hence, Selling Price of 10 articles = Rs. 11.

Profit = Rs. 11 - Rs. 10 = Rs. 1.

Profit percentage = (1 / 10) × 100 = 10%.Shortcut:

Here X = 10 and Y = 11, so profit percentage = ((Y - X) / X) × 100 = 10%.Note: Profit and loss percentages are always calculated with cost price as the base unless the question states otherwise.

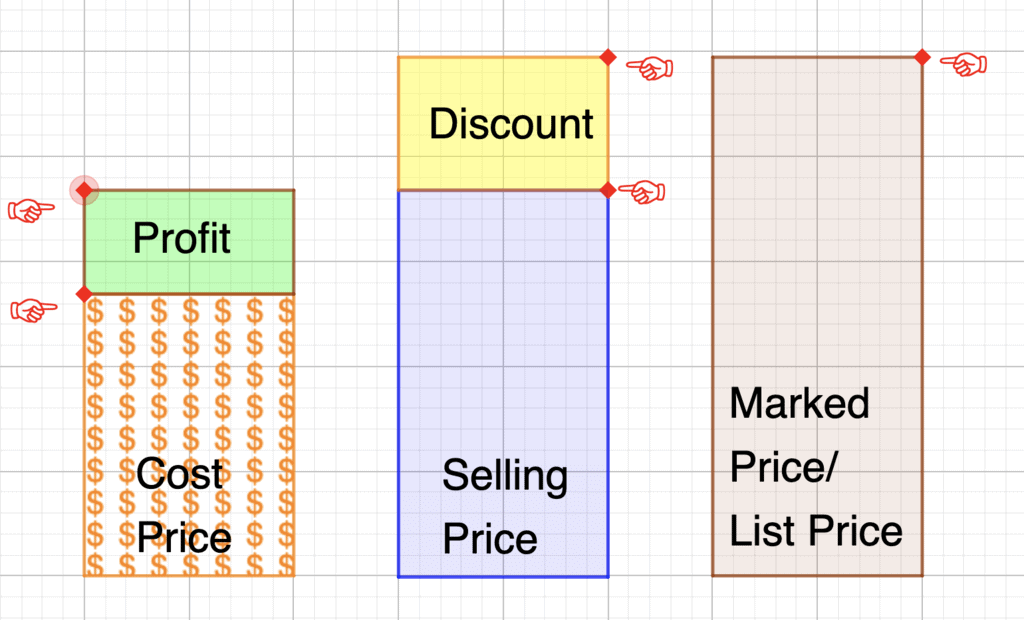

Marked Price (MP) and Markup

The marked price (MP) is the price shown by a seller on an item before any discount. Markup is the amount added to the cost price to arrive at the marked price or selling price.

- Marked Price = Cost Price + Markup

- Marked Price = Cost Price + % Markup on Cost Price

Example: If a product is bought at ₹50 and sold at ₹70, markup = ₹20 and markup percentage = (20 / 50) × 100 = 40%.

Discount

Discount is a reduction from the marked price offered to the buyer. If no discount is offered, SP = MP. If a discount d% is given, SP = MP × (1 - d/100).

- Discount = Marked Price - Selling Price

- Discount percentage = (Discount / Marked price) × 100

Types of Costs

Business costs are classified as:

- Direct / Variable costs: Vary with the number of units produced or sold (e.g., raw materials).

- Indirect / Fixed costs: Remain constant regardless of production level (e.g., rent, salaries).

- Semi-variable costs: Fixed up to a level, then increase (e.g., extra rent for larger premises).

Margin and Break-Even Point

- Margin (Contribution): The difference between the selling price of a product and its variable cost. Contribution first covers fixed costs; remaining contribution is profit.

- Break-Even Point (BEP): The level of sales where total revenue equals total cost - the business makes neither profit nor loss. Sales beyond BEP give profit.

- Formula:

Break-even sales (in units) = Fixed costs ÷ Contribution per unit

Example: Fixed costs = ₹5,000 per month. Selling price per pen = ₹5. Variable cost per pen = ₹2.5. Contribution per pen = ₹2.5.

Break-even units = 5000 ÷ 2.5 = 2000 pens.

Selling more than 2000 pens gives profit; selling fewer gives loss.

Useful relations:

- Profit = (Actual sales - Break-even sales) × Contribution per unit

- Loss = (Break-even sales - Actual sales) × Contribution per unit

Formulae to Remember

- SP = ((100 + P%) / 100) × CP

- SP = ((100 - L%) / 100) × CP

- CP = (100 / (100 + P%)) × SP

- CP = (100 / (100 - L%)) × SP

- SP = MP - Discount

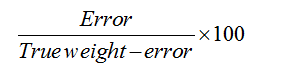

- For false weight, profit percentage P% = ((True weight - False weight) / False weight) × 100

- For two successive profits m% and n%, net profit percentage = m + n + (mn / 100)

- For one profit m% and one loss n%, net percentage ≈ m - n - (mn / 100)

- Effective CP after successive changes can be calculated by applying each percentage change multiplicatively.

- If profit percentage and loss percentage are equal (P = L), then overall % loss = P² / 100 when selling two different-cost items at same SP (special cases).

Profit and Loss Tricks

Shortcuts often used in competitive questions:

- When two successive percentage changes are applied, multiply the factors: final factor = (1 ± m/100)(1 ± n/100).

- When SP of X articles = CP of Y articles, profit% = ((Y - X) / X) × 100.

- For false weight and cheating by weight, combine percentage gain due to price and due to weight using formula: P_total = P_price + P_weight + (P_price × P_weight / 100).

The Concept of Same Selling Price with Profit or Loss

If two items are sold at the same price and one gives a profit of x% while the other gives a loss of x%, the overall result is always a loss.

Example:

- Item A: cost ₹100, sold at 20% profit → SP = ₹120.

- Item B: cost ₹150, sold at 20% loss → SP = ₹120.

Total Cost Price = ₹250. Total Selling Price = ₹240. Net loss = ₹10.

Worked example

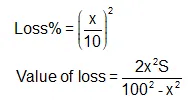

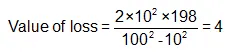

Example: Two articles are sold at Rs. 198 each, such that a profit of 10% is made on the first while a loss of 10% is incurred on the other. What would be the net profit/loss on the two transactions combined?

Sol:

Article 1: Profit = 10%, Selling Price = Rs. 198.

Cost Price = 198 ÷ 1.1 = Rs. 180.Article 2: Loss = 10%, Selling Price = Rs. 198.

Cost Price = 198 ÷ 0.9 = Rs. 220.Total Cost Price = 180 + 220 = Rs. 400.

Total Selling Price = 2 × 198 = Rs. 396.

Net loss = Rs. 400 - Rs. 396 = Rs. 4.

Specific Cases and Rules

- False weight calculation:When a seller gives less than the stated quantity, compute gain due to false weight as a percentage and combine it with price gain if any.

- Net percentage profit for successive profits:Use m + n + (mn / 100).

- Net percentage for a profit and a loss:Use m - n - (mn / 100) when one is profit and the other a loss.

- Effective cost price after successive profits:Work backward by dividing by (1 + percent/100) for each profit or multiplying by (1 - percent/100) for losses.

MULTIPLE CHOICE QUESTION

MULTIPLE CHOICE QUESTIONTry yourself: A shopkeeper bought a bag for Rs. 800 and sold it for Rs 1000. What is the profit percentage earned by the shopkeeper?

Dishonest Dealer

- A dishonest dealer may give less weight or measure, overstate discounts, or combine tactics to appear to offer value while actually earning hidden gains.

- When a shopkeeper gains G% overall while cheating by weight or measure, relationships between true weight and false weight can be used to find the actual gain. For many combined gain/loss situations, use the combined-percentage formula: P_total = P1 + P2 + (P1 × P2 / 100).

- When a shopkeeper sells at cost price but gives short weight, the effective gain can be found from the ratio of true weight to false weight.

Worked example - dishonest dealer:

Example: Let a dishonest shopkeeper sell sugar at Rs 18/kg, which he has bought at Rs 15/kg and he is giving 800 g instead of 1000 g. Find his actual profit percentage.

Sol:

Cost price of sugar = Rs. 15 per kg.

Selling price (per labelled kg) = Rs. 18.

Profit per kg ignoring false weight = 18 - 15 = Rs. 3.

Profit percentage ignoring false weight = (3 / 15) × 100 = 20%.

Because the shopkeeper gives 800 g instead of 1,000 g, there is additional gain due to false weight:

Gain due to false weight = ((1000 - 800) / 800) × 100 = (200 / 800) × 100 = 25%.Overall profit percentage = 20 + 25 + (20 × 25 / 100) = 20 + 25 + 5 = 50%.

Alternate method:

Cost of 800 g = 15 × (800 / 1000) = Rs. 12.

He sells 800 g for Rs. 18, so profit = 18 - 12 = Rs. 6.

Profit percentage = (6 / 12) × 100 = 50%.

Both methods give the same answer; the formula P + Q + (PQ/100) is convenient.

Note: If losses appear in any part, enter them as negative percentages in the combined formula.

Profit Calculation Based on Amount Spent and Amount Earned

Profit or loss is usually calculated by comparing the money spent (total cost) and the money earned (total revenue), especially when the number of items bought and sold differs or some items remain unsold.

When a seller recovers the total money spent before selling all items, the unsold items may be treated as implicit profit depending on the situation.

Solved Problems

These examples apply the concepts to everyday retail scenarios and competitive-exam style questions.

Example 1: Now, suppose a student shows up and wants to buy 5 gel pens worth ₹5 each. The cost price of one pen is ₹4. So, what is the profit earned by the shopkeeper in net terms and its profit percentage?

Sol:

Selling Price (SP) = ₹5 per pen.

Cost Price (CP) = ₹4 per pen.

Profit per pen = SP - CP = ₹5 - ₹4 = ₹1.

Therefore, profit percentage = (Profit / CP) × 100Total profit on 5 pens = 5 × ₹1 = ₹5.

Example 2: Suppose another customer comes to the shop and buys 2 registers worth ₹50 each and a pencil box from him. The shopkeeper has earned 40% profit on the registers. He earned a profit of ₹10 on the pencil box, and the profit % on the pencil box is 20%. Then what is the cost price and profit on the register, and the selling price and cost price of the pencil box?

Sol:

For the registers:

Given S.P. = ₹50 and profit% = 40% (profit on cost price).

Let C.P. = x.

Profit% = ((50 - x) / x) × 100 = 40.

Therefore, (50 - x) / x = 0.4.

So 50 - x = 0.4x.

Therefore 50 = 1.4x.

x = 50 ÷ 1.4 = ₹35.714... ≈ ₹35.71.

Profit per register = 50 - 35.71 = ₹14.29 (approx).

Alternate interpretation: If profit 40% is stated on selling price, then profit = 0.4 × 50 = ₹20 and C.P. = 50 - 20 = ₹30. Check the question context to choose the correct base. Here we used profit percent on cost price.

For the pencil box:

Given profit = ₹10 and profit% = 20% on cost price.

Let C.P. = y.

Then (10 / y) × 100 = 20 ⇒ 10 / y = 0.2 ⇒ y = 10 ÷ 0.2 = ₹50.

Selling price = 50 + 10 = ₹60.

Example 3: The shopkeeper puts up a discount of 20% on all products. A customer bought a packet of pencils and 3 erasers, still giving the shopkeeper a profit of 30% on both items. What is the actual cost price of both items when the pencil packet is marked as ₹30 and the eraser ₹5 each?

What does the underlined marked mean?

Here marked means Marked Price is the price that is offered to customer before discount basically, discount is just difference between marked price and Selling price i.e. Discount = M.P. - S.P.

Sol:

Marked Price of pencil packet = ₹30. Discount = 20% of 30 = ₹6.

Selling Price of pencil packet = 30 - 6 = ₹24.

Profit = 30% on cost price. Let cost price = x.

Profit% = (24 - x) / x = 0.3.

Therefore 24 - x = 0.3x ⇒ 24 = 1.3x ⇒ x = 24 ÷ 1.3 = ₹18.4615... ≈ ₹18.46.

For 3 erasers: Marked price each = ₹5, so marked price for 3 = ₹15.

Discount on 3 erasers = 20% of 15 = ₹3.

Selling Price for 3 erasers = 15 - 3 = ₹12.

Profit% = 30% on cost price. Let cost price for 3 erasers = y.

Then (12 - y) / y = 0.3 ⇒ 12 = 1.3y ⇒ y = 12 ÷ 1.3 = ₹9.2307... ≈ ₹9.23.

Example 4: The stationery sold a Parker pen at a loss of 20% for ₹100 and a pack of coloured sketch pens at a loss of 15% on S.P. What are the cost price and selling price of both the articles?

Sol:

For the Parker pen: Loss is 20% on cost price.

Let C.P. = x. S.P. = 100.

S.P. = 0.8 × C.P.

So 100 = 0.8x ⇒ x = 100 ÷ 0.8 = ₹125.

For the sketch pens: Loss is 15% on S.P.

Let S.P. = y and C.P. = 100 (given in the method used here). If loss is 15% on S.P., then C.P. = S.P. + loss = S.P. + 0.15 S.P. = 1.15 S.P.

If we take C.P. = 100 for calculation, then 100 = 1.15y ⇒ y = 100 ÷ 1.15 ≈ ₹87 (approx).

Interpretation depends on which base the problem gives; follow the wording carefully to set equations correctly.

Example 5: A watch dealer incurs an expense of Rs. 150 for producing every watch. He also incurs an additional expenditure of Rs. 30,000, which is independent of the number of watches produced. If he is able to sell a watch during the season, he sells it for Rs. 250. If he fails to do so, he has to sell each watch for Rs. 100. If he is able to sell only 1,200 out of 1,500 watches he has made in the season, then he has made a profit of:

(a) ₹90000

(b) ₹75000

(c) ₹45000

(d) ₹60000

[CAT 2016]

Sol:

Total number of watches produced = 1,500.

Production cost per watch = ₹150.

Additional fixed expenditure = ₹30,000.

Total cost = (1,500 × 150) + 30,000 = 225,000 + 30,000 = ₹255,000.

Watches sold during season = 1,200 at ₹250 each ⇒ revenue = 1,200 × 250 = ₹300,000.

Remaining watches = 300 sold off-season at ₹100 each ⇒ revenue = 300 × 100 = ₹30,000.

Total revenue = 300,000 + 30,000 = ₹330,000.

Profit = Revenue - Cost = 330,000 - 255,000 = ₹75,000.

Answer: (b) ₹75,000.

Example 6: Instead of a metre scale, a cloth merchant uses a 120 cm scale while buying, but uses an 80 cm scale while selling the same cloth. If he offers a discount of 20% on cash payment, what is his overall profit percentage?

Sol:

Assume the cloth is priced at ₹1 per cm (marked price per actual cm for simplicity).

When buying with a 120 cm scale, the merchant pays for 120 cm but actually receives 100 cm. Effective cost per actual cm = 100 / 120 = ₹0.8333 per cm.

When selling, he uses an 80 cm scale as if it were 100 cm: he gives only 80 cm for the price of 100 cm. Thus, his marked selling rate per actual cm before discount is (100 / 80) times the unit price.

He offers 20% discount on the marked selling price, so selling price per actual cm becomes:

S.P. per actual cm = (100/80) × unit price × (1 - 0.20) = 1 × unit price = ₹1 per cm.

Therefore S.P. per actual cm = ₹1 and C.P. per actual cm = ₹0.8333.

Profit% = ((1 - 0.8333) / 0.8333) × 100 ≈ 20%.

Try yourself: A shopkeeper sells a pen at a loss of 10%. If the cost price of the pen is Rs20, what is the selling price of the pen?

FAQs on Basic Concepts: Profit, Loss & Discount

| 1. What's the difference between cost price and selling price in profit and loss questions? |  |

| 2. How do I calculate profit percentage and loss percentage correctly? | |

| 3. What's the relationship between marked price and selling price when a discount is given? | |

| 4. Can I make a profit even after giving a discount to customers? | |

| 5. How do successive discounts work differently from single discounts? | |