Depreciation - (Part- 3) | Accountancy Class 11 - Commerce PDF Download

Page No 14.50:

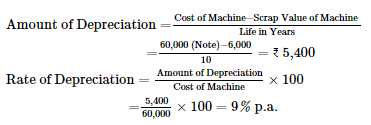

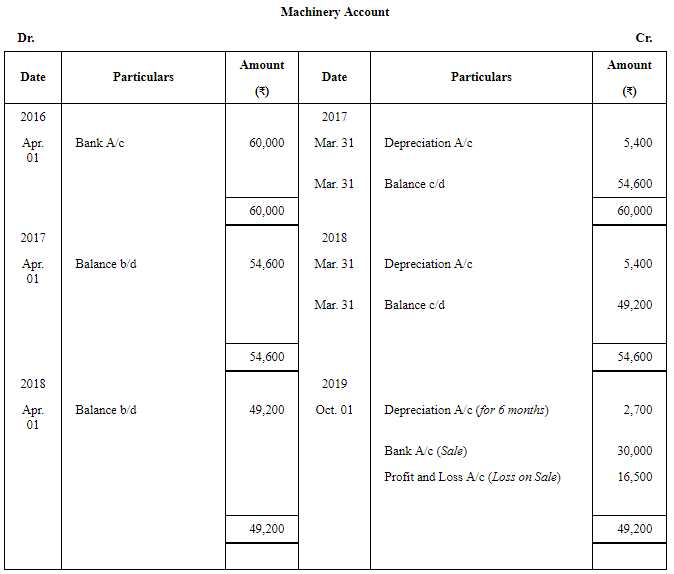

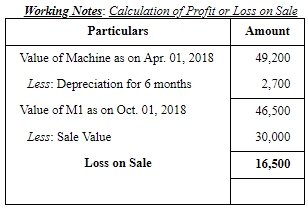

Question 11: On 1st April, 2016, Shivam Enterprise purchased a second-hand machinery for ₹ 52,000 and spent ₹ 2,000 on cartage, ₹ 3,000 on unloading, ₹ 2,000 on installation and ₹ 1,000 as brokerage of the middle man. It was estimated that the machinery will have a scrap value of ₹ 6,000 at the end of its useful life, which is 10 years. On 31st December 2016, repairs and renewals amounted to ₹ 2,500 were paid. On 1st October, 2018, this machine was sold for ₹ 30,600 and an amount of ₹ 600 was paid as commission to an agent.

Calculate the amount of annual depreciation and rate of depreciation. Also prepare the Machinery Account for first 3 years, assuming that firm follows financial year for accounting.

ANSWER:

Note:

1. All the expenses incurred up to the date at which machine is put in use will be added to cost of machine.

2. The amount spent on repairs is a recurring nature expenses. So, it will not be added to Machine A/c.

3. Cost of Machine = 52,000 + 2,000 + 3,000 + 2,000 + 1,000 = Rs 60,000

Page No 14.51:

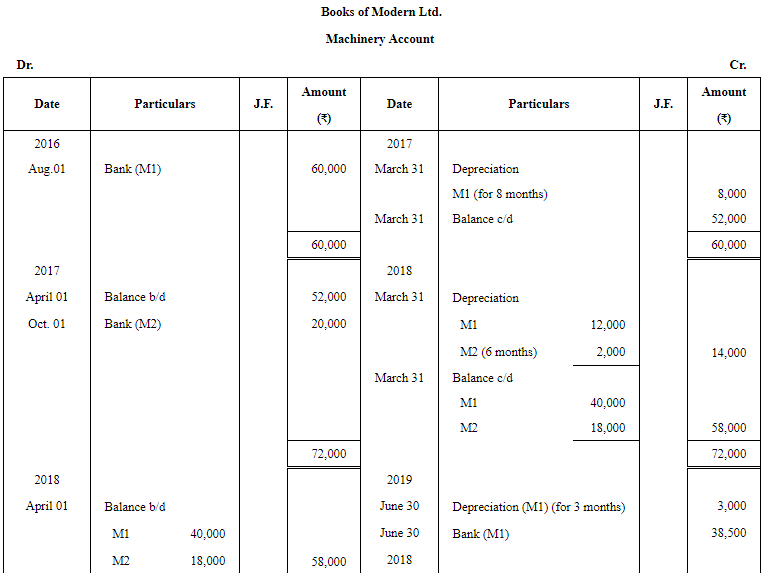

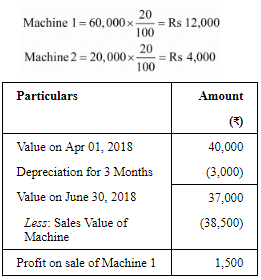

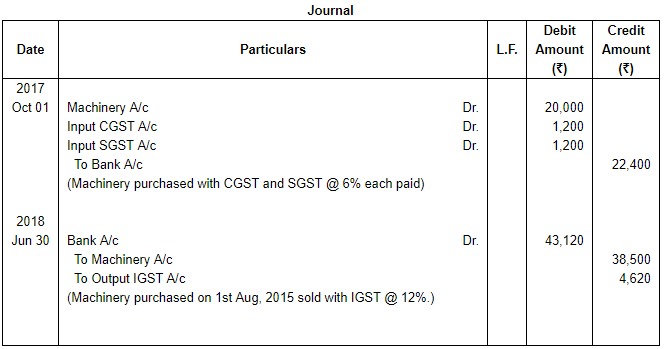

Question 12: Modern Ltd. purchased a machinery on 1st August, 2016 for ₹ 60,000. On 1st October, 2017, it purchased another machine for ₹ 20,000 plus CGST and SGST @ 6% each. On 30th June, 2018, it sold the first machine purchased in 2016 for ₹ 38,500 charging IGST @ 12%. Depreciation is provided @ 20% p.a. on the original cost each year. Accounts are closed on 31st March every year. Prepare the Machinery Account for three years.

ANSWER:

Working Notes

Working Notes

1. Calculation of Annual Depreciation

3. Journal entries for purchase and sale with GST

Page No 14.51:

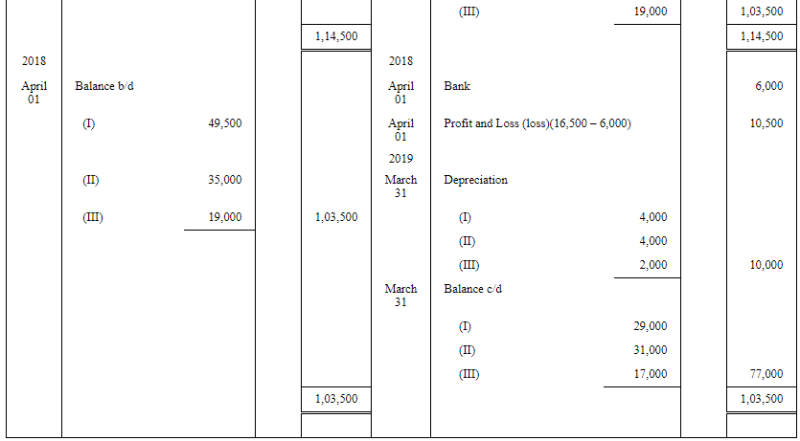

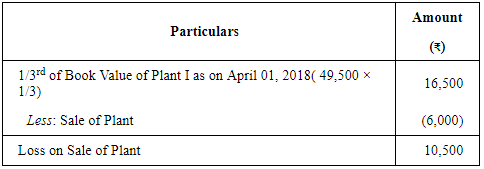

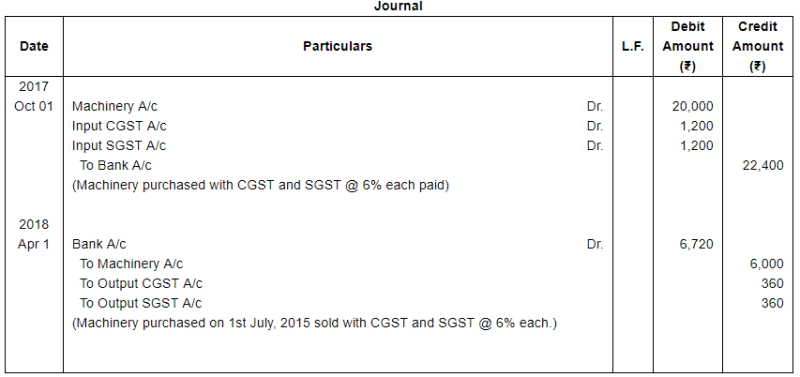

Question 13: On 1st July, 2016, Sohan Lal & Sons purchased a plant costing ₹ 60,000. Additonal plant was purchased on 1st January, 2017 for ₹ 40,000 and on 1st October, 2017, for ₹ 20,000, plus CGST and SGST @ 6% each. On 1st April, 2018, one-third of the plant purchased on 1st July, 2016, was found to have become obsolete and was sold for ₹ 6,000, charging CGST and SGST @ 6% each.

Prepare the Plant Account for the first three years in the books of Sohan Lal & Sons. Depreciation is charged @ 10% p.a. on Straight Line Method. Accounts are closed on 31st March each year.

ANSWER:

Working Notes

1. Calculation of Depreciation

2. Calculation of profit or loss on Sale of Plant I

3. Journal entries for purchase and sale with GST

Page No 14.51:

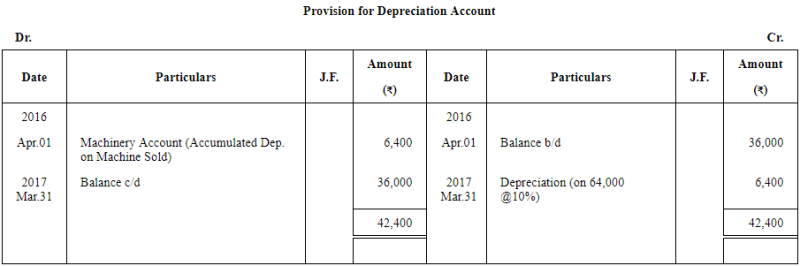

Question 14: Following balances appear in the books of Rama Bros:

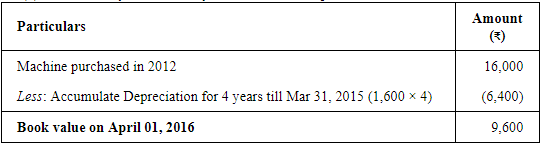

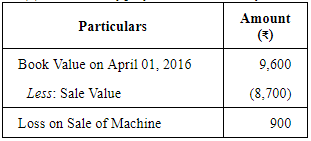

On 1st April, 2016, they decided to sell a machine for ₹ 8,700. This machine was purchased for ₹ 16,000 in April, 2012. Prepare the Provision for

Depreciation Account and Machinery Account on 31st March, 2017, assuming the firm has been charging Depreciation at 10% p.a. on Straight Line Method.

ANSWER:

Working Notes

Working Notes

(1) Calculation of Book Value of Machine Sold on April 01, 2015

(2)Calculation of profit or loss on Sale of Machine

Page No 14.51:

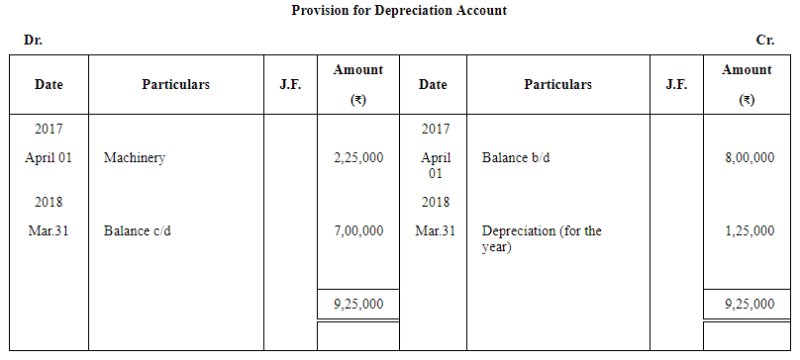

Question 15: Following balances appear in the books of Priyank Brothers:

On 1st April, 2017, they decide to sell a machine for ₹ 5,00,000. This machine was purchased for ₹ 7,50,000 on 1st April, 2014. Prepare the Machinery Account and Provision for Depreciation Account for the year ended 31st March, 2018 assuming that the firm has been charging Depreciation @ 10% p.a. on the Straight Line Method.

ANSWER:

Working Notes

Working Notes

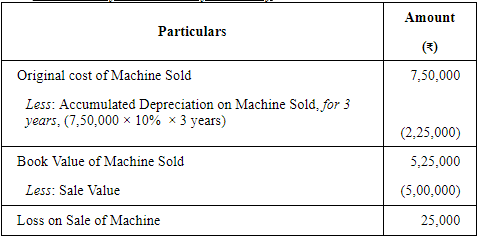

1 Calculation of Loss on Sale of Machinery

|

61 videos|226 docs|39 tests

|

FAQs on Depreciation - (Part- 3) - Accountancy Class 11 - Commerce

| 1. What is depreciation and why is it important in commerce? |  |

| 2. How is depreciation calculated for accounting purposes? | |

| 3. What is the difference between depreciation and amortization? | |

| 4. Can depreciation be reversed or adjusted in the future? | |

| 5. How does depreciation impact a company's taxes? | |

Sample Paper

,Viva Questions

,shortcuts and tricks

,Important questions

,Depreciation - (Part- 3) | Accountancy Class 11 - Commerce

,Depreciation - (Part- 3) | Accountancy Class 11 - Commerce

,practice quizzes

,past year papers

,Previous Year Questions with Solutions

,study material

,MCQs

,Semester Notes

,mock tests for examination

,Exam

,Free

,Objective type Questions

,Summary

,ppt

,video lectures

,Extra Questions

,Depreciation - (Part- 3) | Accountancy Class 11 - Commerce

;

Depreciation - (Part- 3) Free PDF Download

Importance of Depreciation - (Part- 3)

Depreciation - (Part- 3) Notes

Depreciation - (Part- 3) Commerce Questions

Study Depreciation - (Part- 3) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!