Dissolution of a Partnership Firm ( Part - 3) | Accountancy Class 12 - Commerce PDF Download

Page No 7.63:

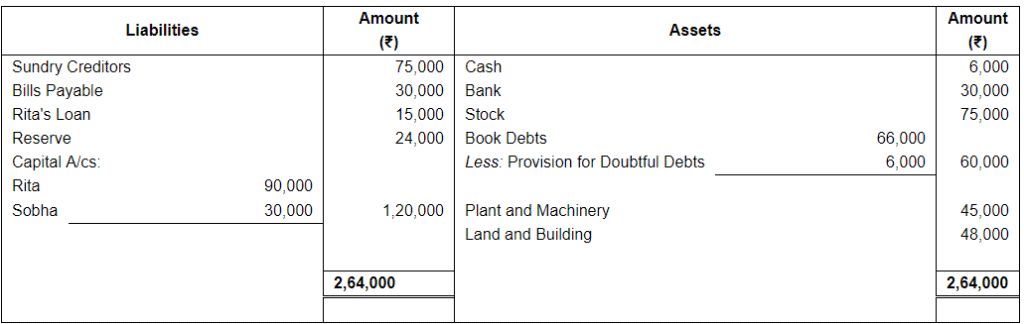

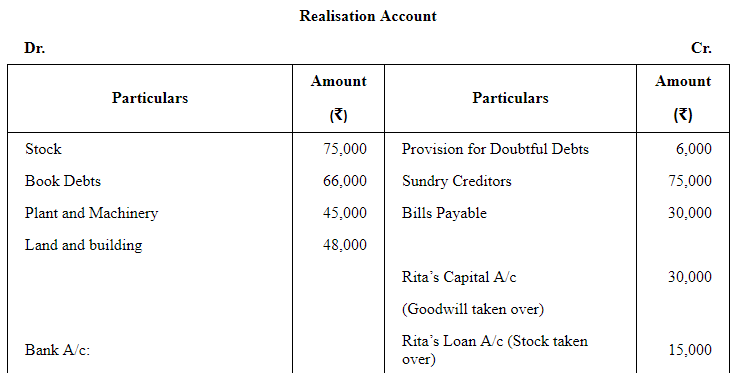

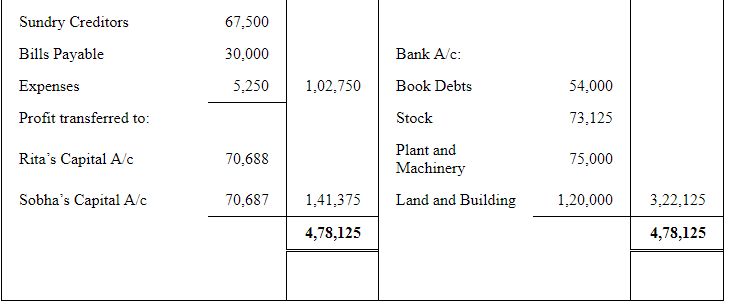

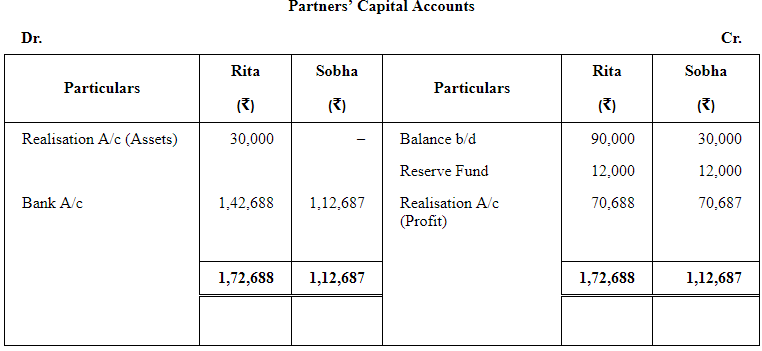

Question 35:

Rita and Sobha are partners in a firm, Fancy Garments Exports, sharing profits and losses equally. On 1st April, 2019, the Balance Sheet of the firm was:

The firm was dissolved on the date given above. The following transactions took place:

(a) Rita took 25% of the Stock at a discount of 20% in settlement of her loan.

(b) Book Debts realised ₹ 54,000; balance of the Stock was sold at a profit of 30% on cost.

(c) Sundry Creditors were paid out at a discount of 10%. Bills Payable were paid in full .

(d) Plant and Machinery realised ₹ 75,000. Land and Building ₹ 1,20,000.

(e) Rita took the goodwill of the firm at a value of ₹ 30,000.

(f) An unrecorded asset of ₹ 6,900 was handed over to an unrecorded liability of ₹ 6,000 in full settlement.

(g) Realisation expenses were ₹ 5,250.

Show Realisation Account, Partners' Capital Accounts and Bank Account in the books of the firm.

ANSWER:

Working Notes:

WN1: Value of Stock Taken Over by Rita

[Since stock is taken over at a discount of 20%]

WN2: Value of Stock Sold

Book Value of Balance of Stock Sold=Value of Stock − Stock Taken over by Rita

Book Value of Balance of Stock Sold=₹(75,000 − 18,750)= ₹56,250

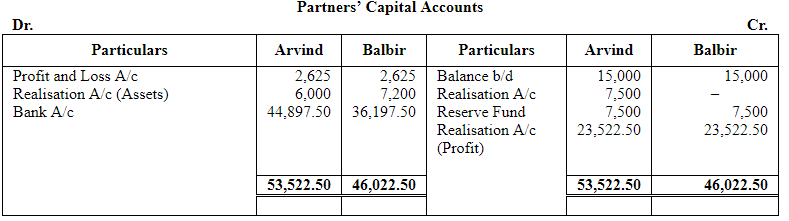

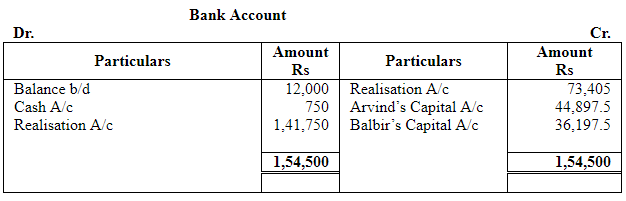

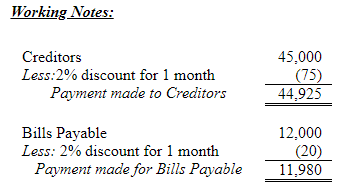

Page No 7.63:

Question 36:

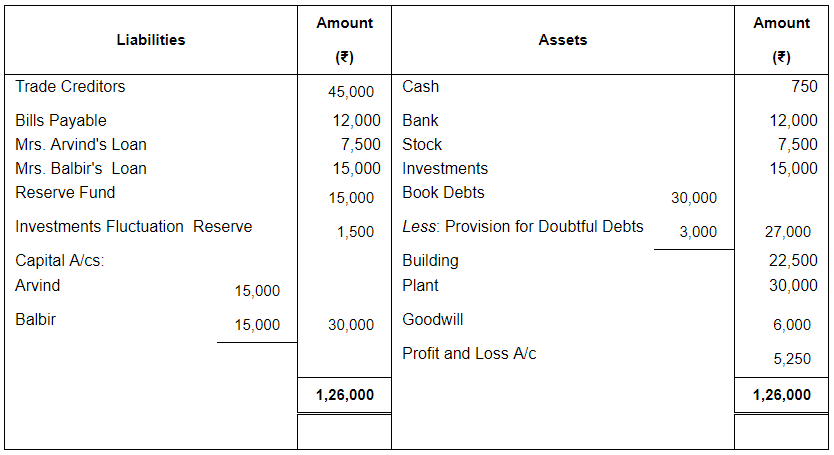

Following is the Balance Sheet of Arvind and Balbir as at 31st March, 2019:

The firm was dissolved on the above date under the following arrangement:

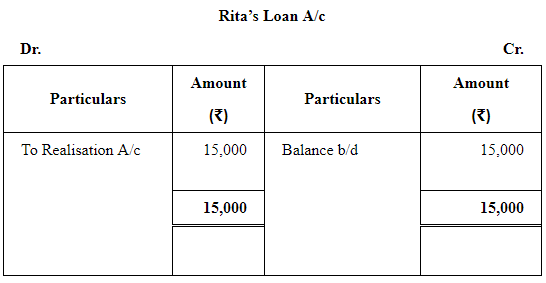

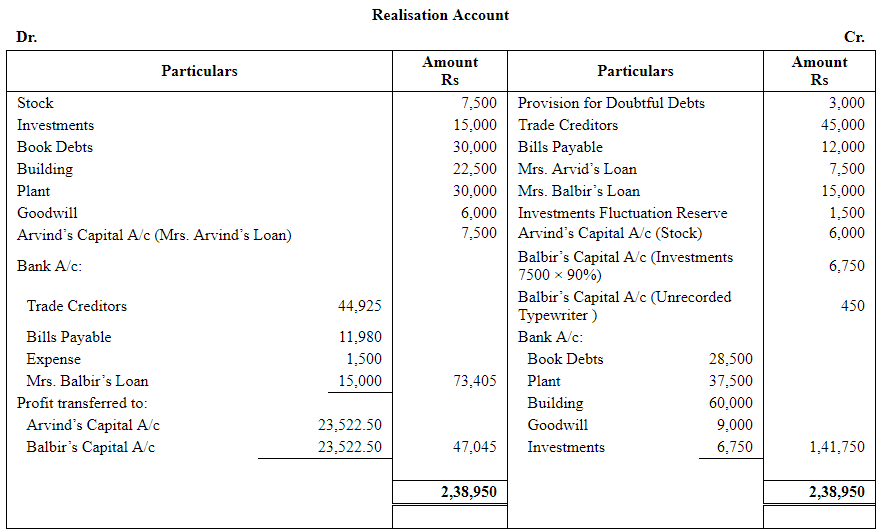

(a) Arvind promised to pay off Mrs. Arvind's Loan and took Stock at ₹ 6,000.

(b) Balbir took half the Investments @ 10% discount.

(c) Book Debts realised ₹ 28,500.

(d) Trade Creditors and Bills Payable were due on average basis of one month after 31st March, but were paid immediately on 31st March @ 2% discount per annum.

(e) Plant realised ₹ 37,500; Building ₹ 60,000; Goodwill ₹ 9,000 and remaining Investments ₹ 6,750.

(f) An old typewriter, written off completely from the firm's books, now estimated to realise ₹ 450. It was taken by Balbir at this estimated price.

(g) Realisation expenses were ₹ 1,500.

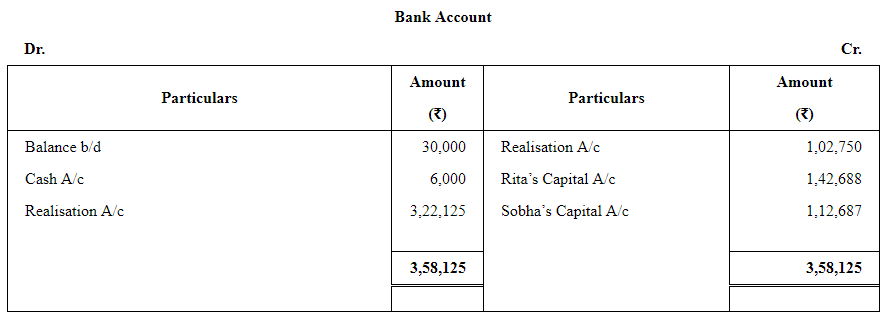

Show Realisation Account, Capital Accounts of Partners and Bank Account.

ANSWER:

Page No 7.64:

Question 37:

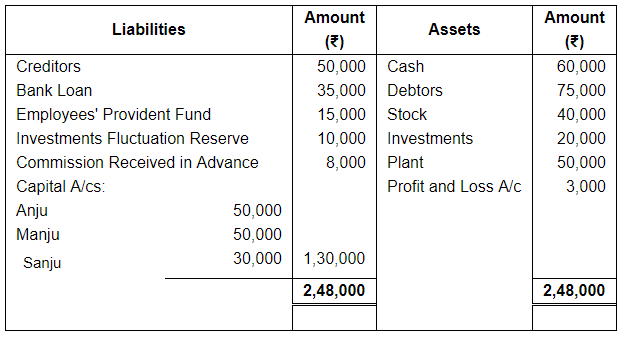

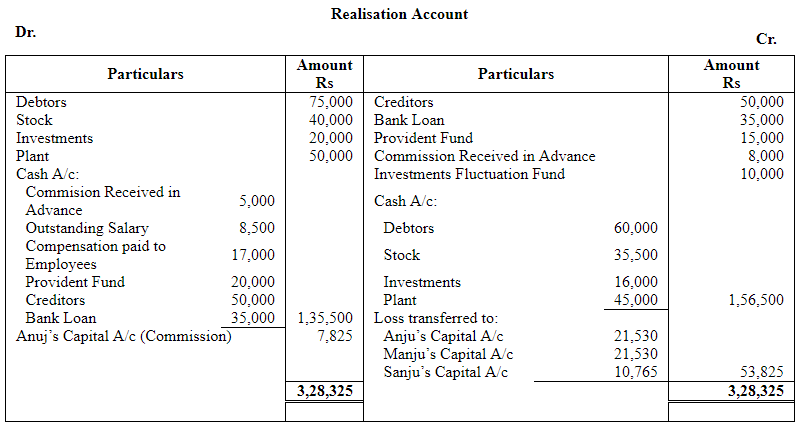

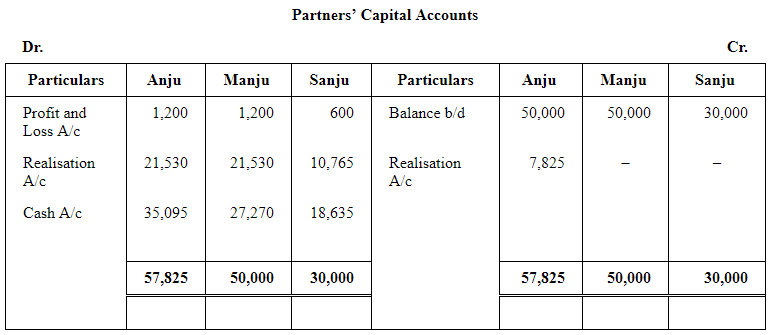

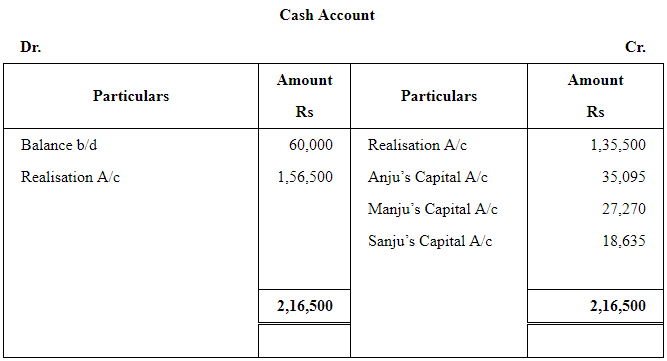

Anju, Manju and Sanju were partners in a firm sharing profits in the ratio of 2 : 2 : 1. On 31st March, 2019, their Balance Sheet was:

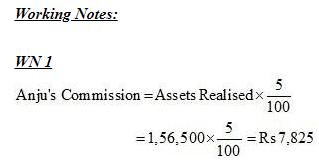

On this date, the firm was dissolved. Anju was appointed to realise the assets. Anju was to receive 5% commission on the sale of assets (except cash) and was to bear all expenses of realisation.

Anju realised the assets as follows: Debtors ₹ 60,000; Stock ₹ 35,500; Investments ₹ 16,000; Plant 90% of the book value. Expenses of Realisation amounted to ₹ 7,500. Commission received in advance was returned to customers after deducting ₹ 3,000.

Firm had to pay ₹ 8,500 for Outstanding Salary, not provided for earlier, Compensation paid to employees amounted to ₹ 17,000. This liability was not provided for in the above Balance Sheet. ₹ 20,000 had to be paid for Employees' Provident Fund.

Prepare Realisation Account, Capital Accounts of Partners and Cash Account.

ANSWER:

Page No 7.64:

Question 38:

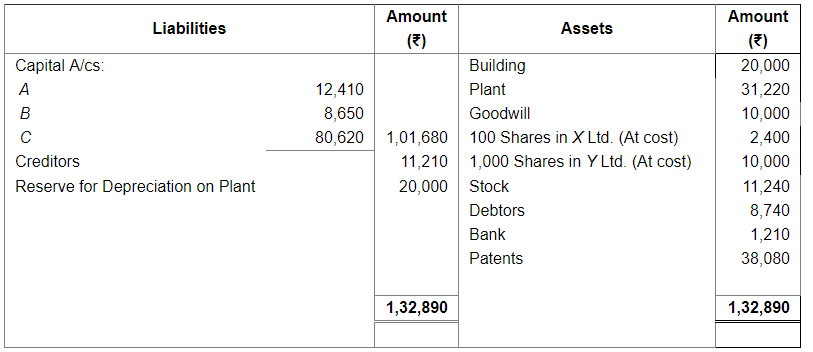

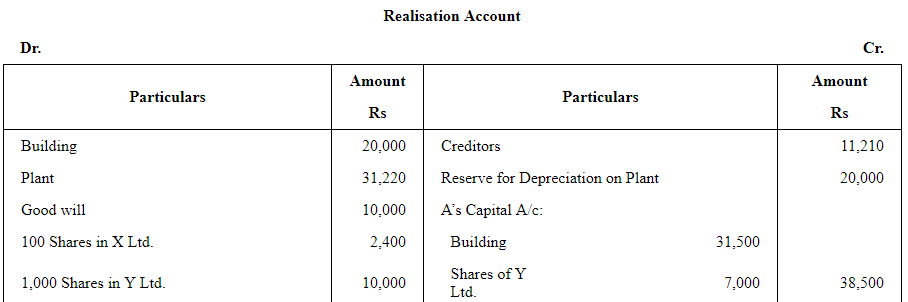

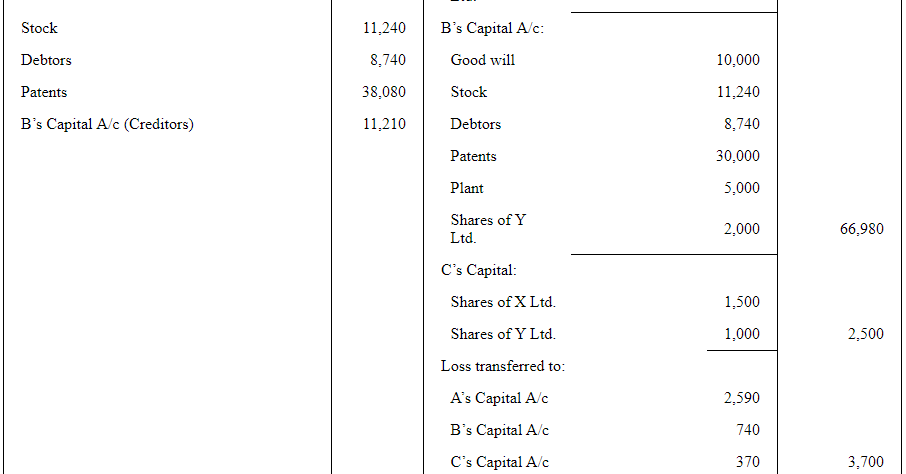

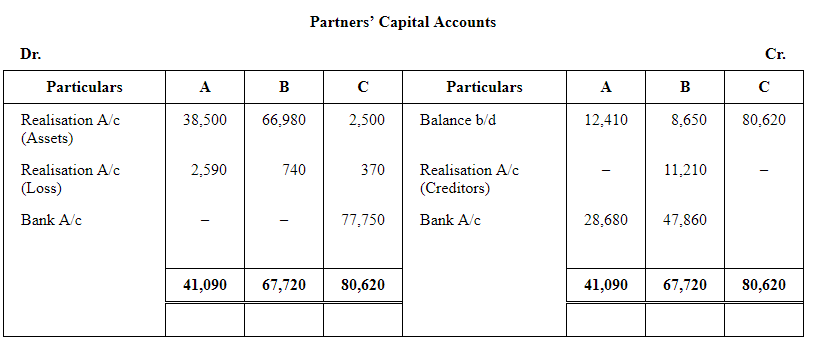

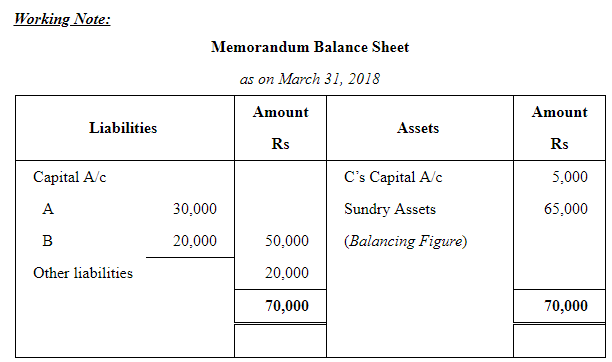

A, B and C were in partnership sharing profits in the ratio of 7 : 2 : 1 and the Balance Sheet of the firm as at 31st March, 2019 was:

It was agreed to dissolve the partnership as on 31st March, 2019 and the terms of dissolution were−

(a) A to take over the Building at an agreed amount of ₹ 31,500.

(b) B, who was to carry on the business, to take over the Goodwill, Stock and Debtors at book value, the Patents at ₹ 30,000 and Plant at ₹ 5,000. He was also to pay the Creditors.

(c) C to take over shares in X Ltd. at ₹ 15 each.

(d) The shares in Y Ltd. to be divided in the profit-sharing ratio.

Show Ledger Accounts recording the dissolution in the books of the firm.

ANSWER:

Working Notes:

Distribution of Shares in Y Ltd.

Distribution of shares in Y Ltd. among the partners

Page No 7.65:

Question 39:

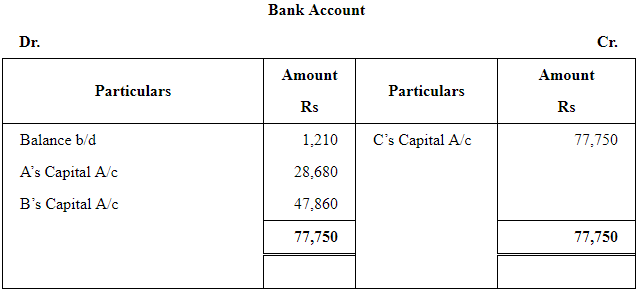

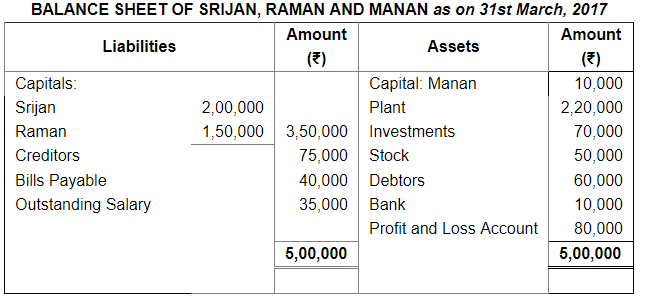

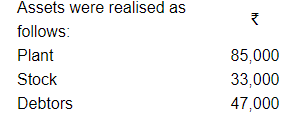

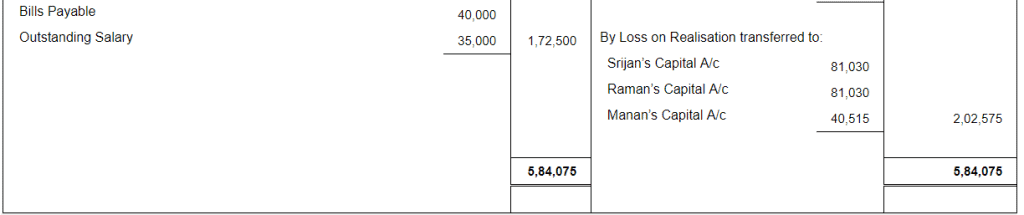

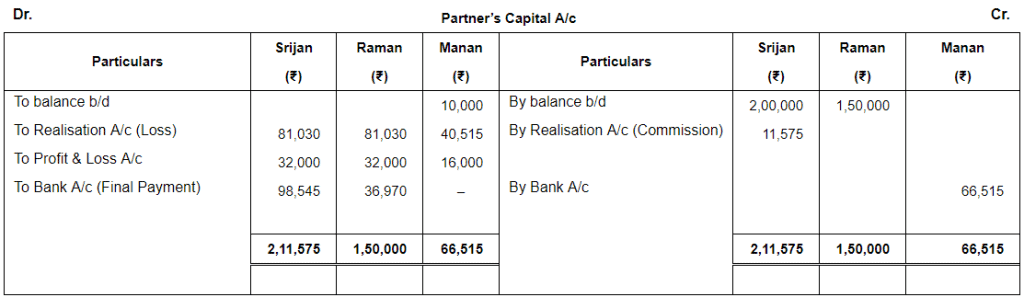

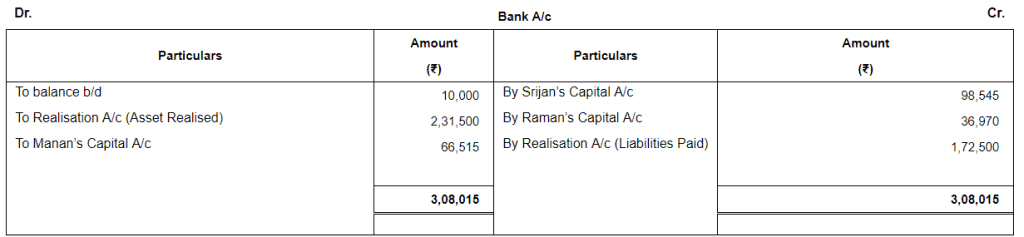

Srijan, Raman and Manan were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. On 31st, March, 2017 their Balance Sheet was as follows:

On the above date they decided to dissolve the firm.

(a) Srijan was appointed to realise the assets and discharge the liabilities. Srijan was to receive 5% commission on sale of assets (except cash) and was to bear all expenses of realisation.

(b)

(c) Investments were realised at 95% of the book value.

(d) The firm had to pay ₹ 7,500 for an outstanding repair bill not provided for earlier.

(e) A contingent liabillity in respect of bills receivable, discounted with the bank had also materialised and had to be discharged for ₹ 15,000.

(f) Expenses of realisation amounting to ₹ 3,000 were paid by Srijan.

Prepare Realisation Account, Partners' Capital Accounts and Bank Account.

ANSWER:

Question 40:

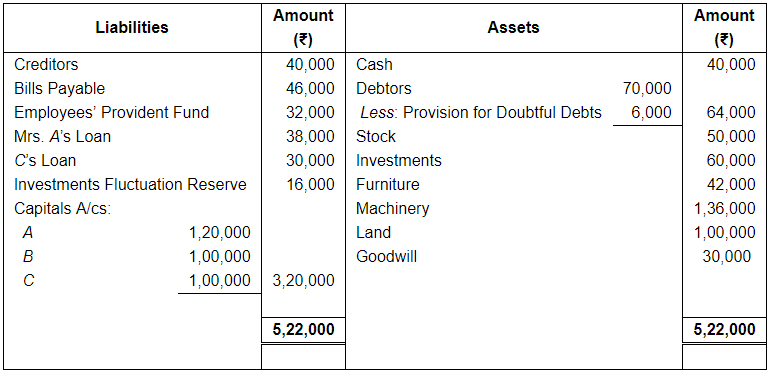

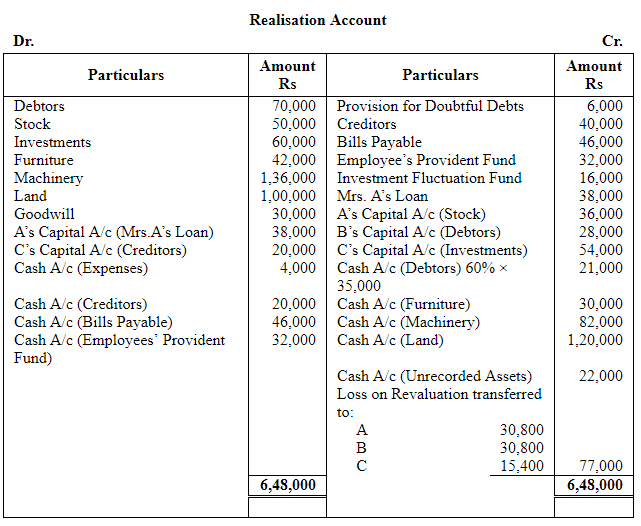

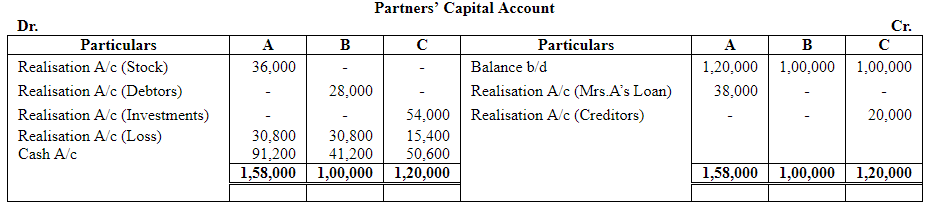

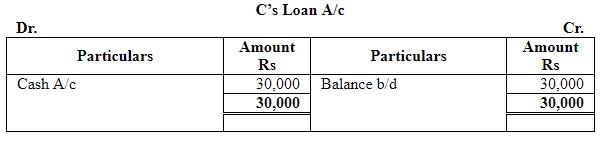

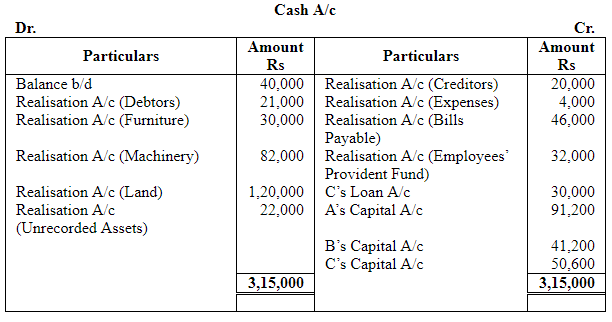

A, B and C were partners sharing profits in the ratio of 2 : 2 : 1. They decided to dissolve their firm on 31st March, 2019 when the Balance Sheet was:

Following transactions took place:

(a) A took over Stock at ₹ 36,000. He also took over his wife's loan.

(b) B took over half of Debtors at ₹ 28,000.

(c) C took over Investments at ₹ 54,000 and half of Creditors at their book value.

(d) Remaining Debtors realised 60% of their book value. Furniture sold for ₹ 30,000; Machinery ₹ 82,000 and Land ₹ 1,20,000.

(e) An unrecorded asset was sold for ₹ 22,000.

(f) Realisation expenses amounted to ₹ 4,000.

Prepare necessary Ledger Accounts to close the books of the firm.

ANSWER:

Page No 7.66:

Question 41:

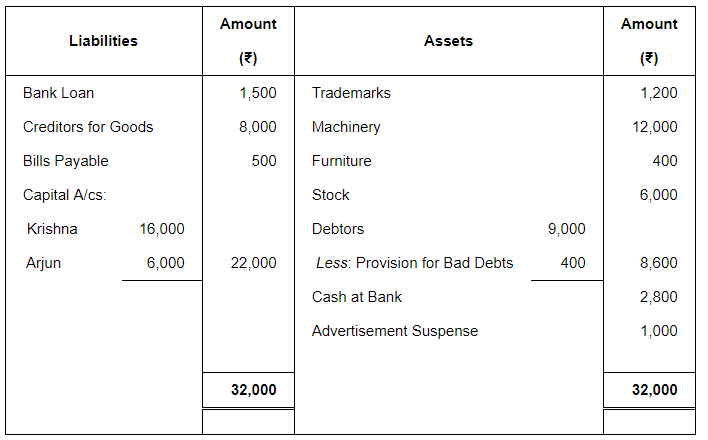

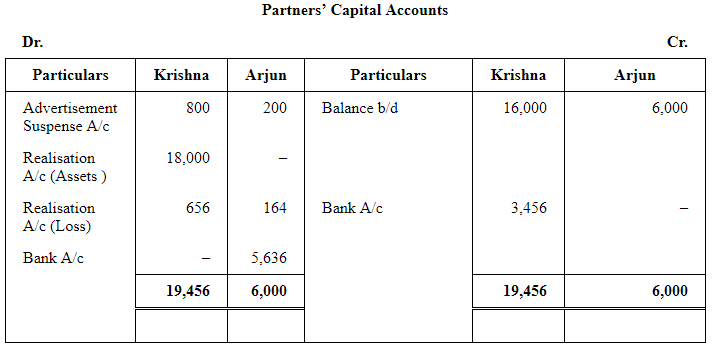

Krishna and Arjun are partners in a firm. They share profits in the ratio of 4 : 1. They decide to dissolve the firm on 31st March, 2019 at which date their Balance Sheet stood as:

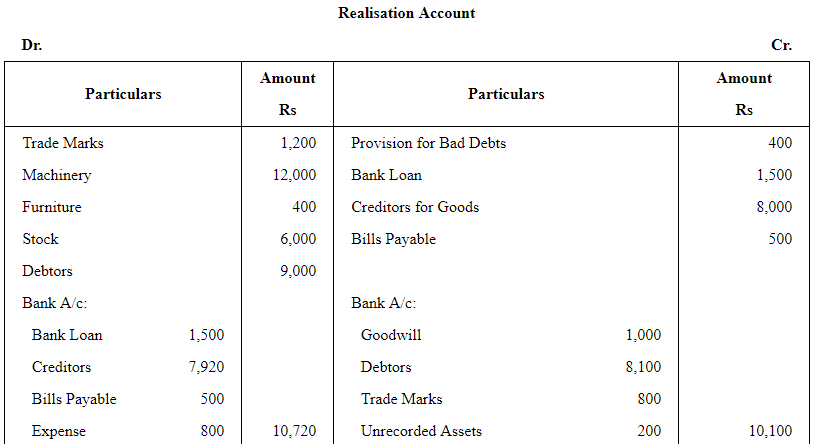

The realisation shows the following results:

(a) Goodwill was sold for ₹ 1,000.

(b) Debtors were realised at book value less 10%.

(c) Trademarks realised ₹ 800.

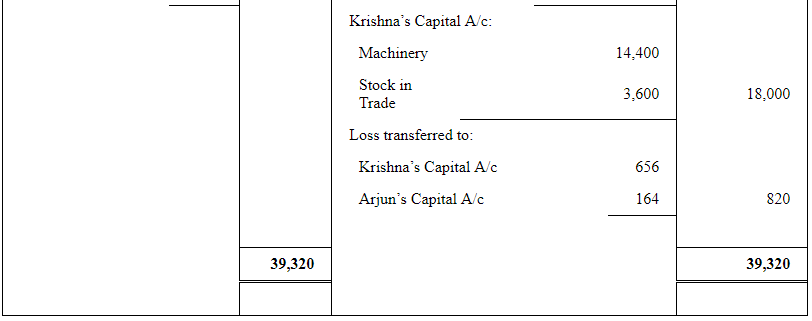

(d) Machinery and Stock-in-Trade were taken by Krishna for ₹ 14,400 and ₹ 3,600 respectively.

(e) An unrecorded asset estimated at ₹ 500 was sold for ₹ 200.

(f) Creditors for goods were settled at a discount of ₹ 80. The expenses on realisation were ₹ 800.

Prepare Realisation Account, Partners' Capital Accounts and Bank Account.

ANSWER:

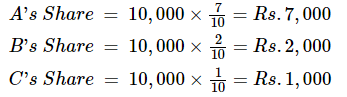

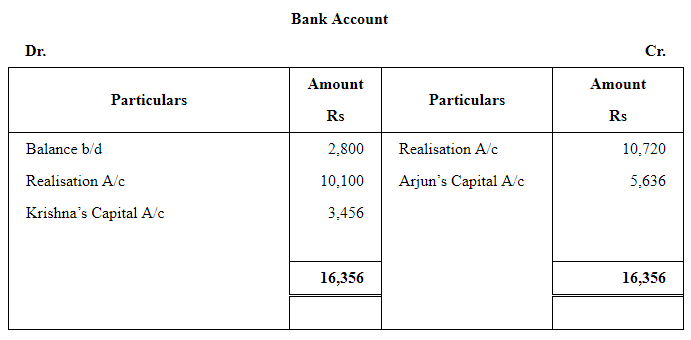

Question 42:

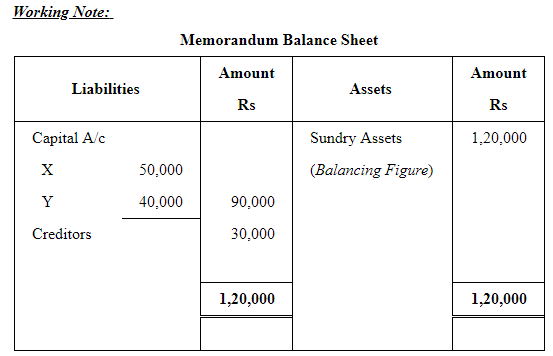

There are two partners X and Y in a firm and their capitals are ₹ 50,000 and ₹ 40,000. The creditors are ₹ 30,000. The assets of the firm realise ₹ 1,00,000. How much will X and Y receive?

ANSWER:

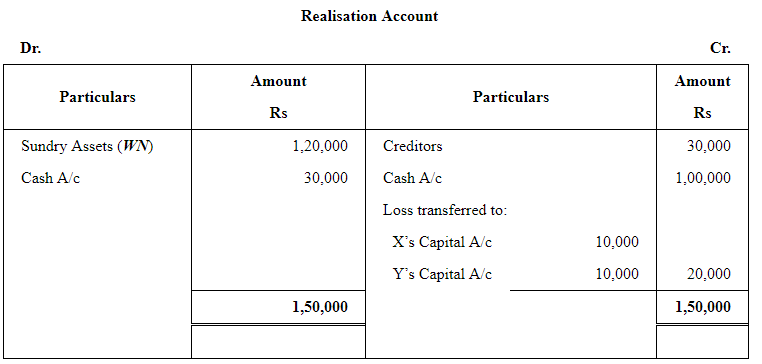

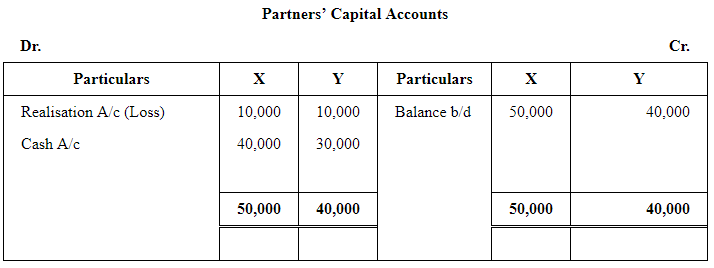

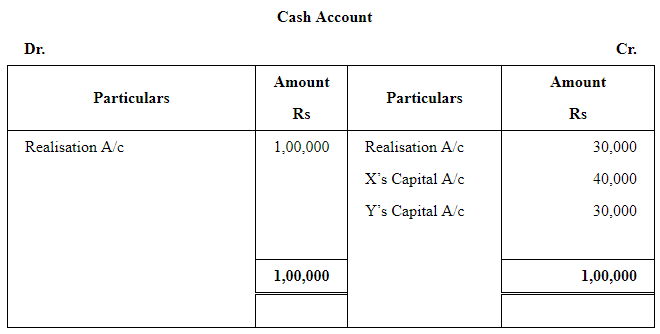

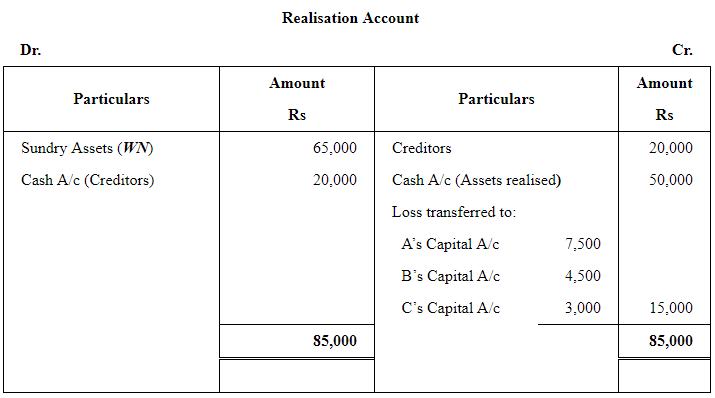

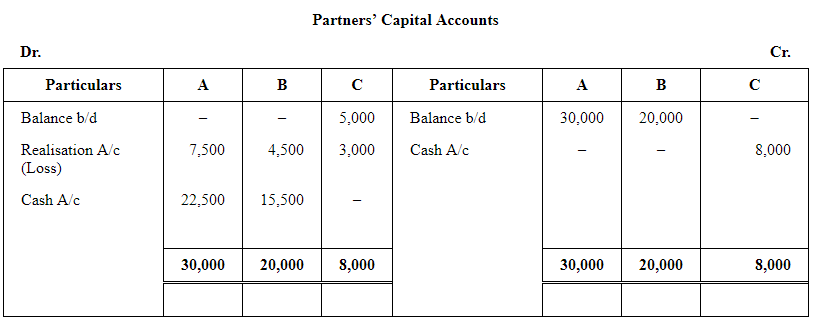

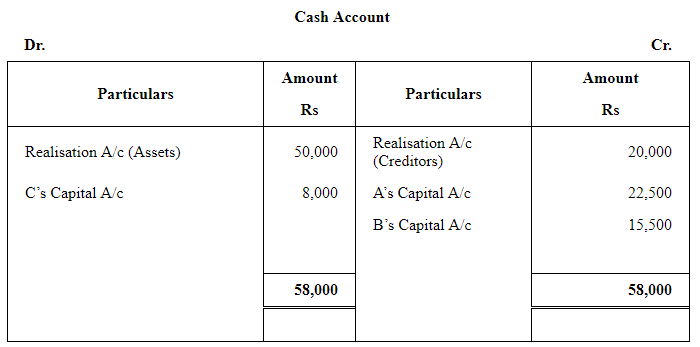

Question 43:

A, B and C were partners sharing profits in the ratio of 5 : 3 : 2. On 31st March, 2019, A's Capital and B's Capital were ₹ 30,000 and ₹ 20,000 respectively but C owed ₹ 5,000 to the firm. The liabilities were ₹ 20,000. The assets of the firm realised ₹ 50,000.

Prepare Realisation Account, Partner's Capital Accounts and Bank Account.

ANSWER:

WN 2

Question 54:

X, Y and Z entered into partnership on 1st April, 2016. They contributed capital ₹ 40,000, ₹ 30,000 and ₹ 20,000 respectively and agreed to share profits in the ratio of 3 : 2 : 1. Interest on capital was to be allowed @ 15% p.a. and interest on drawings was to be charged at an average rate of 5%. During the two years ended 31st March, 2018, the firm made profit of ₹ 21,600 and ₹ 25,140 respectively before allowing or charging interest on capital and drawings. The drawings of each partner were ₹ 6,000 per year.

On 31st March, 2018, the partners decided to dissolve the partnership due to difference of opinion. On that date, the creditors amounted to ₹ 20,000. The assets, other than cash ₹ 2,000, realised ₹ 1,21,000. Expenses of dissolution amounted to ₹ 760.

Draw up necessary Ledger Accounts to close the books of the firm.

ANSWER:

|

42 videos|168 docs|43 tests

|

FAQs on Dissolution of a Partnership Firm ( Part - 3) - Accountancy Class 12 - Commerce

| 1. What is the process of dissolving a partnership firm? |  |

| 2. How can disputes among partners be resolved during the dissolution of a partnership firm? | |

| 3. What are the legal formalities required for the dissolution of a partnership firm? | |

| 4. Can a partnership firm be dissolved without the consent of all partners? | |

| 5. What are the tax implications of dissolving a partnership firm? | |

|

2.5K Views |

|

4.82/5 Rating |

|

Dec 23, 2024 Last updated |

|

Explore Courses for Commerce exam

|

|

Dissolution of a Partnership Firm ( Part - 3) | Accountancy Class 12 - Commerce

,Dissolution of a Partnership Firm ( Part - 3) | Accountancy Class 12 - Commerce

,study material

,Previous Year Questions with Solutions

,Important questions

,MCQs

,Free

,Summary

,Viva Questions

,past year papers

,ppt

,mock tests for examination

,Sample Paper

,video lectures

,shortcuts and tricks

,Objective type Questions

,practice quizzes

,Dissolution of a Partnership Firm ( Part - 3) | Accountancy Class 12 - Commerce

,Extra Questions

,Semester Notes

,Exam

;

Dissolution of a Partnership Firm ( Part - 3) Free PDF Download

Importance of Dissolution of a Partnership Firm ( Part - 3)

Dissolution of a Partnership Firm ( Part - 3) Notes

Dissolution of a Partnership Firm ( Part - 3) Commerce Questions

Study Dissolution of a Partnership Firm ( Part - 3) on the App

|

© EduRev

|

Education Revolution

|

|