Q.1. Explain briefly the three features of perfect competition.

Ans. Following are the three features of perfect competition:

(i) Very Large Number of Buyers and Sellers: There is such a large number of buyers and sellers that none of them is in a position to influence the price in the market. The price of a good is determined by the whole industry, that is, by the combined actions of all the sellers and buyers. The firms are, therefore, called price-takers under perfect competition.

(ii) Homogeneous Goods: The goods sold in the market are homogeneous or identical in every aspect like quality, size, design, colour, etc. The goods are perfect substitutes of one another. As a result, no buyer has reasons to be attached to a particular firm. No seller can charge a higher price otherwise he will lose his customers.

(iii) Free Entry and Exit: Buyers and sellers (firms) are free to enter or leave the market at an y time they like. Large profits will induce the new firms to enter the industry; whereas losses will compel inefficient firms to leave the industry.

Q.2. What is meant by perfect competition? Give its main features.

Or

Explain the characteristics of a perfectly competitive market.

Ans. Perfect competition is a market situation in which a large number of sellers sell homogeneous product with free entry and exit condition. The price of the product under perfect competition is determined in the industry by market forces of demand and supply. An individual firm is merely a price taker and not a price maker.

Features of Perfect Competition: Following are the main features of the perfect competition:

(i) Very Large Number of Buyers and Sellers: There is such a large number of buyers and sellers that none of them is in a position to influence the price in the market. The price of a good is determined by the whole industry, that is, by the combined actions of all the sellers and buyers. The firms are, therefore, called price-takers under perfect competition.

(ii) Homogeneous Goods: The goods sold in the market are homogeneous or identical in every aspect like quality, size, design, colour, etc. The goods are perfect substitutes of one another. As a result, no buyer has reasons to be attached to a particular firm. No seller can charge a higher price otherwise he will lose his customers.

(iii) Free Entry and Exit: Buyers and sellers (firms) are free to enter or leave the market at any time they like. Large profits will induce the new firms to enter the industry; whereas losses will compel inefficient firms to leave the industry.

(iv) Perfect Knowledge: Buyers and sellers have perfect knowledge about the prices and costs of the goods in different parts of the market. Evidently, this leads to emergence of uniform price of the product since no seller can afford to charge a price higher than the prevailing one otherwise he will lose all his customers to his competitors.

(v) Absence of Transport Cost: Under prefect competition, it is assumed that different firms work so close to each other that there is no transport cost for customers.

(vi) Perfect Mobility: There is a free and complete mobility of factors of production. They are free to enter any industry, if considered profitable and leave any industry when remuneration is inadequate. Similarly, there is a perfect mobility of goods.

(vii)Normal Profits to Firms: The firms under perfect competition always earn normal profits in the long-run. Super normal profits attract new firms to enter the market, dragging the profits down to normal. Similarly, losses induce incompetent firms to exit the market, pulling the profit up to normal.

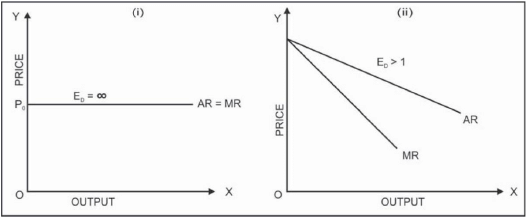

Q.3. Draw AR and MR curves of a firm under

(i) pure competition and

(ii) monopolistic competition. Give reasons for their shapes.

Or

Under perfect competition MR = AR, but under monopolistic competition MR < AR. Give reasons.

Ans. (i) The individual firm’s AR curve under perfect competition is a horizontal straight line or a perfectly elastic curve as the price of the homogeneous product is determined in the industry by the market forces of demand and supply. A firm can sell any level of output at a market-determined price. AR is the price per unit of output. Under perfect competition, the revenue from selling an additional unit is same as price. Thus, AR = MR under perfect competition. Consider part (i) of the diagram.

(ii) The individual firm’s AR and MR curves under monopolistic competition are a downward sloping straight line. However, MR curve lies below AR curve. These curves slope downwards because each firm can sell more only by lowering the price of its product. Consider part (ii) of the diagram.

Q.4. State whether the following statements are true or false. Give reasons for your answer.

(i) When Marginal Revenue is constant and not equal to zero then Total Revenue will also be constant.

(ii) As soon as Marginal Cost starts rising, Average Variable cost also starts rising.

(iii) Total Product always increases whether there are increasing returns or diminishing returns to a factor.

Ans. (i) False. Marginal Revenue (MR) is the rate at which Total Revenue (TR) changes. Thus, if MR is constant and not equal to zero, TR will increase at a constant rate.

(ii) False. Marginal Cost (MC) curve intersects the Average Variable Cost (AVC) curve at its minimum point. After MC starts rising, AVC is still falling. MC cuts AVC at its minimum point. Only after that point AVC starts rising.

(iii) True. Total Product (TP) increases whether there is increasing returns or diminishing returns to a factor. However, when there are increasing returns to a factor, TP increases at an increasing rate. On the other hand, when there are diminishing returns to a factor, TP increases at a diminishing rate.

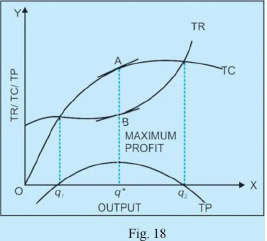

Q.5. Explain the conditions leading to maximisation of profits by a producer. Use Total Cost and Total Revenue approach.

Ans. Producer’s equilibrium refers to a situation in which the producer earns maximum profit. Profit (n) is calculated as a difference between Total Revenue (TR) and Total Cost of production (TC). That is,

n = TR - TC

A producer will produce up to the quantity of output at which the following condition is fulfilled: For maximum profit, the difference between TR and TC should be maximum. Producer’s equilibrium can be explained with the help of the given diagram. In the diagram, TC is the Total Cost curve and TR is the Total Revenue curve. The difference between TR curve and TC curve maximum at the Oq* level of output. It is represented by distance AB. This distance is the maximum compared to any other level of output. The maximum profit of the firm, therefore, is AB.

Profit (TP) curve has also been shown. At Oq* level of output, TP curve is at its highest point P. It implies the firm is earning maximum profit only at this level of output.

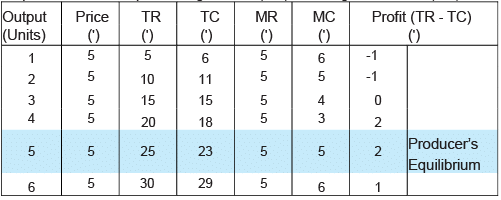

Q.6. Explain the conditions of producer’s equilibrium in terms of Marginal Cost and Marginal Revenue. Use a schedule.

Ans. Producer’s equilibrium refers to a situation in which the producer earns maximum profit. Producer’s equilibrium can be explained with the help of a Marginal Cost (MC) and Marginal Revenue (MR) schedule.

In the schedule, the producer is in equilibrium at 5th unit of output. At this level of output, MR = MC as well as the profit is maximum. However, MR is also equal to MC at 2nd unit of output but here profit is — 1.

Q.7. What is supply? Give its determinants.

Ans. Supply of a good refers to various quantities of a good offered for sale by a producer at a particular time, at various corresponding prices.

Determinants of Supply

(i) Price of the Good: Price of the commodity is the basic determinant of quantity supplied of a good. If other factors remain constant, quantity supplied of a good is more at a higher price and less at a lower price.

(ii) Price of Other Goods: Fall in the price of other goods makes the given product more profitable. Thus, the quantity supplied of the given product increases and the supply curve shifts to the right. Similarly, rise in the price of other product makes them more profitable as compared to the given product. Thus, the quantity supplied of the given product decreases and the supply curve shifts to the left.

(iii) Prices of Inputs: The quantity supplied of a commodity decreases with an increase in the prices of inputs and increases with a fall in its price.

(iv) Goal of the Firm: If the firm has the goal of maximum profit, it may offer more quantity for sale at a higher price and vice-versa. However, if the goal of the firm is to maximise sale, it may supply more quantity at the same price or even a slightly lower price.

(v) State of Technology: The choice of a particular method of production of a commodity is influenced by the available state of technology. With the technical progress, cost of production falls over time and the level of profit increases. The firm in such a situation increases the quantity supplied of a good.

(vi) Expected Future Price: If the price of a given commodity is expected to increase in future, the supply of the good in the current period is likely to be reduced and vice-versa.

(vii) Policy of the Government: If the government imposes high taxes on goods, the supply is likely to fall and vice-versa. On the opposite, grant of subsidy on a commodity may increase its supply and viceversa.

Q.8. Explain the Law of Supply along with its limitations.

Ans. The law of supply states that, other things remaining constant, the quantity supplied of good increases as price increases, and decreases as price decreases. The law of supply represents a positive or direct relationship between price and quantity supplied.

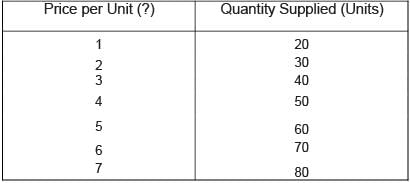

Supply Schedule. The law of supply can be explained with the help of a schedule that shows a positive relationship between price and supply.

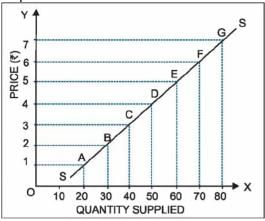

The schedule shows that sellers are willing to sell more at higher prices and less at lower prices. When the price of the good is ' 1, the quantity offered is 20 units. When the price rises to ' 4, the quantity offered for sale is 50 units. However, when the price rises to ' 7, the quantity offered is 80 units. Supply Curve. Supply curve is a graphical representation of the functional relationship between price and the quantity supplied. In the figure on the right, quantity supplied is measured along X axis and price is measured along Y axis. The slope of the supply curve SS is positive. It implies that more units of a good are offered at higher prices and fewer units are offered at lower prices.

Limitations of the Law of Supply: The law of supply has the following limitations:

(i) Future Prices: The law of supply will not be applicable when prices are expected to change in future. If the seller has the fear that the price will fall in future, he will be ready to sell the good even at a lower price. This will cause an unexpected increase in the supply and consequently, the price.

(ii) Agricultural Products: The law usually does not apply to agricultural products because their supply cannot be increased immediately with the increase in price.

(iii) Clearance of Old Stock: When the trader wants to have a new stock and give away the old stock, he will sell more quantity of the good by lowering its price. The law of supply does not apply in this case.

(iv) Auction: In auction, the goods can be sold at any price. In such a situation, the law of supply does not apply.

(v) Change of Place and Trade: When a particular seller is interested in changing the place or type of trade, he sells the goods at a low price to get rid of the stored goods at the earliest.

(vi) Availability of Substitutes: If a large number of substitutes are available for a good in the market, there will be competition among sellers and the law of supply will not apply.

Q.9. State any four factors affecting elasticity of supply.

Ans. Following factors affect the elasticity of supply:

(i) Availability of Factors or Inputs: If the inputs or factors of production are easily available then the elasticity of supply will be more. On the other hand, if the availability of these inputs is difficult then the elasticity of supply will be less.

(ii) Nature of the Product: Nature of the product also affects the elasticity of supply. If the product is perishable then its supply will be inelastic. On the other hand, if the product is durable, its supply will be elastic.

(iii) Time Element: Elasticity of supply is inelastic in the short period while it is elastic in the long run. In the very short period, supply is perfectly inelastic as the firms cannot change its supply according to the price change.

(iv) Future Expectations: These include prices, quantity demanded, change in production techniques, etc. If the producers expect the future rise in prices then present stock of supply will be reduced and supply becomes inelastic.