Long Questions With Answers - The Theory Of The Firm Under Perfect Competition

Q.1. Explain briefly the three features of perfect competition.

Ans: Following are the three main features of perfect competition:

(i) Very Large Number of Buyers and Sellers: There are so many buyers and sellers that no single buyer or seller can influence the market price. Price is determined by the combined actions of all participants in the industry. Individual firms are therefore price-takers - they accept the market price and cannot set a higher price without losing all customers.

(ii) Homogeneous Goods: All firms sell identical or homogeneous products. Goods are perfect substitutes for one another in every relevant attribute (quality, size, design, colour, etc.). Because of this, buyers have no preference for one seller over another and any attempt by a firm to charge a higher price will cause it to lose customers.

(iii) Free Entry and Exit: Firms are free to enter or exit the industry without restrictions. When firms earn supernormal profits, new firms enter the industry, increasing supply and reducing profits; when firms make losses, some exit, reducing supply and restoring normal profits. This freedom ensures that, in the long run, firms earn only normal profits.

Q.2. What is meant by perfect competition? Give its main features.

Or

Explain the characteristics of a perfectly competitive market.

Ans: Perfect competition is a market structure in which a large number of sellers sell a homogeneous product, there is free entry and exit, and the price of the product is determined by overall market demand and supply. An individual firm cannot influence the market price and is therefore a price-taker.

Main features of perfect competition:

(i) Very Large Number of Buyers and Sellers: No individual buyer or seller can influence price; price is determined by the market as a whole.

(ii) Homogeneous Goods: Products offered by different firms are identical and perfectly substitutable.

(iii) Free Entry and Exit: Firms can enter or leave the industry freely, which drives long-run profits to normal levels.

(iv) Perfect Knowledge: Buyers and sellers have full information about prices, quality and production methods. This prevents any firm from charging a price above the market price for long.

(v) Absence of Transport Cost: It is assumed that transport costs are negligible so that buyers face the same price regardless of the seller's location; this supports a single market price.

(vi) Perfect Mobility of Factors: Factors of production (land, labour, capital) can move freely between uses and locations, allowing resources to be reallocated to profitable uses.

(vii) Normal Profits in the Long Run: In the long run, entry and exit of firms ensure that firms earn only normal profits; supernormal profits attract entry while losses cause exit.

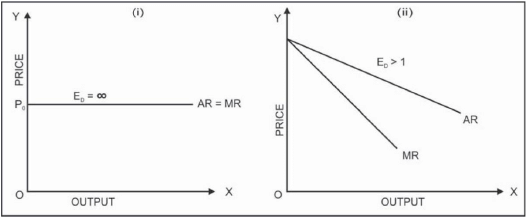

Q.3. Draw AR and MR curves of a firm under

(i) pure competition and

(ii) monopolistic competition. Give reasons for their shapes.

Or

Under perfect competition MR = AR, but under monopolistic competition MR < AR. Give reasons.

Ans:

(i) Under perfect (pure) competition the individual firm faces a perfectly elastic demand at the market price. The Average Revenue (AR) curve is a horizontal straight line at the market price. Since each additional unit sold fetches the same price, Marginal Revenue (MR) equals that price. Therefore AR = MR and both are horizontal lines. A firm can sell any quantity at the market price but cannot charge above it.

(ii) Under monopolistic competition each firm sells a differentiated product and faces a downward-sloping demand curve. The AR curve is downward sloping because to sell more the firm must lower its price. Marginal Revenue (MR) lies below AR because when the firm reduces price to sell one extra unit, it must lower the price on all previously sold units as well; the extra revenue from the additional unit is therefore less than the price at which it is sold. Hence MR < AR and MR lies below the AR curve.

Q.4. State whether the following statements are true or false. Give reasons for your answer.

(i) When Marginal Revenue is constant and not equal to zero then Total Revenue will also be constant.

(ii) As soon as Marginal Cost starts rising, Average Variable cost also starts rising.

(iii) Total Product always increases whether there are increasing returns or diminishing returns to a factor.

Ans:

(i) Ans: False.

Explanation: Marginal Revenue (MR) is the change in Total Revenue (TR) for an additional unit sold. If MR is constant and positive, TR increases at a constant rate as output rises; TR is not constant, it keeps rising. Only if MR were zero would TR remain constant.

(ii) Ans: False.

Explanation: The Marginal Cost (MC) curve intersects the Average Variable Cost (AVC) curve at AVC's minimum point. When MC begins to rise from a low level, AVC may still be falling until MC rises above AVC. AVC starts rising only after MC exceeds AVC. Thus, AVC does not necessarily start rising immediately when MC starts rising.

(iii) Ans: True.

Explanation: Total Product (TP) increases with additional units of the variable factor in both cases. Under increasing returns TP rises at an increasing rate (marginal product is rising). Under diminishing returns TP continues to increase but at a decreasing rate (marginal product falls). TP only falls when negative returns occur.

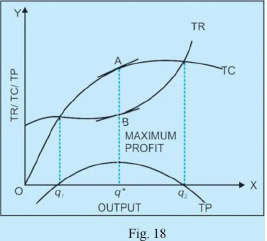

Q.5. Explain the conditions leading to maximisation of profits by a producer. Use Total Cost and Total Revenue approach.

Ans: Producer's equilibrium (profit maximisation) is the output level at which the difference between Total Revenue (TR) and Total Cost (TC) is greatest. Let profit n = TR - TC. The conditions and reasoning are:

- Draw TR and TC curves on the same diagram. The vertical distance between TR and TC at any output measures profit at that output.

- The output at which this vertical distance is maximum is the profit-maximising output. At that output the firm's profit is highest; at any other output profit is smaller or the firm may incur loss.

- The profit curve (TP = TR - TC) reaches its highest point at this output; that is where the slope of the TP curve is zero and TP is maximised.

In the given diagram

the distance AB (vertical gap between TR and TC) is largest at output Oq*, so profit is maximum there. The profit curve peaks at point P corresponding to Oq*, confirming that Oq* is the producer's equilibrium by the TR-TC approach.

the distance AB (vertical gap between TR and TC) is largest at output Oq*, so profit is maximum there. The profit curve peaks at point P corresponding to Oq*, confirming that Oq* is the producer's equilibrium by the TR-TC approach.Q.6. Explain the conditions of producer's equilibrium in terms of Marginal Cost and Marginal Revenue. Use a schedule.

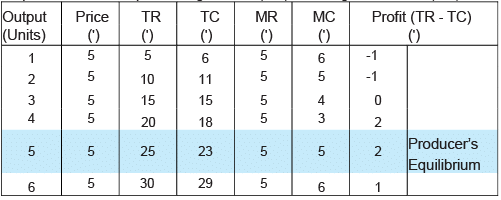

Ans: Producer's equilibrium can also be found using Marginal Revenue (MR) and Marginal Cost (MC). The conditions are:

- First condition (necessary): MR = MC. The firm should expand output up to the point where the additional revenue from selling one more unit equals the additional cost of producing it.

- Second condition (sufficient): MC must be rising at the equilibrium point, i.e., MC should cut MR from below. This ensures that profit is maximised (not minimised).

In the provided schedule

, MR = MC occurs at the 5th unit; here profit is maximum and the MC curve is rising beyond that point. Although MR = MC also happens at the 2nd unit in the schedule, profit there is lower (in the example it is -1), so the 2nd unit does not give profit maximisation. Hence the firm's equilibrium is at 5th unit where both MR = MC and the second condition (MC rising) hold.

, MR = MC occurs at the 5th unit; here profit is maximum and the MC curve is rising beyond that point. Although MR = MC also happens at the 2nd unit in the schedule, profit there is lower (in the example it is -1), so the 2nd unit does not give profit maximisation. Hence the firm's equilibrium is at 5th unit where both MR = MC and the second condition (MC rising) hold.Q.7. What is supply? Give its determinants.

Ans: Supply of a good is the quantity of the good that producers are willing to offer for sale at various prices during a given period.

Determinants of Supply:

(i) Price of the Good: A higher price makes production more profitable and induces producers to supply a larger quantity, other things remaining the same.

(ii) Price of Other Goods: If prices of alternative products rise, producers may switch to producing them, reducing supply of the original good. Conversely, a fall in alternative prices increases supply of the given good.

(iii) Prices of Inputs: A rise in input costs raises production costs and tends to reduce supply; a fall in input costs increases supply.

(iv) Goal of the Firm: If a firm aims to maximise profit it will adjust supply according to profitable price signals; if it seeks to maximise sales it may supply more even at the same or slightly lower price.

(v) State of Technology: Improvements in technology reduce cost of production and increase supply at each price.

(vi) Expected Future Price: If producers expect higher future prices, they may withhold current supply to sell later, reducing present supply; expectation of price falls can increase current supply.

(vii) Government Policy: Taxes, subsidies and regulations affect supply. Higher taxes reduce supply, while subsidies increase it.

Q.8. Explain the Law of Supply along with its limitations.

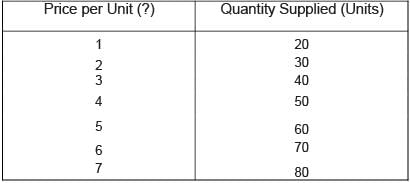

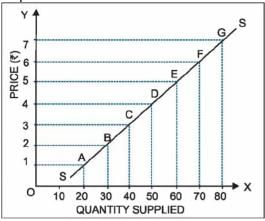

Ans: The Law of Supply states that, ceteris paribus (other things remaining equal), the quantity supplied of a good increases as its price rises and decreases as its price falls. Thus, price and quantity supplied have a direct (positive) relationship.

Supply Schedule: A schedule shows how quantity supplied varies with price; for example, as price rises from ₹1 to ₹4 to ₹7, quantity supplied rises from 20 to 50 to 80 units respectively, illustrating the positive relationship.

Supply Curve: The supply curve (SS) is upward sloping reflecting that sellers offer more at higher prices and less at lower prices.

Limitations of the Law of Supply:

(i) Expectation About Future Prices: If sellers expect prices to fall in future, they may sell more now even at lower prices; conversely, expectation of future price rises may reduce present supply.

(ii) Agricultural Products: Supply of agricultural goods cannot be adjusted quickly to price changes because of biological and time constraints; the law may not hold in the short run for such goods.

(iii) Clearance of Old Stock: Sellers clearing old stock may reduce price to sell more; here higher quantity is sold at lower price, contradicting the law.

(iv) Auction Sales: In auctions price is determined by bidders and quantity supplied is not guided by the simple price-supply relationship assumed by the law.

(v) Change of Place or Line of Business: When sellers wish to relocate or change trade, they may sell off stock at low prices to dispose of goods quickly; this breaks the usual price-supply pattern.

(vi) Availability of Substitutes: If many close substitutes exist, competition among sellers may prevent the normal upward-sloping supply response to price changes.

Q.9. State any four factors affecting elasticity of supply.

Ans: Four factors that influence the elasticity of supply are:

(i) Availability of Factors or Inputs: If inputs (raw materials, labour, machinery) are readily available, firms can increase production quickly when price rises, making supply more elastic. Scarce inputs make supply inelastic.

(ii) Nature of the Product: Perishable goods (e.g., fresh produce) have inelastic supply because they cannot be stored; durable goods can be stored and supplied later, making supply more elastic.

(iii) Time Element: Supply is usually inelastic in the short run when production capacity is fixed; in the long run firms can adjust capacity and supply becomes more elastic. In the immediate (very short) run supply may be perfectly inelastic.

(iv) Future Expectations: If producers expect higher future prices, they may withhold current supply to sell later, making current supply less responsive to current price changes (inelastic). Conversely, expectation of falling prices can make current supply more elastic.

FAQs on Long Questions With Answers - The Theory Of The Firm Under Perfect Competition

| 1. What is the theory of the firm under perfect competition? |  |

| 2. How does perfect competition impact the behavior of firms? | |

| 3. What is the significance of the theory of the firm under perfect competition? | |

| 4. How does a perfectly competitive firm determine its level of output? | |

| 5. What are the characteristics of a perfectly competitive market? | |