NCERT Solutions - Introduction to Microeconomics

Q1: Discuss the central problems of an economy.

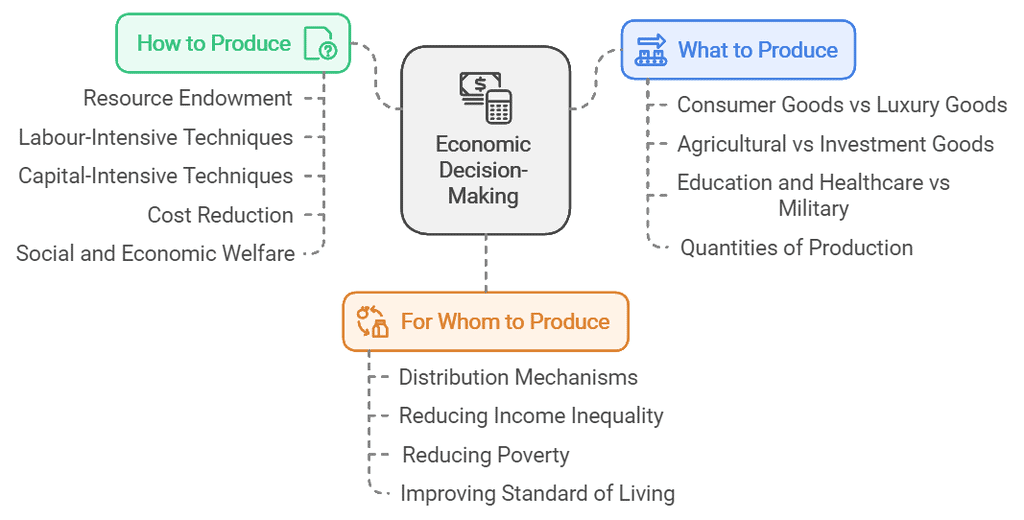

Ans: Every economy faces the problem of scarcity of resources in relation to unlimited wants. Because of this, every society has to make choices regarding the use of its limited resources. These are known as the central problems of an economy:

1. What is produced and in what quantities?

Every society must decide which goods and services to produce and in what quantities. For example, it has to choose between producing more consumer goods or capital goods, or between agricultural and industrial goods.

2. How are these goods produced?

This problem refers to the choice of technique of production. A society has to decide whether to use labour-intensive methods or capital-intensive methods, depending on the availability of resources and cost considerations.

3. For whom are these goods produced?

This problem relates to the distribution of goods and services among individuals in the economy. It involves deciding who will get how much of the total output, i.e., how income and output are shared among people.

Thus, the central problems of an economy arise due to scarcity of resources and involve the allocation and distribution of resources efficiently.

Q2: What do you mean by the production possibilities of an economy?

Ans: The production possibilities of an economy are the different combinations of goods and services that can be produced with the available resources and technology when resources are used efficiently. These combinations show the trade-offs a society faces: producing more of one good requires producing less of another. The concept also helps to illustrate opportunity cost - the value of the next best alternative foregone when a choice is made.

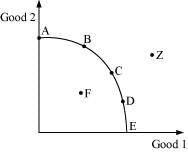

Q3: What is a production possibility frontier?

Ans: The production possibility frontier (PPF), or production possibility curve (PPC), is a curve that shows various efficient combinations of two goods that an economy can produce with a given set of resources and technology.

Points on the curve (for example, points on curve AE in the figure) represent full and efficient use of resources. Points inside the curve (like F) indicate inefficiency or under-utilisation of resources. Points outside the curve (like Z) are unattainable with current resources and technology.

The PPF is typically downward sloping because increasing production of one good requires sacrificing some production of the other. The PPF is concave from the origin because opportunity cost keeps increasing as resources are shifted between the two goods. This happens since resources are not equally efficient in producing both goods.

PPC

PPC

Q4: Discuss the subject matter of economics.

Ans: The subject matter of economics is usually divided into two main branches: microeconomics and macroeconomics. These branches were named by Ragnar Frisch after 1930.

(i) Microeconomics

- Microeconomics studies individual economic units such as households, firms and individual markets.

- It examines how consumers and firms make decisions, how prices and quantities are determined in individual markets through demand and supply, and how resources are allocated.

- Microeconomics is often called price theory because it explains how prices for goods and factors are formed and how they coordinate economic activity.

(ii) Macroeconomics

- Macroeconomics studies the economy as a whole - aggregate output, total employment, the general price level, and overall economic growth.

- Its main concerns are aggregate demand and aggregate supply, national income determination, inflation, unemployment, and balance of payments problems.

- Macroeconomics is also referred to as the theory of income and employment because it explains how total income and employment are established and how policy can influence them.

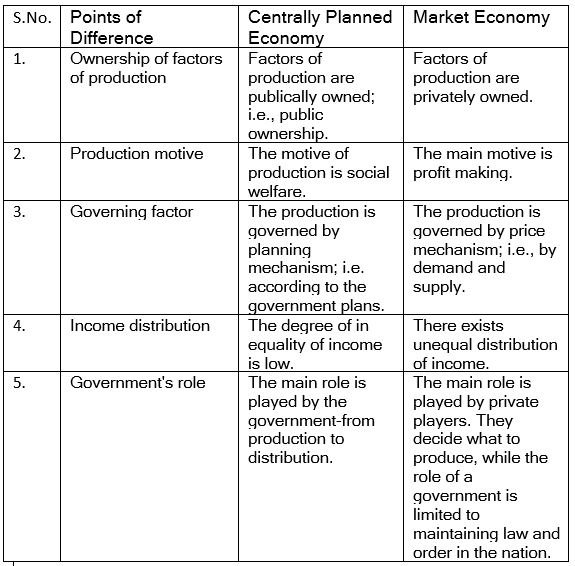

Q5: Distinguish between a centrally planned economy and a market economy.

Ans:

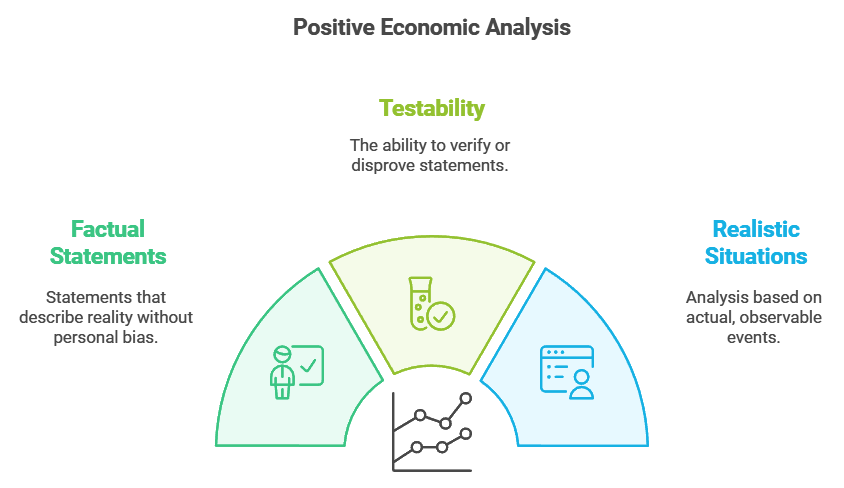

Q6: What do you understand by positive economic analysis?

Ans:

- Positive economic analysis examines economic issues using objective, testable statements about what is or what will be. It describes and explains economic phenomena without value judgments.

- Such statements can be checked against facts or data and accepted or rejected on that basis.

- Example: "An increase in the rate of income tax will reduce disposable income" is a positive statement because it can be tested empirically.

Q7: What do you understand by normative economic analysis?

Ans: Normative economic analysis deals with value judgments about what ought to be. It expresses opinions on desirable policies and goals, and it cannot be tested or proven true or false purely by facts.

- Normative statements reflect personal or societal values and ethics. They concern policy choices and ideals, not objective verification.

- Examples include statements about fairness, equity or what the government should do - for instance, "The government should provide minimum support prices to farmers."

- Because they rely on value judgments, normative conclusions often differ between individuals or societies.

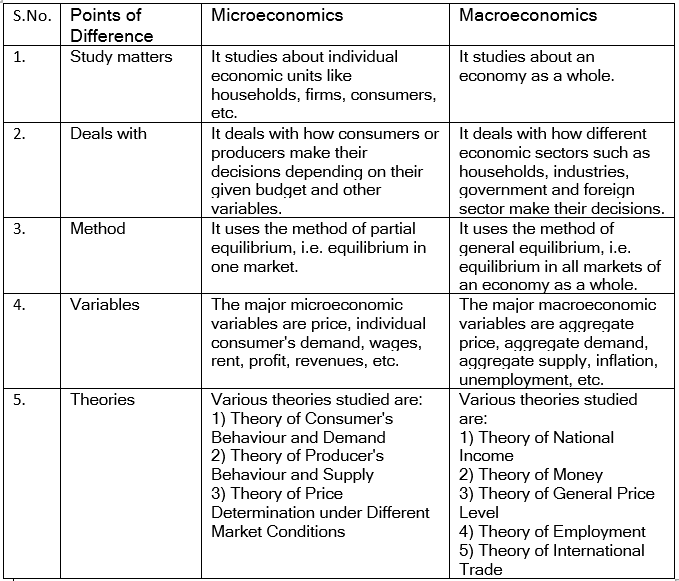

Q8: Distinguish between microeconomics and macroeconomics.

Ans:

FAQs on NCERT Solutions - Introduction to Microeconomics

| 1. What is microeconomics and how is it different from macroeconomics? |  |

| 2. Why do we have to study scarcity and choice in microeconomics? | |

| 3. What exactly is opportunity cost and how does it apply to real life? | |

| 4. How do I understand the difference between positive and normative economics in Class 11? | |

| 5. What are the main assumptions of microeconomic theory that I need to know for exams? | |