Cost Accounting Solved Question Papers - 1

Ques 1: (a) Fill in the blanks:

(1) Fixed cost per unit _____ when volume of production increases.

(2) In printing industries, the method of ______ costing is applied.

(3) In process costing, the output of the each process in the ____ of the next process.

(4) In Cost Accounting, _____ are the combination of indirect material, indirect labour and indirect expenses.

Ans:

(1) decreases

(2) process

(3) input

(4) overheads

(b) Choose and write the correct answer:

(1) Under the ABC analysis of material control, A stands for low value/moderate value/_______.

(2) In a chemical industry, the method of ______/contract costing is applied.

(3) Variable overhead cost is a period cost/______.

(4) Cost of abnormal idle time and overtime is transferred to _____/General Profit and Loss Account.

Ans:

(1) high value items.

(2) process costing

(3) an output cost

(4) costing Profit and Loss Account

Ques 2: Write on the following (any four):

(a) Distinction between Cost Accounting and Financial Accounting (any four points)

Basis | Financial Accounting | Cost Accounting |

1. Nature | Financial accounts are maintained on the basis of historical records. | Cost accounts lay emphasis on both historical and predetermined costs. |

2. Use | Financial Accounting is used even by outside entities. | Cost Accounting is used only the management of the concern. |

3. System | Financial Accounting uses the double-entry system for recording financial data. | Cost Accounting does not use the double-entry for collecting cost data. |

4. Scope | Financial Accounting covers all items of income and expenditure whether related to the cost centers or not, | Cost Accounting covers all items related to a cost centre. |

5. Reports | Financial Accounting results are shown P&L A/c and balance sheet. | Cost Accounting results are shown in Cost Sheet/ Coating Profit & Loss A/c/ Reports Contract A/c/ Process A/c. |

(b) Causes of labour turnover.

Ans: Labour turnover means the rate at which workers leave and are replaced in an organisation during a period. High labour turnover indicates instability and frequent exits; very low turnover may suggest under-performing employees are retained. Causes can be classified under three broad heads:

1. Personal causes

- Circumstances of the family (relocation, marriage, etc.).

- Retirement on reaching prescribed age.

- Change in marital status (often cited for women employees).

- Dislike for the job or the location of work.

- Death of the employee.

- Employee getting a better job elsewhere.

- Permanent disability due to accidents.

- Involvement in activities of moral turpitude.

2. Unavoidable causes

- Termination for insubordination or inefficiency.

- Discharge on account of irregularity or long absence.

- Retrenchment because of shortage of work.

3. Avoidable causes

- Non-availability of promotion opportunities.

- Dissatisfaction with incentive schemes.

- Unhappy with remuneration.

- Wrong placement leading to unsuitability for the job.

- Poor working conditions.

- Non-availability of accommodation, health and recreational facilities.

- Lack of stability of tenure.

The management should identify and reduce avoidable causes by improving pay, working conditions, career development and placement methods.

(c) Allocation and absorption of overheads.

Ans:

Allocation of Overhead Expenses: Allocation is the process of identifying and charging whole overhead items to a specific cost centre where they can be directly identified. An expense that is wholly attributable to a particular department is allocated to that department without division. For example, overtime wages paid exclusively to workers of a department are allocated to that department.

Absorption of Overheads: Absorption is the process of charging an equitable share of overheads (already allocated or apportioned) to cost units or products. CIMA defines absorption as 'the process of absorbing all overhead costs allocated or apportioned over a particular cost centre or production department by the units produced.'

Overheads are apportioned on a suitable base (machine hours, labour hours, units produced, etc.). The common formula is:

Overhead Absorption Rate = Overhead Expenses / Units of the base selected.

The absorption rate is then applied to the actual base units to charge overhead to jobs or products.

(d) Reconciliation of Cost Account and Financial Account.

Ans: When cost accounts and financial accounts are maintained separately (non-integral system), two profit figures arise - one from costing books and one from financial books. These figures often differ because the two systems serve different purposes and apply different treatments:

- Financial accounts aim to ascertain profit for the whole organisation over a period (usually a year) and follow statutory presentation (P&L A/c, balance sheet).

- Cost accounts aim to ascertain cost and profitability by product, department or process for managerial control and decision making.

Differences arise from items included or excluded, valuation methods, treatment of overheads, depreciation, stock valuation, transfers between departments, and treatment of abnormal items. Reconciliation requires a detailed schedule explaining adjustments to convert cost profit to financial profit (or vice versa), such as adding items charged only in financial accounts or eliminating items included only in cost accounts.

(e) Perpetual inventory system.

Ans: Perpetual Inventory System is a continuous system of recording receipts, issues and resulting balances of individual stock items in quantity or quantity and value. Under this system:

- Every receipt and issue is recorded immediately in bin cards and the stores ledger.

- Stock balances are always available and are regularly reconciled with physical stock.

- Frequent verification reduces stock discrepancies and helps prompt investigation and corrective action.

Main advantage: It avoids production disruption due to periodic stock taking and provides reliable stock information for production and purchasing decisions.

(f) Salient features of perpetual inventory system

Ans:

- Requires continuous recording of receipts and issues; hence more effort to maintain.

- Balances shown by the stores ledger and bin cards are regularly reconciled with physical stock.

- Physical checking of selected items is carried out systematically and on rotation.

- It is costlier than periodic inventory due to record-keeping and control effort.

- Store ledger and bin cards keep inventory records up to date and accurate.

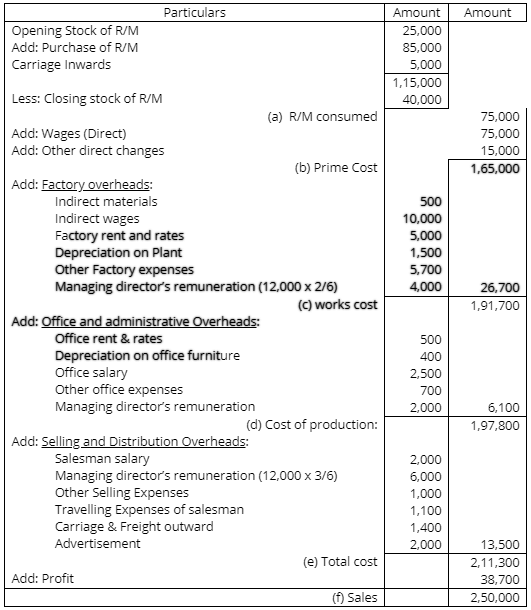

Ques 3: (a) The following data have been extracted from the books of M/s, ABC Industries Ltd. For the calendar year, 2017:

Particulars | (Rs.) |

Opening stock of raw materials Purchase of raw materials Closing stock of raw materials Carriage inwards Wages: Direct Indirect Other direct charges Rent and rates: Factory Office Indirect consumption of materials Depreciation: Plant Office Furniture Salary: Office Salesman Other factory expenses Other office expenses Managing Director's remuneration Other selling expenses Travelling expenses of salesman Carriage and freight outward Sales Advance income-tax paid Advertisement | 25,000 85,000 40,000 5,000 75,000 10,000 15,000 5,000 500 500 1,500 400 2,500 2,000 5,700 700 12,000 1,000 1,100 1,400 2,50,000 15,000 2,000 |

Managing Director's remuneration is to be allocated in the ratio of 2 : 1 : 3 for factory, office and sales departments respectively. From the above information, prepare the different phases of cost and net profit.

Cost Sheet of M/S ABC Industries

Ans:

Compute the cost phases step by step (all figures in Rs.):

Raw materials consumed:

Opening stock of raw materials 25,000 + Purchases 85,000 - Closing stock 40,000 = 70,000

Add: Carriage inwards 5,000 = 75,000 (total materials available for use)

Less: Indirect consumption of materials 500 (treated as factory overhead) = Direct materials consumed 74,500

Prime Cost:

Direct materials 74,500 + Direct wages 75,000 + Other direct charges 15,000 = 1,64,500 (Prime Cost)

Factory (Production) Overheads:

Indirect wages 10,000 + Rent and rates (Factory) 5,000 + Indirect consumption of materials 500 + Depreciation: Plant 1,500 + Other factory expenses 5,700 + Managing Director's allocation to factory (see below) 4,000 = 26,700 (Factory Overheads)

Allocation of Managing Director's remuneration (total Rs.12,000 in ratio 2:1:3 = total parts 6):

Factory = (2/6) × 12,000 = 4,000

Office = (1/6) × 12,000 = 2,000

Sales = (3/6) × 12,000 = 6,000

Works (Factory) Cost / Cost of Production (before office & selling overheads):

Prime Cost 1,64,500 + Factory Overheads 26,700 = 1,91,200

Office Overheads:

Rent & rates (Office) 500 + Depreciation: Office furniture 400 + Salary: Office 2,500 + Other office expenses 700 + MD allocation to office 2,000 = 6,100 (Office Overheads)

Cost of Production (including office overheads):

Works cost 1,91,200 + Office overheads 6,100 = 1,97,300

Selling & Distribution Overheads:

Salesman salary 2,000 + Other selling expenses 1,000 + Travelling expenses of salesman 1,100 + Carriage and freight outward 1,400 + Advertisement 2,000 + MD allocation to sales 6,000 = 13,500 (Selling & Distribution Overheads)

Cost of Sales:

Cost of production 1,97,300 + Selling & distribution overheads 13,500 = 2,10,800

Sales (Revenue): 2,50,000

Gross / Costing Profit: Sales 2,50,000 - Cost of Sales 2,10,800 = 39,200

Note: Advance income-tax paid (15,000) is an asset/advance payment and is not charged as a cost in the cost sheet. Managing Director's remuneration has already been apportioned and included in the relevant overheads. Thus, the net profit as per cost accounts (before any adjustments for items of financial nature) is Rs.39,200.

(b) What do you mean by material control? What are its techniques? Discuss its significances.

Ans: Material (Inventory) Control means maintaining the stock of materials, components and stores at a level that ensures continuous production and service while minimising investment. It involves monitoring receipts, issues and balances and regulating purchases to meet production requirements.

Key techniques of material control

- Budgetary techniques: Preparing purchase budgets based on sales and production budgets to plan required quantities and values.

- ABC analysis: Classifying inventory into A (high-value), B (medium-value) and C (low-value) items and directing most control effort towards A items.

- Economic Order Quantity (EOQ): Determining the order size that minimises total ordering and carrying costs.

- VED analysis: Classifying spare parts as Vital, Essential and Desirable to control critical items for uninterrupted production.

- Perpetual inventory system: Continuous recording of receipts and issues to keep stock records up to date and permit timely action on discrepancies.

Significance / Advantages

- Protects against fluctuations in demand by ensuring adequate stocks are available.

- Improves customer service through timely delivery of finished goods.

- Ensures continuity of production by preventing material shortages.

- Reduces risk of loss due to obsolescence or deterioration through regular checks.

- Minimises administrative workload and avoids duplication of orders.

- Facilitates effective use of working capital by avoiding over-stocking.

- Provides better control over pilferage and material loss.

- Supports accurate cost accounting by providing reliable material consumption data.

Ques 4: EXPLAIN INVENTORY CONTROL TECHNIQUES

Ans: Techniques of Inventory Control

The techniques or the tools generally used to effect control over the inventory are the following:

(1) Budgetary techniques for inventory planning;

(2) A-B-C. System of inventory control;

(3) Economic Order Quantity (E.O.Q.) i.e., how much to purchase at one time economically;

(4) VED Analysis;

(5) Perpetual inventory system and the system of store verification;

(1) Budgetary Techniques: For the purchase of raw materials and stocks, a purchase budget in terms of quantities and values is prepared. The sales budget generally determines the production required, which in turn fixes purchases and planned inventory levels.

(2) ABC Analysis: ABC System: Items of inventory are classified according to their annual consumption value into three classes: A, B and C.

Items in class 'A' are few in number but high in total value (roughly about 5-10% of items accounting for about 70-80% of value).

Items in class 'B' are of medium importance (about 20-25% of items, about 10-15% of value).

Items in class 'C' are large in number but low in value (about 65-75% of items accounting for about 5% of value).

Advantages of ABC analysis

a. Reduction in investment: High value items (A) are ordered in smaller quantities and controlled closely to reduce capital tied up.

b. Optimisation of management effort: Management focuses more on high-value items while less effort is spent on low-value items.

c. Control on high value material: Strict control can be exercised over group A items.

d. Reduction in storage cost: Lower stocks of high-value items reduce storage costs.

e. Saving in time and cost: Concentrated control on important items saves time and cost.

f. Flexible control: Items may move between classes as consumption patterns change, enabling dynamic control.

Disadvantages of ABC analysis

(a) Ineffective if classification is incorrect.

(b) Not suitable where material costs do not vary significantly.

(c) No precise scientific base for fixed percentage cut-offs; judgement is required.

(d) Classification and control may be costly for very small organisations.

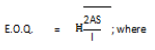

(3) Economic Order Quantity: EOQ determines the order size that minimises total cost = ordering cost + holding (carrying) cost. The formula is:

Where,

A = annual consumption (units),

S = cost per order (ordering cost),

I = carrying cost per unit per annum.

(4) VED Analysis: VED (Vital, Essential, Desirable) analysis is used mainly for spare parts control. Items classified as Vital must be available at all times, Essential should be maintained at reasonable levels and Desirable may be ordered as needed.

(5) Perpetual Inventory System: Perpetual Inventory system records receipts and issues as they occur and maintains up-to-date balances in the stores ledger and bin cards. Regular reconciliation with physical stock helps detect discrepancies early and ensures uninterrupted production.

FAQs on Cost Accounting Solved Question Papers - 1

| 1. How do I solve cost accounting problems from previous year question papers? |  |

| 2. What's the difference between process costing and job costing in B.Com cost accounting exams? | |

| 3. Why do cost accounting solved papers emphasise overhead allocation and absorption costing? | |

| 4. How can I identify which cost accounting formula to use when solving exam questions? | |

| 5. What common mistakes do students make while solving cost accounting numerical problems from previous papers? | |