Bank Cards & their Features

Types of cards

Cards issued for electronic payments and cash access can be classified by their purpose, issuer and payment mechanism. The three principal types are listed below:

- Debit cards

- Credit cards

- Prepaid cards

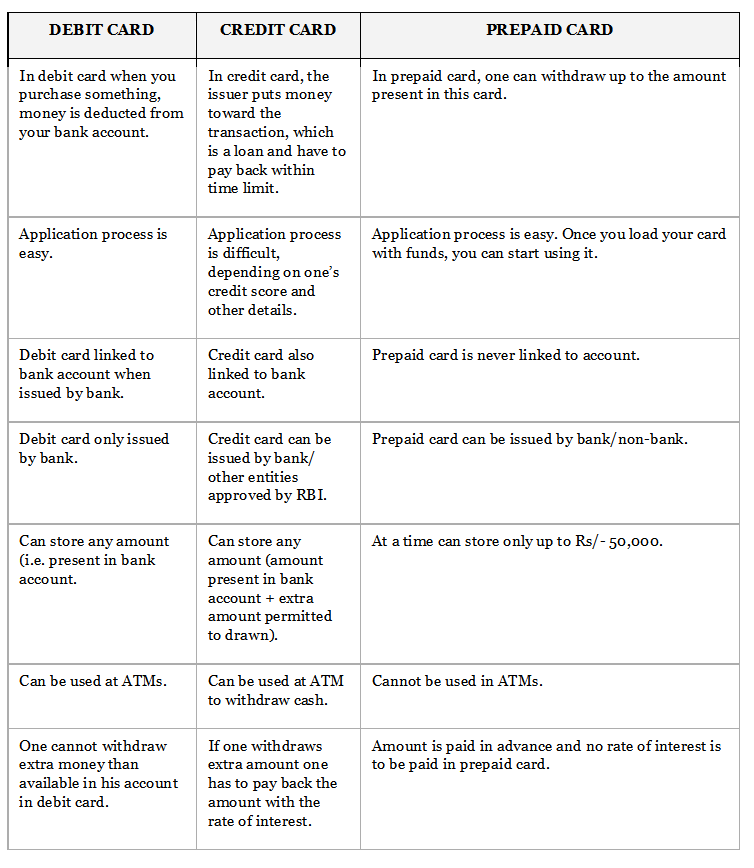

Debit cards

A debit card is issued by a bank and is linked to the cardholder's deposit account. Transactions using a debit card draw funds directly from the linked bank account.

- Usage: Withdraw cash from an ATM, pay at a Point of Sale (POS), and make online (e-commerce) purchases.

- Balance requirement: A transaction will be authorised only if there are sufficient funds in the linked account up to the account or daily withdrawal limit imposed by the bank.

- Domestic and international use: Debit cards may be enabled for domestic use only or for both domestic and international transactions depending on the card scheme and issuer.

- Common schemes: Debit cards are issued under schemes such as RuPay, Visa and MasterCard (scheme availability depends on the issuer).

- Security and authentication: Typical security features include a Personal Identification Number (PIN), EMV chip (chip-and-PIN), magnetic stripe, and sometimes a one-time password (OTP) for online transactions.

- Typical charges: Banks may levy service charges for ATM withdrawals (especially out-of-network or international), replacement cards, and other services as per their tariff schedule.

- Common variants: ATM-cum-debit cards, contactless debit cards (for tap-and-go payments), and dual-purpose cards that also support contactless or mobile wallet tokenisation.

Credit cards

A credit card allows the cardholder to obtain goods, services or cash advances on credit up to a predefined limit granted by the card issuer. The issuer may be a bank or another entity approved by the central bank.

- Credit limit: The issuer sets a credit limit. The cardholder can spend up to that limit; any amount used beyond the cardholder's available balance is treated as credit.

- Repayment and interest: Amounts due must be repaid as per the billing cycle. Interest is charged on unpaid outstanding balances after any interest-free period. Minimum payment requirements and late fees apply as per the issuer's terms.

- Transactions supported: Purchases at POS, online purchases, recurring transactions, mail-order/telephone-order (MOTO), cash advances at ATMs, and fund transfers where the issuer permits.

- Types: Unsecured credit cards (no collateral), secured credit cards (backed by a fixed deposit or other security), co-branded cards, and charge cards with different reward features.

- Features: Reward points, cashback, milestone benefits, travel and insurance benefits, EMV chip, contactless capability, and card-linked services such as instalment/EMI options.

- Security: Use of PIN for ATM and chip transactions, Card Verification Value (CVV) for card-not-present transactions, OTP for online authentication, and issuer monitoring for fraud detection.

- Issuer oversight: Credit cards are issued by banks and other authorised entities and operate under the regulator's guidelines and the rules of the card scheme.

Prepaid cards

A prepaid card is loaded with funds in advance and transactions draw down the stored balance. Prepaid cards are not linked to a deposit account unless the issuer explicitly offers that facility.

- Issuers: Prepaid cards may be issued by banks and by authorised non-bank entities.

- Stored value: The user pays or loads an amount onto the card before use; transactions deduct from that stored value.

- System classifications:

- Open system prepaid cards: Issued by banks and usable for a wide range of payments and ATM withdrawals as permitted by the issuer and the scheme.

- Semi-closed system prepaid cards: Issued by authorised non-bank entities and usable at a specified set of merchants or locations; generally do not permit ATM cash withdrawal.

- Closed system prepaid cards: Issued for use within a single merchant's ecosystem (for example, store gift cards); not usable outside that merchant.

- Usage: Depending on the type and issuer, prepaid cards can be used for POS, online purchases and, where allowed, ATM withdrawals and fund transfers.

- Reloadability: Some prepaid cards are reloadable; others (such as many gift cards) are single-use until the stored value is exhausted.

- Limits and KYC: Stored value and load limits are subject to regulatory limits and KYC requirements. At any point of time, a user may store a maximum of Rs. 50,000 on certain types of prepaid cards as per the prevailing guidelines applicable to those card categories.

- Examples: Travel cards, gift cards, payroll cards and closed-loop retail cards.

Key differences between Debit, Credit and Prepaid cards

Security features and safe practices

- Always protect the PIN and never write it on the card. Change the PIN if compromise is suspected.

- Use EMV chip enabled terminals and cards for better protection against counterfeit fraud.

- Use OTP or two-factor authentication for online card transactions where available.

- Verify the CVV and expiry details only on trusted merchant sites; do not share CVV/PIN/OTP with anyone.

- Enable transaction alerts (SMS/email) to monitor card activity in real time.

- Block the card immediately through the issuer's helpline or mobile app if lost or compromised; follow the issuer's dispute and chargeback procedure for unauthorised transactions.

- Keep KYC details updated with the issuer as per regulatory requirements-this assists in faster resolution of disputes and access to card services.

Common terms and short definitions

- EMV: A global standard for chip cards and the terminals that accept them; improves security versus magnetic-stripe cards.

- PIN: Personal Identification Number used to authenticate cardholder at ATM or POS.

- CVV: Card Verification Value printed on the card, used to authenticate card-not-present transactions.

- POS: Point of Sale device used by merchants to accept card payments.

- Cash advance: Withdrawal of cash using a credit card, usually attracting fees and higher interest.

- Credit limit: Maximum credit available on a credit card as set by the issuer.

- Stored value: Amount preloaded on a prepaid card available for spending.

Practical examples and applications

- If you want to make everyday purchases using money directly from your bank account, a debit card is appropriate.

- If you need short-term credit with benefits such as rewards or a period of interest-free credit, a credit card is suitable, provided you manage repayments promptly.

- For gifting, travel foreign currency needs, or controlled spending for certain use cases, a prepaid card may be the best choice.

Debit, credit and prepaid cards serve distinct purposes: debit cards provide direct access to bank funds; credit cards extend a line of credit with repayment obligations; and prepaid cards let users spend preloaded funds without a bank account linkage. Choice of card depends on the user's need for liquidity, credit, convenience, security features and regulatory limits.

FAQs on Bank Cards & their Features

| 1. What are the main types of bank cards? |  |

| 2. What are the key differences between debit, credit, and prepaid cards? | |

| 3. What security features are typically found on bank cards, and what safe practices should users follow? | |

| 4. What are some common terms associated with bank cards and their definitions? | |

| 5. Can you provide practical examples of when to use each type of card? | |