External Commercial Borrowings

Introduction

Capital inflows are a major tool of development policy. Historically, lack of sufficient domestic capital has led the government and firms to seek foreign capital. Foreign capital means money drawn from abroad to finance investment domestically. Major categories of foreign capital include Foreign Direct Investment (FDI), NRI deposits and External Commercial Borrowings (ECBs). ECBs are an important source of external finance for corporates, public sector undertakings and infrastructure projects.

External Commercial Borrowing

Definition

External Commercial Borrowing (ECB) refers to commercial loans, credit facilities or debt instruments raised from foreign lenders by residents (companies, institutions and sometimes government entities) for financing activities in the country. ECBs are not intended to be traded on Indian stock exchanges.

Minimum average maturity: ECBs are normally required to have a minimum average maturity of three years.

Background

The regulatory framework for overseas borrowing has been revised repeatedly by the Reserve Bank of India (RBI) and the Government to keep pace with changes in the domestic and global financial environment. Rules have been adapted to balance access to international finance with macro-financial stability and exchange-rate risks.

Significance

ECBs have become a major form of foreign capital, often complementing FDI. They have typically contributed a significant share of total capital inflows into the country.

- ECBs have accounted for around 20-35% of total capital inflows in different periods.

- They are widely used by public sector undertakings and private corporates to finance expansion and large projects that require sizeable debt funding.

- ECBs provide access to large volumes of funds at competitive interest rates available in international markets.

Objectives for ECB policy

- To channel foreign borrowings into priority sectors such as power, railways, telecom and infrastructure.

- To support capital formation in small and medium enterprises (SMEs) and other productive uses.

Regulatory framework

ECBs are governed by a two-track access mechanism: the Automatic Route and the Approval Route. The principal regulators and administrators are:

- Exchange Control Department of the RBI.

- ECB Division in the Ministry of Finance.

The main aim of ECB policy is to encourage longer maturities and to finance important sectors so as to support overall economic growth.

Borrowing limits and registration

The RBI keeps limits and conditions under the automatic route and approval route. The automatic route borrowing limit has been set at $750 per financial year under the existing provisions, with sector-wise limits replaced by consolidated access conditions.

All-in-cost ceiling

The all-in-cost ceiling is prescribed as a spread over an applicable benchmark. The prescribed ceiling is 450 basis points per annum over 6-month LIBOR or the applicable benchmark rate for the respective currency.

What is All-in-Cost? All-in-cost includes the interest rate plus other fees and charges such as processing fees, arrangement fees, guarantee fees and Export Credit Agency (ECA) charges, whether paid in foreign currency or in Indian rupees. In formula form:

- All-in-cost = Interest rate + Commitment/arrangement fees + Guarantee fees + ECA charges + Other lender charges

End-use restrictions (Negative list)

ECBs are subject to end-use prescriptions. Borrowings may not be used for certain activities. The negative list includes:

- Investment in real estate or purchase of land, except when used for affordable housing, construction and development of SEZs and industrial parks/integrated townships.

- Investment in the capital market.

- Equity investment.

- Working capital purposes.

- General corporate purposes.

Hedging requirements

To limit currency risk arising from foreign currency borrowings, hedging conditions are prescribed for certain ECBs.

- ECBs with a minimum average maturity of 3 to 5 years in the infrastructure space are required to meet a 70% mandatory hedging requirement. (Notified 6 November 2018)

Hedging typically means taking positions in instruments such as currency forward contracts, options or swaps to reduce the risk of adverse movements in the exchange rate. Mandatory hedging ensures a significant portion of the foreign currency exposure is protected for the specified hedging period.

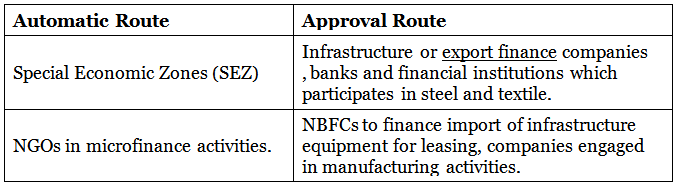

Routes to access ECBs

Automatic Route

Under the Automatic Route, eligible borrowers can enter into loan agreements with recognised foreign lenders and then register the transaction with the RBI. No prior approval from the government or RBI is required for eligible transactions within specified limits and conditions.

Approval Route

Under the Approval Route, the borrower submits an application through an authorised dealer bank to the RBI or the designated authority for prior approval. This route applies where the borrowing or the end-use falls outside the automatic route limits or conditions.

Eligible borrowers

The following classes of borrowers are generally eligible to raise ECBs under either route, subject to conditions and sectoral prescriptions:

Impact on the economy

ECBs can support large capital projects and lower the cost of borrowing for corporations because international rates may be more favourable than domestic rates. Key impacts include:

- Provision of low-cost international funds to finance infrastructure and corporate expansion.

- Enabling large-ticket financing that the domestic market may not be able to supply at similar terms.

- Potential risks to the exchange rate and external debt sustainability if ECBs grow excessively or are used for short-term or non-productive purposes; a sudden stop or reversal of capital inflows can exert depreciation pressure on the domestic currency.

Advantages

- International interest rates can be lower than domestic borrowing rates.

- Large volumes of funds can be accessed from the global financial market.

- Corporates can diversify their funding sources and tenor profile by tapping foreign lenders and export credit agencies.

Risks and cautions

- Currency risk: repayments and interest are in foreign currency, creating exchange-rate exposure.

- Refinancing risk: dependence on global markets can be problematic if international liquidity tightens.

- Macro risk: large and unhedged ECBs may contribute to external vulnerability and create pressure on the rupee.

Future outlook

Demand for ECBs may increase because of:

- Large expected investment and spending on infrastructure projects.

- Periods when domestic interest rates rise relative to international rates, encouraging firms to prefer international borrowing.

Conclusion

ECBs are an important source of external finance for a vibrant corporate and infrastructure sector. They allow firms to access large-scale, often lower-cost funds internationally when domestic markets cannot provide similar tenors or volumes. At the same time, careful regulation of end-uses, maturities, hedging and all-in-cost ceilings is essential to manage currency and external sector risks.

What's new in the ECB norms? (UPDATE)

- The minimum average maturity requirement for ECBs raised by eligible borrowers in the infrastructure space has been reduced to three years from the earlier five years.

- The average maturity requirement for mandatory hedging has been reduced to five years from the earlier ten years.

- ECBs with a minimum average maturity period of seven years can be availed for repayment of rupee loans taken domestically for capital expenditure, and can also be availed by NBFCs for on-lending for the same purpose.

- For repayment of rupee loans availed domestically for purposes other than capital expenditure, and for on-lending by NBFCs for such purposes, the minimum average maturity of the ECB is required to be ten years.