Banker's Right of Set Off

Introduction

The right of set-off (often called banker's right of set-off) is the process by which a bank combines two or more accounts of the same customer for the purpose of arriving at a single net balance and, where appropriate, adjusts one account against another for final settlement. In practice, this means a bank may recover a loan (a debit or overdraft) by appropriating funds standing to the credit of the borrower in another account maintained with the bank.

The following points state the elementary features.

- Mutuality: There must be two accounts between the same parties such that one account shows a debit (amount payable by the customer) and the other a credit (amount payable to the customer).

- Single legal entity: All branches of the same bank are ordinarily treated as one unit for this purpose; a loan from one branch may be adjusted by funds held at another branch of the same bank.

- Contract/Statutory limits: The right is subject to any contract between the bank and the customer and to applicable statutory or regulatory provisions.

Conditions for exercising the right of set-off

A bank may exercise the right of set-off only when certain legal and practical conditions are satisfied. Each condition is stated below and explained with practical clarity.

Relationship

The relationship between the party whose accounts are to be combined must be that of debtor and creditor on one side and creditor and debtor on the other, and those relationships must exist simultaneously. In other words, the bank must be both the creditor in respect of one debt and the debtor in respect of another owed to the same person (the customer).

Notice

Before appropriating funds from a deposit account, the bank should give a prior notice to the depositor expressing the intention to exercise set-off and stating the amount intended to be appropriated. The notice must be of a reasonable period so that the depositor can raise any lawful objection or make arrangements to meet the debt.

Type of loan - due and certain

The debt sought to be recovered by set-off should be certain, determined and due. A future or contingent liability (one not presently due) cannot be set-off against a present deposit. Where a customer is meeting an instalment schedule and the debt is not yet due, set-off is not ordinarily available.

Time-barred loans

Debts barred from legal action by limitation are normally not enforceable by suit; however, such debts remain lawful obligations and may be susceptible to set-off where the bank and depositor have mutual debts. Therefore, a bank may in practice set off a time-barred debt against a credit balance held by the debtor, subject to specific legal and factual circumstances.

Same name and capacity

The accounts must be in the same name and in the same capacity. Funds held in an account as trustee, agent, guardian, executor or for some other capacity distinct from the personal capacity of the customer are not ordinarily available to satisfy the customer's personal liabilities.

Partners and partnership accounts

Where a partner of a firm has a credit balance in his or her personal account, that balance may be applied in discharge of debts of the partnership firm to the bank. Conversely, a credit balance in the firm's account cannot be set off against personal liabilities of an individual partner unless that individual is personally liable to the bank on the very same basis reflected in both accounts.

Guardian and minor accounts

Accounts opened for a minor in the name of the guardian are presumed to belong to the minor and are not available to meet the personal debts of the guardian. Thus, the bank cannot normally exercise set-off against such accounts in respect of the guardian's personal liabilities.

Trust funds

Funds held on trust are separate from the personal assets of the trustee. The bank must not treat trust monies as the trustee's own and therefore cannot use those funds for set-off against the trustee's personal debts.

Joint accounts

If the customer's personal account shows a debit balance, the bank cannot recover that debit directly from a joint account in which the customer is a co-holder unless the joint account holders are also liable for the debt or the joint account is in the same capacity in which liability arises. Conversely, funds lying in the individual account of a joint-account holder may be used to settle a joint liability, where the legal relationship supports such appropriation.

Guarantor's account

The bank may exercise set-off against the account of a guarantor but only after the guarantor's liability has been fixed by demand or by the occurrence of a contractual event that makes the guarantor's obligation due. A mere contingent or potential liability of a guarantor does not permit set-off until it becomes actual.

Term deposits not yet due

Term deposits which have not yet matured are not ordinarily available for set-off until they fall due, unless there is an express agreement between the depositor and the bank permitting premature encashment or the depositor authorises the bank to appropriate the deposit. The bank's right to set-off will therefore normally await maturity of the term deposit unless other contract terms apply.

Procedure, computation and examples

Typical steps a bank follows when exercising set-off:

- Identify the mutual accounts and confirm that one is debit and the other credit.

- Check that both accounts are in the same name and capacity or otherwise legally mutually due.

- Ensure the debt sought to be recovered is due and not barred from set-off by contract or statute.

- Issue a prior notice to the depositor stating the intention to set-off and allow a reasonable time to respond.

- Compute the net balance after appropriation and communicate the result to the customer.

Example 1 - simple numeric illustration:

- Customer's current account at Branch A: overdraft of ₹150,000 (debit).

- Customer's savings account at Branch B: balance ₹200,000 (credit).

- Bank gives notice and after reasonable time appropriates ₹150,000 from the savings account to settle the overdraft.

- Result: savings account reduced to ₹50,000; overdraft settled.

Example 2 - joint account nuance:

- Mr X has a personal overdraft with the bank of ₹80,000 in his individual name.

- Mr X also maintains a joint savings account with Mrs Y having a balance of ₹120,000.

- The bank cannot automatically appropriate funds from the joint account to pay Mr X's personal liability unless Mrs Y is also liable for that indebtedness or the account terms make funds available for such set-off.

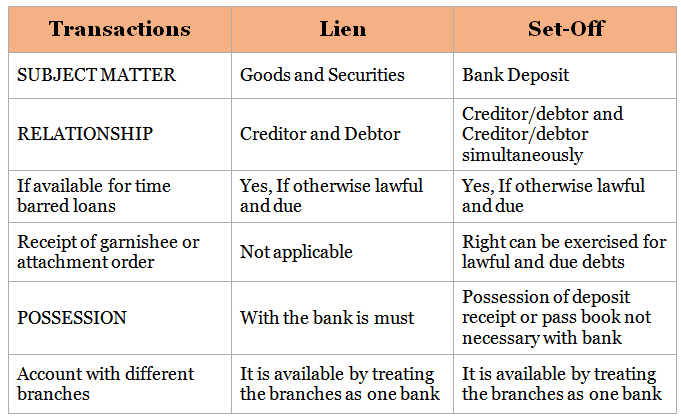

Lien and set-off - key distinctions

Although both lien and set-off are rights a banker may use to protect its position vis-à-vis a customer, they are distinct in nature:

- Nature: A lien is a right to retain the customer's goods or property in the banker's possession until the customer's debt is paid. Set-off is a right to combine mutual accounts and adjust balances.

- Subject matter: Lien applies to tangible property or specific securities in the banker's possession; set-off applies to monetary balances in accounts.

- Operation: Lien involves detention/retention of property; set-off involves appropriation of money from one account to discharge another.

- Consent and agreement: Specific agreement or conduct may create a contractual lien; statutory or equitable rules also operate. Set-off arises from mutual debts between the bank and customer and is subject to notice and mutuality.

- Limitations: Trust property and funds held for a specific purpose generally cannot be subject to lien or set-off for the banker's personal debts.

Practical points, limits and good banking practice

- Banks should act in good faith and give adequate notice before exercising set-off.

- Internal bank rules and product terms determine whether branches may appropriate funds held elsewhere; banks must comply with their own terms and applicable law.

- Courts may restrain a bank from exercising set-off where the exercise would be unconscionable, contrary to statute or would defeat known third-party rights (for example, where funds are subject to an attachment or injunction).

- Where doubt exists about the capacity in which funds are held (personal versus fiduciary), banks should seek clarification and documentary proof before appropriation.

Conclusion

The banker's right of set-off is an important tool for recovery and internal account management, but it is bounded by principles of mutuality, identity of parties and capacity, the requirement of a debt being due, proper notice, and respect for trust, guardian and third-party rights. Proper application requires careful verification of the legal status of each account, clear communication with the customer and adherence to contractual and regulatory constraints.