Production & Costs Class 12 Economics

| Table of contents |

|

| Production |

|

| Production Function |

|

| Total product or Total physical product |

|

| Law of Variable Proportion |

|

| Economic Cost |

|

| MR and MC Methodology |

|

Production

Production mainly focuses on converting resources into goods or services that are useful or valuable to people.

Production Function

In the process of manufacturing, the production function of a firm represents the correlation between the output and production factors involved, where physical inputs are utilized. It shows the minimum amount of inputs required to attain the highest level of final output.

The production function is expressed using the following formula:

Q = f (x1 , x2)

The final quantity of output is represented by Q, while the amounts of production factor 1 and 2 are denoted by x1 and x2, respectively. The equation demonstrates that these production factors can be employed to generate the final output.

Types of Production Function:

There are two types of Production Function.

- Short-run Production Function: The short-run production function is a type of production function in which one production factor is variable, while the others are fixed. This means that the law of return to a factor applies, and it is sometimes referred to as the variable proportion production function. This production function is applicable when there is insufficient time to change all inputs, and only the variable factors can be altered.

- Long-run Production Function: The long-run production function, on the other hand, is a type of production function in which all production factors are variable, and the law of diminishing returns to scale applies. It is sometimes referred to as the constant proportion production function. This production function is applicable when there is enough time to change all inputs, and all inputs can be varied.

Total product or Total physical product

The total product is the cumulative output of a firm that results from utilizing a specific amount of inputs within a specified period. It represents the relationship between the variable inputs of production and the final output, with all other production factors held constant. The following formula can be used to calculate the total product:

Total Product = ∑Qx

The formula shown above represents the correlation between the final output and the variable factors of production.

Average production

The average production is the variable factor's per unit production.

Marginal product can be defined as the increase in total output that results from the utilization of one additional unit of variable factor. Essentially, it measures the impact of each extra unit of a variable factor on the total production output.

Marginal Product of an Input

Law of Variable Proportion

The law of variable proportion suggests that as a firm increases the use of variable factors to produce more output, the initial increase in output is at an increasing rate before eventually diminishing.

Stage I (Stage of Increasing Return to factor)

The first stage of production is known as the Stage of Increasing Return to Factor, where the total physical production (TP) increases at an ever-increasing rate. During this stage, the marginal product (MP) also rises as more units of variable factors are combined with fixed factors. There are several reasons for the increased return, such as the underutilization of fixed factors, the indivisibility of factors, and the increased efficiency of variable factors.

Stage II (Stage of Diminishing Return to factor)

During the Stage II, also known as the Stage of Diminishing Return to factor, the total product (TP) increases at a decreasing rate when additional units of variable factors are combined with fixed factors. Meanwhile, the marginal product (MP) decreases but remains positive until the end of this phase, where TP reaches its maximum and MP is zero.

The diminishing returns occur due to two reasons. Firstly, the fixed factor is being utilized at its best level. Secondly, the factor substitutability is unsatisfactory.

Stage III (Stage of negative return to factor)

In Stage III, also known as the stage of negative return to factor, total output decreases as more units of variable factors are added to fixed factors, resulting in a negative marginal product. This stage is caused by inadequate coordination between fixed and variable factors and excessive use of fixed factors.

Economic Cost

Economic cost is the sum of explicit and implicit costs.

- Explicit Cost: Explicit cost refers to the actual expenditure incurred by a firm on the purchase and hiring of factor inputs for production. These costs are recorded in the accounting books and include expenses such as wage payments, rent, interest payments, raw material purchases, and others.

- Implicit cost: Implicit cost represents the opportunity cost of utilizing self-owned production resources or inputs provided by the owner. These costs are not recorded in the accounting books and include the estimated value of the inputs used.

- Normal profit: Normal profit is the minimum amount required to keep the producers in business, also known as the entrepreneur's minimum supply price or wage.

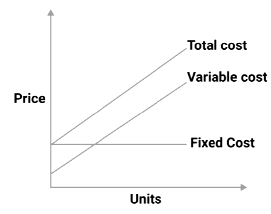

- Total cost: Total cost is the overall amount of money spent by a company to produce a specific quantity of a commodity. It includes the sum of total fixed and variable costs.

TC = TFC + TVC or TC = AC× Q

TFC = TC - TVC or TFC = AFC×Q

Features of Total Fixed Cost

- The TFC curve is parallel to the X-axis and remains constant at all levels of output. It does not become zero even when the output level is zero.

- The total cost at zero output level is equivalent to the total fixed cost.

Total variable cost

The cost that changes with the level of production is known as variable cost. Variable cost is equal to zero when the output level is zero. The TVC (Total Variable Cost) curve is perpendicular to the TC (Total Cost) curve, which excludes costs such as raw material expenses, power expenses, etc.

TVC = TC – TFC or TVC = AVC × Q

Features of Total variable cost: -

- It starts at zero when output is zero.

- It increases proportionally with the level of output.

- Initially, TVC increases at a decreasing rate due to increasing returns to scale, but later it increases at an increasing rate due to diminishing returns to scale.

Average cost

The per-unit expense incurred in manufacturing a product is referred to as its production cost, which comprises the combined amount of average fixed and variable expenses.

Average fixed cost

It is the fixed cost of producing a commodity per unit.

Features of AFC :-

- As output increases, AFC decreases.

- A rectangular hyperbola is the shape of the AFC curve.

- It cannot cross the X or Y axes.

Average variable cost:

The per-unit variable expenditure involved in the production of a commodity is known as its variable cost. As per the law of variable proportions, the AVC (average variable cost) follows a U-shaped curve.

Relation between Short-Term Costs

- The total cost curve and the total variable cost curve maintain a constant distance from each other. The vertical gap between these two curves represents the total fixed cost. The TFC curve runs parallel to the X-axis, while the TVC curve remains parallel to the TC curve.

- As production output rises, the vertical distance between the average fixed cost (AFC) curve and the average cost (AC) curve widens. Meanwhile, the vertical gap between the average variable cost (AVC) and the AC curves narrows, but these two curves do not intersect as the average fixed cost can never reach zero.

MR and MC Methodology

As per this perspective, the requirements for achieving producer equilibrium are as follows:

- (MC should be equal to MR, and AR should also equal MR, resulting in AR = MR = MC. Furthermore, MC should be increasing.

- At the equilibrium position, the MC curve must intersect the MR curve from below. Alternatively, following the equilibrium point, an increase in output should result in MC being greater than MR.

Normal Profit

When the price (P) equals the average cost (AC), it is referred to as a break-even scenario, in which there is neither profit nor loss. This represents the lowest level of return that a producer anticipates from investing capital in the business.

- The break-even point is reached when the average revenue (AR) equals the average cost (AC), or when total revenue (TR) equals total cost (TC). This implies that the firm is not earning any economic profit or normal profit, but simply covering its costs.

- The shut-down point occurs when a company is only able to cover its variable costs, resulting in a loss of fixed costs. (TR < TVC or AR < AVC)

- Supply refers to the quantity of a product that a firm or seller is willing to offer for sale at various prices during a specific period.

|

162 videos|102 docs|66 tests

|

|

Dec 22, 2024 Last updated |

|

Explore Courses for JAMB exam

|

|

Production & Costs Class 12 Economics

,Viva Questions

,MCQs

,Previous Year Questions with Solutions

,Summary

,Production & Costs Class 12 Economics

,mock tests for examination

,study material

,practice quizzes

,Production & Costs Class 12 Economics

,Semester Notes

,Sample Paper

,Exam

,shortcuts and tricks

,past year papers

,Important questions

,Objective type Questions

,Extra Questions

,Free

,video lectures

,ppt

;

Chapter Notes: Production & Costs Free PDF Download

Importance of Chapter Notes: Production & Costs

Chapter Notes: Production & Costs

Chapter Notes: Production & Costs JAMB Questions

Study Chapter Notes: Production & Costs on the App

|

© EduRev

|

Education Revolution

|

|