Important Questions: Production & Costs

Very Short Answer Type Questions

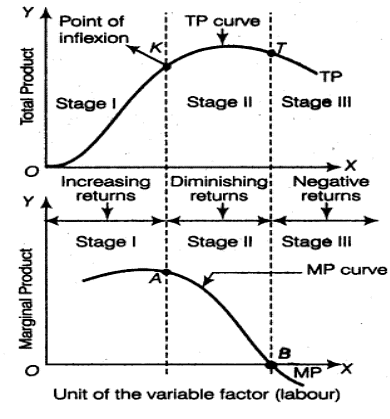

Q1: What will be the MP when TP is maximum?

Ans: Marginal Product will be zero when Total Product is maximum.

Explanation: At the output level where Total Product reaches its highest point, an additional unit of the variable factor adds no extra output, so Marginal Product (MP) = 0.

Q2: TPP increases only when MPP increases.

Ans: False. TPP can continue to increase even when MPP is falling, provided MPP remains positive.

Explanation: If marginal product is positive but declining, each extra unit still adds to total output, so Total Product rises, though at a diminishing rate.

Q3: When there are diminishing returns to a factor marginal and total products always fall.

Ans: False. Only Marginal Physical Product (MPP) falls under diminishing returns; Total Physical Product (TPP) continues to rise but at a decreasing rate until MPP becomes zero or negative.

Explanation: Diminishing returns mean each extra unit adds less than the previous one, not necessarily a negative addition to total output.

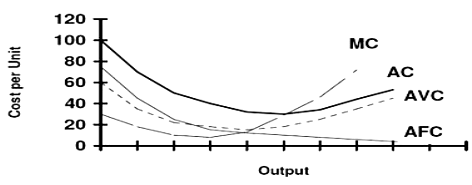

Q4: Why AFC curve never touches "x‟ axis though lies very close to x axis?

Ans: Because Total Fixed Cost (TFC) can never be zero.

Explanation: Average Fixed Cost (AFC) = TFC/quantity. As quantity increases AFC approaches zero but never becomes zero unless TFC = 0, which is not possible when fixed costs exist (e.g., rent, machinery).

Q5: What is meant by production?

Ans: Production means the transformation of inputs into outputs through a specific process to create goods or services.

Q6: When there are diminishing returns to a factor, total product always decreases.

Ans: False. Total Product increases at a decreasing rate when there are diminishing returns; it only falls when Marginal Product becomes negative.

Explanation: Diminishing returns reduce the extra output from each additional unit, but do not immediately reduce total output.

Q7: Increase in TPP always indicates that there are increasing returns to a factor.

Ans: False. An increase in TPP only shows that additional units are adding to output; the rate of increase may be rising (increasing returns) or falling (diminishing returns).

Explanation: If TPP rises but the increments shrink, the situation is diminishing returns even though TPP is increasing.

Q8: Why AVC and AFC always lie below AC?

Ans: Because Average Cost (AC) is the sum of Average Variable Cost (AVC) and Average Fixed Cost (AFC). Therefore AC = AVC + AFC, and AC is always greater than or equal to either AVC or AFC taken separately.

Explanation: Since AFC is positive for positive output, AC remains above AVC; similarly AVC is usually positive so AC is above AFC.

Q9: When TVC is zero at zero level of output, what happens to TFC or Why TFC is not zero at zero level of output?

Ans: Fixed costs have to be incurred even at zero level of output.

Explanation: Total Variable Cost (TVC) is zero when output is zero, but Total Fixed Cost (TFC) such as rent, depreciation or salaried labour still remains and must be paid regardless of production.

Short Answer Type Questions

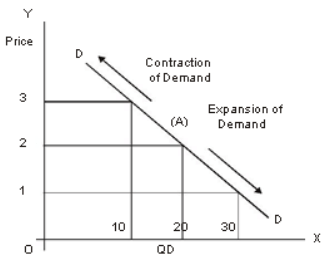

Q10: What is change in quantity demanded?

Ans: It is also called a movement along a demand curve. It occurs when the own price of a commodity changes and, as a result, the quantity demanded changes. Types:

- Extension in Demand

- Contraction in Demand

Q11: Define cost concept. What are the different types of costs?

Ans: Cost refers to the value of resources sacrificed or used to produce goods or provide services. It is a central concept in business decision making.

There are several types of costs:

- Fixed Costs (FC): Expenses that do not change with the level of output within the relevant range (e.g., rent, insurance, salaried staff).

- Variable Costs (VC): Costs that vary directly with output (e.g., raw materials, direct labour paid per unit).

- Total Cost (TC): Sum of fixed and variable costs: TC = FC + VC.

- Marginal Cost (MC): The additional cost of producing one more unit of output; MC = ΔTC / ΔQ.

- Average Fixed Cost (AFC): FC divided by output (AFC = FC/Q); it falls as output increases.

- Average Variable Cost (AVC): VC divided by output (AVC = VC/Q); its shape depends on production technology and factor returns.

- Average Total Cost (ATC or AC): TC divided by output (AC = TC/Q) and equals AFC + AVC.

- Explicit Costs: Actual monetary payments made by a firm (wages, rent, utilities).

- Implicit Costs: Opportunity costs of using owner-supplied resources for which no direct payment is made (e.g., foregone salary of the owner).

- Sunk Costs: Costs already incurred and irrecoverable; they should not affect future decisions.

- Economic Cost: Sum of explicit and implicit costs; it measures the true opportunity cost of production.

Q12: What are Returns to a Factor? What do you mean by the Law of Diminishing Returns?

Ans: Returns to a Factor describe how output changes when only one input is varied while other inputs remain fixed (a short-run concept).

Law of Diminishing Returns: When units of a variable factor are added to fixed factors, marginal product first rises (due to better utilisation), reaches a maximum, and then begins to decline. Eventually marginal product may become zero and then negative. This decline in marginal product after a point is the essence of the law of diminishing returns.

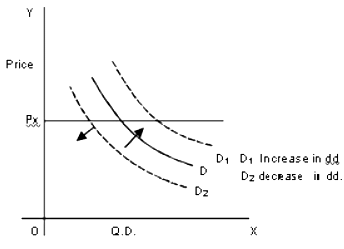

Q13: What is change in demand?

Ans: Change in Demand (also called a shift in the demand curve) happens when quantity demanded changes due to factors other than the good's own price. It can be:

(a) Increase in Demand

(b) Decrease in Demand

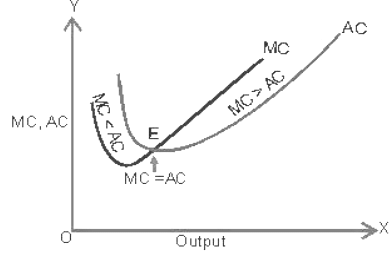

Q14: Explain the relation between AC and MC with the help of a diagram.

Ans: The relation between Average Cost (AC) and Marginal Cost (MC) is as follows:

Observations:

- When AC declines, MC declines faster than AC. So that MC curve remains below AC curve. Implying that AC > MC. In the figure, AC curve is falling till point E and MC continues to be lower than AC.

- When AC increases, MC increases faster than AC. So that MC curve is above the AC curve. Implying that AC < MC. In the figure, AC start rising from point E and beyond E, MC is higher than AC.

- MC curve cuts AC curve from its lowest point. When average curve is minimum then MC = AC. In the figure, MC curve is intersecting AC curve at its lowest or minimum point E.

Long Answer Type Questions

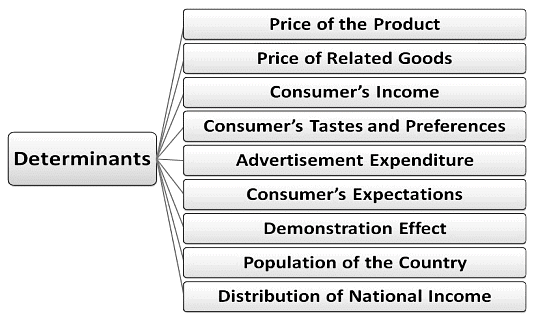

Q15: Explain the determinants of supply?

Ans: Supply is the quantity of a good that producers are willing to sell at a given price over a period of time. It represents how much firms offer for sale, not necessarily how much is actually sold.

The supply function can be written as:

Sx = f (Px, Pa... Pc, PL... PO, T, Cr, St, O, G)

Where Px is own price of good x; Pa...Pc are prices of related goods; PL...PO are prices of inputs; T is time; St is state of technology; O refers to objectives of the firm; and G stands for government policies (taxes, subsidies, regulation).

Some of the key determinants explained:

- Production Cost: Higher input prices or costs reduce profit and discourage supply; lower costs raise supply.

- Technology: Better technology reduces per-unit cost and raises supply by making production more efficient.

- Number of Sellers: More sellers in the market increase total market supply.

- Expectations About Future Prices: If producers expect higher future prices, they may withhold supply now to sell later at higher prices, reducing current supply.

- Government Policies: Taxes can reduce supply while subsidies and favourable regulation can increase it.

Q16: Explain the relation between Marginal Cost and Average Variable Cost with the help of diagram.

Ans: The relationship between Marginal Cost (MC) and Average Variable Cost (AVC) is similar to that between MC and AC:

- When MC is less than AVC, AVC falls.

- When MC is greater than AVC, AVC rises.

- The MC curve cuts the AVC curve at AVC's minimum point; at that point MC = AVC.

Practical note: Variable costs and marginal costs are closely linked because marginal cost reflects the change in variable cost when output changes. For example, if a baker considers adding a new item, she should compare the marginal cost of producing that item with the expected price to decide if it is profitable.

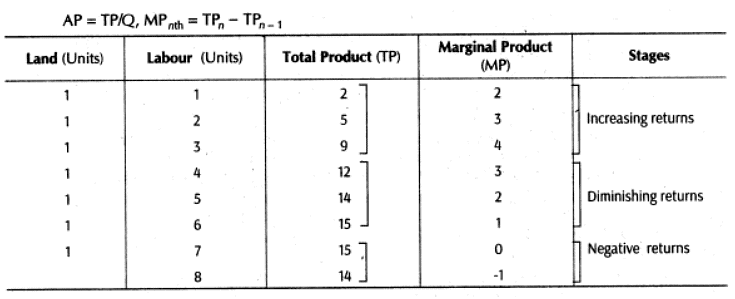

Q17: State the behaviour of Marginal product in the Law of Variable Proportions. Explain the causes of this behaviour.

Ans: The Law of Variable Proportions states that as more units of a variable factor (e.g., labour) are added to fixed factors (e.g., land, machinery), the Marginal Product (MP) of the variable factor initially rises, then reaches a maximum, and thereafter starts to fall. This behaviour is shown in the diagrams below:

Observations from the diagram/table:

(i) MP rises up to the 3rd unit of labour; during this phase Total Product (TP) increases at an increasing rate - this is the stage of increasing returns.

(ii) With the 4th unit of labour MP begins to fall while TP continues to increase but at a decreasing rate - this is diminishing returns.

(iii) When MP falls to zero, TP is at its maximum.

(iv) When MP becomes negative, TP declines.

Causes of this behaviour:

- Fixed Factors: With some inputs fixed, adding more of the variable factor initially improves utilisation of fixed resources, raising MP.

- Crowding: Beyond a point, additional units of the variable factor cause crowding and inefficiency, so each extra unit contributes less output.

- Poor Coordination: When too many variable inputs are used with fixed inputs, coordination falls and MP declines.

- Limited Indivisible Factors: Certain inputs or machines have fixed capacities; once those are fully utilised, extra labour cannot produce proportional output increases.

These reasons together explain why marginal product follows the typical rising-then-falling pattern described by the law of variable proportions.

FAQs on Important Questions: Production & Costs

| 1. What's the difference between total product, marginal product, and average product in economics? |  |

| 2. How do fixed costs and variable costs affect my profit calculations? | |

| 3. Why does marginal cost curve intersect average cost at its lowest point? | |

| 4. What exactly is diminishing marginal returns and when does it happen during production? | |

| 5. How do I calculate total cost, and what's included in the formula for CBSE economics? | |