Worksheet Solutions: Indian Economy 1950-1990 - 1

Multiple Choice Questions

Q1: What was the primary objective of India's economic policy during 1950-1990?

(a) Achieving rapid industrialization

(b) Focusing on agricultural growth

(c) Ensuring social justice and equitable distribution of wealth

(d) Promoting foreign investments

Ans: (c) Ensuring social justice and equitable distribution of wealth

Explanation: India's post-independence policy followed a mixed-economy model with an emphasis on planned development. The government used Five-Year Plans, land reforms and expansion of the public sector to reduce inequality and provide basic services. While industrialisation and agriculture were important, the central policy goal was to achieve social justice and a more equitable distribution of wealth.

Q2: Which of the following sectors saw significant reforms in the 1990s liberalization era?

(a) Agriculture

(b) Manufacturing

(c) Services

(d) All of the above

Ans: (d) All of the above

Explanation: The 1991 reforms reduced controls across the economy. Manufacturing and services saw deregulation, easier licensing and greater foreign participation. Agriculture experienced policy shifts such as reduced trade barriers and increased market orientation. Hence, reforms affected all three sectors, though the degree and pace varied by sector.

Q3: Who was the first Prime Minister of India to introduce economic planning?

(a) Jawaharlal Nehru

(b) Indira Gandhi

(c) Rajiv Gandhi

(d) Lal Bahadur Shastri

Ans: (a) Jawaharlal Nehru

Explanation: Jawaharlal Nehru led the adoption of Five-Year Plans soon after independence and helped set up the Planning Commission. Planning under his leadership prioritised heavy industries, infrastructure and a mixed economy framework.

Q4: Which economic policy in the 1980s aimed at promoting decentralization and local self-sufficiency?

(a) Green Revolution

(b) New Economic Policy

(c) Panchayati Raj

(d) Make in India

Ans: (c) Panchayati Raj

Explanation: Panchayati Raj refers to the system of local self-government. Strengthening Panchayati Raj institutions in the 1980s sought to decentralise decision-making, increase local participation in development and promote self-sufficiency at the village level.

Q5: What was the major factor that led to the balance of payments crisis in India during the 1980s?

(a) Excessive government spending

(b) Decline in export competitiveness

(c) Increase in foreign aid

(d) Stable global oil prices

Ans: (b) Decline in export competitiveness

Explanation: The balance of payments problems were the result of a combination of factors, including a widening trade deficit and weak export performance. Declining export competitiveness meant exports did not keep pace with imports, worsening the deficit. External shocks, high oil import bills and fiscal imbalances further strained foreign exchange reserves.

True and False

Q1: The Indian economy during 1950-1990 was primarily agrarian.

Ans: True

Explanation: Agriculture provided the livelihood for the majority of the population and contributed a large share of national employment. Although the industrial sector grew over the period, agriculture remained central to the economy in terms of employment and rural incomes.

Q2: The Green Revolution in the 1960s contributed significantly to agricultural productivity.

Ans: True

Explanation: The Green Revolution introduced high-yielding varieties, better irrigation, fertilizers and improved farming practices. These changes raised foodgrain production considerably, helping achieve food self-sufficiency in many regions.

Q3: India's economic policies during this period emphasized self-reliance and import substitution.

Ans: True

Explanation: Policy choices such as high import tariffs, quantitative restrictions and a focus on domestic industrial development under the licence-permit system were intended to reduce dependence on imports and build domestic capacity.

Q4: The Industrial Policy of 1956 aimed at promoting the private sector in key industries.

Ans: False

Explanation: The Industrial Policy Resolution of 1956 expanded the role of the public sector and reserved key heavy and basic industries for state ownership, while the private sector was encouraged in other areas under regulated conditions.

Q5: Economic reforms in the 1990s were triggered by a balance of payments crisis.

Ans: True

Explanation: The acute foreign exchange shortage and near-default situation in 1991 forced the government to adopt structural reforms aimed at liberalising the economy, restoring investor confidence and stabilising external accounts.

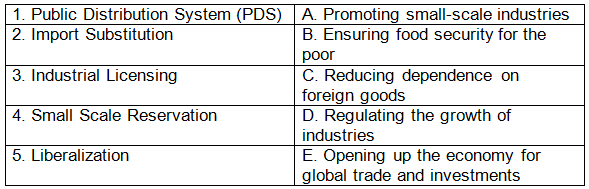

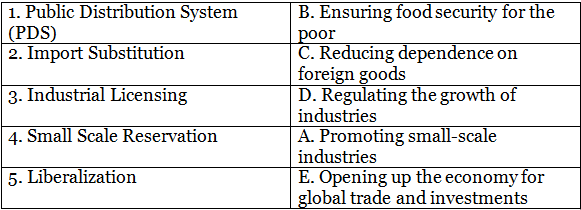

Match the Following

Q: Match the economic policy/tool with its objective.

Ans:

Very Short Answers

Q1: What is the significance of the Green Revolution in Indian agriculture?

Ans: The Green Revolution significantly increased foodgrain production in India by introducing high-yielding varieties, improved irrigation and modern farming practices. It reduced dependence on food imports, improved food security and raised rural incomes in many areas.

Q2: Name one major economic challenge faced by India in the 1980s.

Ans: Balance of payments crisis - a persistent trade deficit and weak foreign exchange reserves that constrained imports and external payments.

Q3: Define import substitution industrialization.

Ans: Import substitution industrialization is a strategy that promotes domestic production of goods previously imported, using tariffs, quotas and incentives to develop local industries and reduce reliance on foreign products.

Q4: Why was the policy of liberalization introduced in India in 1991?

Ans: Liberalization was introduced to stabilise the economy after the balance of payments crisis, attract foreign investment, improve competitiveness and integrate India more closely with the global economy.

Q5: Briefly explain the concept of Five-Year Plans in India's economic planning.

Ans: Five-Year Plans are government blueprints that set economic goals and allocate resources for a five-year period. They prioritise sectors, set targets for production and investment, and guide public expenditure to achieve balanced growth.

Short Answers

Q1: Discuss the impact of the Industrial Policy of 1956 on the Indian economy.

Ans: The Industrial Policy of 1956 broadened the scope of the public sector by reserving key heavy and basic industries for state control. It aimed to build a strong industrial base, reduce dependence on imports and accelerate planned development. The policy led to the establishment of many public sector undertakings and helped create industrial infrastructure, though it also increased the role of state bureaucracy in industry.

Q2: Explain the role of the public sector in India's economic development during 1950-1990.

Ans: The public sector played a central role in building infrastructure, establishing heavy industries, power plants, steel plants and transport networks. It aimed to provide strategic goods and services and promote balanced regional development. While it helped create capacity where private investment was lacking, inefficiencies, under-pricing and bureaucratic delays limited productivity in some enterprises.

Q3: How did the Green Revolution transform Indian agriculture and rural economy?

Ans: The Green Revolution raised yields and production of cereals in many areas, improving food security and increasing farmers' incomes. It encouraged mechanisation, better irrigation and the use of fertilisers, which boosted rural demand and ancillary industries. However, benefits were uneven: regions with good irrigation gained more, and small farmers sometimes faced barriers to adopting new technologies.

Q4: Analyze the reasons behind the balance of payments crisis in India during the 1980s.

Ans: The crisis resulted from multiple factors: a growing trade deficit as imports rose faster than exports; weak export competitiveness; high oil import bills after global price shocks; and fiscal deficits that increased external borrowings. These factors depleted foreign exchange reserves and created pressure on external payments.

Q5: Describe the objectives and outcomes of the New Economic Policy of 1991.

Ans: The main objectives were to liberalise the economy, deregulate industry, reduce protection, encourage foreign investment and privatise non-strategic public enterprises. Outcomes included faster GDP growth, increased foreign inflows, expansion of services and manufacturing sectors, and greater integration with world markets. The reforms also posed challenges such as rising regional and income inequalities that required further policy attention.

Long Answers

Q1: Economic Policies During 1950-1990: Discuss the major economic policies adopted by the Indian government during 1950-1990, emphasizing their objectives and impact on the economy.

Ans: India followed a mixed-economy model with a heavy emphasis on planning and state intervention. Key features included:

- Five-Year Plans: Central planning with sectoral targets and public investment priorities.

- Import substitution: High tariffs and licensing to encourage domestic industry.

- Strong public sector: Reservation of key industries for state ownership to build core industrial capacity.

- Agricultural reforms: Green Revolution technologies to raise foodgrain output.

Impact: These policies built industrial and agricultural capacity and improved food security, while aiming for social justice. However, rigid controls, the licence-permit raj and bureaucratic inefficiencies restrained private initiative and contributed to relatively slow growth in some decades.

Q2: Impact of Liberalization: Evaluate the impact of economic liberalization on various sectors of the Indian economy, highlighting its positive and negative consequences.

Ans: Liberalisation opened the economy through reduced controls, lower tariffs and encouragement of foreign investment. Positive effects included higher GDP growth, expansion of the services sector (especially IT and finance), better access to capital and technology, and more competitive industries. Negative consequences included greater exposure to global fluctuations, rising income inequality in some regions and environmental stresses. Overall, liberalisation improved macroeconomic performance but required complementary policies to address social and regional imbalances.

Q3: Role of Agriculture: Analyze the role of agriculture in India's economic development during the period 1950-1990, considering the Green Revolution and its socio-economic impact.

Ans: Agriculture remained central to livelihoods and rural incomes. The Green Revolution increased productivity and food availability, reduced import dependence and raised rural purchasing power, which stimulated demand for non-farm goods. Socio-economic impacts included improved incomes for many farmers, some rural industrial growth and increased regional disparities where irrigation and inputs were unevenly available. Support services and rural infrastructure improved in many areas.

Q4: Challenges and Reforms: Identify the key challenges faced by the Indian economy in the 1980s. Discuss the economic reforms initiated in response to these challenges, focusing on their effectiveness and outcomes.

Ans: Key challenges in the 1980s included a widening trade deficit, inflationary pressures, fiscal imbalances and inefficient public enterprises. The crisis culminated in acute foreign exchange shortages by 1991. Reforms introduced in 1991 aimed at stabilisation and structural change: devaluation and fiscal correction were followed by liberalisation (deregulation, reduced tariffs), privatisation of non-strategic PSUs and measures to boost exports and foreign investment. These reforms stabilised the economy, increased growth rates and integrated India with global markets, though some social challenges like unemployment and regional inequality persisted.

Q5: Comparative Analysis: Compare and contrast India's economic policies and performance during 1950-1990 with another developing country of your choice, highlighting similarities, differences, and lessons that can be learned.

Ans: Comparing India with Brazil during the same period shows both similarities and differences:

- Similarities: Both countries pursued state-led development, with important roles for public enterprises and protectionist policies in early decades. Each faced external shocks and debt problems in the 1980s.

- Differences: India emphasised import substitution and planning with a larger focus on self-reliance; Brazil, at times, pursued more outward-oriented policies and relied heavily on export commodities and foreign borrowing. Policy responses and timing of reforms also differed.

- Lessons: Balanced opening with strong domestic institutions helps; timely structural reforms can correct external imbalances; and attention is needed to ensure that growth is inclusive and regionally balanced.

FAQs on Worksheet Solutions: Indian Economy 1950-1990 - 1

| 1. What were the major economic policies implemented in India between 1950-1990? |  |

| 2. How did the Green Revolution impact the Indian economy during the 1960s and 1970s? | |

| 3. What were the key challenges faced by the Indian economy during the 1980s? | |

| 4. How did economic liberalization in 1991 change the course of Indian economy? | |

| 5. What role did the public sector play in the Indian economy during the period of 1950-1990? | |