Worksheet Solutions: Trial Balance and Rectification of Errors

Q1: If the suspense account indicates a debit balance, it shows that ____ column of the trial balance is more than the ____ column.

Ans: Credit, Debit

Q2: ____ balance of personal account represents the amount payable to him.

Ans: Credit

Q3: Nominal account having credit balance represents ____.

Ans: Income

Q4: In rectification entry purchase account......................... if purchased goods were not posted in purchase account.

Ans: debit

Q5: Commission account debited by Rs. 500 instead of rent account, so in rectification entry rent account will____

Ans: debit Rs. 500

Q6: Ajay a debtor not included in the list of sundry debtors list. To rectifying this error Ajay account will____.

Ans: debit

MCQs

Q1: Outstanding interest Rs.1,000; prepaid rent Rs. 1,000 ; debtors Rs.2,000; creditors Rs.2,000 ; building Rs.20,000. The amount of capital is ___________.

(a) 30,000

(b) 10,000

(c) 20,000

(d) 15,000

Ans: (c)

Q2: Capital and interest on capital have ______ and _______ balances respectively in a trial balance.

(a) Credit and debit

(b) Debit and credit

(c) Debit and debit

(d) Credit and credit

Ans: (a)

Q3: Interest on given loan and loans and advances (given) have ________and________ balances respectively in a trial balance.

(a) Debit and credit

(b) Debit and debit

(c) Credit and credit

(d) Credit and debit

Ans: (d)

Q4: A dealer dealing in furniture business purchased furniture, recorded in furniture account.

(a) There is an error in the above transaction, but trial balance will agree.

(b) There is not any error in the above transaction, trial balance will not agree.

(c) There is an error and trial balance will not agree.

(d) None

Ans: (a)

Q5: Rent paid for Rs. 5,000 was posted as 5,200 and carriage outwards paid for Rs.8,000 was posted as 7,800. Identify the type of error.

(a) Error of commission

(b) Error of omission

(c) Compensating errors

(d) Error of principle

Ans: (c)

Q6: After providing the trial balance the accountant finds that the total of debit side is short by Rs 2,500. This difference will be

(a) Credited to suspense account

(b) Debited to suspense account

(c) Adjusted to any of the debit balance accounts

(d) Adjusted to any of the credit balance accounts

Ans: (b)

Q7: Rs 3,000 received from sub-tenant for rent and entered correctly in the cash book is posted to the debit of the rent account, in the trial balance

(a) The debit total will be greater by Rs 6000 than the credit total

(b) The debit total will be greater by Rs 3000 than the credit total.

(c) Subject to other entries being correct the total will agree.

(d) None of the above

Ans: (a)

Q8: Sales to Shyam of Rs500 not recorded in the books would affect

(a) Shyam's Account

(b) Sales Account

(c) Sales Account and Shyam's Account

(d) Cash Account

Ans: (c)

Q9: Sales to Ram, Rs 336 posted to his account as Rs 363 will affect:

(a) Sales account

(b) Ram's account

(c) Cash Account

(d) All accounts

Ans: (b)

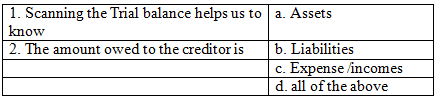

Q10:

Ans: 1-b 2-a

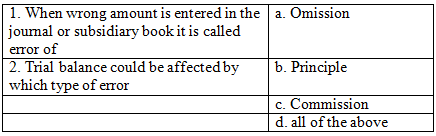

Q11:

Ans: 1 -d 2 - b

Q12:

Ans: 1-a 2- b

Q13:

Ans: 1-c 2 - d

Q14: Sale of office furniture is credited to

(a) Sales Account.

(b) Office Furniture Account.

(c) Cash Account.

(d) None of these.

Ans: (b)

Q15: Suspense Account will give the

(a) Debit balance.

(b) Credit balance.

(c) Debit or credit balance, as the case may be.

(d) None of these.

Ans: (c)

Q16: Wages paid to Mohan for erecting a machine should be debited to :

(a) Wages A/c

(b) Machine A/c

(c) Mohan's A/c

(d) Cash A/c

Ans: (b)

Q17: Sale of typewriter that has been used in the office should be credited to :

(a) Sales A/c

(b) Cash A/c

(c) Capital A/c

(d) Typewriter A/c

Ans: (d)

Q18: The accountant opens the following account when Trial Balance does not match

(a) Capital Account.

(b) Suspense Account.

(c) Drawings Account.

(d) Profit and Loss Account.

Ans: (b)

Q19: Which of the following is not an error of principle?

(a) Purchase of machinery debited to Purchase Account.

(b) Sale of old furniture credited to Sales Account.

(c) Repairs on the overhauling of existing Machinery debited to Machinery Account.

(d) Cash received from Mohan posted to Sohan.

Ans: (d)

Q20: Suspense Account in the trial balance will be entered in the :

(a) Manufacturing A/c

(b) Trading A/c

(c) Profit & Loss A/c

(d) Balance Sheet

Ans: (d)

Q21: Rent paid to landlord amounting to Rs.500 was credited to Rent A/c with Rs.5,000. In the rectifying entry, Rent A/c will be debited with :

(a) 5,000

(b) 500

(c) 5,500

(d) 4,500

Ans: (c)

Q22: Errors are

(a) Undetected mistakes

(b) Intentional Mistakes

(c) Frauds

(d) Unintentional Mistakes

Ans: (d)

Q23: Rs. 2,000 paid as wages for installing a machine should be debited to

(a) Wages Account.

(b) Machinery Account.

(c) Capital Account.

(d) None of these.

Ans: (b)

Q24: Purchased goods from Gopal for Rs.3,600 but was recorded in Gopal's A/c as Rs.6,300. In the rectifying entry, Gopal's A/c will be debited with :

(a) 9,900

(b) 2,700

(c) 3,600

(d) 6,300

Ans: (b)

Q25: Purchased goods from Gopal for Rs.3,600 but was recorded as Rs.6,300 to the debit of Gopal. In the rectifying entry, Gopal's A/c will be credited with :

(a) 9,900

(b) 2,700

(c) 3,600

(d) 6,300

Ans: (a)

Q26: Sohan returned goods to us amounting Rs.4,200 but was recorded as Rs.2,400 in his account. In the rectifying entry, Sohan's A/c will be credited with :

(a) 1,800

(b) 4,200

(c) 2,400

(d) 6,600

Ans: (a)

FAQs on Worksheet Solutions: Trial Balance and Rectification of Errors

| 1. What is a trial balance and why is it important in accounting? |  |

| 2. How is a trial balance prepared? | |

| 3. What are the types of errors that can be identified through a trial balance? | |

| 4. How can errors be rectified after preparing a trial balance? | |

| 5. What are the consequences of not rectifying errors in the trial balance? | |