Economic Development: June 2024 Current Affairs

Global Economic Prospects Report 2024

Why in news?

According to the recently released by the World Bank, India is predicted to remain the fastest-growing major economy globally, with a projected GDP growth rate of 6.6% for FY25.

Key Findings of the Report

- Global:

- Growth Outlook: The global economy is showing signs of stabilization in 2024, with anticipated GDP growth of 2.6% for 2024-25.

- Projection for Global Inflation: Global inflation is forecasted to average 3.5% this year.

- Challenges to Global Growth: Factors such as geopolitical tensions, trade fragmentation, higher interest rates, and climate-related disasters are impacting global growth.

- South Asian Region (SAR):

- South Asia's growth is projected to decrease to 6.2% in 2024, with India experiencing a slowdown from its recent high growth rates.

- Poverty Reduction: Per capita income growth in the South Asian region is expected to decrease to 5.1% in 2024-25.

- India:

- India's growth rate for FY24 is estimated at 8.2%, driven by the industrial and services sectors.

- Fiscal and Trade Balances: India's fiscal deficit relative to GDP is projected to decrease, with narrowing trade deficits contributing to economic stability.

Associated Risks to the Global Economy

- Proliferation of Armed Conflicts and Geopolitical Tensions

- Further Trade Fragmentation and Trade Policy Uncertainty

- Higher Interest Rates and Weaker Risk Appetite

- Weaker-than-expected Growth in China

- More Frequent Natural Disasters with Worsening Impacts

Key Policy Challenges

- Elevated Debt

- Climate Change

- Digital Divide

- Trade Fragmentation

Conclusion

The World Bank's latest report presents a cautiously optimistic outlook for the global economy in 2024. Continued global cooperation and effective policy measures are vital for sustainable economic growth.

Sticky Inflation and RBI's Monetary Policy

Why in news?

The Reserve Bank of India (RBI) in its latest bi-monthly monetary policy review opted to maintain the repo rate unchanged for the 8 consecutive time, amid discussions on inflation targeting and economic growth.

Why is the RBI not Cutting Interest Rates?

- Persistent Inflation:

- Despite high repo rates, inflation hasn't hit the 4% mark since early 2021.

- The decline has been gradual, with inflation hovering around 5% in the first four months of 2024. The RBI is concerned about "sticky" inflation trends.

- Durable Inflation Control:

- The RBI aims for sustained control, not a temporary dip below 4%. RBI Governor emphasizes commitment to achieving the 4% target "on a durable basis".

- Strong GDP Growth:

- India's Gross Domestic Product (GDP) growth has been surprisingly strong, exceeding 7% for four consecutive years. The RBI recently revised the current financial year's GDP forecast upwards to 7.2%. In this scenario, repo rates likely aren't hindering economic growth.

- Upcoming Union Budget:

- The RBI might be considering the upcoming Union budget, which could impact inflation dynamics and monetary strategies.

What is RBI's Inflation Targeting?

- About:

- RBI's Inflation Targeting is a monetary policy framework implemented to maintain price stability in the economy.

- The RBI targets a specific inflation rate, currently set at 4% per year.

- This target is a long-term average and not a rigid ceiling or floor.

- The target is accompanied by a tolerance band of +/- 2 percentage points.

- Goal:

- The main aim of inflation targeting is to achieve and maintain price stability, promoting economic growth, protecting the value of the rupee, and ensuring fair resource allocation in the economy.

- Mechanism:

- The RBI uses monetary policy tools, primarily the repo rate, to influence inflation.

- By raising the repo rate, the RBI makes borrowing more expensive, which discourages spending and investment, ultimately slowing down inflation.

- Conversely, lowering the repo rate encourages borrowing and spending, boosting economic activity but potentially increasing inflationary pressures.

- Limitations:

- Inflation targeting may not effectively address supply-side shocks or structural constraints like inadequate infrastructure, thus leading to higher inflation.

- It can also cause exchange rate volatility in open economies and have social and economic impacts on vulnerable populations.

- Additionally, accurate and timely data on inflation and other macroeconomic variables may not be available in all countries, including India.

What is Sticky Inflation?

- Sticky inflation refers to a persistent economic phenomenon where prices for goods and services do not adjust quickly to changes in supply and demand dynamics.

- Features of Sticky Inflation:

- Prices remain high despite fluctuations in supply and demand. Certain sectors like medical services, education, and housing are particularly prone to sticky inflation.

- Erodes purchasing power and affordability, especially in essential goods and services.

- Poses difficulties for central banks in controlling inflation without causing adverse economic impacts.

- Causes of Sticky Inflation:

- Prices may not respond immediately to changes in market conditions due to factors like rigid pricing mechanisms.

- Rising wages can lead to higher costs for businesses, contributing to inflation stickiness.

- Unique characteristics of sectors such as healthcare and housing contribute to persistent inflationary pressures.

- Managing Sticky Inflation:

- Central banks often raise interest rates to curb inflation, though balancing rate adjustments is critical to avoiding economic downturns.

- Targeted policies addressing specific sectors experiencing inflation stickiness can help mitigate its impact.

- Regular assessment and adjustment of economic forecasts and policies are crucial to managing sticky inflation effectively.

Disbursal of Duty Drawback by PFMS

Why in news?

Recently, the Central Board of Indirect Taxes and Customs (CBIC) has decided to electronically transfer duty drawback funds via the Public Finance Management System (PFMS), directly to exporters' bank accounts to ensure transparency and efficiency.

What is Duty Drawback?

Duty drawback under section 75 of the Customs Act, 1962 rebates customs duty chargeable on any imported materials or excisable materials used in the manufacture of export goods. This system helps exporters mitigate some of the costs incurred during the export process, particularly within the supply or value chain.

What is the Significance of Electronic Disbursal of Duty Drawbacks?

- Streamlining the Process: Electronic transfer has been introduced to streamline the process, reduce processing time, eliminate manual intervention, and enhance transparency in customs operations.

- Less Paperwork: It eliminates the need for physical documentation and manual processing, reducing the time and effort required to claim the refund.

- Promotes Transparency: The electronic system enhances transparency by providing exporters with real-time visibility into their claims' status and enabling seamless refund process tracking.

- Trade Facilitation: This initiative aligns with CBIC's commitment to paperless customs and trade facilitation, building upon its implementation of the World Trade Organization's, Trade Facilitation Agreement (TFA).

Coal and Thermal Power Plants in India

Why in News?Recently, According to the data on NITI Aayog's energy dashboard, India's coal-fired thermal capacity grew to 218 GW in FY24 from 205 GW in FY20, a 6% growth. A recent report alleges that in 2014, a company misrepresented low-grade Indonesian coal as high-quality, and sold it to a public power generation company in Tamil Nadu.

What is the Current Status of India's Power Sector?

Background: The power market is experiencing a growing demand-supply mismatch due to a slowdown in new coal-fired power plant capacity and a lack of effective storage options for renewable energy. This has put pressure on the country's grid managers, especially with increasing power demand during soaring temperatures.

Thermal Power Plants:

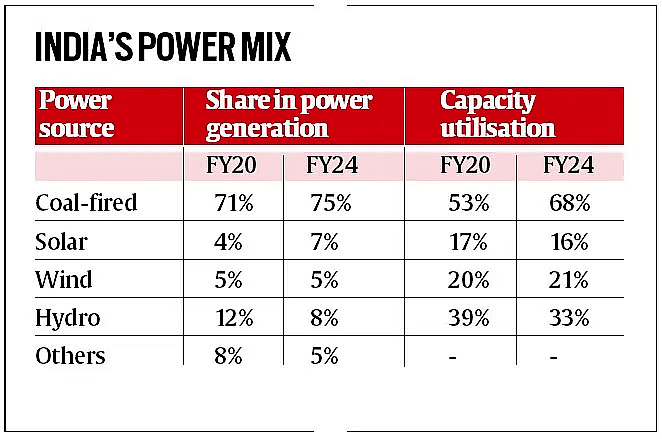

- The share of coal-fired power generation risen to 75% in FY2023-24 from 71% in FY2019-20.

- Generation by coal-fired thermal plants also increased by 34% from 960 billion units (BU) to 1,290 BU, and the average plant load factor (PLF) rose from 53% to 68%.

- In the past five years, thermal capacity addition has fallen short of the government's targets by an average of 54% annually with the private sector only contributing 7% of new capacity.

- The private sector has contributed only 1.7 GW, or 7% of the total thermal capacity added in the last five years.

Renewable Energy:

- Solar capacity has seen a significant surge, doubling to 81 GW.

- Wind power capacity has also witnessed impressive growth, increasing by 22% to reach 46 GW.

- Setting up a new coal plant (Rs 8.34 crore per MW) is considerably more expensive compared to setting up a solar power plant.

What Grade of Coal does India Produce?

Coal is a mixture of carbon, ash, moisture, and other impurities. The most important uses of coal are in thermal power plants and in powering blast furnaces for steel production, each requiring different kinds of coal.

Coking vs. Non-Coking Coal:

- Coking coal is needed for producing coke, an essential component of steel making, and requires minimal ash content.

- Non-coking coal can still be used to generate useful heat for running boilers and turbines despite its ash content.

Characteristics of Indian coal:

- Indian coal historically has high ash content and low calorific value compared to imported coal.

- Domestic thermal coal has an average GCV of 3,500-4,000 kcal/kg, while imported thermal coals have over 6,000 kcal/kg.

- Indian coals also have over 40% ash content, while imported coal has less than 10%.

What are the Technologies to Reduce Emissions from Thermal Power Plants?

- Flue Gas Desulfurization (FGD): FGD systems scrub flue gas with methods like wet or dry scrubbing process that absorbs SO2, removing it from the emissions before they are released into the atmosphere. This technology targets sulfur dioxide (SO2), a major air pollutant linked to respiratory problems.

- Selective Catalytic Reduction (SCR): SCR systems tackle nitrogen oxides (NOx), another group of pollutants contributing to smog and acid rain. During the SCR process, hot flue gas passes through a catalyst coated with precious metals like platinum. This triggers a chemical reaction that converts harmful NOx into harmless nitrogen gas and water vapor.

- Electrostatic Precipitators (ESPs): It targets particulate matter (PM), tiny particles linked to respiratory illnesses. ESPs use high voltage electricity to charge particles in the flue gas. These charged particles then stick to collector plates, which are periodically cleaned.

- Fabric Filters (Baghouses): Similar to ESPs, baghouses capture particulate matter. They may be used in conjunction with ESPs or as a standalone technology. Flue gas passes through a fabric filter bag, trapping PM on the fabric's surface. The bags are periodically shaken to release the collected particles.

- Coal Washing: Pre-combustion technology aims to reduce emissions by improving coal quality. Coal is washed with water to remove impurities like ash and sulfur, which can contribute to air pollution when burned.

- Co-firing with Biomass: This approach involves co-burning biomass along with coal. The revised Biomass Policy of 2023 mandates 5% biomass co-firing in thermal power plants from FY 2024-25.

What are the Existing Challenges and Government Initiatives in Thermal Power Sector?

Challenges:

- Rising electricity demand is outpacing the addition of new capacity of thermal power plant, particularly from renewable sources due to their unreliable nature.

- Coal remains the dominant source of power generation, despite its environmental impact and rising costs.

- Private sector is hesitant to invest in new coal plants due to financial and environmental concerns.

- Domestic coal has lower calorific value and higher ash content compared to imported coal, leading to higher emissions.

Government Initiatives:

- UDAY (Ujwal Discom Assurance Yojana)

- PM-KUSUM

- Green Energy Corridor (GEC)

- National Smart Grid Mission (NSGM) and Smart Meter National Programme

- International Solar Alliance (ISA)

- Sovereign Green Bonds for Solar Sector

Way Forward

- Accelerating the growth of solar and wind power, with a focus on grid integration solutions like large-scale battery storage.

- Implementation of technologies like to reduce emissions from existing coal plants.

- Offering financial and regulatory incentives for private companies to invest in cleaner and more efficient power generation technologies.

- Promoting energy efficiency measures to reduce overall demand and lessen the pressure on the grid.

- Modernising the grid infrastructure to handle the integration of variable renewable energy sources and improve overall efficiency.

- Exploring alternative sources like clean coal gasification, gravity battery, harnessing ocean energy, and nuclear power (with strict safety protocols) to meet energy needs.

Conclusion

India's power sector transformation requires a well-defined roadmap that balances immediate energy needs with long-term sustainability goals. By focusing on renewables, clean coal technologies, and energy efficiency, India can ensure a reliable and sustainable power supply for its growing economy.

Fintechs Leading India's Start-up Ecosystem

Why in News?

Fintech Companies continue to be an attractive option for entrepreneurs in the Start-Up ecosystem. As per the data from Tracxn (a company that provides market intelligence data for private companies), fintechs have received over 15% of the total equity funding into start-ups in FY24 so far.

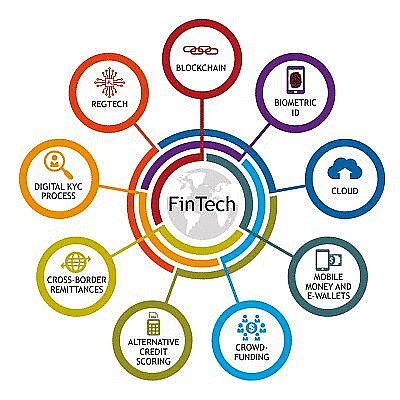

What are Fintechs?

- About: Fintech, a combination of the terms "financial" and "technology," refers to businesses that use technology to enhance or automate financial services and processes.

- Types:

- Digital Payments: These offer digital payment solutions, such as mobile wallets, online payment gateways, and peer-to-peer (P2P) payments. Ex-Phonepe, Paytm etc.

- Alternative Lending: They are also known as marketplace lending (Peer-2-Peer P2P lending), occurring on online platforms that connect borrowers overlooked by traditional lenders with investors looking for high-yield investments. Ex: Lending Club, Prosper, PayPal Working Capital, GoFundMe etc.

- Insurance: These offer digital insurance solutions, such as health insurance, life insurance, and car insurance. Ex-Digit Insurance, Policybazaar etc.

- InvestmentTech: These offer digital investment solutions, such as stock trading, mutual funds, and cryptocurrency trading. Ex-Zerodha, Groww etc.

- Others types include: Crop loan risk management (Eg: Satsure), online fraud detection (e.g. Tutelar), debt management (Debt Nirvana) and Banking-as-a-Service Platform (e.g., FidPay)

What is the State of Fintech Industry in India?

- FinTech Ecosystem: India remains a global leader in fintech, 3rd highest globally after the US and UK, having a combined valuation of over USD 155 billion. Nearly a third of the soonicorn universe (soon to be unicorns) comprises fintechs. Startup India, an initiative by the Ministry of Commerce and Industry, the market size of India's fintech industry is expected to reach USD 150 billion by 2025.

- High Adoption Rate: Economic Survey 2022-23, fintech companies in India witnessed an 87% adoption rate across varied user bases as opposed to the global average rate of 64%.

- Driving Digital Payments: Fintech companies in India account for 70% of digital payment transactions, marking a two-fold rise in their share during FY22 compared to FY19.

- Financial Inclusion: More than 10 million people and small businesses gained access to savings accounts, insurance, investment options, and credit facilities through mobile-based services and digital platforms.

- Democratising Lending Process: Peer-to-peer lending platforms are democratising lending, providing individuals and small businesses with access to funds without the need for traditional financial institutions.

- Rise in Public Investment: Investment platforms and robo-advisors are making investments in stocks, mutual funds, and other financial instruments more accessible.

What are the Government Initiatives Driving the Growth of FinTech?

- Digital Identity Infrastructure (JAM Trinity):

- Jan Dhan Yojana (PMJDY): This world's largest financial inclusion program has provided bank accounts to over 450 million people creating a massive base for FinTech companies to offer new financial products and services like remittances, credit, insurance, and pensions directly through these accounts.

- Aadhaar: According to a World Bank study, Aadhaar has facilitated bank account opening for over 570 million previously unbanked adults in India.

- Aadhaar Enabled Payment System (AePS): AePS has allowed Aadhaar card holders to conduct financial transactions using their Aadhaar number and biometric authentication (fingerprint or iris scan).

- Unified Payments Interface (UPI): UPI transaction volume has surged by 49% year-on-year. More banks are embracing UPI, with the number of integrated banks increasing from 414 in April 2023 to 581 in April 2024. This wider availability is fueling the overall growth in UPI transactions.

- Regulatory Support and Innovation:

- Peer-to-Peer (P2P) lending: In 2017, the RBI granted recognition to Peer-to-Peer lending platforms as Non-Banking Financial Companies (NBFCs) providing legitimacy and facilitated growth within the P2P lending segment, expanding credit access for individuals and small businesses.

- Regulatory Sandbox (RS) and Fintech Repository: RS is an infrastructure that helps Fintech players to live test their products or solutions, before getting the necessary regulatory approvals for a mass launch, saving start-ups time and cost. The RBI established a Regulatory Sandbox in 2017. Additionally, the launched in 2021 serves as a centralised information hub for fintech companies, promoting transparency and streamlining regulatory compliance.

- Self-Regulatory Organisations (SRO) Framework: To promote responsible growth, and recognizing the need for industry-led self-regulation, the introduced a framework for Self-Regulatory Organizations (SROs) in the FinTech sector in 2023. These SROs act like guardians within the industry, establishing and enforcing a code of conduct, grievance redressal mechanisms, and consumer protection standards.

What are Potential Growth Areas for the Fintech Sector in India?

- SME Lending: Small and medium enterprises (SMEs) often face challenges accessing traditional credit channels. Fintech solutions leveraging alternative data sources and AI-powered credit scoring can streamline lending processes and make credit more accessible for SMEs.

- Supply Chain Financing: Traditional supply chain financing methods are often cumbersome and lack transparency. Blockchain-based fintech solutions can streamline payments, improve traceability, and enhance working capital management for businesses within the supply chain.

- Agritech: Solutions for crop loan risk management, micro-insurance for farmers, and digital marketplaces for agricultural products can provide much-needed support and empower rural communities.

- Regulatory Landscape and Long-Term Stability: The RBI's framework for managing "user harm" within the fintech sector, while potentially creating a cautious investment climate in the short term, is a positive development in the long run. Clear and well-defined regulations will enhance consumer protection and build trust in the ecosystem, attracting long-term investors and fostering sustainable growth.

National Health Claim Exchange (NHCX): Revolutionizing Health Insurance in India

Why in news?

Revolutionizing the health insurance landscape in India, the National Health Claim Exchange (NHCX) has emerged as a pivotal initiative.

Current Claim Processing

- Patients typically furnish insurance details or a Third-Party Administrator (TPA) card at healthcare facilities.

- For PMJAY beneficiaries, State Health Agencies (SHAs) issue cards.

- Hospitals utilize specific portals to submit documents for claims or preauthorization.

- Adjudication of claims is manual in India, contrasting with automated processes in developed nations.

Challenges of the Current Process

- Existing claim procedures lack uniformity and rely heavily on manual exchanges.

- Data sharing predominantly involves PDFs or manual methods.

- Health standards remain undefined, leading to operational discrepancies.

- Varying processes among insurers, TPAs, and providers complicate the system.

About

- The Health Claim Exchange Specification serves as a communication protocol for sharing health claim information.

- Designed to be interoperable and verifiable, it aims to ensure trustworthy data exchange.

- Based on open standards, it aligns with IRDAI's 'Insurance for All by 2047' vision.

- Facilitates secure, paperless interactions between hospitals and insurers.

Expected Working

- NHCX will streamline the exchange of health claim data among healthcare stakeholders.

- Enhancing interoperability, it promises efficient claims processing and transparency.

- Centralizing claims will reduce administrative burdens on hospitals.

- Integration completed by twelve insurers and a TPA.

Incentives under NHCX

- The Digital Health Incentive Scheme offers hospitals financial rewards for digital health transactions.

- These incentives aim to encourage the digitization of patient health records.

- Hospitals receive a fixed sum per claim transaction or a percentage of the claim amount under DHIS.

- Promotes digital healthcare services and supports the ABDM.

Findings of a Study

- A study underscores the importance of health insurance in curbing out-of-pocket expenses.

- Hospitalization rates are highest for privately insured individuals.

- Differences exist in healthcare utilization between urban and rural areas.

- Urban settings witness higher in-patient cases compared to rural areas.

Benefits of NHCX

- Standardization and Interoperability

- Efficient Claims Processing

- Standardized Healthcare Pricing

- Reduction in Claims Processing Costs

- Enhancing Hospital-Insurer Relationships

- Addressing Issues

- Building Trust

Authorised Economic Operator (AEO) Programme

Why in news?

The Centre has extended Authorised Economic Operator (AEO) status to the gem and jewellery sector.

Overview:

- An Authorised Economic Operator (AEO) is a business entity involved in the international movement of goods and complies with national customs laws. It is approved by or on behalf of the World Customs Organization (WCO).

- The WCO, in June 2005, adopted the SAFE Framework of Standards (WCO SAFE FoS) to secure the international supply chain, with AEO being one of its three pillars.

- The AEO programme aims to foster a closer partnership between customs departments and the trade industry, forming the basis of the Indian AEO programme.

What is the AEO programme?

- Introduced in India by the Central Board of Indirect Taxes and Customs (CBIC) in 2011, the AEO programme is a voluntary initiative aiming to provide benefits such as simplified customs procedures and faster clearances to businesses offering high security guarantees in the supply chain.

- Entities with AEO status are considered reliable and secure trading partners, allowing customs resources to focus on potentially high-risk businesses for control.

Benefits:

- Direct port delivery and entry, especially for small and medium-scale entities.

- Fast disbursal of refunds, drawback amounts, and adjudications.

- Streamlined processes like paperless declarations and site inspections upon request.

- Recognition by partner government agencies and stakeholders.

Who can apply for AEO Status?

- Business entities involved in international supply chains undertaking customs-related activities in India can apply, regardless of size. Examples include importers, exporters, Custom House Agents (CHA), and Custodians or Terminal Operators.

Key Facts about World Customs Organization (WCO):

- The WCO, established in 1952, is an intergovernmental body focusing on enhancing customs administrations' effectiveness and efficiency.

- It represents 186 customs administrations worldwide, overseeing a significant portion of global trade processes.

- WCO's work includes the development of global standards, customs procedure simplification, trade chain security, facilitation of international trade, and customs enforcement activities.

- It administers technical aspects of WTO Agreements on Customs Valuation and Rules of Origin while maintaining the international Harmonized System goods nomenclature.

Aspirational Goals of RBI

Why in news?

Recently, the Reserve Bank of India (RBI) has outlined several aspirational goals in preparation for India's fast-growing economy, aiming to be "future-ready" by the time it reaches its centenary year, RBI@100.

What are the Aspirational Goals of RBI?

Capital Account Liberalisation and INR Internationalisation:- Capital Account Convertibility: Proposed full capital account convertibility, allowing free conversion between the rupee and foreign currencies for capital transactions.

- Internationalisation of the Rupee: Enabling non-residents to use the rupee for cross-border transactions and enhancing rupee account accessibility for persons outside India.

- Calibrated Interest-Bearing Non-Resident Deposits: Adopting a careful approach toward interest-bearing deposits for non-residents.

- Promotion of Indian MNCs and Global Brands: Supporting overseas investments by Indian multinational corporations.

Digital Payment System Universalisation:

- Domestic and Global Expansion: Expanding the use of India's digital payment systems (UPI, RTGS, NEFT) domestically and internationally, and linking payment systems with other countries.

- Central Bank Digital Currency (e-Rupee): Phased implementation of the e-Rupee.

Globalisation of India's Financial Sector:

- Domestic Banking Expansion: Aligning banking sector growth with national economic growth.

- Top Global Banks: Aiming to position 3-5 Indian banks among the top 100 global banks in terms of size and operations and positioning the Reserve Bank as a model central bank of the global south.

- Support for GIFT City: Assisting the International Financial Services Centres Authority (IFSCA) in making a leading international financial hub.

Monetary Policy Framework Review:

- Balancing Act: Addressing the balance between price stability and economic growth from an Emerging Market Economy perspective.

- Policy Communication: Refining monetary policy communication and addressing spillovers from debt overhang in important economies.

Climate Change Initiatives:

- Providing guidance for stress testing asset portfolios, strengthening payment systems against climate risks, and proposing disclosure norms and a government taxonomy for Short and Medium-Term Measures.

What are the Challenges in Achieving the Aspirational Goals of RBI?

- Triffin Dilemma: It describes the conflict between a country's domestic monetary policy goals and its role as an international reserve currency issuer.

- Exchange Rate Volatility: Opening up the currency to international markets can increase volatility in its exchange rate, especially in the initial stages.

- Impact on Export: The Rupee's internationalisation will lead to increased demand for the currency in global markets, which may make Indian exports costly.

- Limited International Demand: The daily average share for the rupee in the global forex market is only around 1.6%, while India's share of global goods trade is ~2%.

- Convertibility Concern: The absence of full convertibility of INR for capital transactions will restrict its widespread use in international trade and finance.

- Cybersecurity Threats: Digital payment systems are vulnerable to cyberattacks.

- High Non-Performing Assets (NPAs): Indian banks, particularly public sector ones, struggle with a high percentage of non-performing assets.

What are the Steps Needed to Reach the Aspirational Goals?

- Convertible of Rupee: As per the recommendation of Tarapore committee, the goal should be of full convertibility by 2060, letting financial investments move freely between India and abroad.

- Tobin Tax: A safeguard measure by RBI against currency speculation.

- Reforms Suggested by Tarapore Committee: Listed preconditions for achieving capital account liberalisation.

- Strong Fiscal Management: Including reducing fiscal deficits, inflation rates, and non-performing assets.

- Liberalised Scheme for Personal Remittance: Facilitating easier transactions for individuals dealing with foreign exchange.

- Pursue a Deeper Bond Market: Enabling more investment options in rupees.

- Increase Rupee in International Trade: Optimising trade settlement formalities for rupee import/export transactions.

- Encourage domestic banking expansion: Through licensing reforms and branch network expansion.

- Conduct a comprehensive review of the monetary policy framework: To ensure alignment with price stability and economic growth goals.

- Enhance transparency and clarity in monetary policy communication: Managing market expectations effectively.

- Issue guidelines for stress testing of asset portfolios: Assessing climate change risks.

UN Report on Global Debt Crisis

Why in News?

Recently, a report released by the UN Trade and Development (UNCTAD) titled "A World of Debt 2024: A Growing Burden to Global Prosperity," has revealed an unprecedented global debt crisis in the world. Approximately 3.3 billion people currently live in countries where the payment of interest on debts surpasses the expenditure on either education or health.

Key Highlights of the Report

Rapid Increase in Public Debt:

- Institute of International Finance (a global association of financial institutions) has estimated that global debt (including borrowings of households, businesses, and governments) has reached USD 315 trillion in 2024, which is 3 times the global Gross Domestic Product (GDP).

- Global public debt is rising rapidly, due to a combination of recent crises (such as Covid-19, rising food and energy prices, climate change, etc.) and a sluggish global economy (slowing growth of the economy, rising bank interest rates, etc).

- Net interest payments on public debt USD 847 billion in 2023 in developing countries, a 26% increase compared to 2021.

Regional Disparity in Debt Growth:

- Public debt in developing countries is rising at twice the rate of that in developed countries.

- It reached USD 29 trillion (30% of the global total) in 2023, increasing from 16% in 2010.

- Africa's debt burden is growing faster than its economy leading to a rise in the debt-to-GDP ratio.

- The number of African countries with debt-to-GDP ratios above 60% has increased from 6 to 27 between 2013 and 2023.

Higher Debt Servicing Share of Income & Impact on Climate Initiatives:

- Roughly 50% of developing countries are now dedicating a minimum of 8% of their government revenues to servicing their debts, a number that has increased twofold in the last ten years.

- Currently, developing nations are spending a greater portion of their GDP on paying off interest (2.4%) than on climate efforts (2.1%).

- Their ability to address climate change is being constrained by debt. In order to meet the targets of the Paris Agreement, there is a requirement to raise climate investments to 6.9% by 2030.

3 Shifts in Official Development Assistance (ODA):

- ODA is government aid aimed at promoting economic development and welfare in developing countries.

- Repaying loans has become more difficult for developing countries, due to recent changes made in the nature of foreign aid such as decreasing overall aid, more loans and less grants, and less help with existing debt.

Initiatives Related to Solving Debt Crisis

Heavily Indebted Poor Countries (HIPC) Initiative:

- IMF World Bank's initiative tackles debt crises in the world's poorest countries. It recognizes their struggle to repay debts without sacrificing crucial investments. By offering debt relief, the program frees up resources, allowing these nations to invest in healthcare, education, and poverty reduction, promoting long-term economic growth and social progress.

Debt Management and Financial Analysis System (DMFAS) Programme:

- UNCTAD's DMFAS program helps developing countries manage debt responsibly. It provides training and technical support to improve their borrowing practices, including tools for recording debt, assessing risks, and negotiating effectively. This program promotes sustainable debt management so these countries can borrow for development without creating future crises.

Global Sovereign Debt Roundtable (GSDR):

- The roundtable is co-chaired by the IMF, World Bank, and G20 presidency, which aims to address debt challenges comprehensively. It brings together debtor countries and creditors with the objective of fostering a greater common understanding among key stakeholders on issues related to debt sustainability, debt restructuring challenges, and potential solutions.

Measures to Address the Global Debt Crisis

Inclusive Governance, Transparency, and Accountability:

- World Bank's 2022 International Debt Statistics report highlights a concerning rise in public debt, particularly for low-income countries, thus increased participation for these nations in decision-making processes is essential. UN Office for Sustainable Development emphasizes that financial transparency and accountability are crucial for preventing debt crises.

Contingency Financing:

- Performs a vital role in providing emergency financial support. A 2019 IMF Report titled "Three Steps to Avert a Debt Crisis" proposed measures like increased access to Special Drawing Rights (SDRs) to bolster developing countries' reserves during emergencies.

Managing Unsustainable Debt (Managing Debt Challenges):

- Existing frameworks for debt restructuring, such as the G20 Common Framework for Debt Treatment, should be improved. In addition, including automatic provisions for suspending debt payments for countries facing crises would offer essential flexibility to help them stabilize their economies.

Scaling up Sustainable Financing:

- Multilateral Development Banks (MDBs) need to be transformed to play a more prominent role in long-term financing for Sustainable Development Goals (SDGs). Attracting private investment towards sustainable projects like clean energy is also crucial. Fulfilling existing commitments for aid and climate finance, particularly for developing countries, is essential for facilitating this transition.

Household Consumption Expenditure Survey 2022-23

Why in news?

Recently, National Sample Survey Office (NSSO) under the Ministry of Statistics and Programme Implementation released the Household Consumer Expenditure Survey (HCES) conducted from August 2022 to July 2023.

Key Highlights On Household Consumption Expenditure Survey 2022-23

- The survey results show Indian household consumption and patterns, breaking 11-year data since the last exercise was conducted in 2011-12.

- Field work for the second year of HCES 2022-24 has been initiated from August 2023.

Aim

- To generate estimates of household Monthly Per Capita Consumption Expenditure (MPCE) and its distribution separately for the rural and urban sectors of the country, for states and Union Territories, and different socio-economic groups.

Why the Delay in the Survey?

- The survey is supposed to be held every five years. However, the latest iteration comes more than a decade after the previous one after the government controversially junked 2017-18 survey, citing data quality issues.

- The government said there was a significant variation in the levels of consumption patterns and in the direction of change.

Monthly Per Capita Consumption Expenditure (MPCE)

- It is defined as household consumer expenditure over a period of 30 days divided by the household size.

- Poverty line is defined on the basis of MPCE.

Crucial Insights From Household Consumption Expenditure Survey 2022-23

- Growth in Consumption Expenditure: The per capita monthly household expenditure in 2022-23 compared to 2011-12.

- The Average Per Capita Monthly household Expenditure: It stood at Rs 3,773 in rural areas and Rs 6,459 in urban areas for all categories.

- Narrowing the Urban-Rural Gap: Consumption in rural areas is growing faster than in urban areas, narrowing the gap.

- Significant Fall in the Consumption of Cereals and Food: In Rural Areas: cereals as a share in the average MPCE has decreased.

- Increase in the Expenditure on High-value Items: Expenditure on high-value items such as eggs, fish, meat, fruits, and vegetables has increased.

- Increase in the Expenditure on Non-food Items: The expenditure on non-food items has increased across all categories, with the highest expenditure on transport and communication.

- Increase in the Expenditure on Education and Health: Expenditure on education and health has shown an upward trend.

- Gap Narrowing in the Agriculture Sector: The gap between the MPCE of agricultural families and the overall average of rural households has been narrowing over the years.

State on Top and Bottom

- The MPCE is the highest in Sikkim for both rural and urban areas, and it is the lowest in Chhattisgarh.

- The rural-urban difference in average MPCE is highest in Meghalaya followed by Chhattisgarh.

On Imputed Average MPCE Data

- The data provides an imputed value of items received free by households through various social welfare programmes.

- A fractile class of MPCE is the segment of the population lying within two fractiles.

About Household Consumer Expenditure Survey (CES)

- It is a Survey intended to collect information on the consumer spending patterns of households across the country, both urban and rural.

- Frequency of Survey: Quinquennial (every five years)

- Utility of the Survey: The data is used for studies on levels of living in India and for the measurement of absolute poverty.

- New Changes in the Methodology of Survey: The Questionnaire of HCES 2022-23 contains additional items compared to previous surveys.

About National Sample Survey Office (NSSO)

- The NSSO is responsible for conducting large-scale sample surveys in diverse fields on an All India basis.

- Positive Outcomes Household Consumption Expenditure Survey 2022-23

- Cautiousness For Health & Well-being: An increase in the expenditure on high-value items shows that Indian households are consuming nutritious and diverse diets.

- Significance of Conducting the Household Consumption Expenditure Survey 2022-23

- Helps in Assessment For Policy-Makers: The data is essential for updating the, giving policymakers and experts an assessment on the income and expenditure levels of households.

Arising Concerns

- Decline in Value of Self-Employment in Agriculture: For the first time, self-employment in is lower than the rural household average.

- Fall in the Average MPCE of Agricultural Households: Compared to overall rural households, the average MPCE of agricultural households is decreased.

- Increase in Inequality at Higher Income Levels: The top 5% of India's rural and urban population has an average MPCE higher than the bottom 5%.

- Different Calculation for Welfare Programmes: The cited MPCE numbers do not include the imputed values of items received free of cost by individuals through various social welfare programmes.

Conclusion

The release of this survey marks an important step towards filling the data vacuum in the country. The next government should take this forward, initiate the much-delayed census exercise and take steps to strengthen the country's statistical system.

Financing of Large Infrastructure Projects

Why in News?

Recently, the Reserve Bank of India (RBI) has proposed a new framework to improve the regulation of financing for long-term projects in infrastructure, non-infrastructure, and commercial real estate sectors. This is in response to the challenges these projects often face, such as delays and cost overruns.

Key Provisions Proposed by RBI for Project Financing

Mitigating Credit Events:

- The framework prioritises preventing credit events such as loan defaults, extensions of the project's commercial operation start date (DCCO), additional debt requirements, or a decrease in the project's Net Present Value (NPV).

Increased Provisioning:

- To build a buffer against potential losses, the framework proposes a significant increase in provisioning (setting aside funds) by banks. The provisioning is raised from the existing 0.4% to 5% of the loan amount during the construction stage (before the project launch).

- The 5% provisioning will be implemented gradually with 2% in FY25, 3.5% in FY26, and reaching 5% by FY27. The additional provisioning requirements are estimated to be 0.5-3% of banks' net worth and could impact the CET1 (Common Equity Tier 1) ratio.

Reduced Provisioning During Operations:

- If a project demonstrates a positive net operating cash flow (enough income to cover repayments) and reduces its total debt by 20% after starting commercial operations, provisioning can be lowered.

Potential Impacts of the Proposed Framework

Impact on banks:

- Higher provisioning requirements could impact bank profitability in the short term. Additionally, loan pricing might increase slightly to reflect the perceived higher risk. State-owned banks are cautiously optimistic, suggesting the impact on pricing might be moderate.

Impact on borrowers:

- Borrowers might face stricter financing terms and potentially higher interest rates. However, the framework aims to improve project viability and reduce overall risk in the long run. Rating agencies predict a potential rise in funding costs by 20-40 basis points.

Financing Issues Faced by the Large Infrastructure Projects in India

Fiscal Burden on Government:

- Traditionally, the government has been the primary source of funding for infrastructure projects, leading to fiscal deficits. This limits spending on other social programs like education and healthcare. In 2022, the government's infrastructure spending was around 3.3% of GDP, a positive step but still below the desired level.

Asset-Liability Mismatch of Commercial Banks:

- Commercial banks, a key source of infrastructure financing, prioritise short-term loans with quicker returns. Long-term infrastructure projects with slow returns become less attractive. Many infrastructure projects experience delays and cost overruns, leading to financial stress for banks that provide loans, discouraging further lending for large projects.

Subdued Investments in Public-Private Partnerships (PPP) Projects:

- Private sector participation through PPPs hasn't met expectations due to uncertain regulatory environments, complex project structures, and land acquisition issues. A 2023 report by CARE Ratings, an Indian credit rating agency, states that private sector investment in infrastructure projects has been around 5% of the total requirement.

Inefficient and Underdeveloped Corporate Bond Market:

- India's corporate bond market, a potential source of long-term financing for infrastructure, is still relatively small and lacks liquidity. This makes it difficult for infrastructure companies to raise funds through bond issuance. In 2023, the size of India's corporate bond market was approximately USD 1.8 trillion, which is significant but still smaller compared to developed economies like the US at USD 51 trillion.

Investment Obligations of Insurance and Pension Funds:

- Regulations often require insurance and pension funds to invest a significant portion of their funds in government securities, limiting their ability to invest in riskier infrastructure projects that could offer higher returns. According to the World Bank, only around 2% of Indian pension funds' assets are invested in, compared to a global average of 5-10%.

Government Initiatives Related to Financing Large Infrastructure Projects in India

- National Infrastructure Pipeline (NIP)

- National Bank for Financing Infrastructure and Development (NaBFID)

- National Investment and Infrastructure Fund (NIIF)

- Infrastructure Investment Trusts (InvITs) and Real Estate Investment Trusts (REITs)

Public-Private Partnerships (PPP) Model Reforms:

- The government has undertaken measures like reducing legal complexities, simplifying the approval process, and streamlining dispute resolution processes. For example, the Ministry of Finance has established a dedicated PPP cell to address the concerns of private investors and facilitate faster project clearances.

Sovereign Wealth Funds (SWFs):

- The Indian government is actively engaging with countries like UAE, Norway, etc., with large SWFs to facilitate their investment in the Indian market. SWFs can provide a stable source of long-term funding for infrastructure projects and help mitigate the risk burden on the government's budget.

Measures to Improve Financing of Large Infrastructure Projects in India

Enhancing Project Preparation and Risk Mitigation:

- Conducting extensive feasibility studies that accurately assess project viability, costs, and potential risks is crucial to attracting investors. Ensuring a fair and transparent risk allocation framework that balances the interests of both the public and private sectors.

Attract Private Sector Participation:

- The government can provide grants or subsidies to bridge the gap between project costs and what private investors are willing to pay (Viability Gap Funding), making projects more attractive.

Diversifying Funding Sources:

- Encouraging the creation of more to attract investments from pension funds, insurance companies, and other institutional investors. Creating a sovereign wealth fund in India to leverage the country's foreign exchange reserves for long-term infrastructure financing.

Streamline Approvals and Clearances:

- Streamlining land acquisition procedures to ensure timely availability of land for project development, a major bottleneck currently. Developing a more efficient system for environmental impact assessments and clearances, balancing environmental protection with project timelines.

Improve Project Execution and Efficiency:

- Encourage the use of new technologies like prefabrication and modular construction to improve project efficiency and reduce costs. Implementing stricter performance monitoring and accountability measures to ensure the timely completion of large projects and avoid cost overruns.

FAQs on Economic Development: June 2024 Current Affairs

| 1. What is the significance of sticky inflation and how does it impact RBI's monetary policy? |  |

| 2. How are coal and thermal power plants contributing to India's energy sector? | |

| 3. What role do fintechs play in leading India's start-up ecosystem? | |

| 4. What is the Authorized Economic Operator (AEO) Programme and how does it benefit businesses? | |

| 5. What are the aspirational goals of RBI and how are they working towards achieving them? | |