Mutual Funds & Pension Funds

What are Mutual Funds?

Mutual funds are pooled investment vehicles that collect money from many investors and invest it in a diversified portfolio of securities such as equities, debt instruments and money‐market instruments. Pooling enables individual investors to access professional fund management, portfolio diversification and economies of scale that would be difficult to achieve individually.

- Accessible to small investors: Mutual funds allow individuals to start investing with relatively small amounts.

- Professional management: Funds are managed by professional portfolio managers or asset management companies (AMCs) who select securities and manage the portfolio according to the fund's objective.

- Defined investment objectives: Each fund follows stated objectives (for example, capital appreciation, income or preservation of capital) and an investment policy.

- Wide asset choice: Fund managers may invest in equities, bonds, money market instruments and, in some schemes, other permitted assets according to the scheme document.

- Proportionate sharing of returns and losses: Investors share gains or losses in proportion to their holdings of fund units.

Features of Mutual Funds

Key features that make mutual funds a preferred route for many investors are:

- Convenience: Easy account opening, purchases and redemptions through online and offline channels; investors need not research each security themselves.

- Investment flexibility: Investors can invest lump sums or use systematic investment plans (SIPs) to contribute periodically.

- Liquidity: Open‐ended schemes permit buying and selling of units at prevailing Net Asset Value (NAV); redemptions are typically settled within a few working days.

- Charges: Mutual funds levy an expense ratio and other permissible fees to meet management and operational costs.

- Regulation: Fund houses must register with and operate under the supervision of the securities market regulator.

- Diversification: Portfolios spread investments across securities to reduce idiosyncratic risk.

Functions of Mutual Funds

Mutual funds perform several interrelated functions that benefit investors and markets:

- Investment collection and pooling: Collect savings from many investors and pool them for investment.

- Professional portfolio management: Use the expertise of fund managers and research teams to select and manage investments.

- Information and transparency: Provide periodic disclosures such as portfolio holdings and NAV, enabling investors to see how funds are invested.

- Risk management: Reduce risk by diversifying investments across multiple securities and asset classes.

- Facilitating market access: Enable retail investors to access a wide range of domestic and international securities through a single product.

Objectives of Mutual Funds

- Diversification: Reduce risk by holding a variety of securities across sectors and instruments.

- Income generation: Provide regular income through interest or dividend‐oriented schemes.

- Capital preservation: Offer lower‐risk options that prioritise protection of principal.

- Capital growth: Achieve long‐term appreciation through equity or growth‐oriented schemes.

- Encouraging savings and investments: Provide an easy, structured way for individuals to build a habit of saving and investing.

Structure of Mutual Funds

Mutual funds are offered in different structural forms. The principal types are:

- Open‐ended schemes: Allow investors to buy or redeem units directly from the fund at the NAV on any business day; the fund's capital varies as units are issued or redeemed.

- Close‐ended schemes: Have a fixed number of units and a specified maturity. Investors may buy units during the initial offer period; secondary market trading (if listed) provides liquidity thereafter.

- Interval schemes: Combine features of open‐ and close‐ended funds; they allow purchases and redemptions only during specified intervals.

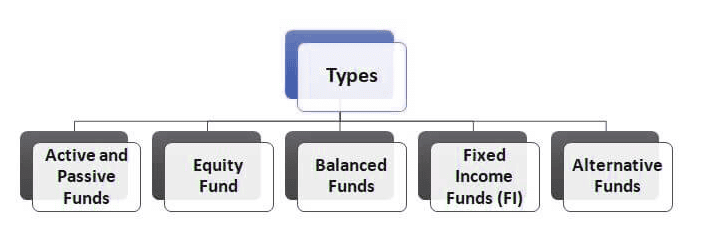

Types of Mutual Funds

Mutual funds are categorised by the asset classes they invest in and by strategy. Common categories include:

- Equity / Growth schemes: Invest predominantly in shares of companies; suitable for investors seeking capital appreciation and willing to accept higher volatility.

- Money Market / Liquid funds: Invest in short‐term debt and money‐market instruments; suitable for parking short‐term surplus with lower risk.

- Fixed Income / Debt funds: Invest primarily in bonds, government securities and other fixed‐income instruments; aim to provide regular income and relative stability.

- Balanced / Hybrid funds: Maintain a mix of equity and debt to balance growth and income objectives; risk and return lie between pure equity and pure debt funds.

How are Mutual Funds Priced?

Most mutual funds use Net Asset Value (NAV) to price their units. NAV represents the per‐unit market value of the fund on a particular day.

NAV formula:

NAV = (Market value of all securities + Cash and receivables - Liabilities) ÷ Number of units outstanding

- Daily valuation: NAV is usually calculated at the close of each business day to reflect changes in the value of underlying securities.

- NAV changes and returns: An increase or decrease in NAV reflects the fund's gains or losses and determines investor returns on disposals or redemptions.

- Calculation methods: Some funds may apply specific policies for pricing across days (for example, averaging prices) as per their scheme document and regulator guidelines.

Pros of Mutual Fund Investing

- Professional management: Benefit from the expertise of experienced fund managers and research teams.

- Reinvestment options: Dividends and interest can often be reinvested to compound returns.

- Diversification and safety: Spreading investments reduces the impact of failure by any single security.

- Convenience: One product gives exposure to a diversified portfolio without the need for direct security selection.

- Transparent pricing: Regular NAV disclosure helps investors to see the value of their holdings.

Cons of Mutual Fund Investing

- Costs and expense ratios: Management fees and operating expenses reduce net returns to investors.

- Manager risk: Performance depends on the skill and integrity of the fund manager.

- Tax considerations: Capital gains and dividend distributions have tax consequences which may affect net returns.

- No capital guarantee: Even low‐risk funds can incur losses; mutual funds generally do not provide guaranteed returns.

- Cash drag: Funds may hold cash to meet redemptions, which can reduce returns compared with fully invested portfolios.

Examples

- HDFC Equity Fund: An equity‐oriented scheme managed by HDFC AMC which primarily invests in shares.

- SBI Equity Hybrid Fund: A hybrid scheme investing in a mix of equities and debt instruments.

- HDFC Liquid Funds: Liquid/debt funds that invest in short‐term debt instruments to provide stability and liquidity.

Summary

Mutual funds offer a regulated, professionally managed route to invest in a diversified portfolio of securities. Different schemes cater to distinct investor objectives-growth, income, liquidity or capital preservation-and investors should choose schemes consistent with their risk tolerance, time horizon and financial goals.

Employees' Provident Fund Organization Pension Scheme

- Administering agency: The Employees' Provident Fund Organisation (EPFO) administers provident fund and pension schemes for organised sector employees under relevant statutes.

- Contributions: Employers and employees make monthly contributions. A portion of the overall EPF contributions is allocated towards the pension corpus under the Employees' Pension Scheme (EPS).

- Pensionable salary cap: For pension calculation purposes, a pensionable salary ceiling of Rs 15,000 per month is applied in the EPS (as per applicable rules and amendments at the time of contribution).

- Pension eligibility age: Members are typically eligible to receive a monthly pension on attaining 58 years of age.

- Early pension and survivor benefits: Early pension options may be available (for example from age 50 under specified conditions), and family/survivor pensions are provided in case of the member's death.

- Portability and identification: The scheme is Aadhaar‐linked and portable across employers, allowing continuity of pension benefits when changing jobs or locations.

- Coverage: The scheme covers employees engaged in establishments covered under the Employees' Provident Funds and Miscellaneous Provisions Act, 1952, across many industries-input sources reference coverage across more than 190 industries.

Pension Fund Regulatory and Development Authority (PFRDA)

The Pension Fund Regulatory and Development Authority (PFRDA) is the statutory regulator for pension funds established by the Government of India under the PFRDA Act (set up in 2003). Its mandate is to promote orderly growth, regulation and supervision of the pension sector and to protect the interests of subscribers.

Key functions of the PFRDA include

- Registration and regulation: Registering and regulating pension fund managers and intermediaries operating under the National Pension System (NPS).

- Overseeing intermediaries: Supervising entities such as the Central Recordkeeping Agency (CRA), Points of Presence (PoPs) and pension fund managers.

- Subscriber protection: Ensuring transparency, fair practices and compliance to protect subscriber interests.

- Promotion of pension coverage: Promoting pension awareness and extending retirement savings solutions, especially to underserved sections.

- Sectoral reforms and grievance redressal: Driving regulatory reforms and handling subscriber grievances and related data maintenance.

Section 80CCC: Pension Fund Contributions

Under the Income Tax framework, certain contributions to pension and annuity products may be eligible for tax deductions. Section 80CCC of the Income Tax Act permits deductions for contributions to specific pension/annuity plans, subject to conditions and limits prescribed by the tax law.

- Objective: Encourage retirement savings by providing tax benefits on contributions to eligible pension/annuity products.

- Limits: Deductions under Section 80CCC form part of the overall limit under Section 80C (aggregate ceiling as per prevailing tax law).

- Withdrawal and taxation: Tax treatment of withdrawals and annuity payouts is governed by the Income Tax Act and Finance Act rules in force at the time of withdrawal.

Pension Funds in India

A pension fund collects contributions from employees and employers, invests those funds to build a retirement corpus and pays a pension or lump sum at retirement. In India, key pension arrangements include the National Pension System (NPS) and statutory schemes administered through the EPFO.

National Pension System (NPS)

- Coverage: Open to central and state government employees (where adopted) and to private sector individuals and others through the NPS architecture.

- Contributions: Subscribers contribute regularly; employers may also contribute depending on the employment contract or organisational policy.

- Choice of investment: Subscribers can choose asset allocation among prescribed asset classes and select pension fund managers from those appointed by the regulator.

- Professional management: Funds are managed by regulated pension fund managers under PFRDA supervision.

Employees' Provident Fund (EPF)

- Applicability: A statutory provident fund scheme for organised sector employees administered by the EPFO.

- Contribution rates (typical): Inputs cite employee contribution at 12% of salary and employer contribution around 13.16% (employers' share is apportioned between EPF and EPS components as per scheme rules).

- Withdrawal and pension features: EPF balances can be partially withdrawn under prescribed conditions; the EPS provides pension benefits for eligible members.

Key features of the National Pension System (NPS)

- Cost‐effective and transparent: Low management costs relative to many pension alternatives and regulated transparency in operations.

- Flexible contributions: Subscribers can adjust contributions within scheme limits; rules govern minimum contributions and account activity.

- Investment choice: Multiple fund managers and asset classes allow tailoring of risk and return preferences.

- Retirement benefits: Options include annuity purchase and partial lump‐sum withdrawal at retirement subject to scheme rules.

Benefits of contributing to a pension fund

- Tax benefits: Contributions to eligible pension products may be eligible for income‐tax deductions under relevant sections of the Income Tax Act.

- Retirement income: A properly accumulated pension corpus can provide a regular income at retirement and supplement other savings.

- Professional management: Investments are handled by regulated fund managers aiming for optimal returns within the chosen risk profile.

Risks involved

- Market and investment risk: Pension funds that invest in market instruments face volatility and market risk which affects returns.

- Early exit penalties and lower returns: Exiting or withdrawing before maturity/retirement may attract lower returns or penalties.

Employees' Pension Scheme (EPS)

- Objective: Provide pension benefits to members of the EPF who satisfy eligibility and contributory service criteria.

- Eligibility and service criteria: Pensionable service is computed based on contributory years; typically a minimum period (for example, ten years) of contributory service is required to receive a monthly pension.

- Contributions: A portion of the employer's provident fund contribution is diverted to the EPS as per scheme rules.

- Pension calculation: Pension amount depends on factors such as pensionable service, average pensionable salary and the pensionable salary factor/formula prescribed under the scheme.

- Types of pension: Includes superannuation pension, early retirement pension, and family pension payable to dependants on the member's death.

- Withdrawal for short service: Members with less than required service who do not qualify for a monthly pension may withdraw the accumulated amount subject to rules.

- Nomination facility: Members can nominate family members to receive benefits in the event of the member's death.

- Government subsidy and amendments: The EPS has received periodic amendments and may be supported by government provisions; members and employers should keep abreast of legislative changes that affect benefits.

Conclusion

Pension funds and mutual funds are distinct yet complementary financial instruments. Mutual funds provide pooled investment across asset classes to meet various investment objectives such as growth, income and liquidity. Pension funds are long‐term retirement vehicles that collect contributions, invest professionally and deliver retirement income. Both require understanding of objectives, risk tolerance and regulatory features. Regular contributions and appropriate product selection, combined with awareness of charges and tax implications, help build a robust retirement and investment plan.

FAQs on Mutual Funds & Pension Funds

| 1. What are Mutual Funds? |  |

| 2. How are Mutual Funds Priced? | |

| 3. What are the types of Mutual Funds? | |

| 4. What are the cons of Mutual Fund investing? | |

| 5. What is the Employees' Provident Fund Organization Pension Scheme? | |