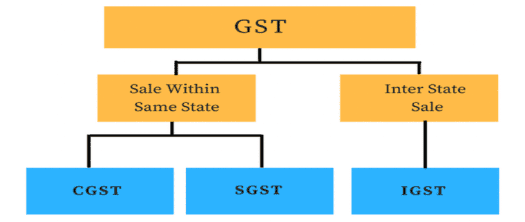

GST is a multi-stage value-added tax on the consumption of goods or services or both. In India, a "dual GST" model has been adopted, where both the Centre and the States simultaneously levy GST on every supply of goods or services within a State or Union territory. This approach is in line with the federal structure of the country.

Rationale for IGST

Before delving into the IGST Model and its features, it's essential to understand how inter-state trade or commerce was regulated in the previous indirect tax system. The Central Sales Tax Act, 1956, played a crucial role in this regard.

Central Sales Tax Act, 1956

The Central Sales Tax Act, 1956, was enacted to regulate inter-state trade or commerce (referred to as "CST") and was based on the constitutional authority derived from Article 269 of the Constitution of India.

Article 286 of the Constitution prohibited States from levying sales tax on sales or purchases of goods that occurred outside the State or during the import or export of goods. Only Parliament had the authority to levy tax on such transactions.

The Central Sales Tax Act provided principles for determining when a sale or purchase of goods takes place in the course of interstate trade or commerce. It also outlined the levy and collection of taxes on such sales.

Shortcomings of CST

CST was collected and retained by the origin state, which was inconsistent with the nature of indirect tax as a consumption tax. Indirect taxes should ideally accrue to the destination state where the consumer is located.

Input Tax Credit (ITC) of CST was not allowed to the buyer, leading to cascading tax effects (tax on tax) within the supply chain.

The requirement of various accountal forms in CST, such as C Form, E1, E2, F, I, J Forms, increased compliance costs for businesses and hindered the free flow of trade.

MULTIPLE CHOICE QUESTION

Try yourself: What was the primary issue with the Central Sales Tax (CST) system before the implementation of Integrated Goods and Services Tax (IGST)?

A

CST was levied only by the States, leading to a loss of revenue for the Centre.

B

CST did not allow Input Tax Credit (ITC), resulting in cascading tax effects.

C

CST required multiple accountal forms, increasing compliance costs for businesses.

D

CST was not applicable on inter-state trade or commerce.

Correct Answer: B

- Input Tax Credit (ITC) was not allowed in the CST system, leading to the cascading effect of taxes within the supply chain. - This meant that taxes were levied on top of taxes, increasing the overall cost of goods and services.

Report a problem

Introduction of IGST

The IGST model was introduced to address the shortcomings of the CST system.

IGST is designed to monitor inter-state trade of goods and services and ensure that the SGST component accrues to the consumer state.

It aims to maintain the integrity of the Input Tax Credit (ITC) chain in inter-state supplies.

The IGST rate is generally equal to the sum of the CGST rate and the SGST rate.

IGST is levied by the Central Government on all inter-State transactions of taxable goods or services.

For example, if the CGST rate is 9% and the SGST rate is 9%, the IGST rate would be 18% (9% + 9%).

Nature of Supply

Determining the nature of supply, whether inter-state or intra-state, is crucial as it dictates the type of tax to be paid (IGST or CGST+SGST).

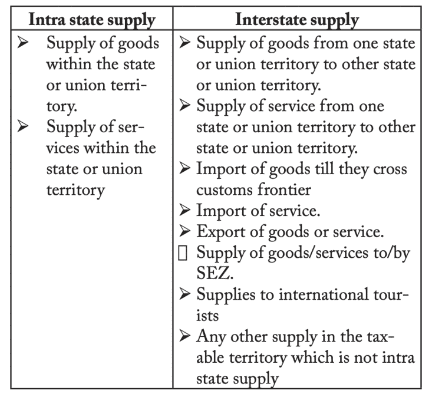

Inter-State Supply refers to supplies where the location of the supplier and the place of supply are in different States, different Union territories, or a State and a Union territory. Such supplies are considered as inter-State trade or commerce.

Examples of inter-State supply include:

Supply of goods or services from one State to another State.

Supply of goods or services from one Union territory to another Union territory.

Supply of goods or services from a State to a Union territory, or vice versa.

Import of goods into India until they cross the customs frontiers.

Import of services into India.

Export of goods or services.

Supply of goods or services to or by a Special Economic Zone (SEZ).

Supplies to international tourists.

Any other supply in the taxable territory that is not classified as intra-State supply.

Intra-State supply is defined as any supply where the location of the supplier and the place of supply are in the same State or Union territory. The determination of intra-state or inter-state supply depends on the location of the supplier and the place of supply, both of which are defined in the IGST Act.

Compensation Cess in GST

The Goods and Services Tax (Compensation to States) Act, 2017 was enacted to impose a Compensation cess aimed at compensating States for revenue losses resulting from the implementation of the Goods and Services Tax (GST).

This cess came into effect from July 1, 2017, coinciding with the enforcement of the Central Goods and Services Tax Act.

The duration of the cess is initially set for five years, but it may be extended based on recommendations from the GST Council.

For goods imported into India, the Compensation cess is levied and collected according to the provisions of section 3 of the Customs Tariff Act, 1975. This occurs at the point when customs duties are imposed on the goods under section 12 of the Customs Act, 1962, and the value of the goods is determined under the Customs Tariff Act, 1975.

Compensation Cess is not applicable to goods exported by an exporter under bond. In such cases, the exporter is entitled to a refund of the input tax credit related to Compensation Cess for the exported goods.

If goods are exported with the payment of Compensation Cess, the exporter is eligible for a refund of the Compensation Cess paid on the exported goods.

Compensation Cess is not applicable to supplies made by a taxable person who opts for the composition levy.

MULTIPLE CHOICE QUESTION

Try yourself: Which type of supply involves transactions between different States or Union territories?

A

Intra-State Supply

B

Inter-State Supply

C

International Supply

D

Export Supply

Correct Answer: B

- Inter-State supply refers to transactions between different States, Union territories, or a State and a Union territory. - It involves supplies where the location of the supplier and the place of supply are in different geographical areas. - This type of supply attracts IGST, which is levied by the Central Government on all inter-State transactions of taxable goods or services.

Report a problem

The document Overview: IGST and Compensation Cess in GST is a part of the CLAT PG Course Tax Law.

FAQs on Overview: IGST and Compensation Cess in GST

1. What is the Integrated Goods and Services Tax (IGST) and its purpose?

Ans. The Integrated Goods and Services Tax (IGST) is a tax levied on the supply of goods and services in a multi-state context within India. Its primary purpose is to facilitate seamless inter-state trade by ensuring that tax is collected at the point of consumption rather than at the point of origin. This helps eliminate the cascading effect of taxes and promotes a unified market across the country.

2. How does the introduction of IGST impact inter-state transactions?

Ans. The introduction of IGST significantly impacts inter-state transactions by allowing businesses to collect and pay taxes in a uniform manner across states. Under IGST, the tax is collected by the central government on inter-state supplies, which is then shared with the respective states. This simplifies compliance for businesses and reduces the complexities associated with multiple state taxes.

3. What role does Compensation Cess play in the GST framework?

Ans. Compensation Cess is an additional tax imposed under the Goods and Services Tax (GST) framework to compensate states for any revenue loss they may incur due to the implementation of GST. This cess is applicable on specific goods and services, particularly those deemed 'sin goods' like tobacco and luxury items. The revenue generated from this cess is used to meet the shortfall in the states' revenue for a stipulated period.

4. How do businesses benefit from the IGST model?

Ans. Businesses benefit from the IGST model as it streamlines the tax process for inter-state transactions, reducing compliance costs and administrative burdens. It allows for seamless input tax credit across states, enabling businesses to offset the tax they pay on purchases against the tax they collect on sales. This results in a more efficient tax system and better cash flow management for businesses.

5. What are the challenges associated with the implementation of IGST?

Ans. The challenges associated with the implementation of IGST include complexities in compliance, particularly for small and medium enterprises that may struggle with the filing of returns and maintaining accurate records. Additionally, there may be issues related to the reconciliation of input tax credits, disputes between states regarding revenue sharing, and the need for robust technology infrastructure to support the new tax regime.

Exam, pdf , ppt, Overview: IGST and Compensation Cess in GST, past year papers, MCQs, Important questions, mock tests for examination, practice quizzes, Sample Paper, Extra Questions, Previous Year Questions with Solutions, Overview: IGST and Compensation Cess in GST, video lectures, Free, shortcuts and tricks, Overview: IGST and Compensation Cess in GST, Summary, Objective type Questions, Viva Questions, study material, Semester Notes;

This approach is in line with the federal structure of the country.

This approach is in line with the federal structure of the country.