DK Goel Solutions: Financial Statements of Companies (As per Schedule III) | DK Goel Solutions - Class 12 Accountancy - Commerce PDF Download

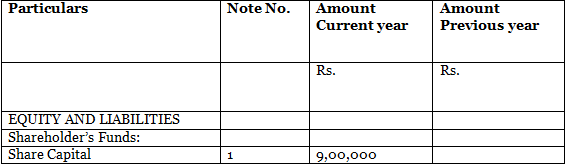

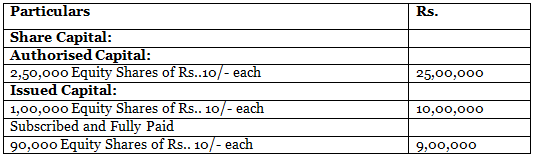

Q1: On 1st April 2018, ABC Ltd. was established with an authorized capital of Rs. 25,00,000/- divided into 2,50,000 equity shares of Rs. 10/- each. Out of these, the company issued 1,00,000 equity shares of Rs. 10/- each at a premium of 10%. The amount was payable as follows:

On Application: Rs. 4/- (including premium)

On Allotment: Rs. 4/-

On Final Call: Rs. 3/-

The public applied for 90,000 equity shares and all the money was duly received. How will you show the ‘Share Capital’ in the Balance Sheet of a company? Also, prepare ‘notes to accounts’ for the same.

Ans:

Extract of Balance Sheet of ABC LTD.

As at 31st March 2019

Notes to Accounts:

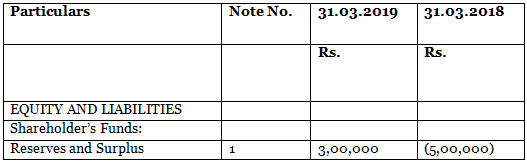

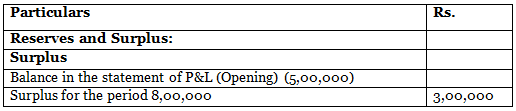

Q2: French Ltd. has an opening debit balance of Rs. 5,00,000/- in Reserves and Surplus as Balance of Statement of Profit and Loss. It earned a profit of Rs. 8,00,000/- for the year ended March 31st 2019. How would you show these items in the Balance Sheet and notes to accounts?

Ans:

French Ltd.

Extract of Balance Sheet as at 31st March 2019

Notes to Accounts:

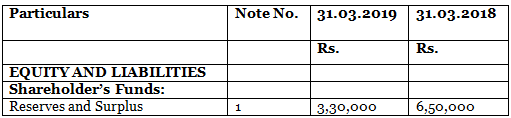

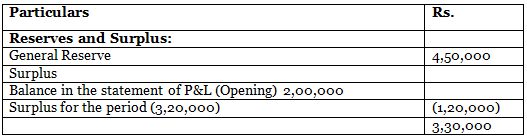

Q3: Neptune Ltd. has the following balances on 1st April 2018:

Rs.

General reserve 4,50,000

Statements of P&L 2,00,000

During the year ended 31st March 2019, it incurred a loss of Rs. 3,20,000/-. How would you show these items in the Balance Sheet and notes to accounts?

Ans:

Neptune Ltd.

Extract of Balance Sheet as at 31st March 2019

Notes to Accounts:

Q4: Name the sub-headings under which the shareholder’s funds shall be classified in a company’s balance sheet.

Ans:

Shareholder’s funds shall be classified as follows:

- Share Capital

- Reserves and Surplus

- Money received against share warrants

FAQs on DK Goel Solutions: Financial Statements of Companies (As per Schedule III) - DK Goel Solutions - Class 12 Accountancy - Commerce

| 1. What are the key components of financial statements as per Schedule III? |  |

| 2. How does Schedule III affect the presentation of financial statements? | |

| 3. What is the significance of the Notes to Accounts in financial statements? | |

| 4. How do companies ensure compliance with Schedule III while preparing financial statements? | |

| 5. What are the consequences of non-compliance with Schedule III for companies? | |

Extra Questions

,Free

,video lectures

,Semester Notes

,past year papers

,Important questions

,Objective type Questions

,DK Goel Solutions: Financial Statements of Companies (As per Schedule III) | DK Goel Solutions - Class 12 Accountancy - Commerce

,study material

,mock tests for examination

,shortcuts and tricks

,Viva Questions

,Summary

,MCQs

,Sample Paper

,practice quizzes

,DK Goel Solutions: Financial Statements of Companies (As per Schedule III) | DK Goel Solutions - Class 12 Accountancy - Commerce

,ppt

,Previous Year Questions with Solutions

,DK Goel Solutions: Financial Statements of Companies (As per Schedule III) | DK Goel Solutions - Class 12 Accountancy - Commerce

,Exam

;

DK Goel Solutions: Financial Statements of Companies (As per Schedule III) Free PDF Download

Importance of DK Goel Solutions: Financial Statements of Companies (As per Schedule III)

DK Goel Solutions: Financial Statements of Companies (As per Schedule III) Notes

DK Goel Solutions: Financial Statements of Companies (As per Schedule III) Commerce Questions

Study DK Goel Solutions: Financial Statements of Companies (As per Schedule III) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!