Chapter Notes- Unit 7: Accounting Standards

Unit Overview

Introduction to Accounting Standards

- Accounting is the language of business used to communicate the financial performance and position of an enterprise to users such as owners, investors, lenders, regulators and the public.

- Without consistent rules and guidance, financial statements may become misleading or biased. Accounting Standards (ASs) provide a framework of principles and standard policies to ensure financial statements are transparent, comparable, reliable and useful for decision-making.

- Accounting standards are authoritative documents issued by recognised standard-setting bodies and/or regulators. They address the recognition, measurement, presentation and disclosure of transactions and events in financial statements.

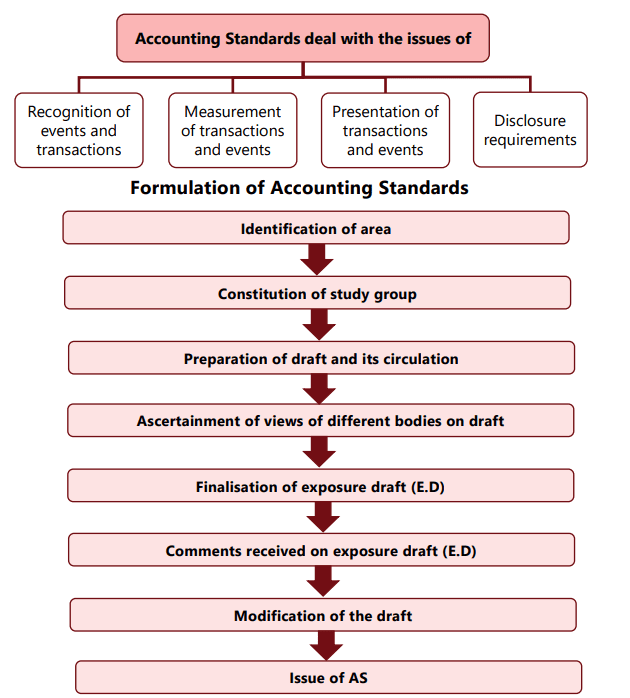

Accounting standards focus on several key areas:

1. Recognition: Determining when events and transactions should be recognized in financial statements.

2. Measurement: Assessing the value of these transactions and events.

3. Presentation: Organizing and presenting these transactions and events in a way that is clear and understandable to readers.

4. Disclosure: Outlining the information that must be disclosed to the public, stakeholders, and potential investors to provide insight into the financial statements and aid in informed decision-making.

Objectives of Accounting Standards

Accounting standards aim to harmonize the accounting policies and practices of different business entities. The goal is to standardize the diverse accounting practices used for various aspects of accounting. By doing so, accounting standards seek to:

- Eliminate non-comparability: Improve the reliability of financial statements by making them more comparable across different entities.

- Provide standard policies: Offer a set of standard accounting policies, valuation norms, and disclosure requirements.

Benefits and Limitations of Accounting Standards

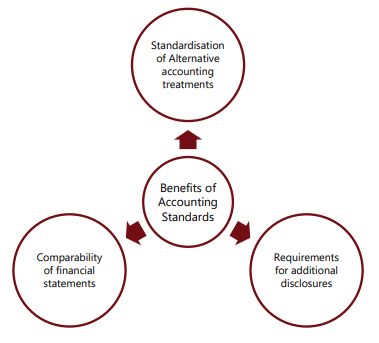

Benefits of Accounting Standards

- Standardisation of accounting treatments: Reduces arbitrary variations in the preparation of financial statements.

- Improved disclosures: Standards may require additional information beyond statutory minimums, improving transparency.

- Enhanced comparability: Comparable financial statements help investors and lenders assess performance across entities and periods.

- Consistency: Application of standards across periods promotes consistency in reporting and helps trend analysis.

- Credibility: Following recognised standards increases confidence among users of financial statements.

Limitations of Accounting Standards

- Choice between acceptable treatments: Some problems admit more than one reasonable solution; standards cannot eliminate all judgment and choice.

- Restricted scope: Standards operate within the legal framework and cannot override statutory provisions.

- Others:

Cost of compliance: Preparing additional disclosures and applying certain measurement bases (e.g., fair value) may increase cost for preparers.

Complexity: Highly detailed standards can be difficult for smaller entities to interpret and apply without specialist help.

Rapid change: Economic and business innovations may outpace the standard-setting process, leaving gaps until standards are revised.

Process of Formulation of Accounting Standards in India

Background: The Institute of Chartered Accountants of India (ICAI) is the principal accounting body in India. In 1977 ICAI constituted the Accounting Standards Board (ASB) to formulate accounting standards for India.

Role and independence of ASB:

- The ASB functions under the aegis of ICAI but is required to operate with professional independence in the process of standard formulation.

- The ASB considers international standards such as IFRS (issued by the International Accounting Standards Board - IASB) and adapts them to the Indian legal, regulatory and economic context.

- The ASB's composition includes representatives from industry associations (for example ASSOCHAM, CII, FICCI), regulators, academicians and government departments to ensure diverse stakeholder inputs.

Standard-setting procedure followed by ASB (step-wise):

- Identification of subject areas: ASB identifies issues requiring standardisation.

- Constitution of study group: A study group of experts researches the topic and prepares a preliminary draft covering objectives, scope, definitions, recognition, measurement, presentation and disclosures.

- ASB review and revision: ASB reviews the draft, suggests revisions and refines the proposals through discussion.

- Exposure draft/circulation: A revised draft (exposure draft) is circulated to ICAI Council members and specified outside bodies for comments.

- Public consultation: Meetings with stakeholders and public comment periods are used to obtain broader feedback.

- Consideration of comments: Comments received are analysed and appropriate changes are made to the draft.

- Finalisation and submission: The final draft is submitted to the ICAI Council for approval.

- Approval and issuance: After approval, the standard is issued. For companies, the Government of India may notify standards under the Companies Act; for non-company entities, ICAI issues standards for application.

After ASB finalises a standard, the ICAI Council may modify it in consultation with ASB if necessary. For corporate entities not covered by Ind AS, the Central Government issues accounting standards under relevant statutory rules (for example, the Companies (Accounting Standards) Rules, 2021).

Three sets of Accounting Standards in India

- Indian Accounting Standards (Ind AS): Converged standards largely aligned with IFRS; applicable to listed companies, certain NBFCs and unlisted companies/ NBFCs meeting statutory thresholds (for example, net worth of INR 250 crore or more where specified by regulation).

- Accounting Standards (AS) notified under Companies (Accounting Standards) Rules, 2021: Applicable to companies which are not required to apply Ind AS.

- Accounting Standards issued by ICAI: Applicable to non-company entities (for example, partnerships, sole proprietorships, societies) and other entities as prescribed.

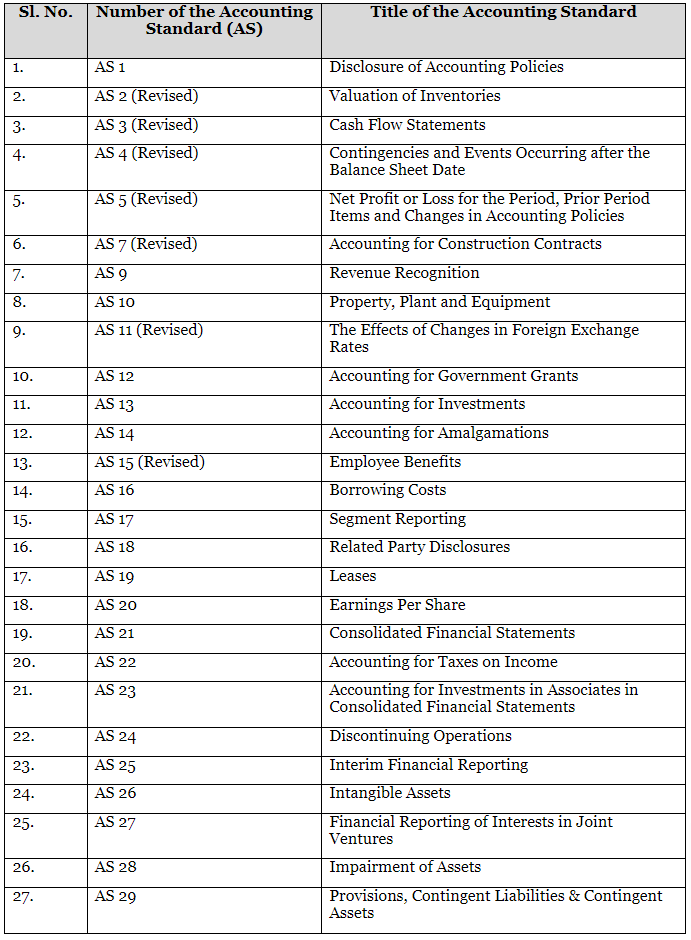

List of Accounting Standards in India

The Accounting Standards Board issues standards that embody generally accepted accounting principles (GAAP). These standards provide detailed guidance on accounting for specific items (for example, inventories, depreciation, revenue, leases, events after reporting period, related party disclosures, etc.).

Refer to the authorised list and current notifications for the exact titles and applicability of each standard.

Note: The list of accounting standards given above does not form part of the syllabus. It has been given here for the knowledge of students only.

**Introduction to Indian Accounting Standards (Ind AS)

- Origin: In 2006, ICAI initiated the process of aligning Indian accounting standards with International Financial Reporting Standards (IFRS) issued by the IASB. The objective was improved comparability and transparency of Indian corporate financial reporting at an international level.

- Convergence (not blind adoption): The Indian approach has been to converge with IFRS - adopt standards that are substantially in line with IFRS while making necessary modifications for the Indian legal, economic and regulatory environment.

- Stakeholder consultation: Adoption/convergence decisions involved wide consultations with government, regulators, industry bodies and accounting professionals to ensure practical applicability.

- Local adaptations: Where required, Ind AS contains departures from IFRS to reflect India's specific needs, laws and economic conditions.

List of Ind AS on 1st August, 2024

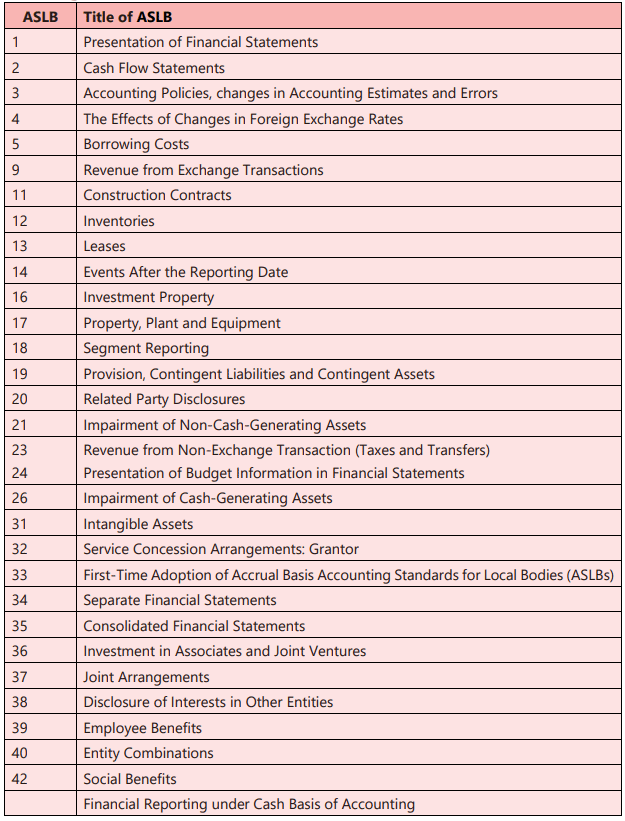

**Accounting Standards for Local Bodies

Accounting Standards for Local Bodies (ASLB) are designed for public service entities such as municipalities, city corporations, panchayats and other local authorities. These entities primarily provide services to the public rather than operating for profit; therefore, financial reporting needs differ from business enterprises.

List of Accounting Standards for Local Bodies (ASLB) as on 1st August, 2024

** Note: The above Ind AS and ASLB illustrations are provided for general knowledge and do not form part of the core examination syllabus unless specifically stated by the examining body.

FAQs on Chapter Notes- Unit 7: Accounting Standards

| 1. What are the objectives of accounting standards in India? |  |

| 2. What are the advantages of implementing accounting standards? | |

| 3. What is the process of formulation of accounting standards in India? | |

| 4. What is the significance of Indian Accounting Standards (IND AS)? | |

| 5. What are the accounting standards applicable to local bodies in India? | |