Chapter Notes- Unit 6: Rectification of Errors

Unit Overview

Introduction

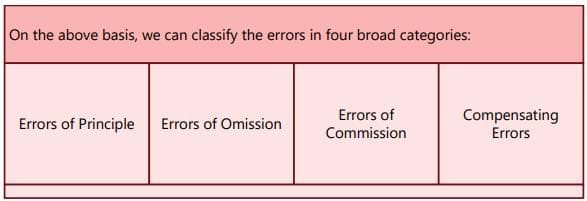

- Errors in accounting are unintentional mistakes made while recording financial transactions; they may involve omission, wrong amounts, wrong account, wrong side (debit/credit) or wrong classification.

- Errors may occur at different stages of the accounting cycle: while collecting source documents, while recording in subsidiary books, while posting to ledger accounts, while balancing ledgers or while preparing the trial balance and final accounts.

- Common causes include arithmetic mistakes, incorrect application of accounting principles, misinterpretation of facts and oversight.

- Preparation of a trial balance checks the arithmetic accuracy of ledger posting. A difference between total debits and total credits indicates the presence of errors that must be investigated and rectified.

- Some errors affect the trial balance (making it disagree); other errors do not affect the agreement of the trial balance even though they may affect profit, assets or liabilities.

Illustrative Case of Errors and their Nature

- After preparing ledger accounts a trial balance is prepared which lists debit and credit balances separately.

- Debits and credits must agree; if not, errors exist and must be located.

- Errors arise in many different forms; identifying their nature helps determine the method of rectification.

- Careful study of examples below clarifies types of errors and their correction.

(a) Wrong Entry (errors in subsidiary books)

Wrong amounts or wrong entries in subsidiary books (Purchases Day Book, Sales Day Book, Journal Proper, Cash Book etc.) are common sources of error.

Example 1: Credit purchases ₹17,270 are entered in the Purchases Day Book as ₹17,720. Credit sales of ₹15,000 gross less 1% trade discount are wrongly entered in Sales Day Book at ₹15,000. Cheque issued ₹19,920 are wrongly entered in the credit of bank column in the Cash Book as ₹19,290.

(b) Wrong casting of subsidiary books

Totals of subsidiary books may be totalled incorrectly and the wrong total posted to ledger accounts.

Example 2: For the month of January, 2022 total of credit sales are ₹1,75,700; this is wrongly totalled as ₹1,76,700 and posted to Sales account as ₹1,76,700.

(c) In case of Cash Book

Wrong castings or wrong entries in the Cash Book affect the cash/bank balances. Cash balances are often verified daily so cash errors are detected early; bank errors may remain until bank reconciliation.

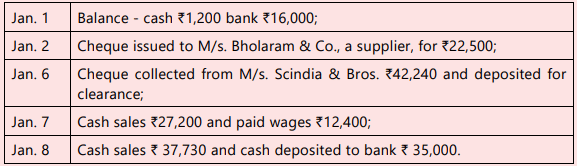

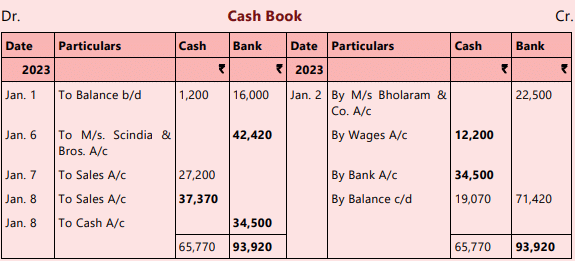

Example 3: The following cash transactions of M/s. Tularam & Co. occurred: 2023

The following Cash Book entries are passed:

Wrong entries and wrong casting are shown in bold prints. In the above example there are four wrong entries and one wrong casting. Bank and cash balances are affected by these errors.

(d) Wrong posting from subsidiary books

Amounts may be posted to the wrong ledger account, posted on the wrong side or posted in a wrong amount. For example, purchases from A may be posted to B's account.

(e) Wrong casting of ledger balances

Balances in ledger accounts may be wrongly totalled or cast; this gives wrong balances although the postings themselves may be correct.

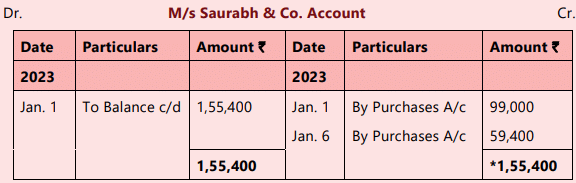

Example 4: The following are the credit purchases of M/s. Ballav Bros.: 2023

Jan. 1 Purchases from M/s. Saurabh & Co.- gross ₹1,00,000 less 1% trade discount.

Jan. 3 Purchases from M/s. Netai & Co.- gross ₹ 70,000 less 1% trade discount.

Jan. 6 Purchases from M/s. Saurabh & Co.- gross ₹ 60,000 less 1% trade discount.

Let us cast M/s. Saurabh & Co.'s Account:*While casting the credit side, an error has been committed and so the account is wrongly balanced.

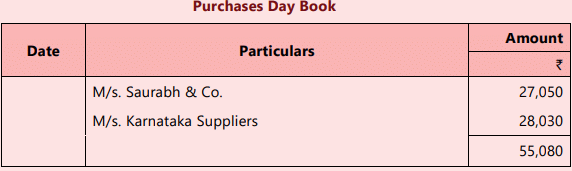

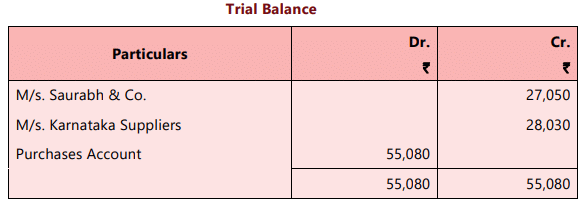

Example 5: Goods are purchased on credit from M/s. Saurabh & Co. for ₹ 27,030 and from M/s. Karnataka Suppliers for ₹ 28,050. The following Purchase Day Book is prepared:

In the above Purchase Day Book, both the transactions are entered wrongly but the first error has been compensated by the second. Even if these errors are not rectified the Trial Balance would tally.

Stages of Errors

Errors can happen at any stage of the accounting process. Classification by stage helps to locate and correct them.

At the Stage of Recording Transactions in the Journal

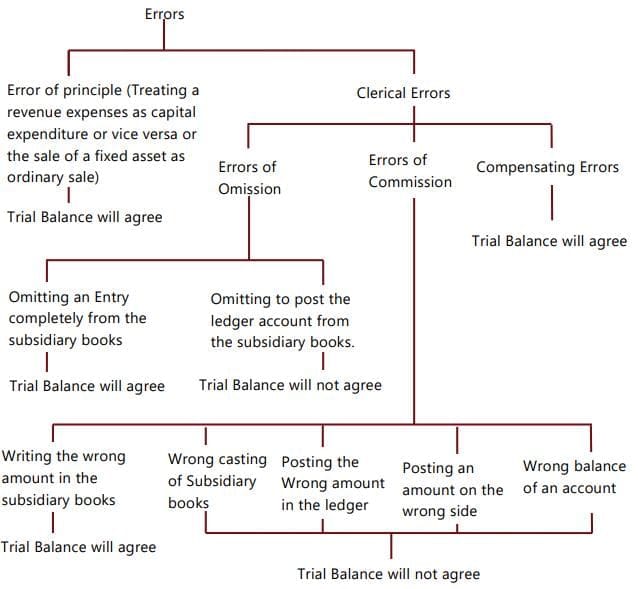

- Errors of Principle: Violation of fundamental accounting principles; e.g., recording capital expenditure as revenue expense.

- Errors of Omission: Transaction completely omitted from books; e.g., failing to record a sale.

- Errors of Commission: Transaction recorded incorrectly (wrong amount, wrong account) but not omitted.

At the Stage of Posting Entries in the Ledger

- Errors of Omission - partial or complete omission while posting.

- Partial Omission - only one side of a transaction posted.

- Complete Omission - entire transaction omitted from ledger.

- Errors of Commission - posting to wrong account, wrong side or wrong amount.

At the Stage of Balancing the Ledger Accounts

- Wrong totalling of accounts.

- Wrong balancing of accounts.

At the Stage of Preparing the Trial Balance

- Errors of omission - omission of an account or balance from the trial balance.

- Errors of commission - wrong amount, wrong column or wrong side taken in the trial balance.

- Taking the wrong account or wrong amount or taking the balance to the wrong side.

- Errors of Principle: Misclassification violates accounting principles.

- Errors of Omission: Transactions omitted wholly or partly.

- Errors of Commission: Wrong postings, totals or balances.

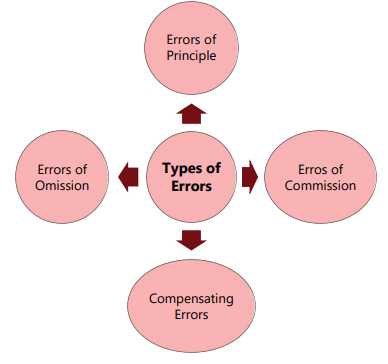

- Compensating Errors: Two or more independent errors that cancel each other so the trial balance still agrees.

Types of Errors - Detailed Notes

(a) Errors of Principle

- Result from incorrect application of accounting concepts - e.g., treating the purchase of an asset as an expense.

- Such errors usually do not affect the agreement of the trial balance because amounts are placed on the correct sides but in the wrong accounts.

(b) Clerical Errors

Ordinary mistakes committed during routine accounting, grouped as:

- Errors of Omission: Not recording or not posting a transaction.

- Errors of Commission: Wrong account, wrong side, wrong totals or wrong balances.

(c) Compensating Errors:

- Compensating errors are mistakes that cancel each other out.

- Because they balance each other, the trial balance still matches.

- Example: Not crediting ₹10 to A's account is cancelled by recording ₹10 extra in the Sales Book.

Errors based on the Trial Balance Affect

Errors Affecting the Trial Balance

- Wrong casting of subsidiary books.

- Wrong balancing of an account.

- Posting an amount on the wrong side.

- Posting the wrong amount.

- Omission of posting from the subsidiary book.

- Omission of subsidiary book totals.

- Omission of cash book balances.

- Incorrect column or wrong totalling in the trial balance.

Errors Not Affecting the Trial Balance

- Omission from subsidiary book (if both debit and credit get omitted, the trial balance may still agree).

- Wrong amount in the subsidiary book where compensating posting occurs.

- Wrong account posting, but the correct side - trial balance still agrees.

Steps to Identify Errors in the Trial Balance

Even a small difference means errors exist. Use systematic checks to locate them.

(i) Recheck the Totals:

- Verify the totals of both columns of the trial balance.

- If a single amount was written instead of the list, re-total the source list (e.g., list of trade receivables).

(ii) Check Cash and Bank Balances:

Ensure cash and bank balances are included correctly in the trial balance.

(iii) Determine the Exact Difference:

- Establish the exact amount of the difference.

- Look for a ledger balance equal to the difference (omitted from trial balance).

- Consider half the difference - an amount equal to half may have been posted on the wrong side.

(iv) Re-Balance Ledger Accounts:

- Balance ledger accounts again to check for totalling or balancing errors.

(v) Check Subsidiary Books:

- Recheck casting of subsidiary books, especially for small differences (₹1, ₹10, ₹10,0 etc.).

(vi) Compare with Previous Period:

- If differences are large, compare current balances with prior period to locate anomalies.

(vii) Check Postings:

- Review postings of amounts equal to the difference or half the difference.

- Check for amounts posted on the wrong side or omitted.

(viii) Complete Checking:

- If a difference remains, a thorough check of all entries, including opening entries, is required.

- Often efficient to begin checking with nominal accounts.

Rectification of Errors

- Do not correct errors by overwriting. Make proper rectifying entries in the books.

- Method of rectification depends on when the error is detected: before trial balance, after trial balance but before final accounts, or in the next accounting period.

Before Preparing the Trial Balance

- Errors discovered before preparing the trial balance are rectified by appropriate adjustments on the relevant accounts.

- Some errors affect only one account and cannot be corrected by a single complete journal entry; these are corrected by adjusting the affected accounts with suitable narration (rectification statement).

Examples (preserve original instructional content):

- The sales book for November is underreported by ₹ 200. Correction: credit Sales Account by ₹200 with narration "By undercasting of Sales Book for November ₹200."

- A discount of ₹ 10 given to Ramesh was not recorded in the cash book's debit side. Correction: post credit to Ramesh of ₹10 with narration "By omission of posting of discount on ----- ₹10."

- Amount of ₹ 200 received from Ram entered on the debit side of his account. Correction: remove wrong debit and credit his account - can be effected by an entry addressing the wrong side posting (narrations and amounts as required).

- Amount of ₹ 50 received from Mahesh was recorded in the cash book but not posted to his account. Correction: post credit to Mahesh of ₹50 with narration "By omission of posting ₹50."

- Payment of ₹ 51 to Mohan was posted as ₹15. Short by ₹36. Correction: post ₹36 with narration "To mistake in posting ₹36."

- Goods sold to Ram for ₹ 1,000 were posted to Purchases instead of Sales (Ram's account credited correctly). This cannot be corrected by a single complete journal entry; corrections are made by posting to purchases and sales accounts appropriately with explanatory narrations.

- Bill receivable of ₹ 500 from A posted to the Bills Payable account; correction requires debiting Bills Payable and crediting the Bills Receivable with suitable narrations.

- Goods purchased from Vinod for ₹ 1,000 were credited as ₹100 to Vimal's account - rectification needs correcting postings and narrations to reflect true amounts.

Thus, the general rule that errors involving two accounts are always rectified by one journal entry does not always hold. Some multi-account errors require separate adjustments or explanatory rectification entries.

ILLUSTRATION 1

1. The total in the Purchases Book has been undercast by ₹ 100.

2. The Returns Inward Book has been undercast by ₹ 50.

3. A sum of ₹ 250 written off as depreciation on Machinery has not been debited to Depreciation Account.

4. A payment of ₹75 for salaries (to Mohan) has been posted twice to Salaries Account.

5. The total of Bills Receivable Book ₹ 1,500 has been posted to the credit of Bills Receivable Account.

6. An amount of ₹ 151 for a credit sale to Hari, although correctly entered in the Sales Book, has been posted as ₹ 115.

7. Discount allowed to Satish ₹ 25 has not been entered in the Discount Column of the Cash Book. The amount has been posted correctly to the credit of his personal account.

SOLUTION

- The Purchases Account should be debited by ₹ 100 as it was undercast previously. Narration: "To Undercasting of Purchases Book for the month of --- ₹100."

- Undercasting of the Returns Inward Book: post "To Undercasting of Returns Inward Book for the month of --- ₹50."

- Omission of the debit to Depreciation Account: rectified by posting "To Omission of posting on ₹250."

- Excess debit (double posting) to Salaries Account should be removed by crediting Salaries Account with the excess amount (exact narration as per books).

- The Bills Receivable Book total of ₹1,500 was posted to the credit instead of debit; correct by debiting Bills Receivable Account by ₹3,000 with narration "To Wrong posting of B/R received on ₹3,000." (Explanation: reversing the wrong posting and restoring the correct side.)

- Hari's personal A/c is debited ₹36 short. Rectify by posting "To Wrong posting ₹36."

- Discount allowed to Satish ₹25 omitted from discount column: rectify by posting "By double posting on ₹75" and "To omission of discount allowed to Satish on ₹25." (Narrations as per ledger practice.)

The corrections above show that some errors affecting single accounts are rectified by adjusting those accounts with suitable narrations rather than by a single journal entry debiting one account and crediting another.

We now consider errors affecting more than one account where a complete journal entry is possible for rectification.

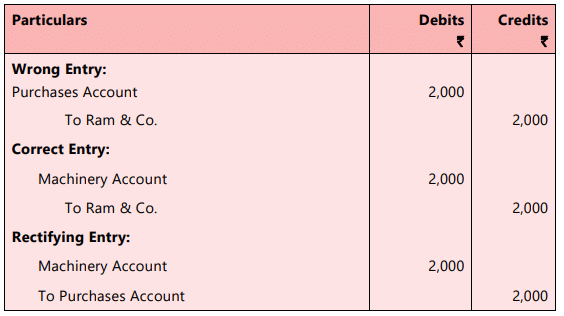

(i) The purchase of machinery for ₹2,000 recorded in the Purchases Book - the supplier account correctly credited by ₹2,000 but Purchases was debited instead of Machinery. Correction: transfer debit from Purchases to Machinery by crediting Purchases and debiting Machinery.

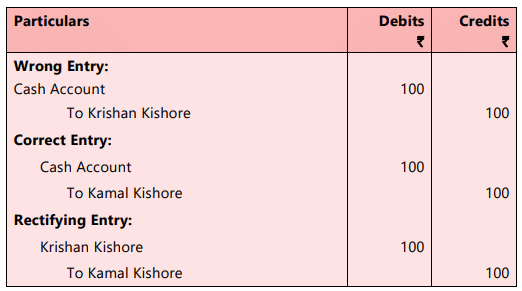

(ii) ₹100 received from Kamal Kishore credited to Krishan Kishore - Krishan should be debited and Kamal credited. Rectify by debiting Krishan and crediting Kamal (with appropriate reversal and posting entries).

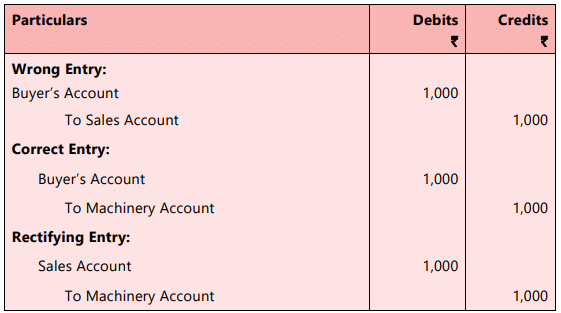

(iii) Sale of old machinery ₹1,000 entered in Sales Book - buyer correctly debited but Sales credited instead of Machinery. Rectify by debiting Sales and crediting Machinery to reverse the wrong posting and post correct one.

ILLUSTRATION 2

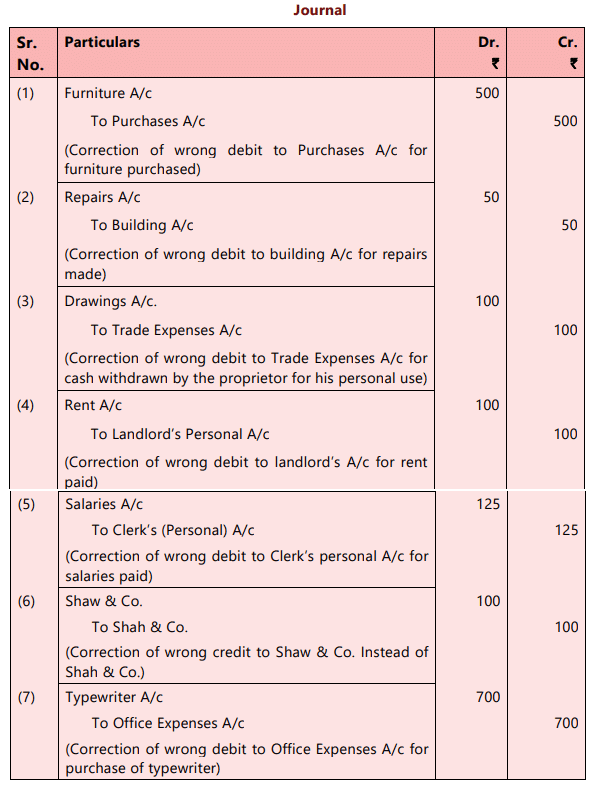

The following errors were found in the book of Ram Prasad & Sons. Give the necessary entries to correct them.

- ₹ 500 paid for furniture purchased has been charged to ordinary Purchases Account.

- Repairs made were debited to Building Account for ₹ 50.

- An amount of ₹ 100 withdrawn by the proprietor for his personal use has been debited to Trade Expenses Account.

- ₹ 100 paid for rent debited to Landlord's Account.

- Salary ₹ 125 paid to a clerk due to him has been debited to his personal account.

- ₹ 100 received from Shah & Co. has been wrongly entered as from Shaw & Co.

- ₹ 700 paid in cash for a typewriter was charged to Office Expenses Account.

SOLUTION

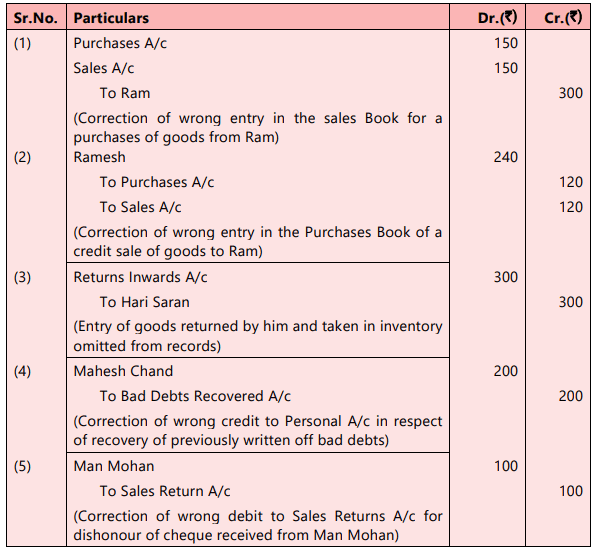

ILLUSTRATION 3

Give journal entries to rectify the following:

- A purchase of goods from Ram amounting to ₹150 has been wrongly entered through the Sales Book.

- A credit sale of goods amounting ₹120 to Ramesh has been wrongly passed through the Purchase Book.

- On 31st December, 2022 goods of the value of ₹300 returned by Hari Saran and were taken into inventory on the same date but no entry was passed in the books.

- An amount of ₹200 due from Mahesh Chand, which had been written off as a Bad Debt in a previous year, was unexpectedly recovered and had been posted to the personal account of Mahesh Chand.

- A cheque for ₹100 received from Man Mohan was dishonoured and had been posted to the debit of Sales Returns Account.

SOLUTION

Thus, it can be said that errors detected before the preparation of trial balance can be rectified either through rectification statements (not entries) or through rectification entries.

After Trial Balance but before Final Accounts

When errors are detected after the trial balance is prepared, correction methods differ. Sometimes the trial balance is made to agree by opening a Suspense Account.

Suspense Account - Key Points

- A Suspense Account is used to balance the trial when debit and credit totals differ.

- If the credit column is short, the Suspense Account is credited; if the debit column is short, Suspense is debited.

- The agreement obtained by using the Suspense Account is temporary; errors must be located and the Suspense Account cleared.

Rectification of Errors (after trial balance)

- Errors that caused the opening of the Suspense Account are rectified by journal entries debiting or crediting the Suspense Account as appropriate and correcting affected accounts.

- Errors that can be corrected by complete journal entries (affecting more than one account) are rectified in the same manner as when discovered earlier.

Example: If the Sales Book is cast short by ₹100, then the credit column of the trial balance is ₹100 short, and the Suspense Account is credited by ₹100. To rectify: credit the Sales Account by ₹100 and debit the Suspense Account to close it.

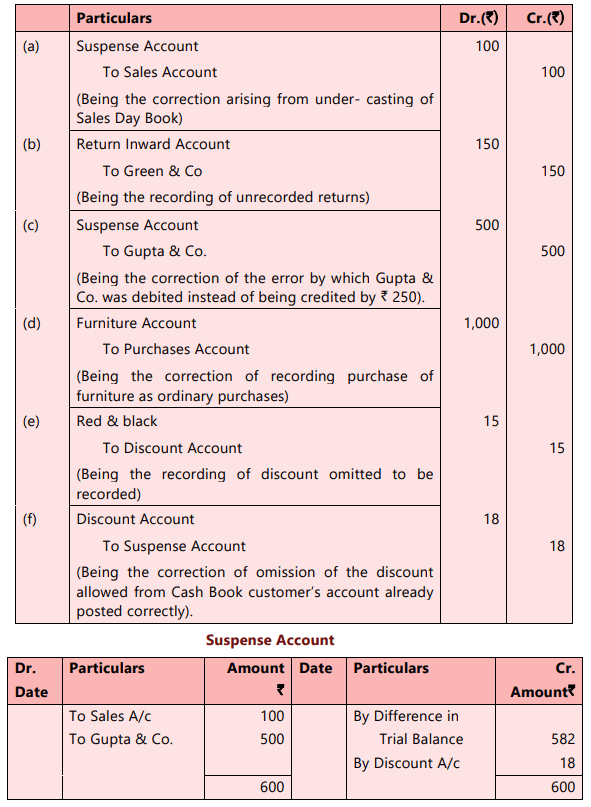

ILLUSTRATION 4

Correct the following errors (i) without opening a Suspense Account and (ii) opening a Suspense Account:

(a) The Sales Book has been totalled ₹100 short.

(b) Goods worth ₹150 returned by Green & Co. have not been recorded anywhere.

(c) Goods purchased ₹250 have been posted to the debit of the supplier Gupta & Co.

(d) Furniture purchased from Gulab & Bros, ₹1,000 has been entered in Purchases Day Book.

(e) Discount received from Red & Black, ₹15, has not been entered in the Discount Column of the Cash Book.

(f) Discount allowed to G. Mohan & Co. ₹18 has not been entered in the Discount Column of the Cash Book. The account of G. Mohan & Co. has, however, been correctly posted.

SOLUTION

If a Suspense Account is not opened:

(a) Sales Book cast short ₹100 - Credit Sales Account by ₹100 with narration "By wrong totalling of the Sales Book ₹100".

(b) To rectify omission of return by Green & Co.: Debit Returns Inwards Account and Credit Green & Co. The entry is:

(c) Gupta & Co. were debited ₹250 instead of being credited. Now credit Gupta & Co. by ₹500 to remove wrong debit and give correct credit. Narration: "By errors in posting ₹500".

(d) Furniture purchase mistakenly in Purchases Account - debit Furniture (or Furniture Account) and credit Purchases by ₹1,000.

(e) Discount ₹15 received from Red & Black should have been entered in discount column of Cash Book, which would have credited Discount Account and debited Red & Black; correct by appropriate entries.

(f) In this case the customer's account is correct; Discount Account has been debited ₹18 short. Debit Discount Account by ₹18 with narration "To omission of entry in the Cash Book ₹18."

If a Suspense Account is opened:

Notes:

(i) Opening balance in the Suspense Account equals the difference in the trial balance.

(ii) If a question does not state whether a Suspense Account is opened, state your assumption and proceed accordingly.

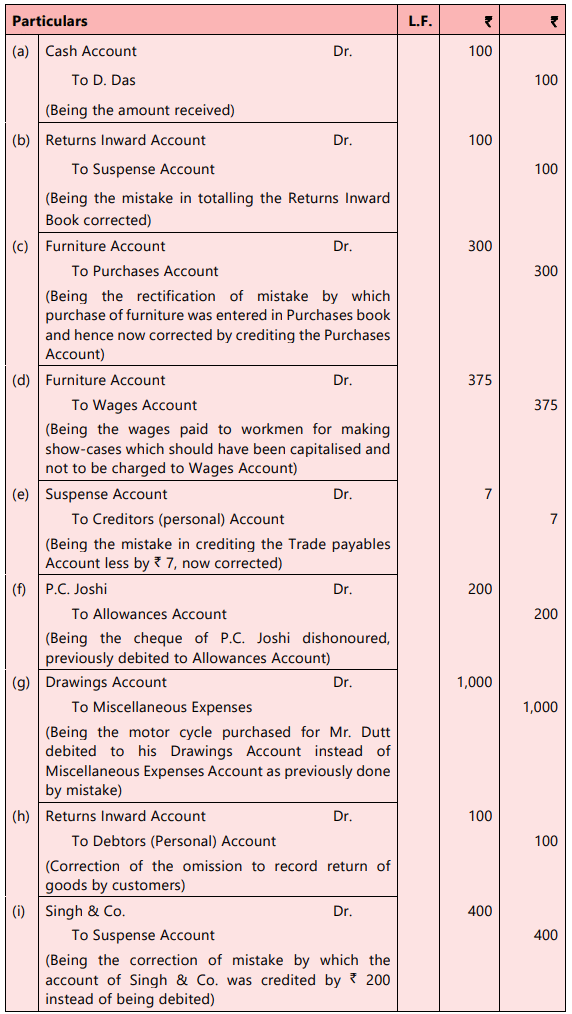

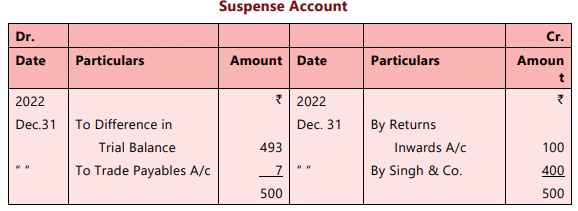

ILLUSTRATION 5

Correct the following errors found in Mr Dutt. The Trial Balance was out by ₹493 excess credit. The difference thus has been posted to a Suspense Account.

(a) An amount of ₹100 was received from D. Das on 31st December, 2022 but has been omitted to enter in the Cash Book.

(b) The total of Returns Inward Book for December has been cast short by ₹100.

(c) The purchase of an office table costing ₹300 has been passed through the Purchases Day Book.

(d) ₹375 paid for Wages to workmen for making show-cases had been charged to "Wages Account".

(e) A purchase of ₹67 had been posted to the trade payables' account as ₹60.

(f) A cheque for ₹200 received from P. C. Joshi had been dishonoured and was passed to the debit of "Allowances Account".

(g) ₹1,000 paid for the purchase of a motor cycle for Mr. Dutt for his personal use had been charged to "Miscellaneous Expenses Account".

(h) Goods amounting to ₹100 had been returned by customer and were taken into inventory, but no entry was made into the books.

(i) A sale of ₹200 to Singh & Co. was wrongly credited to their account. Entry was correctly made in sales book.

SOLUTION

ILLUSTRATION 6

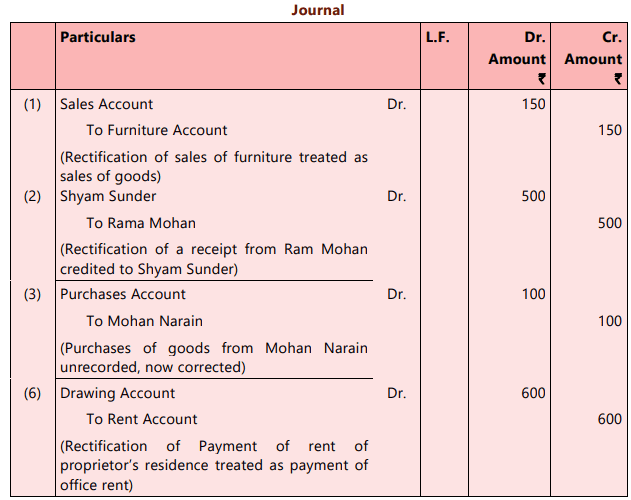

The following errors, affecting the account for the year 2022 were detected in the books of Jain Brothers, Delhi:

(1) Sale of old Furniture ₹150 treated as sale of goods.

(2) Receipt of ₹500 from Ram Mohan credited to Shyam Sunder.

(3) Goods worth ₹100 bought from Mohan Narain remained unrecorded.

(4) A return of ₹120 from Mukesh posted to his debit.

(5) A return of ₹90 to Shyam Sunder posted as ₹9 in his account.

(6) Rent of proprietor's residence ₹600 debited to Rent Account.

(7) A payment of ₹215 to Mohammad Sadiq posted to his credit as ₹125.

(8) Sales Book cast short by ₹900.

(9) The total of Bills Receivable Book ₹1,500 left unposted.

Pass the necessary rectifying entries and show how the trial balance would be affected by the errors.

SOLUTION

N.B. : For items 4, 5, 7, 8, 9 no journal entry can be passed as they affect a single account. Corrections are made by adjusting the affected account balances. The corrections are:

(4) Credit Mukesh's Account with ₹240.

(5) Debit the account of Shyam Sunder by ₹81.

(7) Debit the account of Mohammad Sadiq by ₹340.

(8) Credit Sales Account by ₹900.

(9) Debit Bills Receivable Account with ₹1,500.

Effect of the Errors on Trial Balance

1. No effect

2. No effect

3. No effect

4. Trial Balance credit total short by ₹240.

5. Trial Balance debit total short by ₹81.

6. No effect

7. Trial Balance debit total short by ₹340.

8. Trial Balance credit total short by ₹900.

9. Trial Balance debit total short by ₹1,500.

ILLUSTRATION 7

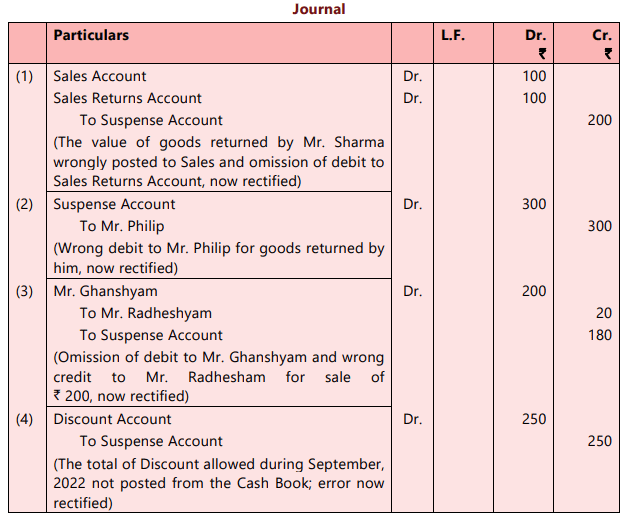

Write out the Journal Entries to rectify the following errors, using a Suspense Account.

(1) Goods of the value of ₹100 returned by Mr. Sharma were entered in the Sales Day Book and posted therefrom to the credit of his account;

(2) An amount of ₹150 entered in the Sales Returns Book, has been posted to the debit of Mr. Philip, who returned the goods;

(3) A sale of ₹200 made to Mr. Ghanshyam was correctly entered in the Sales Day Book but wrongly posted to the debit of Mr. Radheshyam as ₹20; and

(4) The total of "Discount Allowed" column in the Cash Book for the month of September, 2022 amounting to ₹250 was not posted.

SOLUTION

Correction in the Next Accounting Period

- Rectification is ideally done before closing books for the year. If errors are found in the following year, corrections can be made, but care is needed so the current-year profit is not distorted.

- Carrying forward the Suspense Account balance or transferring it to the Capital Account is possible if not rectified within the year, but not desirable where it distorts profit or balances.

Prior Period Items and Avoiding Profit Misrepresentation

- Corrections affecting prior periods that are material should be shown as Prior Period Items (or adjustments in a Profit and Loss Adjustment Account) rather than altering current period nominal accounts directly.

- Prior Period Items are material incomes/expenses arising from errors/omissions of prior periods and should be disclosed separately in the current period's statement of profit and loss.

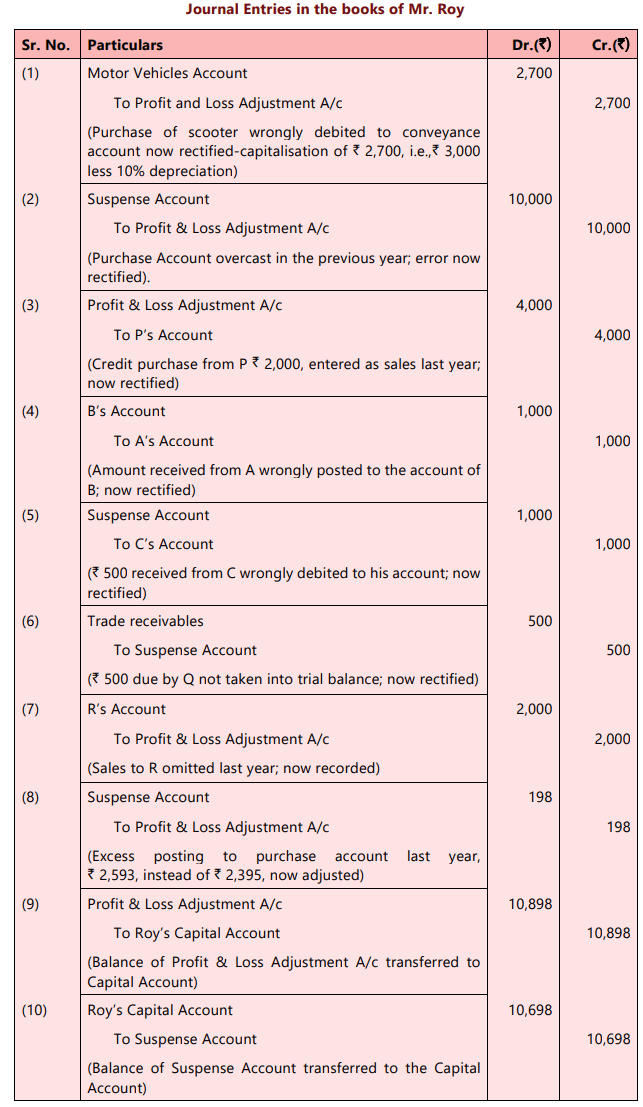

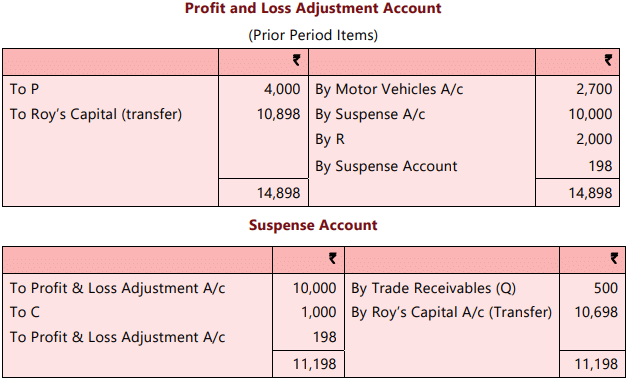

ILLUSTRATION 8

Mr Roy was unable to agree on the Trial Balance last year and wrote off the difference to the Profit and Loss Account of that year. Next Year, he appointed a Chartered Accountant who examined the old books and found the following mistakes:

(1) Purchase of a scooter was debited to the Conveyance Account ₹3,000.

(2) The purchase account was overcast by ₹10,000.

(3) A credit purchase of goods from Mr. P for ₹2,000 was entered as a sale.

(4) Receipt of cash from Mr. A was posted to the account of Mr. B ₹1,000.

(5) Receipt of cash from Mr. C was posted to the debit of his account, ₹500.

(6) ₹500 due by Mr. Q was omitted to be taken to the trial balance.

(7) Sale of goods to Mr R for ₹2,000 was omitted to be recorded.

(8) The amount of ₹2,395 of purchase was wrongly posted as ₹2,593.

Mr Roy used 10% depreciation on vehicles. Suggest the necessary rectification entries.

SOLUTION

Note : Entries No. (2) and (8) may even be omitted; but this is not advocated.

Summary

- Classify errors by type and stage to determine the correction method.

- Rectify errors by appropriate journal or adjustment entries - never by overwriting.

- Use the Suspense Account only as a temporary measure to make the trial balance agree; locate and clear errors as soon as possible.

- When correcting in a later period, treat material prior-period corrections as Prior Period Items to avoid distorting current profits.

FAQs on Chapter Notes- Unit 6: Rectification of Errors

| 1. What are the stages of errors in accounting? |  |

| 2. What are the broad categories of errors in accounting? | |

| 3. How can errors be identified in a trial balance? | |

| 4. What is the rectification of errors in accounting? | |

| 5. What is meant by correction in the next accounting period? | |