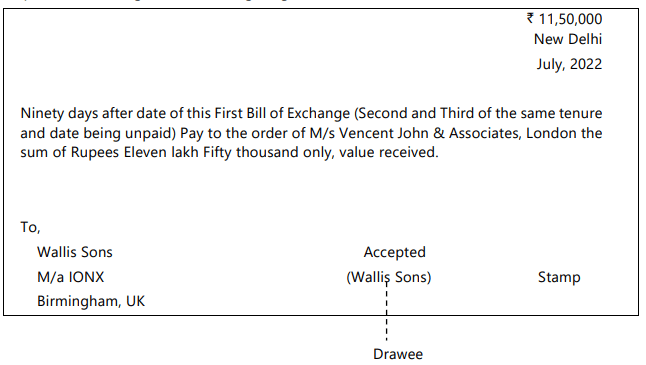

Bill of Exchange (simple meaning):

- A written order by one person (the drawer) telling another person (the drawee) to pay a fixed amount to someone (the payee) or the bearer.

- The drawee must write "accepted" and sign it for it to become a valid bill.

- Example: A orders B to pay ₹50,000 after 3 months. B writes "accepted" and signs - this becomes a bill of exchange.

CA Foundation Exam > CA Foundation Notes > Accounting > Chapter Notes: Bills of Exchange and Promissory Notes

Chapter Notes: Bills of Exchange and Promissory Notes

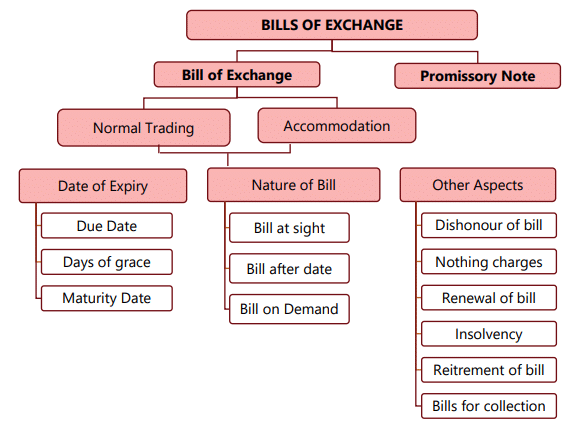

Chapter Overview

Bills of Exchange

- When a seller gives goods or services on credit, they may ask the buyer for a written promise to pay later.

- This written document can also be used to get money from a bank or be given to someone else.

- These documents, when written in the correct format and properly stamped, are important credit instruments like Bills of Exchange and Promissory Notes.

Characteristics of a Bill of Exchange

- Writing: The bill must be in writing.

- Date: It should bear the date on which it is drawn.

- Order to Pay: It must contain an order to pay a specified sum of money.

- Unconditional: The order to pay must be unconditional.

- Payee: The sum must be payable to a specified person, their order, or to the bearer.

- Acceptance: The drawee must accept the draft for it to become an accepted bill.

- Stamping: The bill should be properly stamped as per law, except in the case of bills payable on demand in some jurisdictions.

- Legal Currency: Payment must be in the legal currency of the country where the instrument is payable.

Parties Involved

- Drawer: The party who makes the order (draws the bill).

- Acceptor / Drawee: The party on whom the bill is drawn and who accepts the order to pay.

- Payee: The party to whom the amount is payable. The drawer and the payee may be the same person.

Endorsement and Liability

- Endorsement: A bill of exchange can be transferred to another person by endorsement, similar to the endorsement of a cheque.

- Primary Liability: The acceptor (drawee who has accepted) bears the primary liability to pay the bill on maturity. If the acceptor fails to pay, the holder may recover the amount from previous endorsers, the drawer or other parties liable on the instrument according to negotiable instruments law.

Foreign Bills of Exchange

- Definition: A Foreign Bill of Exchange is one drawn in one country and payable in another.

- Triplicate: Foreign bills are often prepared in triplicate so that at least one copy reaches the intended party if others are lost in transit.

- Payment: Payment made on one copy renders the other copies void.

- Legal Provision: Under negotiable instruments legislation, instruments not classified as inland instruments are deemed foreign instruments.

Examples of Foreign Bills of Exchange:

1. A bill drawn in India on a person residing outside India and made payable outside India.

2. A bill drawn outside India on a person residing outside India.

3. A bill drawn outside India and made payable in India.

4. A bill drawn outside India and made payable outside India.

MULTIPLE CHOICE QUESTIONTry yourself: Which of the following is a characteristic of a Bill of Exchange?

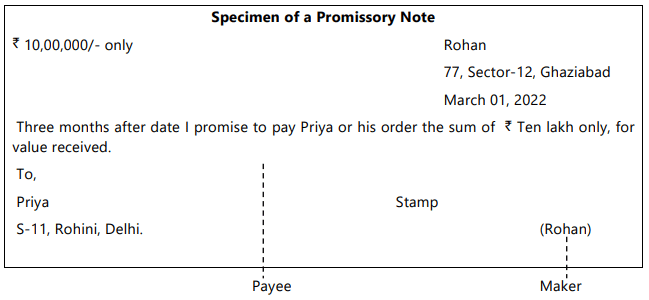

Promissory Notes

- A Promissory Note is a written financial instrument (distinct from currency), containing an unconditional promise by one person (the maker), signed by him, to pay a certain sum of money to a specified person or to his order.

- Under certain central bank regulations (for example, Section 31(2) of the Reserve Bank of India Act), promissory notes cannot be made payable to bearer.

Characteristics of a Promissory Note

1. Written Document: A promissory note must be in writing.

2. Clear Promise: It must contain a clear promise to pay; mere acknowledgement of debt is insufficient.

3. Unconditional Promise: The promise to pay must be unconditional; statements such as "I promise to pay ₹50,000 as soon as I can" are not unconditional.

4. Signature: The maker must sign the promissory note.

5. Certain Maker: The maker must be clearly identifiable.

6. Certain Payee: The payee must be a certain person.

7. Certain Amount: The sum payable must be definite; vague phrases like "plus all fines" make the amount uncertain.

8. Legal Currency: Payment must be in the legal currency of the country.

9. Non-Bearer: Promissory notes are generally not payable to bearer (subject to local law).

10. Proper Stamping: The instrument must be properly stamped where applicable.

11. No Acceptance Required: A promissory note does not require acceptance by the payee.

Specimen of a Promissory Note:

MULTIPLE CHOICE QUESTIONTry yourself: Which of the following is NOT a characteristic of a promissory note?

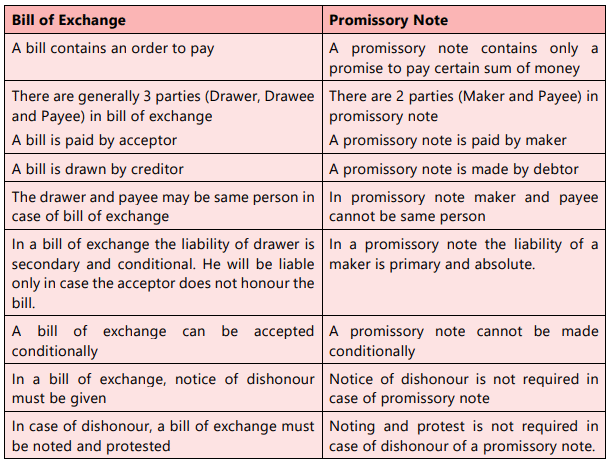

Differences - Bill of Exchange and Promissory Note

Record of Bills of Exchange and Promissory Notes

- Promissory notes and bills of exchange are used in commercial transactions to document credit and payment obligations.

- When a firm receives a promissory note or an accepted bill of exchange, it records the instrument as an asset under Bills Receivable.

- When a firm issues a promissory note or accepts a bill of exchange, it records the instrument as a liability under Bills Payable.

Entries in the Books of the Party Receiving Promissory Notes or Bills

- When a party receives a bill (either a promissory note or an accepted bill of exchange), the usual journal entry is:

- Bills Receivable Account - Debit

- To Drawee/Maker - Credit

Scenario 1: A accepts a bill from B.

In the books of B:

Bills Receivable Account - Debit

To A

Scenario 2: B receives acceptance from A.

In the books of B:

Bills Receivable Account - Debit

To A

Options for the Bill Receiver

- Holding the Bill: The receiver can keep the bill until maturity. No further entries are required until maturity.

- Endorsing the Bill: The receiver may endorse the bill in favour of another party (for example, Z). The entry is: Z (Debit) To Bills Receivable Account (Credit).

- Discounting the Bill with a Bank:The receiver may discount the bill with a bank. The bank deducts a discount fee and pays the balance.

- Typical entries are:

Bank Account - Debited with the amount received.

Discount Account - Debited with the discount amount (expense).

To Bills Receivable Account - Credited.

Entries on Maturity Date

1. If the Bill is Paid (Honoured)

- If the Bill was Kept: The holder receives payment and records:

Bank Account - Debit

To Bills Receivable Account - Credit - If the Bill was Endorsed or Discounted: The original holder makes no entry on payment; the endorsee or bank (who held/discounted the bill) receives the payment and records it in their books.

2. If the Bill is Dishonoured

- If the Bill was Kept:

Drawee/Maker Account - Debit

To Bill's Receivable Account - Credit - If the Bill was Endorsed:

Drawee/Maker Account - Debit

To Creditor Account - Credit - If the Bill was Discounted:

Drawee/Maker Account - Debit

To Bank Account - Credit

Summary

- The initial holder of the bill is responsible for pursuing payment in case of dishonour.

- The credit entry on dishonour varies depending on whether the bill was retained, endorsed, or discounted.

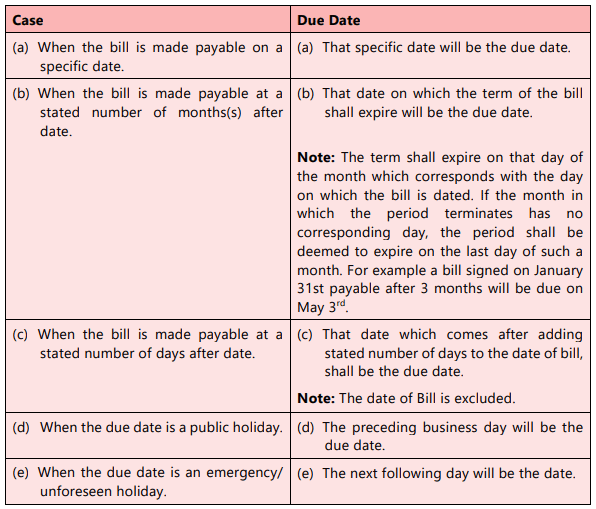

Term of a Bill of Exchange

- Duration: The term of a bill varies and is commonly within 90 days from the date the bill is drawn, unless otherwise stated.

- Bill Drawn After Sight: When a bill is drawn payable a specified period after sight, the term commences from the date of acceptance or the date of sighting.

- Bill Drawn After Date: When a bill is drawn payable after date, the term begins from the date the bill is drawn.

Expiry / Due Date of a Bill

The Expiry / Due Date is the day on which the bill's term ends; it is the date on which the instrument becomes payable (subject to the addition of days of grace where applicable).

Days of Grace

- Instruments payable on a specific date, such as promissory notes or bills, commonly allow three days of grace. These days are added to the due date to compute the date of maturity (except for instruments payable on demand).

- If the due date falls on a holiday or non-business day, presentation for payment can be made on the next business day without penalty because of the days of grace.

MULTIPLE CHOICE QUESTIONTry yourself: What is the term of a bill of exchange usually within from the date it is issued?

Date of Maturity of Bill

- Date of Maturity: The maturity date of a bill is found by adding three days of grace to its due/expiry date (where days of grace apply).

- Definition: The maturity of a promissory note or bill of exchange is the date on which it is due for payment; typically the third day after it is expressed to be payable, unless payable on demand.

- Exceptions: Instruments payable on demand (at sight, on presentment) mature on presentation and do not receive days of grace.

- On Demand / At Sight / On Presentment: An instrument so expressed is payable immediately upon demand or presentment.

Bill at Sight

A Bill at Sight is payable on demand because no specific time for payment is stated. Examples:

- Cheques are always payable on demand.

- Promissory notes and bills of exchange are payable on demand when they lack a specified time or are expressly stated to be payable on demand, at sight, or on presentment.

Notes:

(i) "At sight" and "presentment" mean "on demand".

(ii) An instrument payable on demand can be presented for payment at any time.

(iii) Days of grace are not added when calculating maturity for instruments payable on demand.

Bill After Date

A Bill after Date is a time instrument where the time for payment is specified. A promissory note or bill of exchange is a time instrument when it is payable:

- after a specified period,

- on a specified day,

- after sight, or

- upon the occurrence of an event that is certain to happen.

Notes:

(i) The expression "after sight" means:

- in a promissory note - after presentment for sight;

- in a bill of exchange - after acceptance or noting/protest for non-acceptance.

(ii) A cheque cannot be a time instrument because it is always payable on demand; although a cheque can be post-dated, a cheque normally has a validity (e.g., 90 days) after which banks will consider it stale.

How to Calculate the Date of a Bill

Note: The term of a bill after sight commences from the date of acceptance of the bill whereas the term of a bill after date commences from the date of drawing of the bill.

Noting Charges

Noting charges are fees charged by a Notary Public when a bill is presented and dishonoured (or when it is presented for notice). The Notary Public notes the fact and the reasons for dishonour and returns the bill to the client. Noting charges are recoverable from the party responsible for the dishonour.

Example with Noting Charges

If X receives a bill from Y for ₹1,000 and the bill is dishonoured, noting charges of ₹10 are paid, the entries are:

- Dr. Y: ₹1,010 - to record the total amount due from Y (including noting charges charged to Y).

- Cr. Bills Receivable Account: ₹1,000 - to cancel the bill receivable.

- Cr. Bank A/c: ₹10 - to record the payment of noting charges to the notary.

When X endorses the bill in favour of Z:

- Dr. Y: ₹1,010 - Z claims ₹1,010 from X.

- Cr. Z: ₹1,010 - to record the amount payable to Z.

If the Bill has been Discounted with a Bank:

- Dr. Y: ₹1,010 - to record the amount due from Y (debtor).

- Cr. Bank A/c: ₹1,010 - to record the amount to be paid to the bank (where the bill was discounted).

MULTIPLE CHOICE QUESTIONTry yourself: What is the date of maturity of a bill after sight if it is accepted on 5th May?

Renewal of Bill

- When an acceptor cannot pay on the due date, the parties may agree to renew the bill by drawing a new bill for an extended period. Interest for the extended period is usually paid at the time of renewal.

- The old bill is cancelled and the new bill is drawn; entries for cancellation are made in the same manner as for dishonour (if the old bill is treated like dishonoured and replaced).

- The entries for the new bill are recorded as receipt of a fresh bill and are identical to entries when a bill is originally received.

The amount of the new bill may represent different cases:

- If the drawee pays nothing at renewal, the new bill equals the original bill amount plus interest for the extended period.

- If the drawee pays the interest at renewal, the new bill equals the original bill amount.

- If the drawee makes part payment of the original amount and/or interest, the new bill equals the unpaid portion of the total (original plus interest).

Retirement of Bills of Exchange

- Definition: Retirement of a bill occurs when the acceptor pays the amount due before the maturity date.

- Process: The acceptor, having funds, approaches the payee to make early payment.

- Rebate/Discount: The payee may allow a rebate (discount) for early payment. The rebate is income for the acceptor and an expense for the payee.

- Example: If a bill of ₹10,000 due in 30 days is paid in 20 days with a ₹500 rebate, the acceptor saves ₹500, and the payee incurs ₹500 expense.

Rebate on Premature Payment

- Concept: When the acceptor retires the bill before due date, he may be entitled to a rebate for early payment.

- Income and Expense: The rebate is income for the acceptor (reduction in cash paid) and an expense for the payee (reduction in cash received).

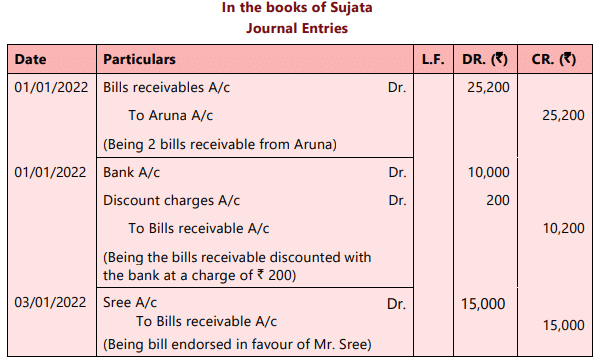

ILLUSTRATION 1

Ms. Sujata received two bills from Ms. Aruna dated 1st January 2022 for 2 months. The first bill is for 10,200 and the second bill is for ₹15,000. The first bill is discounted immediately with the bank for ₹10,000 and the second bill was endorsed in favour of Mr. Sree on 3rd January 2022. Pass the necessary journal entries in the books of Ms. Sujata.

SOLUTION

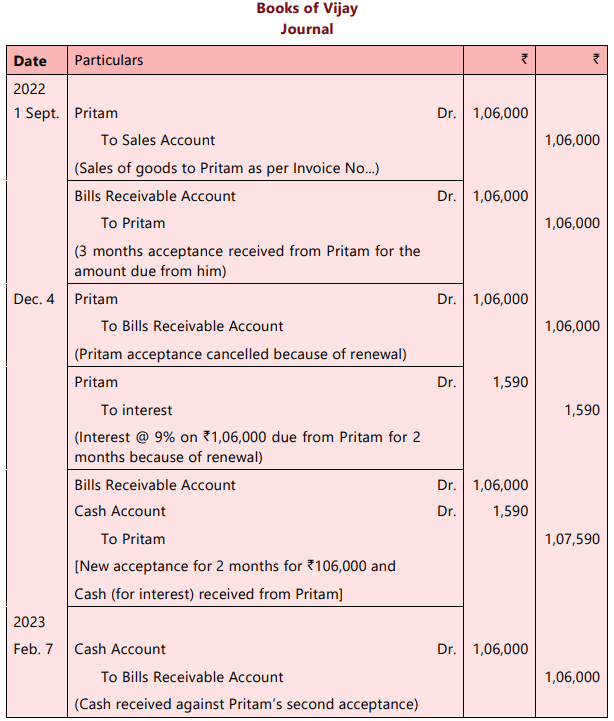

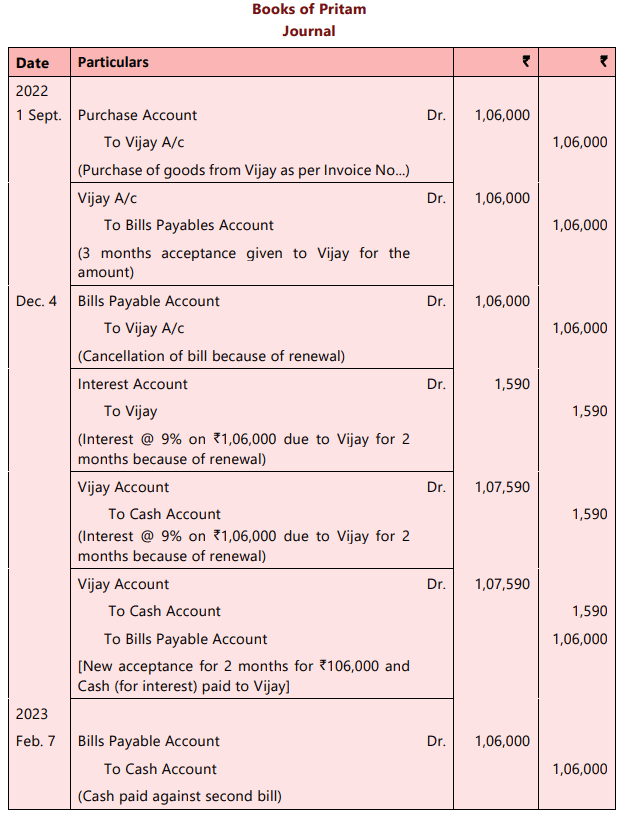

ILLUSTRATION 2

Vijay sold goods to Pritam on 1st September, 2022 for ₹1,06,000. Pritam immediately accepted a three months bill. On due date Pritam requested that the bill be renewed for a fresh period of two months. Vijay agrees provided interest at 9% p.a. was paid immediately in cash. To this Pritam was agreeable. The second bill was met on due date. Give Journal entries in the books of Vijay and Pritam.

SOLUTION

ILLUSTRATION 3

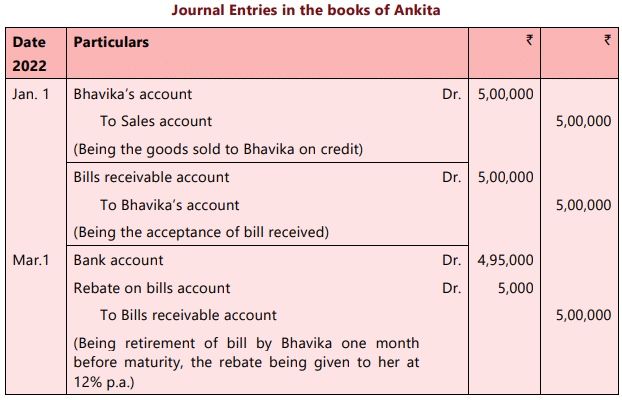

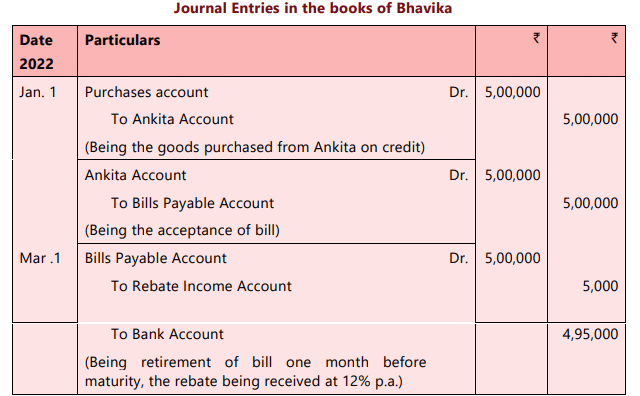

On 1st January 2022, Ankita sells goods for ₹5,00,000 to Bhavika and draws a bill at three months for the amount. Bhavika accepts it and returns it to Ankita. On 1st March, 2022, Bhavika retires her acceptance under rebate of 12% per annum. Record these transactions in the journals of Ankita and Bhavika.

SOLUTION

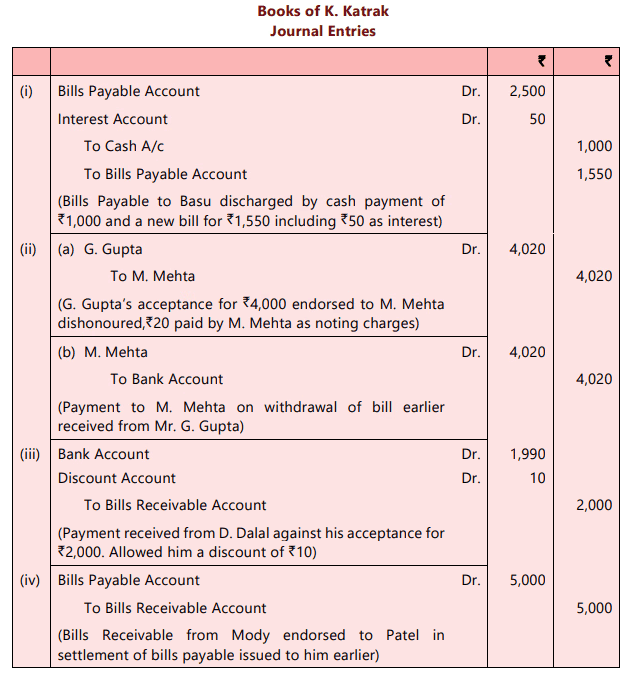

ILLUSTRATION 4

Journalise the following transactions in K. Katrak's books:

(i) Katrak's acceptance to Basu for ₹2,500 discharged by a cash payment of ₹1,000 and a new bill for the balance plus ₹50 for interest.

(ii) G. Gupta's acceptance for ₹4,000 which was endorsed by Katrak to M. Mehta was dishonoured. Mehta paid ₹20 noting charges. Bill withdrawn against cheque.

(iii) D. Dalal retires a bill for ₹2,000 drawn on him by Katrak for ₹10 discount.

(iv) Katrak's acceptance to Patel for ₹5,000 was discharged by endorsing Mody's acceptance to Katrak for a similar amount.

SOLUTION

ILLUSTRATION 5

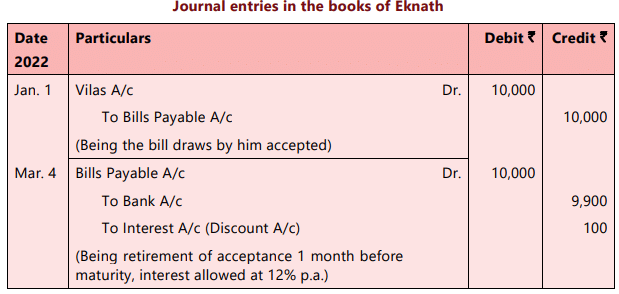

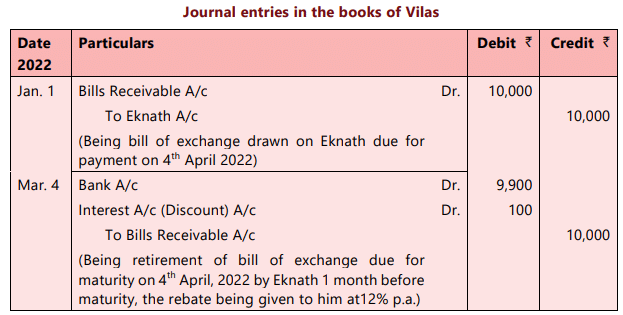

On 1st January, 2022, Vilas draws a bill of exchange for ₹10,000 due for payment after 3 months on Eknath. Eknath accepts this bill of exchange. On 4th March, 2022 Eknath retires the bill of exchange at a discount of 12% p.a. You are asked to show the journal entries in the books of Eknath.

SOLUTION

ILLUSTRATION 6

On 1st January, 2022, Vilas draws a Bill of Exchange for ₹10,000 due for payment after 3 months on Eknath. Eknath accepts this bill of exchange. On 4th March, 2022, Eknath retires the bill of exchange at a discount of 12% p.a. You are asked to show the journal entries in the books of Vilas.

SOLUTION

Insolvency

- Insolvency is a state where a person cannot meet their financial obligations and is unable to pay liabilities. Accepted bills and other debts will normally be dishonoured in such circumstances.

- When the insolvency of a drawee becomes known, the holder should pass the appropriate dishonour entry in the books.

- Subsequently, if any amount is recovered from the insolvent's estate, the cash received is debited and the debtor's personal account is credited. A portion may remain irrecoverable and must be written off as bad debt after preparing the insolvent's account.

- In the books of the drawer/drawee, any deficiency (amount not ultimately paid due to insolvency) should be credited to a Deficiency Account.

ILLUSTRATION 7

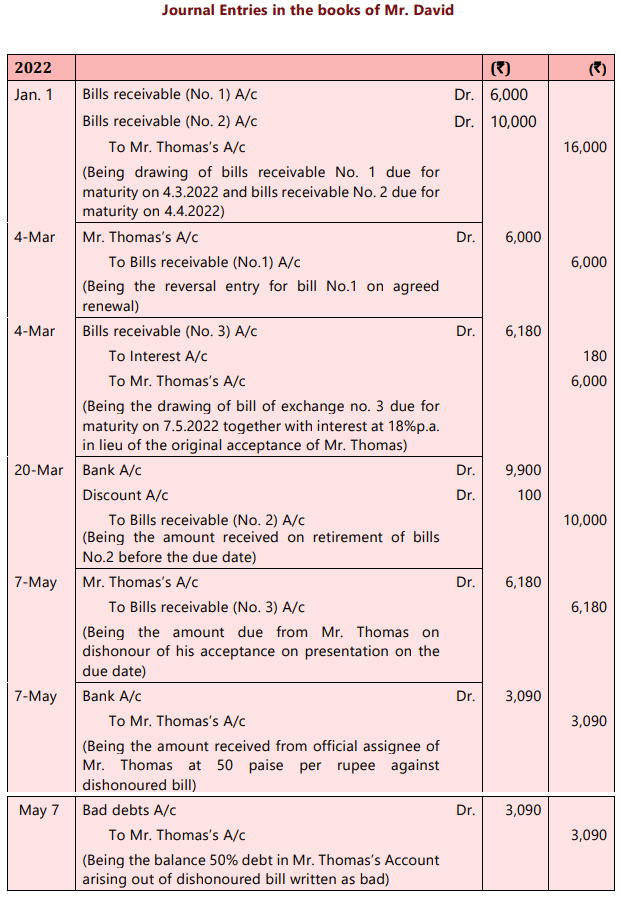

Mr David draws two bills of exchange on 1.1.2022 for ₹6,000 and ₹10,000. The bill for ₹6,000 is for two months while the bill for ₹10,000 is for three months. These bills are accepted by Mr. Thomas. On 4.3.2022, Mr. Thomas requests Mr. David to renew the first bill with interest at 18% p.a. for a period of two months. Mr. David agrees. On 20.3.2022, Mr. Thomas retires the acceptance for ₹10,000, the interest rebate (discount) being ₹100. Before the due date of the renewed bill, Mr Thomas became insolvent, and only 50 paise in the rupee could be recovered from his estate. Give the journal entries in the books of Mr. David.

SOLUTION

ILLUSTRATION 8

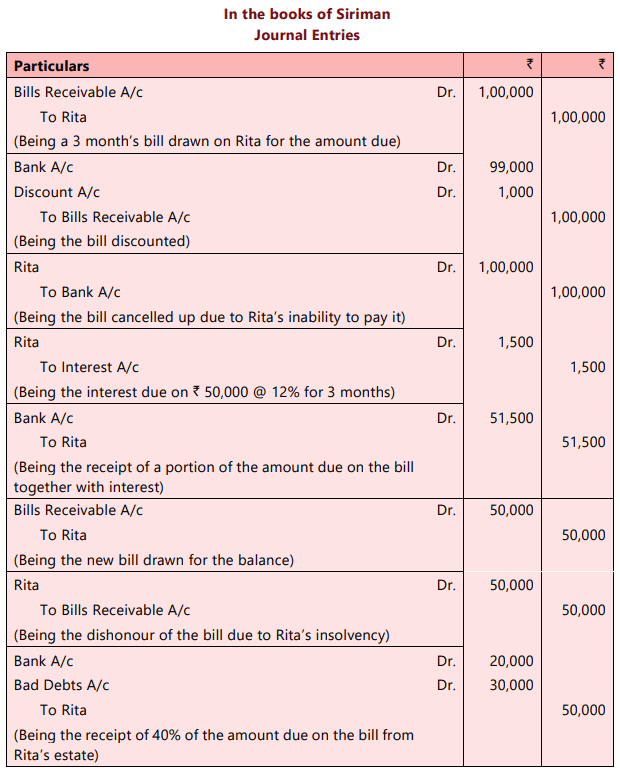

Rita owed ₹1,00,000 to Siriman. On 1st October, 2021, Rita accepted a bill drawn by Siriman for the amount at 3 months. Siriman got the bill discounted with his bank for ₹99,000 on 3rd October, 2021. Before the due date, Rita approached Siriman for renewal of the bill. Siriman agreed on the conditions that ₹50,000 be paid immediately together with interest on the remaining amount at 12% per annum for 3 months and for the balance, Rita should accept a new bill at three months. These arrangements were carried out. But afterwards, Rita became insolvent and 40% of the amount could be recovered from his estate. Pass journal entries (with narration) in the books of Siriman.

SOLUTION

MULTIPLE CHOICE QUESTIONTry yourself: What happens when the acceptor of a bill of exchange is unable to pay the amount on the due date?

Accommodation Bills

An Accommodation Bill is an instrument used to raise funds where the acceptor lends his name (by accepting the bill) to the drawer so that the drawer can obtain cash (for example, by discounting the bill with a bank). No genuine trade transaction may be involved; it is primarily a means of obtaining finance.

Example: If the Boss needs funds for three months, he may persuade his friend Kapoor to accept his draft. Boss takes that acceptance to a bank and gets it discounted for cash. On maturity, Boss repays Kapoor, who then meets the bill.

- If both parties need finance, either may accept a bill, discount it and share the proceeds and discount charges as mutually agreed.

- Accommodation bills are recorded in the books of the drawer and acceptor similarly to ordinary bills, with additional entries to record remittances and sharing of discount/charges.

ILLUSTRATION 9

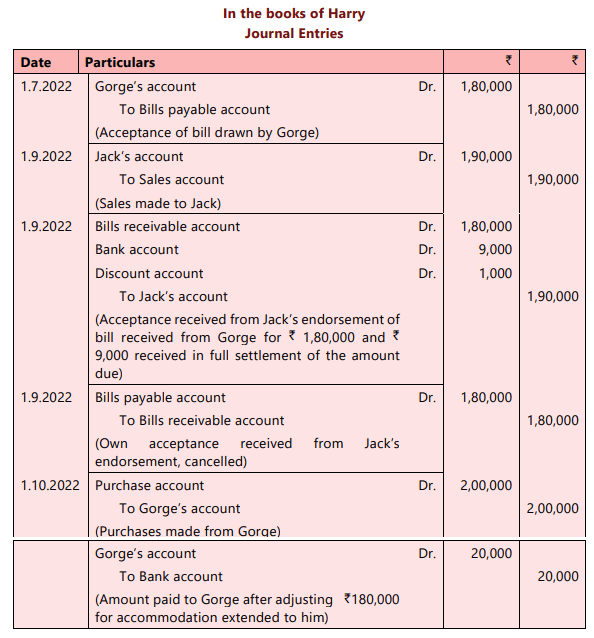

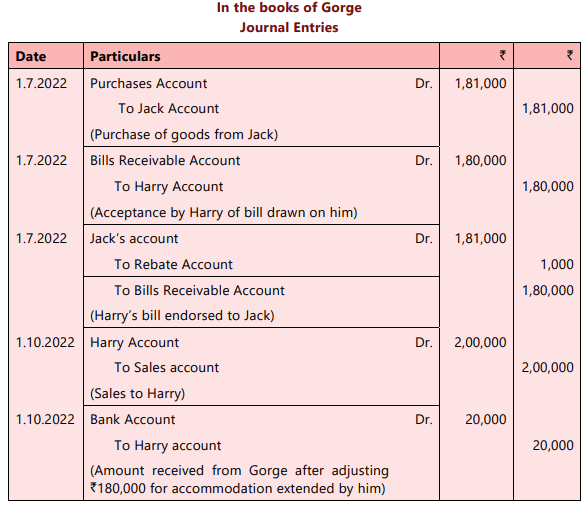

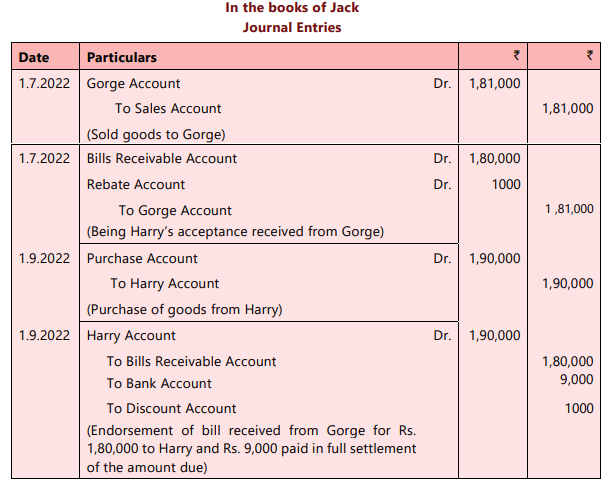

On 1st July, 2022 Gorge drew a bill for ₹1,80,000 for 3 months on Harry for mutual accommodation. Harry accepted the bill of exchange. Gorge had purchased goods worth ₹1,81,000 from Jack on the same date. Gorge endorsed Harry's acceptance to Jack in full settlement. On 1st September, 2022, Jack purchased goods worth ₹1,90,000 from Harry. Jack endorsed the bill of exchange received from Gorge to Harry and paid ₹9,000 in full settlement of the amount due to Harry. On 1st October, 2022, Harry purchased goods worth ₹2,00,000 from Gorge. Harry paid the amount due to Gorge by cheque. Give the necessary Journal Entries in the books of Harry, Gorge and Jack.

SOLUTION

ILLUSTRATION 10

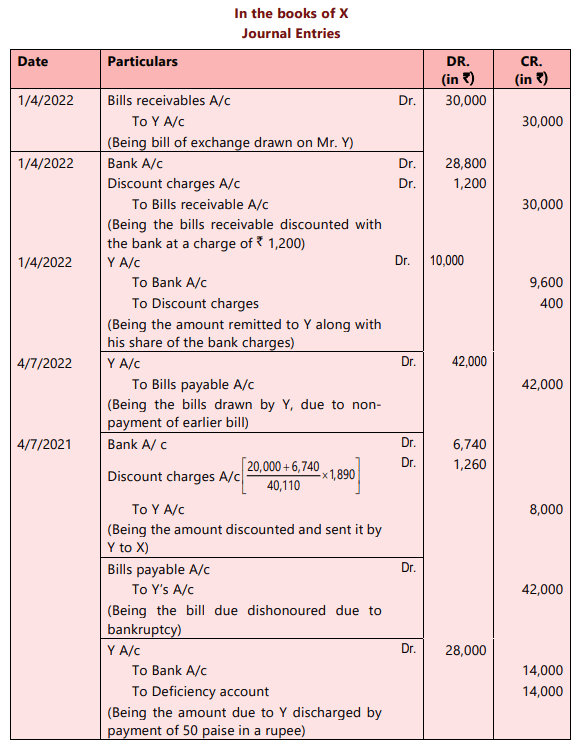

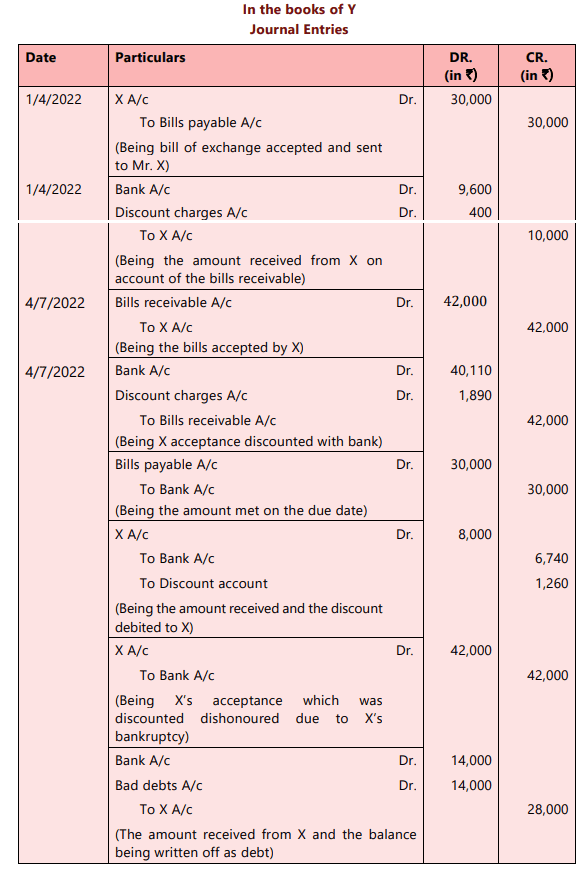

X draws on Y a bill of exchange for ₹30,000 on 1st April, 2022 for 3 months. Y accepts the bill and sends it to X who gets it discounted for ₹28,800. X immediately remits ₹9,600 to Y. On the due date, X, being unable to remit the amount due, accepts a bill for ₹42,000 for three months which is discounted by Y for ₹40,110. Y sends 6,740 to X. Before the maturity of the bill, X becomes bankrupt; his estate pays fifty paise in the rupee. Give the journal entries in the books of X and Y.

SOLUTION

ILLUSTRATION 11

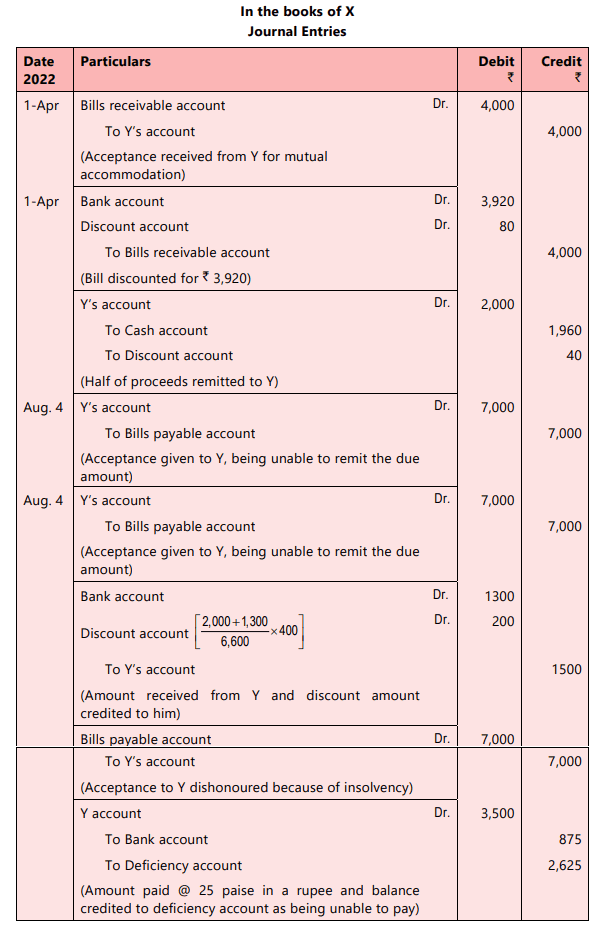

For the mutual accommodation of X and Y on 1st April, 2022, X drew a four months' bill on Y for ₹4,000. Y returned the bill after acceptance on the same date. X discounts the bill from his bankers @ 6% p.a. and remits 50% of the proceeds to Y. On due date, X is unable to send the amount due and therefore Y draws a bill for ₹7,000, which is duly accepted by X. Y discounts the bill for ₹6,600 and sends ₹1,300 to X. Before the bill is due X becomes insolvent. Later 25 paise in a rupee is received from his estate. Record Journal entries in the books of X.

SOLUTION

Bills of Collection

When a holder sends a bill to his bank with instructions to collect payment on the due date, it is termed Bill sent for Collection. The bank only credits the client when the amount is actually collected. This process differs from discounting where the bank advances funds immediately (less discount).

Recording Bills for Collection

When a bill is sent for collection, a record entry is usually passed in the books as follows:

Bills for Collection Account - Debit

To Bills Receivable Account

Realising the Amount

When the bank realises the amount and remits it to the client, the entry is:

Bank Account - Debit

To Bills for Collection Account

Handling Dishonoured Bills

If the bill sent for collection is dishonoured, the usual entry is:

Drawee's Account - Debit (the person from whom the bill was expected)

To Bills for Collection Account

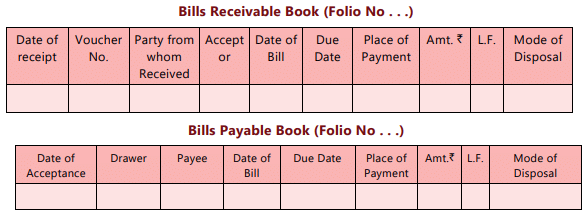

Bills Receivable and Bills Payable Books

- Organisations that transact many bills maintain separate Day Books titled Bills Receivable Book and Bills Payable Book to record bill details chronologically.

- Transactions are first entered in Day Books; totals and particulars are posted periodically to individual debtor/creditor accounts and to Bills Receivable and Bills Payable control accounts.

- These books aid follow-up for outstanding bills, tracing dishonoured bills and identifying reasons for non-payment on maturity.

MULTIPLE CHOICE QUESTIONTry yourself: What is the purpose of sending a bill of exchange to the bank for collection?

The document Chapter Notes: Bills of Exchange and Promissory Notes is a part of the CA Foundation Course Accounting for CA Foundation.

All you need of CA Foundation at this link: CA Foundation

FAQs on Chapter Notes: Bills of Exchange and Promissory Notes

| 1. What is a bill of exchange and how does it work? |  |

Ans. A bill of exchange is a written financial instrument that contains an unconditional order from one party (the drawer) to another party (the drawee) to pay a specific sum of money to a third party (the payee) at a predetermined date. It serves as a payment mechanism and can be used in trade transactions. The drawer creates the bill, which the drawee must accept to make it effective.

| 2. What is a promissory note and how is it different from a bill of exchange? | |

Ans. A promissory note is a written promise made by one party (the maker) to pay a specified amount to another party (the payee) at a designated time. Unlike a bill of exchange, which involves three parties (drawer, drawee, and payee), a promissory note only involves two parties (maker and payee). The key difference lies in the nature of the obligation; a bill of exchange requires acceptance from the drawee, while a promissory note does not.

| 3. How do you calculate the maturity date of a bill of exchange? | |

Ans. The maturity date of a bill of exchange is determined based on the terms stated in the bill. If the bill is payable on demand, the maturity date is the date it is presented for payment. If it is payable at a fixed date, the maturity date is the stated date. For bills payable after a certain period (e.g., 30 days after sight), you add the specified number of days to the date of acceptance or to the date of the bill if it is payable at a fixed time.

| 4. What are noting charges in the context of bills of exchange? | |

Ans. Noting charges refer to the fees incurred when a bill of exchange is presented for payment but is dishonored (not paid). The bank or financial institution notes the dishonor, and this process includes recording the details of the dishonor on the bill. These charges are typically borne by the drawer of the bill and can vary depending on the bank's policies.

| 5. What is the process for renewing a bill of exchange? | |

Ans. Renewing a bill of exchange involves creating a new bill to replace an existing one that is due for payment. This typically occurs when the parties agree to extend the payment period. The new bill will state the new maturity date and may involve recalculating interest or additional charges. The original bill should be canceled upon renewal, and the new terms should be documented and accepted by all parties involved.

About this Document

4.61/5 Rating

Apr 19, 2026 Last updated

Related Exams

Document Description: Chapter Notes: Bills of Exchange and Promissory Notes for CA Foundation 2026 is part of Accounting for CA Foundation preparation. The notes and questions for Chapter Notes: Bills of Exchange and Promissory Notes have been prepared according to the CA Foundation exam syllabus. Information about Chapter Notes: Bills of Exchange and Promissory Notes covers topics like and Chapter Notes: Bills of Exchange and Promissory Notes Example, for CA Foundation 2026 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Chapter Notes: Bills of Exchange and Promissory Notes.

Introduction of Chapter Notes: Bills of Exchange and Promissory Notes in English is available as part of our Accounting for CA Foundation for CA Foundation & Chapter Notes: Bills of Exchange and Promissory Notes in Hindi for Accounting for CA Foundation course. Download more important topics related with notes, lectures and mock test series for CA Foundation Exam by signing up for free. CA Foundation: Chapter Notes: Bills of Exchange and Promissory Notes

Description

Chapter Notes: Bills of Exchange & Promissory Notes of Accounting with clear explanations of key concepts & important topics of the chapter, to help you underst& lessons better & revise quickly, & crack the CA Foundation exam.

Information about Chapter Notes: Bills of Exchange and Promissory Notes

In this doc you can find the meaning of Chapter Notes: Bills of Exchange and Promissory Notes defined & explained in the simplest way possible. Besides explaining types of Chapter Notes: Bills of Exchange and Promissory Notes theory, EduRev gives you an ample number of questions to practice Chapter Notes: Bills of Exchange and Promissory Notes tests, examples and also practice CA Foundation tests

Related Searches

Sample Paper, Previous Year Questions with Solutions, Extra Questions, MCQs, Exam, Chapter Notes: Bills of Exchange and Promissory Notes, Chapter Notes: Bills of Exchange and Promissory Notes, ppt, practice quizzes, mock tests for examination, past year papers, Semester Notes, Free, Objective type Questions, study material, video lectures, Viva Questions, Important questions, pdf , shortcuts and tricks, Summary, Chapter Notes: Bills of Exchange and Promissory Notes;