Definitions of Input Tax Credit

Input

What are Inputs Under GST?

- Inputs, as defined in the Goods and Services Tax (GST) framework, refer to the goods acquired by a business for use in its operations. According to Section 2(59) of the CGST Act, inputs are any goods, excluding capital goods, that are used or intended to be used by a supplier in the course or furtherance of business.

Key Characteristics of Inputs

- Tangible Property: Inputs are physical goods that can be touched and seen.

- Used in Business: These goods are employed in the day-to-day operations of a supplier's business.

- Excludes Capital Goods: Goods classified as capital goods, which are typically long-term assets, are not considered inputs.

Distinction Between Inputs and Capital Goods

- Inputs: The cost of inputs is usually charged to the profit and loss account as an expense.

- Capital Goods: The cost of capital goods is capitalized and depreciated over their useful life.

Examples of Inputs

- Raw Materials: Basic substances used in manufacturing processes, such as steel, plastic, or fabric.

- Packing Materials: Items used to package the final product, including cartons, boxes, and plastic bags.

- Consumable Supplies: Goods used up in the normal course of business, such as stationery, cleaning supplies, and office consumables.

- Spare Parts: Components used for repairing or maintaining machinery and equipment, like motors, belts, and filters.

Importance of Inputs in GST

- Input Tax Credit (ITC): Businesses can claim credit for the GST paid on inputs, which helps reduce their overall tax liability.

- Valuation of Output Supply: The cost of inputs is often considered when determining the value of the final product or service offered to customers.

- Record Keeping: It is essential for businesses to maintain accurate records of inputs to support ITC claims and comply with other GST requirements.

Input Service

Who is an Input Service Distributor (ISD) under GST?

- An Input Service Distributor (ISD) is a taxpayer who receives invoices for services used by its branches. The ISD distributes the Input Tax Credit (ITC) to these branches on a proportional basis by issuing ISD invoices. While the branches can have different GST Identification Numbers (GSTINs), they must share the same Permanent Account Number (PAN) as the ISD.

Let's understand with an example:

- Suppose the head office of M/s ABC Limited is located in Bangalore, with branches in Chennai, Mumbai, and Kolkata. The head office incurs an annual software maintenance expense on behalf of all its branches and receives the invoice for this service.

- Since the software is used by all branches, the input tax credit for the entire service cannot be claimed solely in Bangalore. Instead, it needs to be distributed among all three locations. In this scenario, the head office in Bangalore acts as the Input Service Distributor.

Situations where ISD is not applicable

- ISD cannot distribute the input tax credit in cases where ITC is paid on inputs and capital goods, such as raw materials and machinery purchases.

- ITC cannot be distributed to outsourced manufacturers or service providers.

Purpose of registering as ISD

- Registering as an Input Service Distributor (ISD) serves the purpose of streamlining the credit-taking process for businesses with a significant amount of common expenditure managed from a centralized location. This mechanism simplifies the distribution of input tax credit and enhances the seamless flow of credit under the Goods and Services Tax (GST) regime.

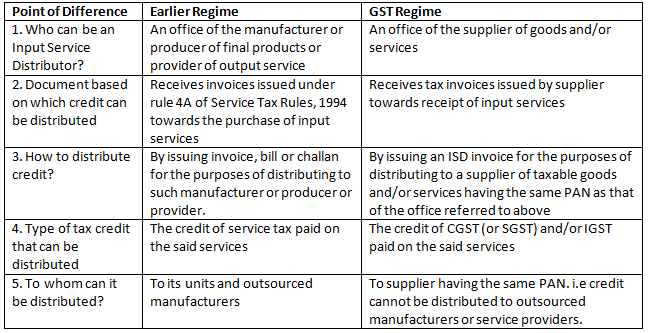

Insight on ISD under Earlier regime and GST regime

Thus, the key difference between the earlier regime and the GST regime regarding the ISD is that the distribution of credit is restricted to the office having the same PAN. This change is likely due to the shift of the taxable event from manufacture to supply, where the tax liability arises at the time of supply, ultimately paid by the ISD using the available input tax credit.

Conditions to be fulfilled by ISD

- Registration: Input Service Distributor must register as "ISD" in addition to their normal GST registration. During the registration process, they should specify their status as an ISD in the REG-01 form. This declaration is necessary for the ISD to distribute tax credits to recipients.

- Invoicing: The ISD can distribute tax credits to recipients by issuing an ISD invoice. This invoice serves as a record of the tax credit being distributed.

- Returns: The amount of tax credit distributed by the ISD should not exceed the tax credit available to them at the end of the month. This information must be filed in GSTR-6 by the 13th of the following month. The ISD can obtain information about their ITC from the GSTR-2B return.

- The recipients of the tax credit can view the distributed credits in GSTR-6A, which is auto-populated from the supplier's return. The recipient branches can claim these credits by declaring them in GSTR-3B. It's important to note that ISDs are not required to file annual returns in GSTR-9.

Distribution of Input Tax Credit

- The Input Tax Credit (ITC) available for distribution in a month must be distributed within the same month, and the details of this distribution should be reported in the GSTR-6 form.

- The tax credit resulting from payments made under the reverse charge mechanism as per sections 9(3) and 9(4) of the GST Act should also be distributed to the recipients by the Input Service Distributor (ISD).

- If a specific input service is used entirely by one recipient, the tax credit associated with that service can only be allocated to that recipient for their use, and not to other recipients.

- For input services used by multiple recipients, the tax credit should be allocated to all operational recipients for the year on a proportionate basis. This allocation should be done based on the ratio of their operations during the year.

Allocation of Tax Credit for Common Input Services by Input Service Distributor (ISD)

When input services are used commonly by multiple recipients, the tax credit available against these services can be allocated by the Input Service Distributor (ISD) to all operational recipients in a given year. The allocation is done on a proportionate basis using the following ratio:

Ratio: Turnover in the State/Union Territory of the recipient during the relevant period Aggregate of the turnover of all recipients

Recovery Procedure for Wrongful Distribution of Credit by ISD

- Inappropriate Distribution: The GST Act outlines certain scenarios that constitute inappropriate distribution of tax credit by the Input Service Distributor.

- Excess Credit Distribution: Credit distributed to all or any recipient in excess of the amount available for distribution is considered inappropriate.

- Inappropriate Ratio: Distributing credit in an inappropriate ratio to all or any recipient is deemed inappropriate.

- Excess Distribution: Distributing credit in excess to what a supplier is entitled to is also considered inappropriate.

- Recovery Process: In cases of inappropriate distribution, the excess credit shall be recovered from the recipient(s) along with interest. The provisions of 'Demand and Recovery' shall apply for effecting such recovery.

Capital Goods in GST

Capital goods in India, as per the Goods and Services Tax (GST) framework, refer to items that are used or intended for use in the course or furtherance of business and are recorded as capital assets in the taxpayer's financial accounts. This definition is outlined in Section 2(19) of the Central Goods and Services Tax (CGST) Act. Capital goods play a crucial role in determining eligibility for Input Tax Credit (ITC), as businesses can claim ITC based on their capital expenditure on these goods.

Eligibility for ITC on Capital Goods

- Registered GST Taxpayers: Only taxpayers registered under GST are eligible to claim ITC on capital goods.

- Business Use Requirement: Capital goods must be used exclusively for business purposes, including manufacturing or providing taxable services.

- Capitalization in Financial Records: The value of capital goods must be capitalized in the financial accounts of the business.

- Taxable Goods or Services: Capital goods should be used in the production of taxable goods or services. ITC is not available for items used to supply exempted goods or services.

Conditions and Restrictions for Claiming ITC on Capital Goods

- Exclusive Use for Taxable Supplies: ITC is allowed if capital goods are used exclusively for taxable supplies. For mixed-use (both taxable and exempt), ITC must be claimed proportionately.

- Depreciation on Tax Component: ITC is ineligible if the tax component is included in the depreciation claimed under the Income Tax Act.

- Blocked Credit Items: ITC cannot be claimed on capital goods intended for personal use or those used for constructing immovable property (except for plant and machinery).

- Time Limit for ITC Claims: ITC must be claimed by the due date of the September return following the financial year or by the date of filing the annual return, whichever is earlier.

- Reversal of ITC: If capital goods are subsequently used for exempt supplies or non-business activities, a proportionate reversal of ITC is required.

- Invoice Documentation Requirement: Valid tax invoices or appropriate documentation are essential to claim ITC on capital goods.

Examples of Capital Goods in GST

1. Weaving Machine in Textile Industry. A textile production company purchases a weaving machine for ₹20,00,000, with ₹3,60,000 (18%) GST.

- GST Treatment: The machine's cost, including GST, is capitalized in the company's accounts.

- ITC Eligibility: The business can claim ITC on ₹3,60,000 GST paid.

- Claiming ITC: The company must hold a valid tax invoice and submit its monthly GST return claiming the ITC.

2. Machinery in Manufacturing. A manufacturing unit buys machinery for ₹10,00,000 plus ₹1,80,000 (18%) GST.

- GST Treatment: The total cost is capitalized in the unit's accounts.

- ITC Eligibility: ITC on ₹1,80,000 GST is claimable.

- Claiming ITC:. valid invoice is required to claim ITC in monthly GST returns.

3. Computer Systems in IT Services. An IT services firm purchases computer systems for ₹5,00,000 plus ₹90,000 (18%) GST.

- GST Treatment: The cost is capitalized in the firm's accounts.

- ITC Eligibility: ITC on ₹90,000 GST is claimable.

- Claiming ITC:. valid invoice is needed to claim ITC in monthly returns.

4. Office Furniture in Corporate Sector. A corporate office buys furniture for ₹3,00,000 plus ₹54,000 (18%) GST.

- GST Treatment: The cost is capitalized in the office's accounts.

- ITC Eligibility: ITC on ₹54,000 GST is claimable.

- Claiming ITC:. valid invoice is required for ITC claims.

5. Printing Equipment in Publishing. A publishing company purchases printing equipment for ₹15,00,000 plus ₹2,70,000 (18%) GST.

- GST Treatment: The total cost is capitalized in the company's accounts.

- ITC Eligibility: ITC on ₹2,70,000 GST is claimable.

- Claiming ITC:. valid tax invoice is necessary for ITC claims.

Input Tax

Changes to Provisional ITC Claims from 2022

- Starting from January 1, 2022, provisional ITC claims are no longer permitted as per Section 16(2)(aa).

- This means that the ITC reported in GSTR-3B will reflect the actual ITC as per GSTR-2B, without the provisional 5% allowance.

- Regular matching of the purchase register or expense ledger with GSTR-2B has become essential.

- Before December 31, 2021, taxpayers could claim provisional ITC in GSTR-3B up to 5% of the ITC available in GSTR-2B, in addition to the ITC in GSTR-2B.

Conditions for Availing ITC

To avail Input Tax Credit (ITC), certain conditions must be met:

- The buyer must have received the goods and/or services.

- Goods are considered received when delivered by the supplier to the buyer or their authorized representative, along with a document of title transfer.

- Services are deemed received when rendered by the supplier to the buyer or their authorized representative.

Example of ITC Claim

- For instance, if Mr. Manoj receives a tax invoice for purchases dated January 10, 2022, but the goods are not received until February 20, 2022, he cannot report ITC on that invoice in GSTR-3B for January 2022. The claim can be made in the future once the goods are delivered.

Filing Requirements and Payment Terms

- The buyer must furnish GST returns in Form GSTR-3B.

- If goods are received in lots or installments, ITC can be availed when the last lot or installment is received.

- Payment for goods and/or services must be made within 180 days from the invoice date. If this condition is not met, the claimed ITC must be paid to the government along with interest under Section 50. The ITC claim can be reinstated once the payment is made to the supplier.

Restrictions on ITC Claims

- ITC is not allowed if depreciation has been claimed on the tax component of a capital good purchased.

- ITC on a tax invoice or debit note belonging to a financial year must be claimed within the time limits specified by GST provisions.

- Common credit of ITC must be identified and split when used for both exempt and taxable supplies, and/or business and non-business activities.

- Certain items listed under Section 17(5) of the CGST Act are not eligible for ITC claims, known as blocked credits.

Note: The provision regarding payment of ITC under Section 50 will come into force once notified by the CBIC.

Time Limit for Claiming Input Tax Credit (ITC)

- The time limit for claiming ITC against an invoice or debit note is the earlier of the following two dates:

- 30th November of the next financial year.

- The date of filing the annual returns in form GSTR-9 for the relevant financial year.

Example of ITC Claim Timing

For instance, if XY Corp has a purchase invoice dated December 8, 2021, and wants to claim GST paid on that purchase for FY 2021-22:

- The two dates to consider are:

- 30th November 2022.

- The date of filing the GST annual return for FY 2021-22, which is 31st December 2022.

- The earlier date is 30th November 2022, which is the deadline for claiming ITC for FY 2021-22. XY Corp can claim this ITC in any tax period between April 2021 and October 2022.

Note: For debit notes, the timing condition applies to the debit note itself, not the original invoice it is associated with.

Cases Where ITC is Not Allowed

- Motor vehicles with a seating capacity of 13 or fewer persons (including the driver), goods transport agencies, vessels, and aircraft, except in specific cases:

- When such vehicles and conveyances are sold.

- For the transport of passengers and goods.

- For training on driving, flying, or navigating such vehicles or conveyances.

- For services related to general insurance, servicing, repair, and maintenance of motor vehicles, vessels, or aircraft.

- Food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, unless they are part of a composite supply or used to provide the same category of services.

- Membership in a club, health, and fitness center.

- Rent-a-cab, health insurance, and life insurance, except when mandated by law for employers to provide to employees.

- For example, mandatory cab services for female staff working night shifts.

- For providing the same category of services or as part of a composite supply, ITC will be available.

Ineligible ITC under GST

1. Introduction to Ineligible ITC

- Input Tax Credit (ITC) is a crucial aspect of the Goods and Services Tax (GST) regime in India. It allows businesses to claim credit for the tax paid on inputs used for making taxable supplies.

- However, there are specific circumstances under which ITC cannot be claimed, known as ineligible ITC.

2. When is ITC Ineligible?

ITC is ineligible in the following cases:

- Supply of goods or services: When the supply is made by a non-resident who is not registered under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to collect tax under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to claim credit under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to collect tax under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to claim credit under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to collect tax under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to claim credit under the GST Act.

- Supply of goods or services: When the supply is made by a registered person who is not eligible to collect tax under the GST Act.

3. Detailed Explanation of Ineligible ITC Cases

- Rent-a-Cab Services: If Mr. Dev provides rent-a-cab services to Mr. Manoj, a customer, he can claim ITC on purchases.

- Leasing, Renting, or Hiring: ITC is not allowed for leasing, renting, or hiring motor vehicles, vessels, or aircraft, except in specific cases.

- Travel Benefits to Employees: ITC is not allowed for travel benefits provided to employees for vacation purposes, such as leave or home travel concessions.

- Works Contract Service: ITC is not allowed for works contract services related to the construction of immovable property, except for plant and machinery or for providing further works contract services.

- Goods and Services for Construction: ITC is not allowed for goods and services used for the construction of immovable property, whether for personal or business use.

- Composition Scheme: ITC is not allowed for goods and services where tax has been paid under the composition scheme.

- Personal Use: ITC is not allowed for goods and services used for personal purposes.

- Non-Resident Taxable Person: ITC is not allowed for goods and services received by a non-resident taxable person, except for goods imported by them.

- Lost, Stolen, or Destroyed Goods: ITC is not allowed for goods that are lost, stolen, destroyed, written off, or disposed of by way of gift or free samples.

- Fraud or Misstatement: ITC is not allowed for tax paid due to non-payment or short tax payment, excessive refund, or ITC utilized or availed due to fraud, willful misstatements, suppression of facts, or confiscation and seizure of goods.

- Standalone Restaurants: Standalone restaurants charge only 5% GST but cannot enjoy any ITC on the inputs.

- Corporate Social Responsibility (CSR): Expenditure on CSR initiatives by corporates is not eligible for ITC.

4. Claiming Accurate ITC

- To claim ITC accurately and within the stipulated time, Indian enterprises must verify ITC details before claiming them in Form GSTR-3B for a tax period.

- This involves regular reconciliation of GSTR-2B with books of accounts and frequent follow-ups with suppliers who have not reported tax invoices or debit notes.

- Clear GST offers a solution to ensure GSTR-2B data is fetched without manual intervention and matches data between books and GSTR-2B to identify gaps, allowing users to claim 100% ITC in GSTR-3B.

- The platform also enables annual reconciliation of ITC across financial years for accurate preparation of GSTR-9 and GSTR-9C.

5. Clear Max ITC:

- Clear Max ITC is an end-to-end enterprise solution for maximizing input tax credit claims.

- The platform features fast AI-based reconciliations, automated data reconciliations, vendor communication, smart payment decisions, and advanced user access management.

- It establishes a two-way connection with the ERP/accounting system, schedules automatic reconciliations, and syncs vendor payment decisions.

- The platform helps reduce defaulting vendors, optimize input tax credit, and unblock working capital, leading to reduced GST cash outflows and increased profits through ITC maximization.

FAQs on Definitions of Input Tax Credit

| 1. What are Capital Goods in GST and how do they differ from other inputs? |  |

| 2. How is Input Tax Credit (ITC) calculated for Capital Goods under GST? | |

| 3. What are the conditions for claiming Input Tax Credit on Capital Goods? | |

| 4. Can Input Tax Credit on Capital Goods be reversed? If yes, under what circumstances? | |

| 5. What are the implications of not claiming Input Tax Credit on Capital Goods? | |