Introduction to Taxation Law

Concept and Scope of Taxation Law

Taxation Law encompasses the legal principles, statutes, and regulations governing the imposition, collection, and administration of taxes. Taxes are mandatory contributions levied by the government on individuals, businesses, and other entities to fund public services such as infrastructure, healthcare, education, and national security.

Objectives of Taxation

- Revenue Generation: To finance government expenditure on public goods and services.

- Economic Stabilization: To control inflation, reduce unemployment, and promote economic growth.

- Social Equity: To redistribute wealth and reduce income disparities through progressive taxation.

- Behavioral Regulation: To encourage or discourage certain activities (e.g., higher taxes on tobacco to reduce smoking).

Scope of Taxation Law

Taxation Law covers:

Key Point: Taxation is a sovereign power rooted in the social contract, balancing state authority with taxpayer rights.

Example: When you earn a salary, a portion is deducted as income tax, which the government uses to fund public services like roads or schools.

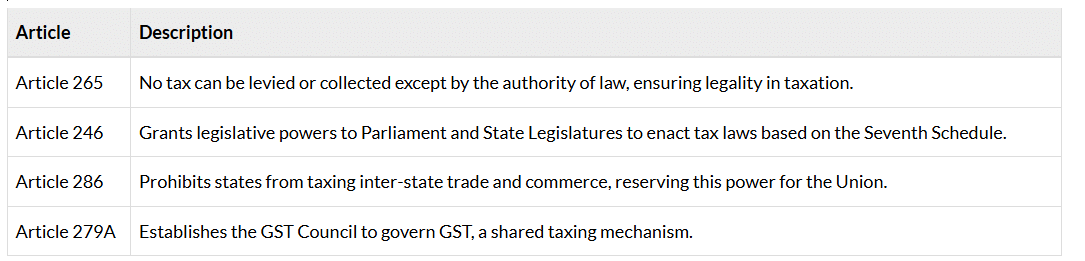

Constitutional Framework of Taxation in India

The Indian Constitution provides the legal basis for taxation, delineating the powers of the Union and State governments to ensure a federal structure. This aligns with your prior interest in the constitutional aspects of law, as seen in your queries about the Indian Constitution's features and non-constitutional bodies.

Key Constitutional Provisions

Division of Taxing Powers

The Seventh Schedule divides taxing powers into:

- Union List (List I):Taxes levied by the Central Government, including:

- Income tax (except agricultural income).

- Corporate tax.

- Customs duty.

- Central GST (CGST).

- State List (List II):Taxes levied by State Governments, including:

- State GST (SGST).

- Stamp duty.

- Land revenue.

- Professional tax.

- Concurrent List (List III): No taxing powers are assigned.

Goods and Services Tax (GST)

Introduced in 2017, GST is a unified indirect tax system that replaced multiple taxes like VAT, service tax, and excise duty. It operates under a dual structure:

- CGST: Collected by the Central Government.

- SGST: Collected by State Governments.

- IGST: Collected by the Centre for inter-state transactions.

The GST Council, a constitutional body, ensures uniformity in GST rates, exemptions, and policies.

Key Point: GST reflects cooperative federalism, with the Union and States sharing taxing powers.

Example: If you buy a laptop in Delhi, you pay CGST and SGST, which are split between the Centre and Delhi government.

Taxes are classified into Direct Taxes and Indirect Taxes, a distinction critical for CLAT PG, similar to your queries about distinctions in tort law.

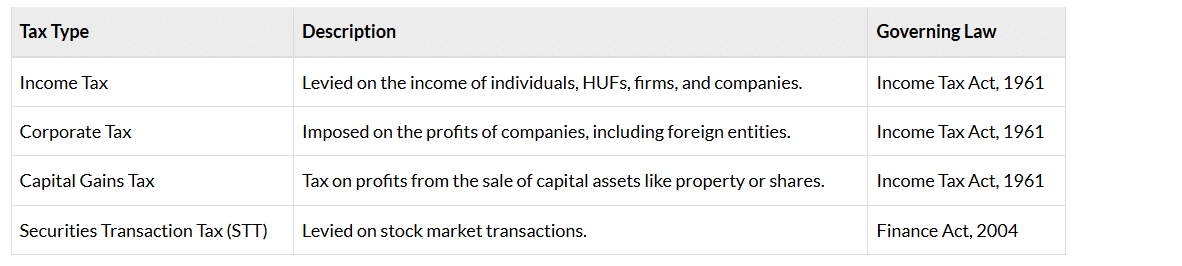

Direct Taxes

Direct taxes are levied on the income, wealth, or property of individuals or entities. The taxpayer bears the burden directly.

Example: If you earn ₹15 lakh annually, you pay income tax based on slab rates, such as 30% for income above ₹10 lakh.

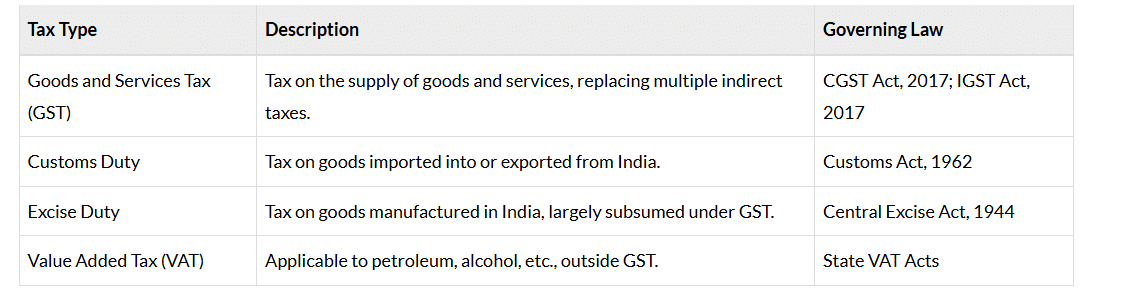

Indirect Taxes

Indirect taxes are imposed on goods and services, with the burden passed on to consumers through pricing.

Example: When you buy a smartphone for ₹20,000, the price includes 18% GST, which the seller remits to the government.

Key Point: Direct taxes are progressive, while indirect taxes are regressive, impacting all consumers equally.

Principles of Taxation

Taxation laws are guided by principles to ensure fairness, efficiency, and compliance, a concept akin to the foundational principles you explored in tort law.

Classical Principles (Adam Smith)

- Equity: Taxes should be based on the ability to pay, with higher earners paying more.

- Certainty: Tax laws should be clear, predictable, and stable.

- Convenience: The tax system should be user-friendly, with easy compliance mechanisms.

- Economy: The cost of tax collection should be minimal compared to revenue.

Modern Principles

- Neutrality: Taxes should not unduly influence economic decisions.

- Transparency: Taxpayers should understand tax calculations and usage.

- Simplicity: The tax system should avoid unnecessary complexity.

Example: The GST portal simplifies compliance by allowing online registration and return filing, aligning with the principle of convenience.

Statutory Framework of Taxation

Taxation laws are codified in statutes, supplemented by rules, notifications, and judicial precedents.

Major Statutes

- Income Tax Act, 1961: Governs direct taxes, covering assessment, exemptions, deductions, and penalties.

- Central Goods and Services Tax Act, 2017: Regulates CGST, with parallel SGST Acts for states.

- Integrated Goods and Services Tax Act, 2017: Governs IGST for inter-state supplies.

- Customs Act, 1962: Regulates import/export duties and anti-dumping measures.

- Finance Acts: Annual laws amending tax rates and provisions.

Supporting Rules and Regulations

- Income Tax Rules, 1962: Detail procedures for filing returns, claiming deductions, etc.

- GST Rules, 2017: Cover registration, invoicing, and compliance processes.

- Customs Rules: Outline valuation and clearance procedures.

Example: The Income Tax Rules specify that salaried individuals can claim a ₹50,000 standard deduction under Section 16.

Tax Administration and Authorities

Tax administration ensures compliance, collection, and dispute resolution, similar to the non-constitutional bodies you studied for CLAT PG.

Key Authorities

- Central Board of Direct Taxes (CBDT): Oversees income tax and corporate tax administration.

- Central Board of Indirect Taxes and Customs (CBIC): Manages GST, customs, and excise duties.

- GST Council: Decides GST policies, rates, and exemptions.

- Income Tax Department: Conducts assessments, audits, and investigations.

- GST Network (GSTN): A digital platform for GST compliance.

Dispute Resolution Mechanisms

- Commissioners (Appeals): First-level appellate authority for tax disputes.

- Appellate Tribunals: E.g., Income Tax Appellate Tribunal (ITAT) and GST Appellate Tribunal.

- Courts: High Courts and Supreme Court for legal interpretations.

- Advance Rulings: Provide clarity on tax liabilities for complex transactions.

- Settlement Commissions: Resolve disputes amicably in direct tax cases.

Example: If a taxpayer disputes a GST demand, they can appeal to the GST Appellate Tribunal after the Commissioner (Appeals).

Landmark Case Laws in Taxation

Judicial precedents shape taxation law, a focus area given your interest in case laws for IPC, torts, and environmental law. Key cases include:

- McDowell & Co. Ltd. v. CTO (1985): The Supreme Court distinguished between legitimate tax planning and illegal tax evasion, ruling that artificial transactions to avoid tax are invalid.

- Vodafone International Holdings v. Union of India (2012): The Court held that indirect share transfers outside India (e.g., Vodafone's acquisition of Hutch) are not taxable in India, limiting the scope of capital gains tax.

- Commissioner of Income Tax v. Glaxo SmithKline Asia (2010): Emphasized transfer pricing rules to prevent tax avoidance in multinational transactions.

- Union of India v. Azadi Bachao Andolan (2003): Upheld the validity of tax treaties and ruled that treaty shopping (using tax havens) is permissible unless mala fide.

Key Point: These cases illustrate the judiciary's role in balancing revenue collection with taxpayer rights.

International Taxation and Double Taxation

International taxation deals with cross-border transactions and preventing double taxation (taxing the same income in two countries).

Double Taxation Avoidance Agreements (DTAAs)

India has DTAAs with over 90 countries to allocate taxing rights and provide relief from double taxation through:

- Exemption Method: Income is taxed in one country and exempt in the other.

- Tax Credit Method: Tax paid in one country is credited against tax liability in the other.

Base Erosion and Profit Shifting (BEPS)

BEPS refers to tax avoidance strategies by multinationals. India has adopted BEPS measures like:

- Country-by-Country Reporting.

- General Anti-Avoidance Rules (GAAR) under the Income Tax Act.

Example: Under the India-USA DTAA, a US company earning royalties in India pays tax in India, with a credit in the USA.

Key Point: International taxation is relevant for CLAT PG due to globalization and cases like Vodafone.

Conclusion

Taxation Law is a multifaceted subject that integrates constitutional law, statutory provisions, and judicial precedents to regulate government revenue collection. For CLAT PG, it demands a deep understanding of the legal framework, practical applications, and recent developments. By mastering the constitutional basis, types of taxes, landmark cases, and international aspects, you can excel in the exam. Consistent practice, case law analysis, and engagement with current tax policies will prepare you for both academic and professional success in tax law.

- Direct taxes (e.g., income tax, corporate tax).

- Indirect taxes (e.g., GST, customs duty).

- Constitutional provisions governing taxing powers.

- Administrative mechanisms for tax collection and dispute resolution.

- Judicial interpretations through landmark cases.

FAQs on Introduction to Taxation Law

| 1. What is the constitutional framework of taxation in India? |  |

| 2. What are the main types of taxes in India? | |

| 3. What are the key principles of taxation? | |

| 4. What is the role of tax administration and authorities in India? | |

| 5. How does international taxation and double taxation work in India? | |