Anti-Avoidance and International Taxation: Income Tax Act, 1961

Introduction to Anti-Avoidance and International Taxation

Anti-Avoidance measures are provisions in the Income Tax Act to prevent taxpayers from exploiting loopholes to reduce or evade tax liability. These rules ensure that tax is paid on the true economic substance of transactions rather than their legal form.

International Taxation deals with taxing cross-border transactions, addressing issues like double taxation, tax treaties, and income earned by residents and non-residents across jurisdictions.

Key Point: Anti-avoidance and international taxation provisions aim to curb tax evasion and ensure fair taxation in a globalized economy.

Anti-Avoidance Measures

The Income Tax Act includes specific anti-avoidance rules to tackle tax planning strategies that artificially reduce taxable income. Key provisions are:

General Anti-Avoidance Rules (GAAR) (Sections 95-102)

GAAR empowers tax authorities to disregard transactions or arrangements that lack commercial substance and are primarily designed to obtain tax benefits.

- Applicability:GAAR applies to arrangements where the main purpose is to avoid tax, and they meet one of these conditions:

- Not at arm's length.

- Lack commercial substance.

- Abuse of tax provisions.

- Not for bona fide purposes.

- Consequences:The tax authorities can:

- Deny tax benefits.

- Recharacterize transactions.

- Impose tax liability as if the arrangement didn't exist.

- Procedure: GAAR is invoked only after approval from a high-level panel to prevent misuse.

Example: A company sets up a shell entity in a tax haven to route profits and avoid tax in India. GAAR can disregard the entity and tax the profits in India.

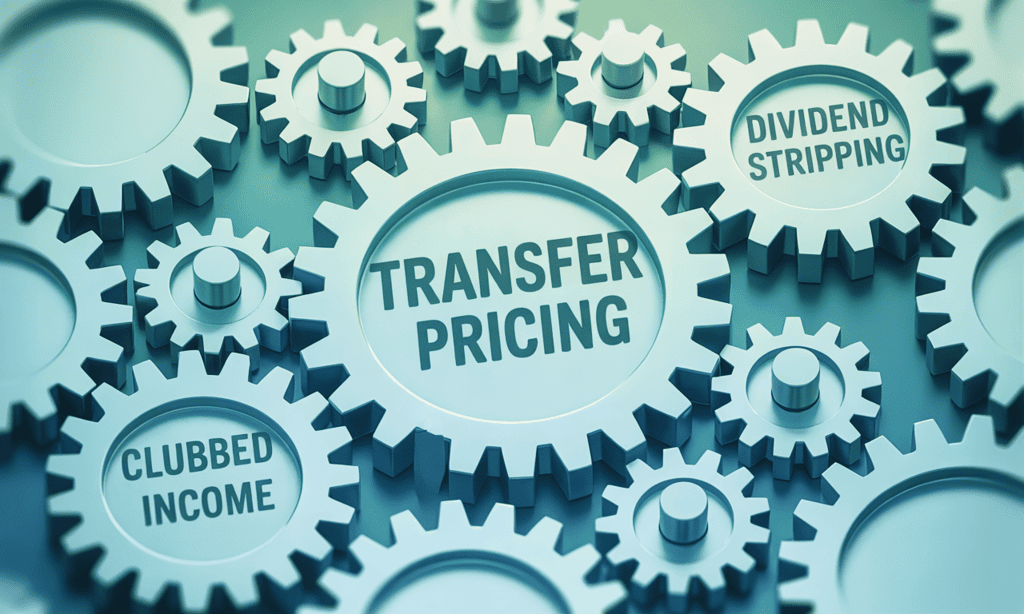

Specific Anti-Avoidance Rules (SAAR)

SAAR targets specific transactions or arrangements, such as:

- Transfer Pricing (Sections 92-92F): Ensures that transactions between related parties (e.g., parent and subsidiary companies) are conducted at arm's length prices to prevent profit shifting.

- Clubbed Income (Sections 60-64): Income transferred to another person (e.g., spouse, minor child) without transferring the asset is clubbed with the transferor's income for taxation.

- Dividend Stripping (Section 94): Prevents tax avoidance by buying securities before dividend declaration and selling them at a loss afterward.

Thin Capitalization Rules

These rules limit the deduction of interest paid on excessive debt borrowed from related parties to reduce taxable income.

- Section 94B: Interest deduction is capped at 30% of EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) for loans from non-residents or related parties.

International Taxation

International taxation governs the taxation of income involving cross-border transactions, addressing issues like residency, source of income, and double taxation.

Residential Status and Tax Liability

The tax liability of an assessee depends on their residential status (as discussed in earlier notes):

- Resident: Taxed on global income.

- Non-Resident: Taxed only on income sourced or received in India.

- Resident but Not Ordinarily Resident (RNOR): Taxed on Indian income and foreign income derived from a business controlled in India.

Key Point: Determining residential status is critical for international taxation to ascertain the scope of taxable income.

Source Rule

Income is taxed based on its source. Examples of income deemed to arise in India (Section 9):

- Income from a business connection in India.

- Income from property, assets, or sources located in India.

- Salaries for services rendered in India.

- Royalties or fees for technical services paid by an Indian resident.

Example: A US company earns royalties from an Indian company for using its technology. This royalty is deemed to arise in India and is taxable.

Double Taxation

Double taxation occurs when the same income is taxed in two jurisdictions (e.g., India and another country). To avoid this, India uses:

- Double Taxation Avoidance Agreements (DTAAs): Bilateral treaties with other countries to allocate taxing rights and provide relief from double taxation.

- Foreign Tax Credit (FTC): Tax paid in a foreign country can be credited against Indian tax liability (Section 90/91).

Key Point: DTAAs override domestic tax laws if they provide more beneficial provisions to the taxpayer.

Transfer Pricing (Sections 92-92F)

Transfer pricing ensures that transactions between related parties (Associated Enterprises) are conducted at arm's length prices to prevent profit shifting to low-tax jurisdictions.

- Arm's Length Price (ALP): The price that would be charged in a transaction between unrelated parties.

- Methods to Determine ALP:

- Comparable Uncontrolled Price (CUP) Method

- Resale Price Method

- Cost Plus Method

- Profit Split Method

- Transactional Net Margin Method (TNMM)

- Documentation: Taxpayers must maintain detailed records to justify the ALP.

- Penalties: Non-compliance (e.g., failure to maintain documentation) attracts penalties under Section 271.

Example: An Indian subsidiary buys goods from its US parent company at an inflated price to reduce taxable profits in India. Transfer pricing rules require the price to be adjusted to the ALP.

Permanent Establishment (PE)

A Permanent Establishment is a fixed place of business through which a foreign enterprise carries out business in India, making its profits taxable in India.

- Types of PE:

- Fixed Place PE (e.g., office, branch).

- Agency PE (e.g., dependent agent acting on behalf of the foreign enterprise).

- Service PE (e.g., employees providing services in India for a specified period).

- Taxation: Profits attributable to the PE are taxed in India.

Base Erosion and Profit Shifting (BEPS)

BEPS refers to tax avoidance strategies by multinational companies that exploit gaps in tax rules to shift profits to low-tax jurisdictions. India has adopted BEPS Action Plans, including:

- Country-by-Country Reporting (CbCR): Multinational enterprises with revenue above ₹5,500 crore must report their global income, taxes, and activities (Section 286).

- Master File and Local File: Detailed transfer pricing documentation to ensure transparency.

Significant Economic Presence (SEP)

Introduced to tax digital businesses, SEP deems a non-resident to have a taxable presence in India if they have:

- Revenue from India exceeding a specified threshold, or

- A significant number of users or digital interactions in India.

Impact: Targets e-commerce and digital companies operating in India without a physical presence.

Tax Treaties (DTAAs)

India has signed DTAAs with over 90 countries to promote trade and investment while avoiding double taxation. Key features:

- Relief Methods:

- Exemption Method: Income is taxed in only one country.

- Credit Method: Tax paid in one country is credited in the other.

- Key Articles:

- Article 5: Permanent Establishment.

- Article 7: Business Profits.

- Article 10: Dividends.

- Article 12: Royalties and Fees for Technical Services.

- Multilateral Instrument (MLI): India has adopted the MLI to amend DTAAs and prevent BEPS.

Penalties for Non-Compliance

Non-compliance with anti-avoidance or international taxation provisions attracts penalties, such as:

- Section 271AA: Penalty for failure to maintain transfer pricing documentation (2% of transaction value).

- Section 271G: Penalty for failure to furnish transfer pricing documents (2% of transaction value).

- Section 270A: Penalty for under-reporting income due to tax avoidance (50-200% of tax evaded).

Recent Developments

Key updates in anti-avoidance and international taxation (as of 2023):

- Equalisation Levy: A 2% levy on e-commerce transactions by non-residents (e.g., online advertising, digital platforms).

- SEP Implementation: Expanded taxation of digital economy businesses.

- BEPS Compliance: Stricter reporting requirements for multinational enterprises.

Conclusion

Anti-avoidance and international taxation provisions under the Income Tax Act, 1961, are critical to prevent tax evasion and ensure fair taxation of cross-border transactions. A thorough understanding of these concepts is essential for CLAT PG aspirants.

FAQs on Anti-Avoidance and International Taxation: Income Tax Act, 1961

| 1. What are anti-avoidance measures in international taxation? |  |

| 2. How do tax treaties (DTAAs) work in international taxation? | |

| 3. What are the penalties for non-compliance with international tax laws? | |

| 4. What recent developments have occurred in international tax regulation? | |

| 5. How does the Income Tax Act, 1961 address anti-avoidance measures? | |