Short Notes: Reconstitution of a Partnership Firm: Admission of a Partner

Introduction

A partnership is an agreement between two or more individuals, known as partners, to run a business and share its profits based on mutual trust, cooperation, and a legal agreement. Reconstitution of a partnership firm occurs when the existing agreement ends, and a new one is formed, but the business continues under the same name. This happens due to changes like admitting a new partner, altering profit-sharing ratios, or a partner's retirement, death, or insolvency.

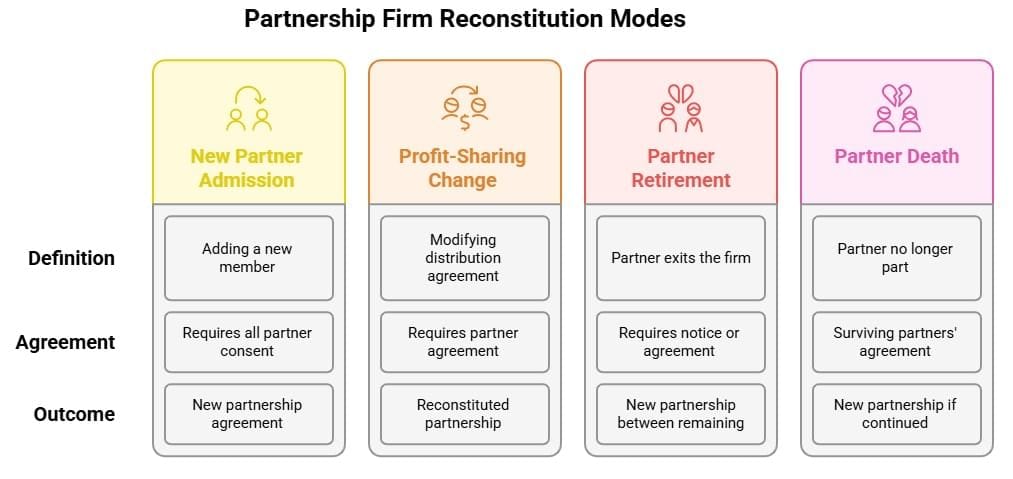

Modes of Reconstitution of a Partnership Firm

Reconstitution involves altering the existing partnership agreement while the business continues. The main modes are:

1. Admission of a New Partner

- A new partner is admitted when the firm needs additional capital or managerial support.

- As per the Indian Partnership Act, 1932, all existing partners must agree, unless the partnership deed states otherwise.

- Example: Hari and Haqque share profits in a 3:2 ratio. They admit John for a 1/6 share, ending the old agreement and forming a new one.

Explanation: The remaining 5/6 profit is shared by Hari and Haqque in their old ratio. This changes their shares, leading to the reconstitution of the partnership with three partners and a new profit-sharing arrangement.

2. Change in Profit-Sharing Ratio Among Existing Partners

- Partners may revise their profit-sharing ratio due to changes in capital contribution or responsibilities.

- Example: Ram, Mohan, and Sohan share profits in 3:2:1. After Sohan adds more capital, they agree to share profits equally (1:1:1).

- Explanation: The shift from 3:2:1 to 1:1:1 changes each partner's profit share. This requires a new agreement, leading to the reconstitution of the firm, even though the number of partners remains the same.

3. Retirement of a Partner

- A partner may retire voluntarily due to age, health, or personal reasons.

- In a partnership at will, retirement requires notice to other partners.

- Example: Roy, Ravi, and Rao share profits in 2:2:1. Ravi retires due to illness, and Roy and Rao continue the business.

- Explanation: Ravi's 2/5 share is removed. Roy and Rao form a new agreement (e.g., using the old 2:1 ratio). This leads to reconstitution, as the number of partners and profit-sharing ratio have changed.

4. Death of a Partner

- When a partner dies, the partnership ends unless the surviving partners agree to continue with a new agreement.

- Example: X, Y, and Z share profits in a 3:2:1 ratio. X dies, and Y and Z decide to continue with an equal profit share (1:1).

- Explanation: X's death removes their 3/6 share. Y and Z choose to continue, now sharing profits equally (1/2 each). A new agreement is formed, resulting in reconstitution due to the change in partners and profit-sharing ratio.

Admission of a New Partner

Admission occurs when a firm requires more capital or expertise. According to the Partnership Act, 1932, all partners must agree unless otherwise stated. The new partner gains rights to share in firm assets and profits, contributing capital and possibly a goodwill premium to compensate existing partners for their reduced profit share.

Key considerations include:

- New profit-sharing ratio

- Sacrificing ratio

- Valuation and adjustment of goodwill

- Revaluation of assets and liabilities

- Distribution of accumulated profits

- Adjustment of partners' capitals

New Profit-Sharing Ratio

- A new partner's profit share is taken from existing partners, changing their shares. If not specified, it's assumed to be in the old ratio.

- Example: Anil and Vishal share profits in 3:2. Sumit is admitted for a 1/5 share, taken equally from both.

- Calculation:

- Anil: old share = 3/5 (6/10), sacrifice = 1/10 → new share = 5/10

- Vishal: old share = 2/5 (4/10), sacrifice = 1/10 → new share = 3/10

- Sumit's share = 2/10

- New ratio: Anil: Vishal: Sumit = 5:3:2

- Explanation: Sumit's share is equally deducted from Anil and Vishal, reducing their shares and forming a new profit-sharing ratio. This adjustment reflects the reconstitution of the firm.

Sacrificing Ratio

The sacrificing ratio shows how much profit share the old partners give up for the new partner.

It is calculated as: Old Share - New Share.

Example: Rohit and Mohit share profits in 5:3. Bijoy is admitted for a 1/7 share. The new ratio becomes 4:2:1.

Calculation:

Rohit: old = 5/8, new = 4/7 → sacrifice = 5/8 - 4/7 = 3/56

Mohit: old = 3/8, new = 2/7 → sacrifice = 3/8 - 2/7 = 5/56

Sacrificing ratio = 3:5

Explanation: By subtracting the new share from the old, we find how much each partner gives up. This ratio is used for sharing goodwill brought in by the new partner.

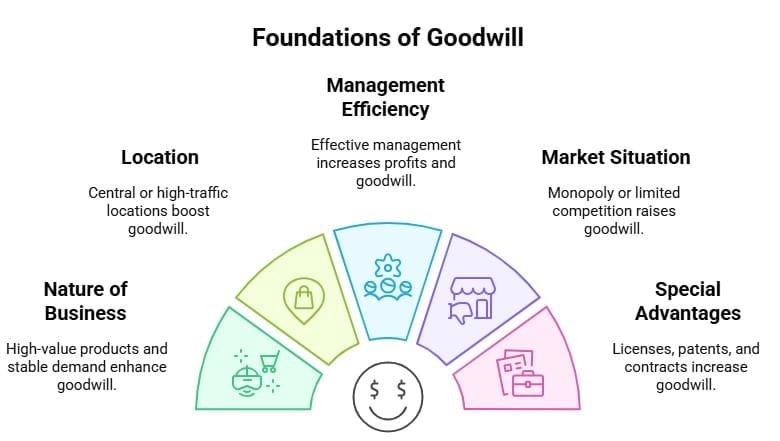

What is Goodwill?

Goodwill is an intangible asset that reflects a firm's reputation and ability to earn super profits above normal industry returns. It arises from factors like a strong brand, loyal customers, and good business relations. Goodwill represents the present value of excess earnings and only exists when a firm earns more than average profits.

Factors Influencing the Value of Goodwill

- Nature of Business: High-value products or stable demand increase goodwill.

- Location: Central or high-traffic locations enhance goodwill.

- Efficiency of Management: Effective management boosts profits and goodwill.

- Market Situation: Monopoly or limited competition raises goodwill.

- Special Advantages: Licenses, patents, or long-term contracts increase goodwill.

Reasons for Goodwill Valuation

Goodwill valuation is needed during:

- Change in profit-sharing ratio

- Admission, retirement, or death of a partner

- Dissolution or amalgamation of firms

- Sale of the business

Methods for Valuing Goodwill

1. Average Profits Method

- Goodwill is calculated as the average past profits multiplied by the number of years' purchase.

- Example: Profits for 2013-2017 are Rs. 4,00,000, Rs. 3,98,000, Rs. 4,50,000, Rs. 4,45,000, Rs. 5,00,000.

- Average profit = Rs. 21,93,000 / 5 = Rs. 4,38,600.

- Goodwill = Rs. 4,38,600 × 4 years = Rs. 17,54,400.

- Explanation: Total profits over five years (Rs. 21,93,000) are averaged to get Rs. 4,38,600. Goodwill is then valued by multiplying this by 4, assuming stable future profits and a buyer paying for four years' earnings.

2. Super Profits Method

- Goodwill is based on super profits (actual profits minus normal profits) multiplied by years' purchase.

- Example: Capital employed: Rs. 5,00,000. Profits (2011-2015): Rs. 40,000, Rs. 50,000, Rs. 55,000, Rs. 70,000, Rs. 85,000.

- Average profit = Rs. 3,00,000 / 5 = Rs. 60,000.

- Normal profit = 10% of Rs. 5,00,000 = Rs. 50,000.

- Super profit = Rs. 60,000 - Rs. 50,000 = Rs. 10,000.

- Goodwill = Rs. 10,000 × 3 = Rs. 30,000.

- Explanation: Average profit is Rs. 60,000; normal profit is Rs. 50,000 (10% of Rs. 5,00,000). Super profit is Rs. 10,000. Goodwill is calculated as super profit × 3 years' purchase = Rs. 30,000, representing the value of excess earnings.

3. Capitalisation Method

(a) Capitalisation of Average Profits:

- Goodwill = Capitalised value of average profits - Net assets.

- Example: Average profit = Rs. 1,00,000, normal return = 10%, net assets = Rs. 8,20,000.

- Capitalised value = Rs. 1,00,000 × 100 / 10 = Rs. 10,00,000.

- Goodwill = Rs. 10,00,000 - Rs. 8,20,000 = Rs. 1,80,000.

- Explanation: Average profit of Rs. 1,00,000 is capitalised at 10%, giving Rs. 10,00,000. After subtracting net assets (Rs. 8,20,000), goodwill is Rs. 1,80,000. This shows the extra capital needed to earn an average profit at the normal rate.

(b) Capitalisation of Super Profits: Goodwill = Super profits × 100 / Normal rate of return.

Treatment of Goodwill

When a new partner joins, they compensate old partners for their sacrificed profit share via a goodwill premium. If paid in cash, it's distributed to old partners per the sacrificing ratio. If not paid, the new partner's current account is debited, and the sacrificing partners' capital accounts are credited.

- Example: Hem and Nem (3:2 ratio, capitals Rs. 80,000, Rs. 50,000) admit Sam for 1/5 share with Rs. 60,000 capital.

- Total firm capital = Rs. 60,000 × 5 = Rs. 3,00,000.

- Actual capital = Rs. 1,90,000. Goodwill = Rs. 1,10,000.

- Sam's goodwill share = Rs. 1,10,000 × 1/5 = Rs. 22,000.

- If Sam doesn't bring goodwill, his current account is debited, and Hem and Nem's capital accounts are credited in a 3:2 ratio.

- Explanation: Sam's Rs. 60,000 capital for a 1/5 share implies total firm capital of Rs. 3,00,000. Actual capital is Rs. 1,90,000, so goodwill is Rs. 1,10,000. Sam's share is Rs. 22,000 (1/5 of Rs. 1,10,000), debited to him if unpaid, and credited to Hem and Nem in their 3:2 sacrificing ratio.

Adjustment of Accumulated Profits and Losses

Accumulated profits (e.g., general reserve) are credited to old partners' capital accounts in their old ratio, as new partners are not entitled to them. Losses are debited similarly.

- Example: Rajinder and Surinder (4:1 ratio) have Rs. 20,000 in general reserve and Rs. 10,000 debit in P&L.

- On Narender's admission, reserve is credited and loss debited to Rajinder and Surinder's capital accounts in 4:1.

- Explanation: The general reserve of Rs. 20,000 is shared between Rajinder (Rs. 16,000) and Surinder (Rs. 4,000) in the 4:1 ratio, as Narender isn't entitled to past profits. The P&L debit balance of Rs. 10,000 is treated as a loss, debited to Rajinder (Rs. 8,000) and Surinder (Rs. 2,000) in the same ratio.

Revaluation of Assets and Liabilities

A Revaluation Account records gains/losses from revaluing assets and liabilities. Gains (e.g., asset value increase) are credited, and losses (e.g., liability increase) are debited. The net balance is transferred to the old partners' capital accounts in their old ratio.

Adjustment of Capitals

Capitals may be adjusted to match the new profit-sharing ratio. Excess capital is withdrawn, and deficiencies are contributed.

- Example: A and B (2:1 ratio, capitals Rs. 45,000, Rs. 15,000) admit C for 1/4 share with Rs. 20,000.

- New ratio: 2:1:1. Total capital = Rs. 80,000.

- A's new capital = Rs. 40,000 (withdraws Rs. 5,000).

- B's new capital = Rs. 20,000 (contributes Rs. 5,000).

- Explanation: C's Rs. 20,000 capital for a 1/4 share implies total capital of Rs. 80,000. In the new 2:1:1 ratio, A's share (2/4) needs Rs. 40,000; he has Rs. 45,000, so withdraws Rs. 5,000. B's share (1/4) needs Rs. 20,000; he has Rs. 15,000, so adds Rs. 5,000. This adjusts capitals to match the new ratio.

Change in Profit-Sharing Ratio Among Existing Partners

Partners may alter their profit-sharing ratio without admitting or losing partners, requiring adjustments for goodwill, revaluation, accumulated profits/losses, and capitals.

- Example: A, B, and C (8:5:3 ratio) change to 5:6:5.

- A sacrifices 3/16, while B and C gain 1/16 and 2/16.

- Goodwill and other adjustments are made in the sacrificing/gaining ratio.

- Explanation: The old ratio is 8:5:3, and the new ratio is 5:6:5. A's share drops from 8/16 to 5/16, sacrificing 3/16. B's share rises from 5/16 to 6/16 (gain of 1/16), and C's from 3/16 to 5/16 (gain of 2/16). Goodwill is adjusted by crediting A and debiting B and C based on their respective gains, ensuring fair compensation for the change in profit-sharing.

Conclusion

Reconstitution of a partnership firm ensures business continuity despite changes like partner admission, retirement, death, or profit-sharing ratio adjustments, requiring careful handling of goodwill, assets, and capital. These short notes offer a concise overview of these processes, mainly focusing on the admission of a new partner. For more detailed problems and in-depth explanations, refer to the comprehensive chapter notes here.

FAQs on Short Notes: Reconstitution of a Partnership Firm: Admission of a Partner

| 1. What does reconstitution of a partnership firm entail? |  |

| 2. How is goodwill defined in the context of a partnership firm? | |

| 3. What are the key steps involved in admitting a new partner into a partnership firm? | |

| 4. What factors can influence the valuation of goodwill during reconstitution? | |

| 5. Why is it important to document the reconstitution of a partnership firm? | |