Past Year Questions: Accounts from Incomplete Records

Q1: The following are some of the transactions of Digital Stores for the year 2024-25 as per their Rough Book: (5 Marks, May 2025)

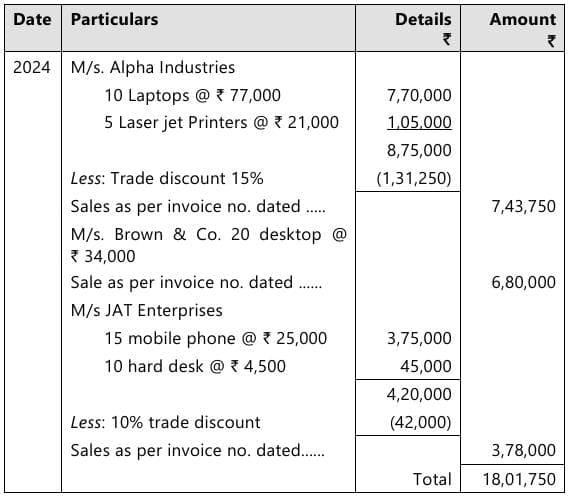

Sold to M/s Alpha Industries

10 Laptops @ ₹ 77,000 per laptop

5 LaserJet Printers @ 21,000 per printer

Less: Trade Discount @ 15%

Sold old furniture to Singh Consultants on credit ₹ 19,000

Sold 20 Desktops to Brown & Co. @ ₹ 34,000 per desktop on credit

Sold 10 Tablets to GOKU Institute @ ₹ 7,000 per tablet for cash

Sold on credit to JAT Enterprises

15 Mobile phone @ ₹ 25,000 per mobile phone

10 External Hard Disk @ ₹ 4,500 per external hard disk

Less: Trade Discount @ 10%

Make out the Sales Book of Digital Store.

Ans: Sales Book of Digital Stores  Note: Cash sale and sale of furniture are not entered in Sales Book.

Note: Cash sale and sale of furniture are not entered in Sales Book.

Working (calculations) - amounts to be entered in the Sales Book:

- M/s Alpha Industries: 10 × ₹77,000 = ₹7,70,000; 5 × ₹21,000 = ₹1,05,000; gross amount = ₹8,75,000. Trade discount @ 15% = ₹1,31,250. Net credit sale = ₹8,75,000 - ₹1,31,250 = ₹7,43,750.

- Brown & Co.: 20 × ₹34,000 = ₹6,80,000 (no trade discount given).

- JAT Enterprises: 15 × ₹25,000 = ₹3,75,000; 10 × ₹4,500 = ₹45,000; gross amount = ₹4,20,000. Trade discount @ 10% = ₹42,000. Net credit sale = ₹4,20,000 - ₹42,000 = ₹3,78,000.

- Items excluded from Sales Book: Sale of furniture to Singh Consultants (credit) ₹19,000 and cash sale to GOKU Institute are not entered in Sales Book.

- Total to be recorded in Sales Book (sum of net credit sales): ₹7,43,750 + ₹6,80,000 + ₹3,78,000 = ₹18,01,750.

Total credit sales recorded in the Sales Book = ₹18,01,750.

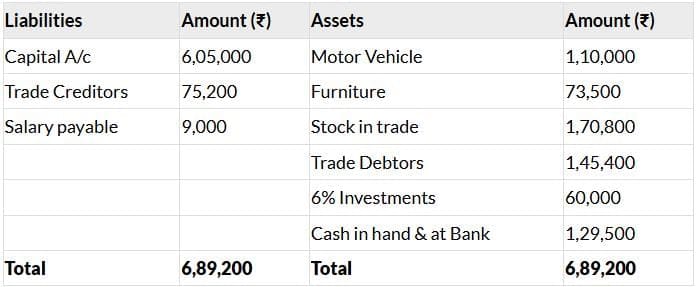

Q2: Harshit Traders are carrying on the retail business of electrical goods. They keep their books of account under a single-entry system. The Balance Sheet as on 31st March, 2023 was as follows: (8 Marks, Jun 2024)

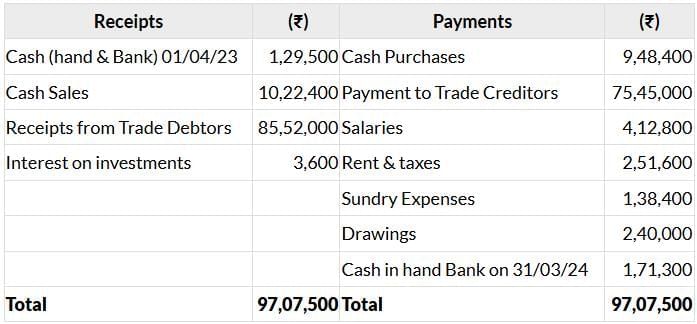

The summary of Cash and Bank Book for the year ended 31st March, 2024 was given as below:

Additional Information:

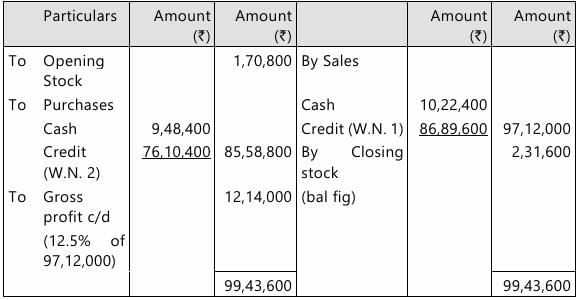

(i) Gross Profit ratio of 12.5% on Sales is maintained throughout the year.

(ii) During the year, discount allowed to Trade debtors was for ₹ 62,500 and discount received from Trade Creditors amounted to ₹ 35,000.

(iii) As on 31st March, 2024, the closing balances of Trade Debtors and Trade Creditors were ₹ 2,20,500 and ₹ 1,05,600 respectively.

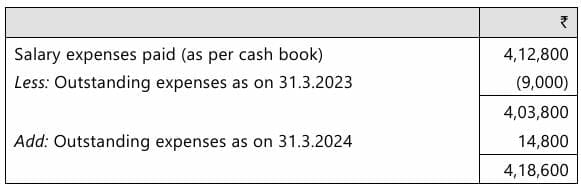

(iv) On 31st March, 2024 an amount of ₹ 14,800 was outstanding towards Salary.

(v) Depreciation @ 10% p.a. to be charged on Motor Vehicle and Furniture.

You are required to prepare Trading and Profit & Loss account for the year ended 31st March 2024, and Balance Sheet as on that date.

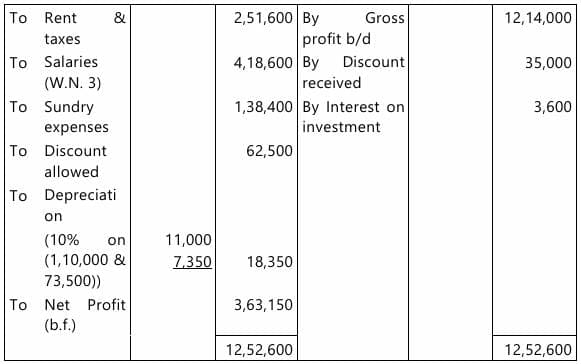

Ans: In the books of Harshit Traders

Trading and Profit and Loss Account for the year ended 31st March, 2024

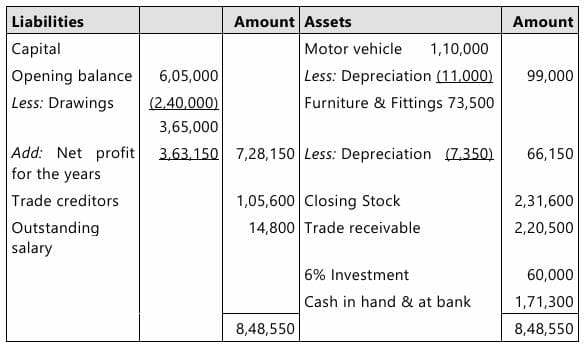

Balance Sheet as at 31st March, 2024

Balance Sheet as at 31st March, 2024 Working Notes:

Working Notes:

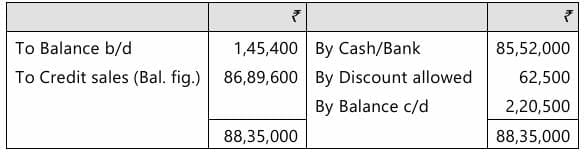

1. Trade Debtors Account  2. Trade Creditors Account

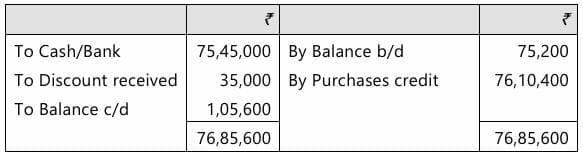

2. Trade Creditors Account 3. Computation of salary to be charged to Profit & Loss A/c

3. Computation of salary to be charged to Profit & Loss A/c Explanation and workings (approach used):

Explanation and workings (approach used):

- Under single-entry, the complete Trading and Profit & Loss Account and Balance Sheet are reconstructed using the opening Balance Sheet, the Cash and Bank summary and the additional information supplied.

- The gross profit ratio 12.5% on sales is used to derive the gross profit from sales when necessary; gross profit = 12.5% of sales. From gross profit we obtain cost of goods sold and hence purchases or closing stock adjustments as required.

- Adjustments incorporated in the accounts:

- Discount allowed to trade debtors ₹62,500 and discount received from trade creditors ₹35,000 are taken to Profit & Loss A/c.

- Closing balances of trade debtors ₹2,20,500 and trade creditors ₹1,05,600 are used in the Balance Sheet and in working ledgers.

- Outstanding salary ₹14,800 is accrued in Profit & Loss A/c and shown as a current liability in the Balance Sheet.- Depreciation at 10% p.a. on Motor Vehicle and Furniture has been charged and shown both in Profit & Loss A/c (expense) and deducted from the respective asset values in the Balance Sheet.

Q3: The following information relates to Mr. Prem who maintains his books under single entry system. He is not able to ascertain the amount of bad debts incurred by him and seeks your help.

Debtors as on 01.04.2023 ₹ 6,50,000

Debtors as on 31.03.2024 ₹ 8,50,000

Sale for FY 2023-2024 is 16,00,000 out of which 80% is on credit.

Payment received during the year is ₹ 7,50,000 out of which cheques of ₹ 18,000 were dishonored. Bills of exchange accepted by customers ₹ 2,90,000.

Discount allowed is 1% of the credit sale.

You are required to ascertain the amount of bad debts. (5 Marks, Sep 2024)

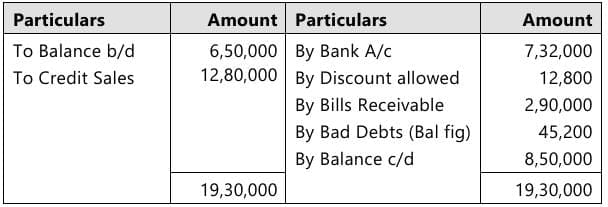

Ans: Debtors Account

Working and calculation:

- Credit sales: 80% of ₹16,00,000 = ₹12,80,000.

- Discount allowed: 1% of credit sales = 1% of ₹12,80,000 = ₹12,800.

- Payments received from debtors: ₹7,50,000, however cheques of ₹18,000 were dishonoured. The dishonoured amount is treated as not received and therefore increases debtors. Net effective receipt for closing the account is treated accordingly in the Debtors account workings.

- Bills of exchange accepted by customers: ₹2,90,000 - these reduce debtors (debtor converted into bills receivable).

Prepare Debtors account (summary):

- Opening debtors (1.4.2023) = ₹6,50,000

- Add: Credit sales during the year = ₹12,80,000

- Add: Dishonoured cheques (re-instated to debtors) = ₹18,000

- - Total debits = ₹6,50,000 + ₹12,80,000 + ₹18,000 = ₹19,48,000

- Credit side items:

- Cash/Bank receipts from debtors = ₹7,50,000

- Discount allowed = ₹12,800

- Bills accepted by customers = ₹2,90,000

- Closing debtors (31.3.2024) = ₹8,50,000

- Balancing figure - Bad debts = Total debits - known credits = ₹19,48,000 - ₹19,02,800 = ₹45,200.

Bad debts for the year = ₹45,200.

FAQs on Past Year Questions: Accounts from Incomplete Records

| 1. What are incomplete records in accounting? |  |

| 2. How can one prepare accounts from incomplete records? | |

| 3. What are the common methods used to ascertain profit from incomplete records? | |

| 4. What is the significance of maintaining complete records in accounting? | |

| 5. What challenges do businesses face when dealing with incomplete records? | |