Cheatsheet: Subsidiary Books

Overview

Subsidiary books are specialized accounting journals used to record transactions of similar nature. Instead of recording every transaction in the Journal, they help simplify, classify and speed up the accounting process. They reduce clerical work and allow division of work, making accounting more accurate and efficient.

Why Subsidiary Books?

- They replace the need for a full journal in big businesses.

- Each subsidiary book deals with one type of transaction only, ensuring accuracy.

- They help in internal control, division of work, and error reduction.

- Ledger posting becomes easier because consolidated totals are posted, not individual entries.

Types of Subsidiary books

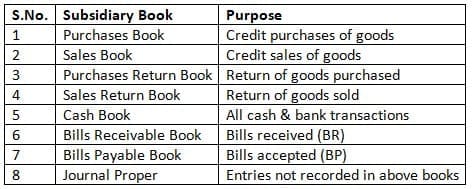

Subsidiary books are mainly 8 types:

Purchases Book

Purpose: Records credit purchases of goods only.

Format: Points to Remember:

Points to Remember:

- Cash purchases never enter Purchases Book.

- Non-goods items (machinery, furniture) are also excluded.

- Total posted to Purchases A/c periodically; supplier-wise amounts posted to individual creditor accounts.

Sales Book

Purpose: Records credit sales of goods only.

Format:

Important Notes:

- Cash sales are not recorded here.

- Total posted to Sales A/c; customer-wise posting to Debtors Accounts.

Purchases Return Book (Return Outward Book)

Purpose: Records goods returned to suppliers.

Format:

Debit Note Issued: A Debit Note is sent to the supplier showing why goods are returned.

Posting:

- Total → Purchases Return A/c.

- Individual amounts → supplier's account.

Sales Return Book (Return Inward Book)

Purpose: Records goods returned by customers.

Format: Credit Note Issued: A Credit Note is issued by the business for goods received back.

Credit Note Issued: A Credit Note is issued by the business for goods received back.

Posting:

- Total → Sales Return A/c.

- Customer-wise → Debtors A/c.

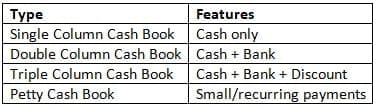

Cash Book

It is both a book of original entry and a ledger because it performs two functions.

Types of Cash Book

Format: (Double Column)

Cash Book (Double Column)

Debit Side - Receipts Credit Side - Payments

Credit Side - Payments

Quick Facts: Cash Book

- No closing balance on credit side for cash (cash cannot be negative).

- Contra entries occur when cash is deposited/withdrawn from bank.

- Petty Cash Book often uses Imprest System.

Bills Receivable Book

Purpose: Records all bills received from customers.

Format:

Posting:

- Total → Bills Receivable A/c.

- Individual entries → Customer accounts.

Bills Payable Book

Purpose: Records all bills accepted in favor of creditors.

Format: Posting:

Posting:

- Total → Bills Payable A/c.

- Individual entries → Supplier accounts.

Journal Proper (Miscellaneous Journal)

Journal Proper is used when entries cannot be recorded in any other subsidiary book.

Contents of Journal Proper

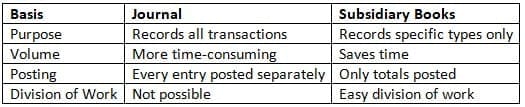

Difference Between Subsidiary Books & Journal

Advantages of Subsidiary Books

- Saves time

- Facilitates division of work

- Allows internal control

- Reduces clerical errors

- Simplifies ledger posting

- Ensures better accuracy

Quick Revision

- Purchases Book = Credit purchases of goods

- Sales Book = Credit sales of goods

- Debit Note = Goods returned to supplier

- Credit Note = Goods returned by customer

- Cash Book = Also a Ledger

- Journal Proper = For remaining entries

FAQs on Cheatsheet: Subsidiary Books

| 1. What are subsidiary books? |  |

| 2. Why are subsidiary books necessary in accounting? | |

| 3. What is recorded in the Purchases Book? | |

| 4. How does the Cash Book differ from other subsidiary books? | |

| 5. What information is included in the Sales Return Book? | |