Chapter Notes: Banks and the Magic of Finance

This chapter explores financial infrastructure in India - the network of banks, payment systems, stock markets, and other financial institutions that help people, businesses, and government facilitate financial transactions and manage money.

Introduction

- Financial infrastructure is a network of banks, payment systems, stock markets, and other financial institutions.

- It helps people, businesses, and government facilitate financial transactions and manage money.

A bank

A bank

Connection with Physical Infrastructure

- Physical infrastructure (roads, railways, telecommunication) supports economic activities driven by money-related transactions.

- Financial infrastructure enables these monetary transactions to take place between people.

- It also helps fund the development and maintenance of physical infrastructure.

What are Banks and What Do They Do?

- A bank is a financial institution that collects money from people in the form of deposits and lends money to people or borrowers as loans.

Example: Navdeep and Rima

- Navdeep saves ₹3,000 from his salary every month.

- Saving all that money in his cupboard might not be safe.

- So he deposits the money in a bank.

- Rima runs a business making bamboo products and needs money for business operations.

- When friends and family couldn't help as much as required, she takes a loan from the bank and repays it later.

- Navdeep deposits his surplus money with the bank, and the bank provides Rima with the amount she needs as a loan.

Bank Services

- Banks help make monetary transactions easy by offering services like saving, withdrawing, and borrowing money.

- These services are used by farmers, shopkeepers, nurses, businesses, and institutions.

- To use bank services, one first needs to open a bank account.

- The person or business is then called a bank account holder.

Hold Deposits

- Deposits are money placed in a bank account that can be withdrawn as per the bank's terms and often earns interest.

- A bank accepts and holds money (deposits) that people put into the bank account.

- They keep it safe and also lend it to businesses or other people.

- In return, banks give depositors extra money over a regular period (quarterly, monthly, or annually) in the form of interest.

- Interest is the amount charged for borrowing money or the amount gained by lending money, usually expressed as a percentage.

- This helps the amount of saved money grow over time.

- Through this, banks encourage individuals to save.

Types of Bank Accounts

1. Savings Account

- This account is for individuals who save regularly and earn interest on such savings.

- It opens with a minimum deposit and allows money to be added or withdrawn.

- There are limits on how often the depositor can withdraw each month.

2. Current Account

- This account is for businesses and traders who often make and receive payments.

- It doesn't earn interest.

- Generally, there are no limits on how many times money can be deposited or withdrawn.

3. Fixed Deposit Account

- This is a one-time deposit kept for a fixed period (like 3 or 5 years).

- After that time, the bank returns the original amount plus interest.

- Interest is usually higher than what a savings account offers.

Understanding Compound Interest

- Example: You deposit ₹1,000 in your account.

- The bank pays 6% interest each year if you don't withdraw it.

- At the end of one year: ₹1,000 + 6% of ₹1,000 = ₹1,000 + ₹60 = ₹1,060

- If you don't spend this money next year, you earn interest on ₹1,060 (not just ₹1,000).

- Interest in second year: 6% of ₹1,060 = ₹63.60

- Total at end of second year: ₹1,060 + ₹63.60 = ₹1,123.60

- You earn interest not just on the original amount but on the amount including interest earned in previous years.

- This process is called compounding.

- If you continue saving for 12 years, your money will grow to ₹2,012.20.

- Compounding is a powerful financial concept that helps money grow exponentially over time.

The Magic of Compounding - Story of a King and a Sage

- A king from Ambalappuzha, Kerala, loved chess and challenged a visiting sage to a game.

- The sage asked for a simple reward: one grain of rice on the first square of the chessboard, two on the second, four on the third, doubling each time for all 64 squares.

- The king agreed, thinking it was a small demand.

- But as grains kept doubling, the total grew significantly.

- By the 8th square: 128 grains

- By the 16th square: 32,768 grains

- By the 32nd square: over 210 crore!

- The king realized how powerful exponential growth can be.

- This story shows how compounding works and how small amounts can grow into large sums over time.

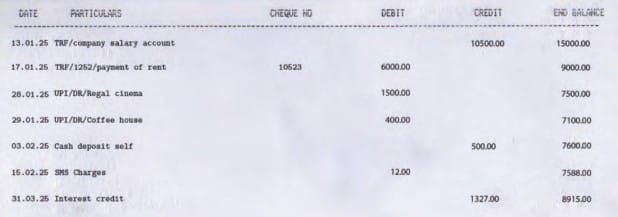

Passbook

- The bank provides a diary-like document called a passbook that keeps a record of all receipts and payment transactions.

- It can be updated regularly at the bank.

- Debit: Taking money out of an account (expenses)

- Credit: Receiving money in an account (income)

- Keeping records of financial transactions is important for tracking money flow.

Offer Loans or Credit

- A loan is an amount borrowed from banks or financial institutions, with the obligation to repay it with interest at a later time.

- Banks lend money to borrowers as loans for specific purposes:

- Buying a house or vehicle

- Funding education

- Business purposes (purchasing machinery, raw materials, transporting products, launching new products) - Just as banks pay interest on savings to depositors, they charge interest from borrowers on the loans they provide.

- After a specified period, the borrower repays the loan amount along with the interest.

Don't Miss Out

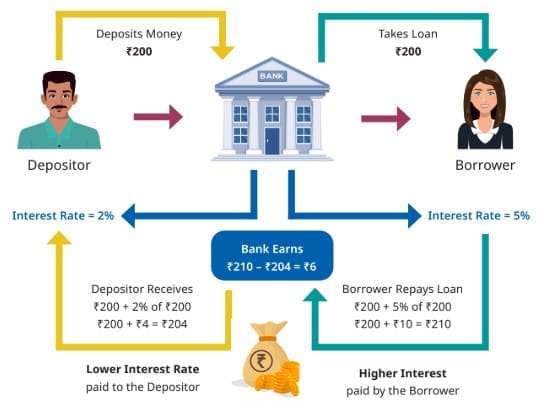

- Banks pay lower interest rates on savings deposits to depositors.

- They charge higher interest rates on loans from borrowers.

- This difference in interest rate is a source of income for banks.

Example:

- Anand deposits ₹200 in his bank account.

- Bank offers an interest rate of 2% on his savings.

- Bank lends ₹200 to Shreya and charges an interest rate of 5%.

- Shreya repays ₹10 (5% of ₹200) as interest along with original loan amount of ₹200 = ₹210 total.

- Bank pays ₹4 (2% of ₹200) to Anand as interest.

- Bank earns ₹210 - ₹204 = ₹6.

- Note: Banks have reserve money and do not lend all deposits as loans.

How banks make money

How banks make money

Jan Dhan Yojana

- Before 2014, only 15 crore Indians had bank accounts; most relied on cash.

- Pradhan Mantri Jan Dhan Yojana was launched in 2014.

- Aimed to give every Indian, especially low-income earners, access to a bank account.

- No minimum balance or fees required.

- Since then, over 50 crore accounts have been opened (mainly by women).

- Now banking services are used by people from all walks of life.

Benefits:

- Farmers borrow money to start small business or expand agricultural activities

- Workers receive wages directly into bank accounts

- Students receive scholarships directly into accounts

- Direct transfers have reduced middlemen and ensure timely disbursement of funds

Other Financial Institutions

Post Offices

- Indian post offices offer a variety of financial services.

- Include savings schemes like:

- National Savings Certificates (NSC)

- Kisan Vikas Patra accounts

- Sukanya Samriddhi accounts - Their vast network and presence, even in remote locations, make them a popular savings option.

Others

- Industrial Finance Corporation of India: Funds businesses in areas like power and textiles

- National Bank for Agriculture and Rural Development (NABARD): Supports rural development by funding banks that give loans for farming, village industries, and infrastructure (roads, irrigation)

Reserve Bank of India (RBI) - Banker to Banks

- The Reserve Bank of India (RBI) is the bank that supervises the Indian banking system.

- It is also called India's central bank.

- Countries have central banks which supervise and manage policies related to their banking system.

- RBI was established in 1935 and performed some functions of a central bank.

- After Independence, RBI was transferred to the Government of India.

- It has been functioning as the banker of banks, the central bank, since 1949.

- Maintains accounts of other banks

- Facilitates exchange of funds between banks

- Provides loans to banks and the government

Sets rules and regulations regarding:

- Printing and distributing Indian currency (banknotes)

- Fixing of the benchmark interest rate (the base interest rate that RBI fixes for lending money to commercial banks)

- The entrance of the RBI office in Delhi is flanked by statues of a yakṣha and yakṣhi.

- According to Hindu mythology, yakṣhas are demigods who act as guards of treasures for Kubera, the God of Wealth.

- RBI could be compared to Kubera, with its sole right of issuing currency and being a banker to banks.

Payment Modes and Systems

- Payment modes and systems are another key part of financial infrastructure.

- They help with the transfer of money from one person to another.

- Payment system: A mechanism that facilitates the clearing and settlement of financial transactions, allowing individuals, businesses, and organisations to transfer funds between each other.

How to Withdraw Cash from Bank Deposits

Method 1: Withdrawal Slip at Bank

- Fill out a withdrawal slip at the bank.

- Submit it at the cash counter.

- Withdraw cash from the account.

Method 2: Debit Card and ATM

- Banks provide debit cards to customers when they open an account.

- Debit cards can be used to withdraw cash from Automated Teller Machines (ATMs) at any time.

- These self-service machines are like mini-banks, available 24×7 at public places (bus depots, shopping markets, railway stations, airports, malls).

Steps to withdraw cash: 1. Insert debit card into the machine

1. Insert debit card into the machine

2. Input the PIN (Personal Identification Number - a numeric code, usually 4 to 6 digits, used for authentication and security)

3. Type amount to be withdrawn

4. Collect cash

How can money is transferred from one bank account to another

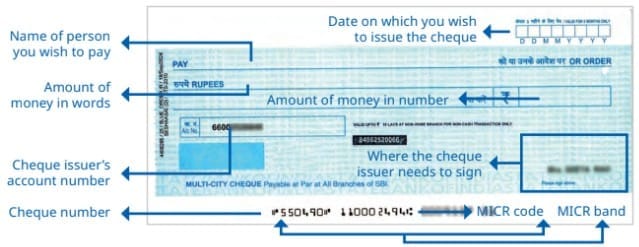

Cheque

- A cheque is a paper instrument that allows you to pay someone directly from your bank account.

- The bank provides a cheque book with multiple cheques.

- Process:

- To pay ₹5,000 to your friend Rohan, you write a cheque with the exact amount, Rohan's name, and your signature

- Rohan can then deposit the cheque in his bank

- The amount gets withdrawn (debited) from your account and transferred (credited) to Rohan's bank account - Limitation: Transfer through cheque requires physically visiting a bank and takes time.

Electronic Payment Methods

Electronic modes of payment allow instant transfers from sender's account to receiver's account.

Debit Cards and Point of Sale (POS) Machines

- Debit cards can be used to make payments at retail stores (grocery, clothing store, chemist).

- They help withdraw cash from ATMs (as seen above).

- They enable transfer of money from customers to store owner.

- Process:

- Customers use their debit card by swiping or inserting it into a POS machine

- Input the amount and enter the PIN

- Cashier can also enter the amount while customer enters PIN

- Amount is instantly deducted from customer's account

Internet Banking (Netbanking)

- Another electronic tool for transferring money.

- Allows account holders to:

- Check balances and transaction history

- Transfer money - Done through the bank's website or mobile application using a computer or smartphone.

Mobile Payments

- Digital payments are made through mobile phones using digital payment applications such as BHIM.

- Based on the Unified Payments Interface (UPI) payment system.

- UPI enables easier and quicker digital money transfers using a QR code or phone number of the recipient.

- Allows quick payments and receipts.

- Reduces the need for physical passbook updates.

- Allows users to check balances and track transactions anytime on their phone.

Unified Payments Interface (UPI) - India's Gift to the World

- Traditionally, transferring funds required:

- Filling out cheque with receiver's details

- Dropping it into bank's drop box or handing it to a bank official - It was time-consuming.

- Discouraged majority of people from using banking services.

- Led to heavy reliance on cash.

- Billions of rupees were used every day without a record.

Launch of UPI

- This changed in 2016 when the National Payments Corporation of India (NPCI) launched UPI.

- UPI is a fast and secure digital payment system that enables transfer of funds.

How UPI Works: Example

- Kumar scans Piyush's (a vegetable vendor) QR code using a payment application on his phone.

- Enters his UPI PIN and the amount to be sent.

- Process:

- The application sends a payment request to Kumar's bank

- Kumar's bank forwards the request to NPCI

- NPCI decrypts the request, verifies the user's UPI PIN, and processes the transfer

- Funds are received by Piyush's bank

- Piyush receives the payment in his bank account

Benefits of UPI

- Allows effortless digital transactions.

- During COVID-19 pandemic, UPI gained popularity for supporting cashless transactions (social distancing was essential).

- User-friendly design in multiple languages makes it accessible to everyone.

Think About It

- India's digital payments revolution is expanding rapidly across borders.

- Nepal was the first country to adopt India's UPI as a payment platform in 2022.

- Today, nations such as United Arab Emirates, France, Sri Lanka, Bhutan, Mauritius have adopted it.

- More countries are increasingly showing interest.

- This instant, efficient, and secure system is truly India's gift to the world of payment systems.

Stock Market

- A share is a unit of ownership in a company, representing a portion of its capital stock.

- When you buy a share of a company, you become a part-owner of that company due to your investment (the act of putting resources in assets expected to gain value over time).

- The more shares you own, the higher your ownership.

- A collection of shares can be referred to as a stock.

Example: Restaurant Business

- Suppose you own a small restaurant and wish to expand it with a variety of cuisines.

- If you do not have enough money, you can borrow it from friends in exchange for a share of profits.

- They become part-owners of your business.

- Similarly, when you buy a share of a company, you become a part-owner.

Purpose

- For individuals: Holding stocks allows individuals to put their savings where they expect to see an increase in value when share price increases.

- For companies: Issuing shares helps companies raise funds for their operations.

Stock Exchange

Bombay Stock Exchange

Bombay Stock Exchange

- The actual buying and selling of shares takes place at the stock exchange (marketplace where financial securities like stocks are traded).

- In India, the Bombay Stock Exchange (BSE) was established in 1875.

- It is one of the oldest stock exchanges in the world.

- Back then, share transactions were conducted manually using paper tickets.

- In the modern world, these have been replaced by digital transactions using advanced computers and other devices.

Share Price Fluctuations

- Like commodity prices, share prices also rise and fall.

- Stock market crash: When share prices of many companies fall simultaneously.

- Stock market boom: When share prices of many companies rise simultaneously.

- Trading shares can bring gains or losses as their prices fluctuate due to many factors.

Factors Affecting Share Prices

Company Performance

- If a company is doing well and people think it will earn money, its shares become more valuable.

- If the company has problems (bad product, workers' strike, big loss), fewer people want its shares, so price drops.

External Factors

- Government's policy changes (new laws, tax rules - compulsory contribution to government on income and profit)

- Political instability, wars

- Economic shocks (sudden unexpected events causing big changes in economy - natural disasters, pandemic, sudden changes in government policies, commodity prices)

Financial Frauds and How to Prevent Them

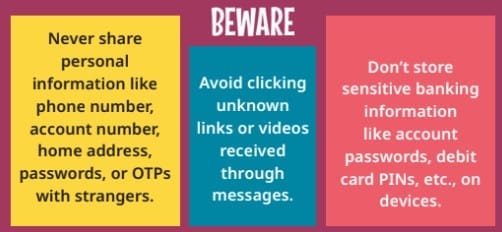

Digital payments have made life easier, but users must beware of fraud and scams.

Fraudsters trick people through:

- Fake calls or messages

- Downloading harmful apps

Misleading people into sharing bank details or One-Time Passwords (OTPs - unique temporary code of letters or numbers used for verifying identity or authorising transactions)

- This gives them access to user's mobile or computer.

- Enables them to steal personal data from device and drain money from bank accounts.

- In case of fraud: Report via helpline 1930 or the National Cybercrime Reporting Portal

FAQs on Chapter Notes: Banks and the Magic of Finance

| 1. What is financial infrastructure? |  |

| 2. What are the main functions of banks? | |

| 3. What types of bank accounts can individuals open? | |

| 4. What is the Jan Dhan Yojana? | |

| 5. How does the Unified Payments Interface (UPI) work? | |