Commerce Exam > Commerce Notes > Accountancy Class 12 > Infographic: Dissolution of a Partnership Firm

Infographic: Dissolution of a Partnership Firm

The document Infographic: Dissolution of a Partnership Firm is a part of the Commerce Course Accountancy Class 12.

All you need of Commerce at this link: Commerce

FAQs on Infographic: Dissolution of a Partnership Firm

| 1. What are the primary reasons for the dissolution of a partnership firm? |  |

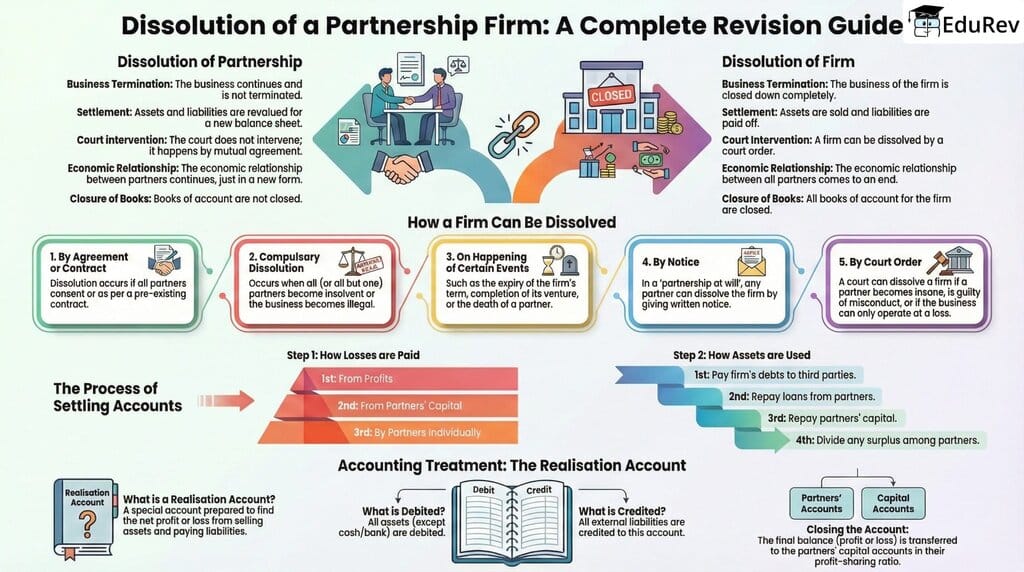

Ans. The dissolution of a partnership firm can occur for several reasons, including mutual consent among partners, expiration of the partnership tenure, completion of the business objective, insolvency or bankruptcy of the firm, or the death or incapacity of a partner. Additionally, certain legal issues or disputes can also lead to dissolution.

| 2. What steps are involved in the dissolution process of a partnership firm? | |

Ans. The dissolution process typically involves several steps: first, the partners must agree on the terms of dissolution. Next, they should notify all stakeholders, including creditors and employees. Following this, the firm's assets need to be liquidated, and liabilities must be settled. Finally, a formal deed of dissolution should be executed, and necessary filings with regulatory authorities should be completed.

| 3. How are assets and liabilities distributed upon dissolution of a partnership firm? | |

Ans. Upon dissolution, the assets of the partnership are first used to pay off any outstanding debts and liabilities. After all creditors have been settled, any remaining assets are distributed among the partners according to the profit-sharing ratio specified in the partnership agreement. If no such ratio exists, the assets will be divided equally among the partners.

| 4. What legal documentation is required for the dissolution of a partnership firm? | |

Ans. The primary legal documentation required includes a deed of dissolution, which outlines the terms of the dissolution and any agreements made between the partners. Additionally, any regulatory filings or notifications to creditors and stakeholders must be documented. It is also advisable to prepare a final account statement summarising the firm's financial position at the time of dissolution.

| 5. What are the consequences of a partner withdrawing from a partnership before its dissolution? | |

Ans. If a partner withdraws from a partnership before official dissolution, it may result in the need to settle the withdrawing partner's share of the assets and liabilities. The remaining partners may need to negotiate new terms for the partnership or decide on the continuation of the business. The withdrawal can also create legal complications, depending on the partnership agreement and local laws, necessitating proper documentation and possibly a formal dissolution process.

About this Document

4.94/5 Rating

Apr 26, 2026 Last updated

Related Exams

Document Description: Infographic: Dissolution of a Partnership Firm for Commerce 2026 is part of Accountancy Class 12 preparation. The notes and questions for Infographic: Dissolution of a Partnership Firm have been prepared according to the Commerce exam syllabus. Information about Infographic: Dissolution of a Partnership Firm covers topics like and Infographic: Dissolution of a Partnership Firm Example, for Commerce 2026 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Infographic: Dissolution of a Partnership Firm.

Introduction of Infographic: Dissolution of a Partnership Firm in English is available as part of our Accountancy Class 12 for Commerce & Infographic: Dissolution of a Partnership Firm in Hindi for Accountancy Class 12 course. Download more important topics related with notes, lectures and mock test series for Commerce Exam by signing up for free. Commerce: Infographic: Dissolution of a Partnership Firm

Description

Infographic: Dissolution of a Partnership Firm of Accountancy Class 12 provides you one-page visual summary of the chapter covering all the important topics. Download the PDF from EduRev.

Information about Infographic: Dissolution of a Partnership Firm

In this doc you can find the meaning of Infographic: Dissolution of a Partnership Firm defined & explained in the simplest way possible. Besides explaining types of Infographic: Dissolution of a Partnership Firm theory, EduRev gives you an ample number of questions to practice Infographic: Dissolution of a Partnership Firm tests, examples and also practice Commerce tests

Related Searches

video lectures, Infographic: Dissolution of a Partnership Firm, shortcuts and tricks, Summary, Extra Questions, practice quizzes, study material, MCQs, Important questions, Infographic: Dissolution of a Partnership Firm, pdf , ppt, Previous Year Questions with Solutions, Exam, Objective type Questions, Infographic: Dissolution of a Partnership Firm, mock tests for examination, Semester Notes, Viva Questions, past year papers, Free, Sample Paper;