Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Bill, 2025

The Sabka Bima Sabki Raka Amendment of Insurance Laws Bill 2025

The program opens with an introduction to the Sabka Bima Sabki Raka Amendment of Insurance Laws Bill 2025, which marks a transformative shift in India's insurance sector by amending three key legislations:

- The Insurance Act, 1938

- The Life Insurance Corporation Act, 1956

- The Insurance Regulatory and Development Authority Act, 1999

Key features of the bill include:

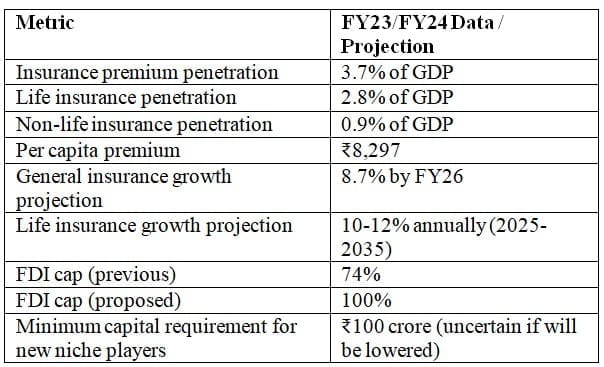

- Raising the Foreign Direct Investment (FDI) cap from 74% to 100% in Indian insurance companies, with a stipulation that one of the top leadership roles (Chairman, Managing Director, or CEO) must be held by an Indian citizen to ensure domestic control.

- Empowering the Insurance Regulatory and Development Authority (IRDA) with new powers to recover wrongful gains.

- Granting greater operational autonomy to the Life Insurance Corporation of India (LIC), including the ability to open zonal offices and manage overseas operations in compliance with local laws.

Insurance penetration in India remains low at 3.7% of GDP (FY24), with life insurance at 2.8% and non-life at 0.9%. Per capita premium was ₹8,297 in FY23. Growth projections indicate:

- General insurance expected to grow at 8.7% by FY26

- Life insurance projected to grow 10-12% annually between 2025-2035

Positioning India as the second largest life insurance market in the region.

Expert Views on the Amendments and Impact on Insurance Landscape

Mr. Suresh Matur, former Executive Director IRDA, emphasizes:

- The amendments are essential to achieve the government's goal of 'Insurance for All by 2047'.

- Increasing FDI to 100% will bring more capital inflows, enhance competition, and drive product innovation.

- IRDA's enhanced powers to recover wrongful gains shift the regulatory approach from mere penalties to real accountability.

- LIC gains operational autonomy, enabling faster decision-making such as opening zonal offices without government approval.

- The bill supports market expansion and penetration, especially in underserved rural areas, facilitated by digital approaches.

Increasing Insurance Access in Rural and Underserved Areas

Dr. Casey Haridas, PhD Insurance Flei, highlights:

- The increase in FDI limit is a welcome step to attract foreign investment and bring global best practices in underwriting, claims settlement, and technology.

- This will likely boost insurance penetration significantly within 3 to 5 years.

- Foreign investors view India as a developing insurance market with potential to grow penetration from current ~4% to possibly 10% of GDP by 2047.

- New foreign entrants are expected to introduce product diversity and technological upgrades.

Impact of 100% FDI on Competitiveness, Stability, and Associated Risks

Mr. Matur explains:

- 100% FDI will attract more foreign players, removing joint venture constraints, and enable freer introduction of innovative products, particularly in health and specialized insurance sectors.

- More capital will help insurers expand reach in rural areas via digital tools or physical offices.

- The bill safeguards domestic control by mandating that top leadership positions (CEO, Chairman, MD) be held by Indian citizens, mitigating risks of market dominance and profit repatriation.

- Potential risks include:

- Market dominance by large foreign players potentially marginalizing smaller competitors.

- Foreign firms prioritizing high-margin urban segments instead of rural outreach.

- Strong regulatory oversight is expected to ensure inclusive growth and market stability.

Consumer Protection and Accountability Enhancements

Dr. Haridas notes:

- The bill establishes a fund by IRDA dedicated to policyholder education, addressing a key gap in awareness and understanding of insurance products.

- Transition from a statutory penalty regime to a regulator-controlled regime enhances IRDA's powers to protect policyholders, insurers, and intermediaries.

Mr. Matur adds:

- Previous penalties only fined insurers but did not compensate affected policyholders directly.

- The new powers allow IRDA to recover wrongful gains and return them to rightful claimants, fostering greater trust and transparency.

- This change is expected to create a more transparent and trustworthy insurance environment.

Concerns on Overregulation and Innovation

Dr. Haridas addresses concerns:

- The bill is not expected to lead to overregulation, as regulatory checks and balances are necessary in the insurance sector.

- The current IRDA leadership is proactive, and the regulatory regime aims to favor policyholders, especially given many grievances filed in health insurance.

- The fear of penalties should encourage insurers to improve customer service and compliance without stifling innovation.

Operational Autonomy for LIC

Mr. Matur explains:

- LIC's board receives significant autonomy, for example, to open offices independently in underpenetrated regions like the Northeast, without needing government approvals which previously caused delays.

- This flexibility allows LIC to expand faster, respond swiftly to market needs, and maintain its extensive reach, especially in areas private players may not cover.

Challenges and Collaborative Solutions to Achieving Insurance for All by 2047

Dr. Haridas suggests:

- Insurers should develop innovative, customer-friendly products to attract wider segments.

- The regulator can facilitate this by easing the 'file and use' product approval process.

- Foreign entrants are expected to bring advanced products and generate significant employment opportunities in underwriting, claims, sales, and technical roles.

- Licensing reforms for surveyors and loss assessors will also boost employment and service quality.

Competition Between LIC and Private Players

Mr. Matur states:

- LIC, despite increased competition from private and foreign players, is well equipped to compete due to its unmatched reach and brand strength.

- The new autonomy granted by the bill will help LIC innovate and enhance its offerings, ensuring it remains competitive in the evolving market.

Comparison with Global Insurance Markets and Regulatory Framework

Dr. Haridas compares:

- India's regulatory framework is clear, objective, and superior compared to several countries including UAE and African nations, focusing on policyholder protection and industry development.

- The bill continues to align India's insurance regulation with global best practices, facilitating industry growth.

Digital Transformation and Inclusion

Dr. Haridas highlights:

- India is one of the most digitally empowered societies, with Aadhaar, UPI, and linked bank accounts facilitating easy access to insurance products.

- Common citizens can use online platforms or local Customer Service Centres (CSCs) to purchase insurance, reducing the risk of digital exclusion.

- This digital-first approach supports the goal of insurance for all, including rural and less tech-savvy populations through assisted access points.

Reforms in Licensing for Insurance Intermediaries

Dr. Haridas explains:

- The bill proposes one-time registration for insurance intermediaries (agents and brokers), replacing the current renewal every three years with extensive documentation.

- This reform will allow intermediaries to focus more on client servicing rather than administrative compliance, improving efficiency and service quality.

Future Outlook: India's Insurance Industry in 5-10 Years

Mr. Matur predicts:

- The bill's provisions will have a far-reaching positive impact, driving industry growth and enhancing customer protection.

- The introduction of the 'Beimma Sugam' platform will create an accessible marketplace where consumers can buy insurance products from multiple companies seamlessly.

- India's tech-savvy population is likely to embrace these digital innovations, accelerating insurance penetration and modernization.

Raising Public Awareness and Education on Insurance

Dr. Haridas recommends:

- Similar to SEBI's mandate on mutual fund education, insurance companies should be required to allocate a dedicated budget for policyholder education.

- This will increase awareness about insurance benefits and help build trust.

- The bill's provisions inviting niche players (e.g., cyber insurance) are positive but the minimum capital requirement of ₹100 crore may need reassessment to encourage innovation and entry.

Conclusion

The bill represents a transformative and inclusive step for the insurance sector in India by:

- Increasing FDI limits to attract foreign capital and expertise

- Enhancing consumer protection and accountability

- Expanding insurance coverage to underserved populations

- Empowering LIC and intermediaries with greater autonomy and operational flexibility

- Encouraging digital innovation and market competition

Together, these changes aim to shape a robust, customer-centric, and growth-oriented insurance industry, aligning with the government's vision of universal insurance coverage by 2047.

Quantitative Data Summary

Key Terms and Concepts

- Sabka Bima Sabki Raka Bill 2025: Amendment bill aiming to reform insurance laws in India.

- FDI (Foreign Direct Investment): Increase from 74% to 100% to enhance capital inflows and competition.

- IRDA (Insurance Regulatory and Development Authority): Insurance regulator empowered with new powers for accountability and consumer protection.

- LIC (Life Insurance Corporation of India): State-owned insurer granted operational autonomy.

- Beimma Sugam platform: Proposed marketplace for insurance products to enhance accessibility.

- Policyholder Education Fund: New fund to promote awareness and understanding of insurance products.

- One-time registration for intermediaries: Simplification of licensing for agents and brokers.

Key Insights

- The bill aims to transform India's insurance sector by balancing foreign investment with domestic control.

- Consumer protection is strengthened through mechanisms allowing recovery of wrongful gains to policyholders, beyond mere penalties on insurers.

- Digital innovation and expansion into underserved rural areas are prioritized to increase penetration and inclusivity.

- LIC's enhanced autonomy is critical for it to maintain competitiveness amid increasing private and foreign players.

- Regulatory reforms will encourage innovation, employment, and ease of doing business for intermediaries.

- Collaboration between government, regulators, and insurers is essential to raise public awareness and achieve the vision of insurance for all by 2047.

FAQs on Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Bill, 2025

| 1. What is the purpose of the Sabka Bima Sabki Raksha Amendment of Insurance Laws Bill? |  |

| 2. How does the amendment aim to increase insurance access in rural areas? | |

| 3. What impact does the introduction of 100% Foreign Direct Investment (FDI) have on the insurance sector? | |

| 4. What consumer protection measures have been enhanced under the amendment? | |

| 5. What are the concerns regarding overregulation and its impact on innovation in the insurance sector? | |