Saving Money

Saving money is the practice of setting aside a portion of income or pocket money for future use instead of spending it immediately. For students, developing saving habits early builds financial discipline and prepares them for managing larger financial responsibilities in adulthood. Understanding saving methods and goals is essential for effective money management.

1. Meaning of Saving

Saving refers to the act of keeping money aside from current income or allowance for future needs and wants. It is the difference between income received and expenditure made.

- Definition: Saving = Income - Expenditure. Money not spent immediately is considered saved.

- Purpose: Savings serve as a financial cushion for emergencies, planned purchases, or future investments.

- Student Context: For students, income includes pocket money, gifts, rewards, or earnings from small tasks.

- Key Principle: Regular small savings accumulate over time to create substantial amounts through consistency.

2. Why Students Should Save

Developing saving habits during student years establishes lifelong financial responsibility and independence. There are several compelling reasons for students to start saving early.

- Emergency Preparedness: Unexpected expenses like lost stationery, broken items, or urgent needs can be met without seeking help.

- Goal Achievement: Saving enables purchasing desired items like books, games, sports equipment, or gadgets independently.

- Financial Independence: Reduces dependency on parents or guardians for every small need or want.

- Learning Responsibility: Managing savings teaches decision-making, planning, and delayed gratification.

- Building Habits: Early practice of saving creates disciplined financial behavior that continues into adulthood.

- Understanding Value: Saving teaches the real value of money and the effort required to earn it.

3. Benefits of Saving Early

Starting to save at a young age provides both immediate and long-term advantages. Early savers develop skills and accumulate resources that compound over time.

3.1 Immediate Benefits

- Financial Security: Creates a safety net for unexpected needs without borrowing from others.

- Purchase Power: Enables buying desired items through own resources, building self-confidence.

- Stress Reduction: Having savings reduces anxiety about money-related problems or emergencies.

- Decision-Making Skills: Regular saving requires prioritizing needs over wants, strengthening judgment.

3.2 Long-Term Benefits

- Compound Growth: Money saved in interest-bearing accounts grows over time through earned interest on principal and interest.

- Habit Formation: Neural pathways for financial discipline form more easily during youth, lasting lifetime.

- Future Opportunities: Accumulated savings can fund higher education, skill development, or business ventures later.

- Financial Literacy: Early savers naturally learn about banking, interest rates, and financial planning concepts.

- Wealth Building Foundation: Early start provides more time for savings to grow exponentially through compounding effect.

3.3 Time Value of Money

Money saved early is worth more than the same amount saved later due to growth potential.

- Example: ₹1,000 saved at age 10 with 5% annual interest becomes ₹1,629 by age 20.

- Comparative Disadvantage: ₹1,000 saved at age 15 with 5% annual interest becomes only ₹1,276 by age 20.

- Key Learning: Starting early, even with small amounts, yields better results than starting late with larger amounts.

4. Saving Methods

Various practical methods exist for students to save money safely and systematically. Choosing appropriate methods depends on age, saving goals, and parental support available.

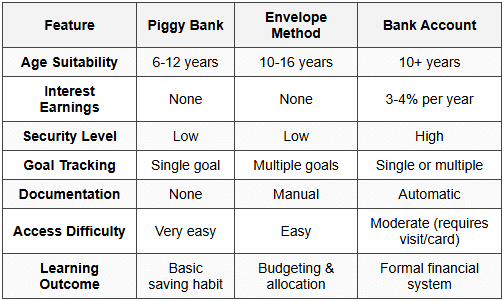

4.1 Piggy Bank Method

A piggy bank is a container used to store coins and small currency notes. It is the most basic and traditional saving tool.

- Suitable For: Younger students (ages 6-12) learning basic saving concepts.

- Advantages: Visual reminder of savings progress; physically seeing money grow motivates continued saving; no paperwork required.

- Limitations: No interest earned; money remains idle; risk of theft or misplacement; temptation to break open for spending.

- Best Practice: Empty and count savings weekly; transfer larger amounts to safer storage methods periodically.

- Variants: Transparent jars (show progress visually), multiple containers (separate savings by goal), locked boxes (reduce temptation).

4.2 Envelope Method

The envelope method involves dividing money into different envelopes labeled for specific purposes or savings goals.

- Process: Create labeled envelopes for different categories like "Emergency Fund," "Books," "Gifts," or "Long-term Savings."

- Allocation: Distribute incoming money (pocket money, gifts) across envelopes according to predetermined percentages or amounts.

- Suitable For: Students aged 10-16 managing multiple financial goals simultaneously.

- Advantages: Clear goal visualization; prevents mixing of funds; teaches budgeting and allocation skills; flexible and customizable.

- Recommended Distribution: 50% spending, 30% short-term savings, 20% long-term savings (adjust based on personal needs).

- Limitations: Physical cash required; no interest earnings; requires discipline to maintain system; vulnerable to loss or damage.

4.3 Bank Account Method

A savings bank account is a formal banking facility where money is deposited and earns interest over time.

4.3.1 Types of Student Accounts

- Minor Savings Account: Operated jointly with parent/guardian for children under 10 years; teaches banking basics.

- Independent Minor Account: Available for ages 10-18; student operates account with some parental oversight.

- Student Savings Account: Specialized accounts with zero or minimal balance requirements and educational benefits.

4.3.2 Advantages of Bank Accounts

- Interest Earnings: Money deposited earns interest (typically 3-4% annually), making savings grow automatically.

- Security: Bank deposits protected by insurance up to ₹5,00,000 under Deposit Insurance and Credit Guarantee Corporation (DICGC).

- Formal Records: Passbook and statements provide clear tracking of deposits, withdrawals, and interest earned.

- Banking Literacy: Students learn practical banking operations, digital transactions, and financial documentation.

- Reduced Temptation: Physical distance from money reduces impulsive spending compared to cash at home.

- Foundation Building: Establishes banking relationship and credit history useful for future financial needs.

4.3.3 Important Features

- Minimum Balance: Student accounts typically have zero or very low (₹100-500) minimum balance requirements.

- Withdrawal Limits: May have restrictions on frequency or amount of withdrawals to encourage saving habit.

- ATM/Debit Card: Many banks issue cards to older students (12+) for supervised usage and emergency access.

- Internet Banking: Online access allows monitoring balance and transactions, teaching digital financial management.

4.4 Comparison of Saving Methods

5. Short-Term and Long-Term Savings Goals

Effective saving requires clear goals categorized by time horizon. Savings goals are specific targets for which money is being accumulated.

5.1 Short-Term Savings Goals

Short-term goals are targets achievable within days, weeks, or up to one year. These provide quick satisfaction and reinforce saving habits.

- Definition: Financial objectives achievable within 1-12 months through regular small savings.

- Characteristics: Specific amount required; clear timeline; immediate or near-future benefit; motivates consistent saving.

5.1.1 Examples of Short-Term Goals

- School Supplies: Saving ₹200-500 for new geometry box, art materials, or calculator needed next month.

- Books and Entertainment: Accumulating ₹300-800 for buying favorite storybook series or video game within 2-3 months.

- Birthday Gifts: Setting aside ₹150-400 monthly for giving gifts to friends or family members.

- School Trip: Collecting ₹500-2,000 over 3-6 months for participating in educational excursion or picnic.

5.1.2 Planning Short-Term Savings

- Identify Goal: Clearly define what you want to buy or achieve with specific details.

- Calculate Cost: Determine exact or approximate amount needed including any additional expenses.

- Set Timeline: Decide target date by when you need the money saved completely.

- Determine Weekly/Monthly Amount: Divide total cost by number of weeks/months to find required saving rate.

- Track Progress: Monitor savings weekly to ensure staying on track toward goal.

5.2 Long-Term Savings Goals

Long-term goals require sustained effort over months or years. These build patience, discipline, and create substantial financial resources.

- Definition: Financial objectives requiring 1-10+ years of consistent saving and patience.

- Characteristics: Large amounts involved; extended timelines; significant life benefits; requires strong commitment and discipline.

5.2.1 Examples of Long-Term Goals

- Higher Education: Saving ₹10,000-50,000 over 2-5 years for college fees, entrance exam coaching, or vocational courses.

- Electronic Gadgets: Accumulating ₹15,000-40,000 over 1-3 years for laptop, tablet, or smartphone needed for studies.

- Bicycle/Two-Wheeler: Collecting ₹5,000-20,000 over 1-2 years for purchasing personal transportation vehicle.

- Skill Development: Saving ₹8,000-25,000 over 1-3 years for learning courses like coding, music, sports training, or language classes.

5.2.2 Planning Long-Term Savings

- Define Clear Vision: Write down specific goal with detailed description of what, why, and when.

- Research Actual Costs: Investigate current prices and estimate future costs considering inflation (3-5% annual increase).

- Break into Milestones: Divide total goal into quarterly or yearly milestones to maintain motivation.

- Automate Savings: Set fixed amount to save immediately upon receiving pocket money before any spending.

- Review Quarterly: Assess progress every 3 months and adjust saving rate if needed based on changed circumstances.

- Consider Interest: Factor in interest earnings if using bank account; this reduces required monthly saving amount.

5.3 Balancing Short-Term and Long-Term Goals

Effective money management requires maintaining both goal types simultaneously without compromising either.

- Allocation Strategy: Divide savings between short-term (40-50%) and long-term (50-60%) goals based on priorities.

- Flexibility Principle: Adjust allocation when short-term goal is achieved; redirect that portion to long-term savings.

- Emergency Reserve: Always maintain 10-20% of total savings as emergency fund accessible for unexpected needs.

- Priority System: Rank goals by importance (needs before wants) and urgency (deadline-driven before flexible ones).

5.3.1 Sample Goal-Based Savings Plan

Example for student receiving ₹500 monthly pocket money:

- Immediate Spending: ₹200 (40%) for snacks, stationery, daily needs.

- Short-Term Savings: ₹120 (24%) for book purchase goal in 3 months (₹360 total).

- Long-Term Savings: ₹150 (30%) for laptop goal in 3 years (₹5,400 + interest).

- Emergency Fund: ₹30 (6%) kept separate for unexpected urgent needs.

6. Common Mistakes and Trap Alerts

Students often make predictable errors when starting their saving journey. Awareness of these pitfalls helps avoid them.

- Trap 1 - No Clear Goals: Saving "for the future" without specific targets leads to loss of motivation and impulsive withdrawals. Always define clear, specific goals with amounts and dates.

- Trap 2 - Saving What's Left: Planning to save whatever remains after spending usually results in zero savings. Correct approach: Save first immediately upon receiving money, then spend from remainder.

- Trap 3 - Unrealistic Targets: Setting overly ambitious saving rates (like 90% of pocket money) causes failure and discouragement. Start with achievable 20-30% rate and increase gradually.

- Trap 4 - Frequent Goal Changes: Constantly switching saving goals before achieving them wastes effort and creates frustration. Commit to one goal until completion before changing priorities.

- Trap 5 - No Emergency Buffer: Using all savings for planned goals leaves nothing for emergencies, forcing borrowing or abandoning goals when urgent needs arise.

- Trap 6 - Comparing with Others: Feeling inadequate because peers save more or have larger pocket money demotivates personal progress. Focus on individual growth and consistency regardless of amounts.

- Trap 7 - Ignoring Interest: Keeping large long-term savings in piggy bank instead of interest-bearing bank account results in significant opportunity loss over years.

7. Building a Sustainable Saving Habit

Consistency matters more than amount in developing lifelong saving behavior. Several practices strengthen saving discipline over time.

7.1 Psychological Techniques

- Visual Progress Tracking: Maintain savings chart or graph showing growth over time; visual achievement motivates continued effort.

- Reward Milestones: Celebrate reaching 25%, 50%, 75% of goal with small non-monetary rewards (special activity, privilege).

- Accountability Partner: Share goals with parent, sibling, or friend who regularly checks progress and provides encouragement.

- Delay Gratification Practice: When tempted to spend, implement "48-hour rule" - wait two days before deciding; often desire fades.

7.2 Practical Strategies

- Automate Process: Create routine of immediately separating savings amount the moment you receive money before doing anything else.

- Increase Gradually: Start with comfortable 20% saving rate; increase by 5% every 3 months as habit strengthens.

- Capture Windfalls: Save 50-70% of unexpected money (gifts, rewards, found money) since it wasn't in spending plans.

- Round-Up Method: When spending, round up to next ₹10 and save the difference (₹7 purchase → pay ₹10, save ₹3).

- Weekly Review Ritual: Set specific day and time each week to count, record, and review savings progress consistently.

Saving money is a fundamental financial skill that students can begin practicing immediately regardless of age or pocket money amount. Starting with simple methods like piggy banks and progressing to formal bank accounts builds confidence and competence. Clear short-term goals provide quick wins that motivate continued effort, while long-term goals develop patience and discipline essential for adult financial success. The key to effective saving lies not in the amount saved but in the consistency of the habit. Students who learn to save regularly, even small amounts, establish financial behaviors that compound into significant advantages throughout their lives. Regular practice of these saving principles transforms money management from a challenge into a natural, rewarding skill.

FAQs on Saving Money

| 1. What is the meaning of saving? |  |

| 2. Why should students save money? | |

| 3. What are the benefits of saving early? | |

| 4. What are some common saving methods? | |

| 5. What are short-term and long-term savings goals? | |