Building Financial Literacy

Financial literacy is the ability to understand and effectively use various financial skills. These skills include personal financial management, budgeting, and investing. Building financial literacy helps students make informed decisions about money, avoid debt traps, and achieve financial security. For students, mastering basic financial concepts early creates a strong foundation for lifelong financial wellness.

1. Meaning of Financial Literacy

Financial literacy refers to the knowledge and skills needed to manage money effectively. It involves understanding how money works in real life. A financially literate person can make sound decisions about earning, spending, saving, and investing.

- Core Definition: The ability to understand and apply financial concepts to personal money management.

- Key Components: Knowledge of financial products, understanding of financial risks, ability to plan for future needs.

- Practical Application: Reading bank statements, comparing loan options, understanding credit card terms.

- Student Context: Knowing how to manage pocket money, understanding savings accounts, recognizing needs versus wants.

1.1 Financial Capability vs Financial Literacy

- Financial Literacy: The knowledge and understanding of financial concepts.

- Financial Capability: The ability to apply that knowledge effectively in real situations.

- Relationship: Literacy provides knowledge; capability ensures you can actually use it.

- Example: Knowing what a budget is (literacy) versus creating and following your own budget (capability).

2. Importance of Financial Knowledge

Financial knowledge is critical for students as it prepares them for independent financial decision-making. It protects against financial mistakes and builds long-term wealth creation habits.

2.1 Personal Benefits

- Better Money Management: Helps track income and expenses systematically. Students can avoid overspending and plan purchases.

- Debt Avoidance: Understanding borrowing costs prevents accumulation of unnecessary debt. Recognizing high-interest traps like payday loans or credit card debt.

- Goal Achievement: Enables setting and reaching financial goals like buying a laptop, funding education, or emergency funds.

- Stress Reduction: Financial confidence reduces anxiety about money matters. Knowing how to handle financial emergencies builds mental peace.

2.2 Long-Term Benefits

- Wealth Creation: Early understanding of saving and investing leads to compound growth over time.

- Financial Independence: Ability to support oneself without relying on others or falling into debt cycles.

- Retirement Planning: Starting early with retirement savings maximizes benefits through compound interest.

- Economic Contribution: Financially literate citizens make better economic decisions, strengthening the overall economy.

2.3 Protection from Financial Risks

- Fraud Prevention: Recognizing common financial scams like phishing, fake investment schemes, or identity theft.

- Poor Investment Choices: Avoiding high-risk investments without understanding them. Not falling for "get rich quick" schemes.

- Insurance Understanding: Knowing when and what insurance is needed protects against unexpected losses.

- Contract Awareness: Reading and understanding terms before signing loan agreements or financial contracts.

3. Understanding Basic Financial Terms

Mastering financial vocabulary is essential for understanding money-related documents and making informed decisions. These terms appear frequently in banking, shopping, and investment contexts.

3.1 Banking and Savings Terms

- Account Balance: The total amount of money currently in your bank account.

- Deposit: Money added to your account. Can be cash, cheque, or electronic transfer.

- Withdrawal: Money taken out from your account for spending or other purposes.

- Interest: Money earned on savings or money paid on loans. Expressed as a percentage per year.

- Principal: The original amount of money deposited or borrowed, excluding interest.

- Savings Account: A bank account that earns interest and allows deposits and withdrawals.

- Fixed Deposit (FD): A savings option where money is locked for a fixed period at higher interest rates.

- Minimum Balance: The lowest amount that must be maintained in an account to avoid charges.

3.2 Credit and Borrowing Terms

- Credit: The ability to borrow money or access goods/services with the promise to pay later.

- Debit: Money deducted from your account when you spend or withdraw.

- Loan: Money borrowed from a bank or lender that must be repaid with interest.

- Interest Rate: The percentage charged on borrowed money or earned on savings. Can be fixed or variable.

- EMI (Equated Monthly Installment): Fixed monthly payment made to repay a loan. Includes both principal and interest components.

- Credit Score: A numerical rating (300-900) that shows creditworthiness. Higher scores indicate better repayment history.

- Debt: Money owed to someone else. Can be in the form of loans, credit card balances, or unpaid bills.

- Default: Failure to repay a loan or meet financial obligations on time.

3.3 Transaction and Payment Terms

- Transaction: Any activity involving money movement in or out of an account.

- UPI (Unified Payments Interface): Digital payment system allowing instant bank-to-bank transfers via mobile apps.

- Net Banking: Online platform to manage bank accounts, transfer money, and pay bills.

- ATM (Automated Teller Machine): Electronic banking machine for cash withdrawals, deposits, and balance checks.

- Debit Card: Card linked to bank account that allows spending only available balance.

- Credit Card: Card that allows borrowing money up to a limit. Must be repaid monthly to avoid interest charges.

- PIN (Personal Identification Number): Secret code used to authorize transactions. Should never be shared.

- OTP (One-Time Password): Temporary code sent to mobile for transaction verification and security.

3.4 Investment and Growth Terms

- Investment: Money put into assets like stocks, bonds, or property expecting future returns.

- Return: Profit or gain earned from an investment. Can be positive (profit) or negative (loss).

- Risk: The possibility of losing money on an investment. Higher risk often means potential for higher returns.

- Diversification: Spreading investments across different assets to reduce risk.

- Compound Interest: Interest calculated on both principal and accumulated interest. Formula: A = P(1 + r/n)^(nt) where A = final amount, P = principal, r = interest rate, n = compounding frequency, t = time.

- Simple Interest: Interest calculated only on principal amount. Formula: SI = (P × r × t)/100 where P = principal, r = rate, t = time.

- Inflation: The rate at which prices of goods and services increase over time. Reduces purchasing power of money.

- Asset: Something of value that you own. Examples include cash, savings, property, or investments.

3.5 Budget and Planning Terms

- Budget: A financial plan showing expected income and planned expenses for a specific period.

- Income: Money received from various sources like allowance, salary, gifts, or part-time work.

- Expense: Money spent on goods, services, or bills.

- Fixed Expense: Regular costs that remain the same each month. Examples include school fees, rent, subscriptions.

- Variable Expense: Costs that change from month to month. Examples include food, entertainment, transportation.

- Surplus: Amount remaining when income exceeds expenses. This can be saved or invested.

- Deficit: Situation when expenses exceed income. Requires borrowing or using savings.

- Emergency Fund: Money set aside specifically for unexpected expenses or urgent needs.

4. Reading Bills and Statements

Financial documents contain important information about your money transactions. Learning to read them correctly prevents errors and helps track spending patterns.

4.1 Understanding Bank Statements

A bank statement is a document showing all transactions in your account during a specific period. It is usually generated monthly.

- Account Details Section: Shows account number, account holder name, branch, and statement period.

- Opening Balance: Amount in account at the start of the statement period.

- Transaction Details: Lists all deposits (credits) and withdrawals (debits) with dates, descriptions, and amounts.

- Closing Balance: Amount remaining in account at the end of statement period.

- Interest Credited: Shows interest earned on savings during the period.

- Charges Deducted: Lists fees like SMS charges, ATM fees, or minimum balance penalties.

4.1.1 How to Verify Bank Statement

- Match opening balance with previous statement's closing balance.

- Check each transaction against your receipts or records.

- Look for unknown or unauthorized transactions immediately.

- Verify all deposits have been credited correctly.

- Calculate closing balance: Opening Balance + Total Credits - Total Debits = Closing Balance.

- Report any discrepancies to the bank within the specified timeframe (usually 30-60 days).

4.2 Reading Mobile/DTH Recharge Receipts

- Transaction ID: Unique number identifying the recharge. Keep this for dispute resolution.

- Mobile Number: Number recharged. Always verify before payment.

- Recharge Amount: Base pack value purchased.

- Validity Period: Duration for which the recharge is active.

- Benefits: Data, SMS, and calling minutes included in the pack.

- Payment Method: How payment was made (UPI, card, wallet).

- Transaction Time: Date and time of successful recharge.

4.3 Understanding Electricity and Utility Bills

- Consumer Number: Unique identification for your connection. Required for all payments and queries.

- Billing Period: The dates for which consumption is measured (usually one month).

- Previous Reading: Meter reading at the start of billing period.

- Current Reading: Meter reading at the end of billing period.

- Units Consumed: Difference between current and previous readings. Formula: Units = Current Reading - Previous Reading.

- Rate per Unit: Price charged for each unit of electricity consumed. May have different slabs.

- Fixed Charges: Basic service charges applied regardless of consumption.

- Total Amount: (Units Consumed × Rate per Unit) + Fixed Charges + Taxes.

- Due Date: Last date for payment without late fees or penalty.

- Late Payment Charges: Extra fee if bill is paid after due date.

4.4 Reading Shopping Receipts and Invoices

- Shop/Vendor Name: Identifies where purchase was made.

- Date and Time: When the purchase occurred.

- Item Description: Names or codes of products purchased.

- Quantity: Number of units of each item bought.

- Unit Price: Price per single item.

- Item Total: Quantity × Unit Price for each product.

- Subtotal: Sum of all item totals before taxes and discounts.

- Discount: Amount reduced from subtotal. Can be percentage or fixed amount.

- GST/Tax: Government tax added to purchase. May show CGST, SGST, or IGST separately.

- Final Amount: Subtotal - Discount + Tax = Amount paid.

- Payment Mode: How payment was made (cash, card, UPI).

- Return Policy: Conditions and timeframe for returning products.

4.5 Common Statement Verification Mistakes

- Not checking statements regularly - should review at least monthly.

- Ignoring small unknown charges that may be fraudulent.

- Forgetting to save receipts makes verification impossible.

- Confusing credit (money added) with debit (money deducted).

- Not reporting errors within the allowed timeframe (usually 30-60 days).

- Assuming closing balance equals available balance - pending transactions may reduce available funds.

5. Making Informed Money Decisions

Financial decisions impact both short-term and long-term financial health. An informed decision involves gathering information, comparing options, and considering consequences before spending or saving money.

5.1 The Decision-Making Process

- Identify the Need: Determine if the expense is a need (essential) or want (desirable but optional).

- Gather Information: Research product details, prices, features, and reviews from multiple sources.

- Compare Options: Evaluate at least 3-4 alternatives based on price, quality, and value for money.

- Check Affordability: Ensure the expense fits within your budget without affecting essential needs.

- Consider Timing: Determine if purchase is urgent or can wait for better deals or sales.

- Evaluate Long-term Impact: Consider maintenance costs, durability, and future value.

- Make the Decision: Choose the option that offers best value within budget constraints.

- Review the Outcome: After purchase, assess if the decision was correct to improve future choices.

5.2 Evaluating Purchase Options

- Price Comparison: Check prices across different sellers, online and offline stores. Use comparison websites and apps.

- Quality Assessment: Read product reviews, check ratings, and verify brand reputation. Cheaper is not always better.

- Hidden Costs: Consider installation, maintenance, accessories, and running costs beyond purchase price.

- Warranty and Support: Check warranty period, service center availability, and customer support quality.

- Return Policy: Understand conditions for returns, exchanges, and refunds before purchasing.

- Payment Terms: Compare cash price versus EMI options. Calculate total interest paid in installment plans.

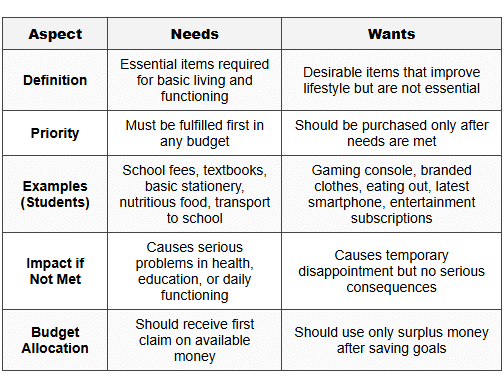

5.3 Needs vs Wants Framework

5.4 Avoiding Impulsive Purchases

- 24-Hour Rule: Wait for 24 hours before making non-essential purchases. Immediate desire often fades.

- List-Based Shopping: Prepare shopping list before going to market or browsing online. Stick to the list.

- Avoid Shopping During Sales: Sales create artificial urgency. Buy only what you already needed, not because it's discounted.

- Unsubscribe from Marketing: Remove promotional emails, SMS, and app notifications that trigger spending desires.

- Calculate in Time: Convert price into work hours. Example: ₹500 item equals 5 hours of work at ₹100/hour.

- Opportunity Cost Thinking: Consider what you're giving up by spending this money. Could it serve a better purpose?

5.5 Understanding Opportunity Cost

Opportunity cost is the value of the next best alternative given up when making a decision. Every rupee spent on one thing cannot be spent on something else.

- Simple Example: If you spend ₹200 on a movie, you lose the opportunity to buy a book or save that money.

- Decision Framework: Before spending, ask "What am I giving up by choosing this?"

- Savings Context: Money not saved today means losing future growth through compound interest.

- Time Value: Money saved today can grow over time, making it worth more in the future.

5.6 Red Flags in Financial Decisions

- Too Good to Be True: Promises of very high returns with no risk are usually scams.

- Pressure to Decide Quickly: Legitimate offers don't require immediate decisions without time to think.

- Lack of Written Documentation: Always insist on written agreements, receipts, and terms.

- Unclear Terms: If you don't understand what you're signing or agreeing to, don't proceed.

- Request for Sensitive Information: Never share PIN, OTP, or password with anyone, including bank staff.

- Upfront Payment Demands: Be cautious of schemes requiring large advance payments before delivering value.

- Emotional Manipulation: Sellers using fear, greed, or peer pressure to force decisions.

5.7 Smart Shopping Strategies

- Use Cashback and Rewards: Utilize credit card rewards, cashback apps, and loyalty programs for planned purchases only.

- Buy Generic/Store Brands: These are often same quality as branded products at lower prices.

- Bulk Buying for Essentials: Purchase non-perishable essentials in bulk during offers for lower per-unit cost.

- Seasonal Shopping: Buy seasonal items (clothes, electronics) during off-season for better discounts.

- Student Discounts: Always check for student discounts on software, subscriptions, transport, and entertainment.

- Refurbished Products: Consider certified refurbished electronics for significant savings with warranty protection.

5.8 Digital Payment Safety

- Verify URLs: Check that payment websites start with "https://" and show padlock symbol for security.

- Use Strong Passwords: Create unique, complex passwords for banking and payment apps. Never reuse passwords.

- Enable Two-Factor Authentication: Adds extra security layer requiring OTP or biometric verification.

- Avoid Public WiFi for Transactions: Never use public WiFi networks for banking or payment activities.

- Monitor Transactions: Check account statements regularly for unauthorized transactions. Report immediately.

- Download Official Apps: Install banking and payment apps only from official app stores, not third-party sources.

- Never Share OTP: One-Time Passwords should never be shared with anyone. Banks never ask for OTP.

- Beware of Phishing: Don't click suspicious links in SMS or emails claiming to be from banks.

5.9 Evaluating Financial Advice

- Source Credibility: Check qualifications and reputation of the person giving financial advice.

- Conflict of Interest: Be cautious if advisor benefits from your decision (commission-based products).

- Cross-Verify Information: Confirm financial advice from multiple reliable sources before acting.

- Understand Before Acting: Never follow advice you don't fully understand, regardless of source.

- Seek Written Information: Request documents, brochures, and terms in writing for review.

- Consult Parents/Guardians: Discuss significant financial decisions with family before proceeding.

Building financial literacy is a continuous process that improves with practice and experience. Start with mastering basic terms and gradually apply these concepts to real-life situations. The ability to read financial documents accurately, understand key terms, and make informed decisions protects you from financial mistakes and builds a foundation for long-term financial success. Remember that every financial decision, no matter how small, is an opportunity to practice and strengthen your financial literacy skills.