Investment Strategies

Investment strategies are systematic approaches investors use to build and manage their stock portfolios. Choosing the right strategy depends on your financial goals, risk tolerance, time horizon, and investment knowledge. Understanding different strategies helps you align your investments with your personal objectives and market conditions.

1. Value Investing

Value investing means buying stocks that trade below their intrinsic value (true worth). Investors search for undervalued companies that the market has temporarily priced too low.

1.1 Core Principles

- Intrinsic Value: The actual worth of a company based on fundamentals like assets, earnings, and cash flow. Value investors calculate this using financial analysis.

- Market Price vs. Intrinsic Value: When market price is lower than intrinsic value, the stock is undervalued. This creates a buying opportunity.

- Market Inefficiency: Value investing assumes markets sometimes misprice stocks due to emotions, short-term thinking, or lack of information.

- Contrarian Approach: Often involves buying when others are selling (during market fear or negative sentiment).

1.2 Finding Undervalued Stocks

Value investors use specific metrics to identify cheap stocks:

- Price-to-Earnings (P/E) Ratio: Low P/E ratios (below industry average) suggest undervaluation. Formula: P/E = Market Price per Share ÷ Earnings per Share.

- Price-to-Book (P/B) Ratio: Compares stock price to book value (assets minus liabilities). P/B below 1 means trading below asset value. Formula: P/B = Market Price per Share ÷ Book Value per Share.

- Dividend Yield: Higher dividend yields may indicate undervaluation. Formula: Dividend Yield = Annual Dividend per Share ÷ Market Price per Share × 100.

- Debt-to-Equity Ratio: Lower ratios indicate financial stability. Value investors prefer companies with manageable debt.

- Free Cash Flow: Positive and growing cash flow shows a company generates real money, not just accounting profits.

1.3 Margin of Safety

The margin of safety is the difference between intrinsic value and purchase price. This concept protects investors from losses.

- Definition: Buying significantly below intrinsic value to cushion against calculation errors or unforeseen problems.

- Example: If intrinsic value is ₹100, buying at ₹70 provides a 30% margin of safety.

- Risk Reduction: Larger margins reduce downside risk. Even if intrinsic value estimates are slightly wrong, investors still profit.

- Typical Range: Value investors often seek 20-50% margin of safety depending on uncertainty levels.

- Protection Against: Calculation errors, business deterioration, market volatility, unexpected events.

1.4 Long-Term Hold Approach

Value investing requires patience as market recognition of true value takes time.

- Holding Period: Typically 3-5 years or longer. Markets eventually recognize undervaluation.

- Compounding Benefits: Long holding periods allow earnings and dividends to compound, multiplying returns.

- Tax Efficiency: Longer holding reduces trading costs and qualifies for favorable Long-Term Capital Gains (LTCG) tax rates.

- Avoiding Market Timing: Focus on business fundamentals rather than short-term price movements.

- Famous Practitioners: Warren Buffett, Benjamin Graham (father of value investing), Charlie Munger.

1.5 Common Student Mistakes

- Value Trap: Buying cheap stocks that remain cheap because of fundamental problems. Not all low P/E stocks are good investments.

- Ignoring Quality: Focusing only on price metrics without checking business quality, management competence, or competitive advantages.

- Impatience: Selling too early before market recognizes true value. Value investing requires discipline.

2. Growth Investing

Growth investing focuses on companies with above-average revenue and earnings growth potential. Investors prioritize future growth over current valuation.

2.1 Identifying High-Growth Companies

Growth investors look for businesses expanding rapidly in revenue, earnings, and market share.

- Revenue Growth Rate: Annual revenue increase of 15-25% or higher. Formula: Revenue Growth Rate = [(Current Year Revenue - Previous Year Revenue) ÷ Previous Year Revenue] × 100.

- Earnings Growth Rate: Consistent increase in net profit, often 20%+ annually. Formula: EPS Growth Rate = [(Current Year EPS - Previous Year EPS) ÷ Previous Year EPS] × 100.

- Industry Position: Market leaders or disruptors in high-growth sectors (technology, healthcare, renewable energy).

- Innovation Focus: Companies investing heavily in R&D, new products, or services with competitive advantages.

- Scalable Business Model: Ability to grow revenue without proportional cost increases (high operating leverage).

- Total Addressable Market (TAM): Large market opportunity allowing years of expansion.

2.2 Key Growth Metrics

- Price-to-Earnings Growth (PEG) Ratio: Adjusts P/E for growth rate. Formula: PEG = P/E Ratio ÷ Earnings Growth Rate. PEG below 1 suggests reasonable valuation relative to growth.

- Return on Equity (ROE): High ROE (15%+ or higher) indicates efficient profit generation. Formula: ROE = Net Income ÷ Shareholder Equity × 100.

- Profit Margins: Expanding margins show operational efficiency and pricing power.

- Market Share Trends: Growing share in expanding markets signals competitive strength.

2.3 Accepting Higher Valuations

Growth stocks typically trade at premium valuations because investors pay for future potential.

- High P/E Ratios: Growth companies often have P/E ratios of 30, 50, or even 100+. Investors justify this by expected future earnings expansion.

- Premium Pricing: Market prices in optimistic future growth assumptions. Higher risk if growth doesn't materialize.

- Valuation Justification: If earnings grow 25% annually, today's high P/E becomes reasonable in future years.

- Risk Factor: Any growth disappointment causes sharp price corrections. Valuation multiples compress quickly.

- Trade-off: Higher potential returns come with higher volatility and downside risk.

2.4 Momentum Consideration

Momentum investing is a subset where investors buy stocks with strong upward price trends, expecting continuation.

- Price Momentum: Stocks rising in price tend to continue rising (at least temporarily). Based on market psychology and trend following.

- Relative Strength: Comparing stock performance to broader market or sector. Strong relative performers attract more buyers.

- Technical Indicators: Using moving averages, RSI (Relative Strength Index), MACD (Moving Average Convergence Divergence) to identify trends.

- Earnings Momentum: Stocks with accelerating earnings growth or positive earnings surprises attract momentum buyers.

- Short-Term Focus: Momentum strategies typically hold for weeks to months, not years.

2.5 Common Student Mistakes

- Overpaying for Growth: Buying at excessive valuations that even strong growth cannot justify. Future returns become limited.

- Ignoring Profitability: Focusing on revenue growth while ignoring whether company actually makes profit or burns cash.

- Chasing Hype: Buying popular growth stocks after major price run-ups. Often leads to buying high and selling low.

3. Dividend Investing

Dividend investing prioritizes stocks that pay regular cash dividends, generating steady income alongside potential capital appreciation.

3.1 Income Generation Focus

Dividend investors build portfolios to create reliable cash flow, especially useful for retirement or passive income.

- Dividend: Portion of company profits distributed to shareholders, usually quarterly or annually. Paid as cash per share.

- Dividend Yield: Annual dividend as percentage of stock price. Formula: Dividend Yield = (Annual Dividend per Share ÷ Current Market Price) × 100.

- Example: Stock priced at ₹500 paying ₹25 annual dividend has 5% yield (₹25 ÷ ₹500 × 100).

- Income Stability: Dividends provide returns even when stock prices are volatile or falling.

- Cash Flow Needs: Suitable for retirees or investors needing regular income without selling shares.

- Tax Consideration: Dividend income taxed differently than capital gains. Check current Dividend Distribution Tax (DDT) rules.

3.2 Dividend Aristocrats

Dividend aristocrats are companies with long track records of consistently paying and increasing dividends.

- Definition: Companies that have increased dividends annually for 25+ consecutive years (international standard). In Indian context, 10+ years of consistent dividend growth is considered strong.

- Financial Strength: Only financially stable, profitable companies can maintain consistent dividend growth through economic cycles.

- Business Quality: Dividend aristocrats typically have strong competitive positions, predictable cash flows, and conservative management.

- Lower Volatility: These stocks generally experience less price volatility than broader market during downturns.

- Sector Concentration: Common in mature sectors like FMCG, utilities, pharmaceuticals, and consumer staples.

3.3 Key Dividend Metrics

- Dividend Payout Ratio: Percentage of earnings paid as dividends. Formula: Payout Ratio = (Dividend per Share ÷ Earnings per Share) × 100.

- Sustainable Range: 40-60% payout ratio generally sustainable. Below 40% suggests room for increase; above 80% may be unsustainable.

- Dividend Coverage Ratio: How many times earnings cover dividend payment. Formula: Coverage Ratio = Earnings per Share ÷ Dividend per Share. Ratio above 2 indicates safety.

- Dividend Growth Rate: Annual percentage increase in dividend. Formula: [(Current Year Dividend - Previous Year Dividend) ÷ Previous Year Dividend] × 100.

- Free Cash Flow: Company must generate sufficient cash to pay dividends. Check if cash flow from operations exceeds dividend payments.

3.4 Reinvestment Strategies

How investors use received dividends significantly impacts long-term wealth creation.

- Dividend Reinvestment Plan (DRIP): Automatically using dividends to purchase more shares of same company, often without brokerage fees.

- Compounding Effect: Reinvested dividends buy more shares, which generate more dividends, accelerating wealth growth exponentially.

- Example: ₹10,000 investment with 5% annual dividend yield and reinvestment grows faster than same investment with dividends spent.

- Dollar-Cost Averaging: Regular dividend reinvestment buys more shares when prices are low, fewer when high, reducing average cost.

- Manual Reinvestment: Using dividends from multiple stocks to buy shares of best-valued opportunities in portfolio.

- Accumulation Phase: Younger investors typically reinvest all dividends for maximum compounding during wealth-building years.

- Distribution Phase: Retirees may use dividends for living expenses rather than reinvesting.

3.5 Common Student Mistakes

- Yield Chasing: Buying stocks solely for very high yields (8-10%+) without checking sustainability. High yields often signal financial distress or upcoming dividend cuts.

- Ignoring Growth: Focusing only on dividend income while missing companies that reinvest profits for higher total returns.

- Ex-Dividend Confusion: Stock price drops by dividend amount on ex-dividend date. Buying just before this date doesn't create free money.

4. Index Investing

Index investing involves buying funds that replicate market indices rather than selecting individual stocks. This passive investment approach seeks to match overall market returns.

4.1 Passive Investment Approach

Passive investing means accepting market returns instead of trying to beat the market through active stock selection.

- Index Fund: Mutual fund or ETF that holds all stocks in a specific index (like Nifty 50, Sensex, or Nifty 500) in same proportions.

- No Stock Picking: Fund automatically owns whatever stocks the index contains. No research or judgment about individual companies needed.

- Buy and Hold: Long-term holding with minimal trading. Funds only adjust holdings when index composition changes.

- Market Returns: Index investors accept they will earn approximately what the overall market earns, nothing more or less.

- Diversification: Instant diversification across many companies. Nifty 50 index fund provides exposure to 50 large companies simultaneously.

- Simplicity: Requires minimal investment knowledge or time commitment. Suitable for beginners and busy professionals.

4.2 Types of Index Funds

- Broad Market Indices: Nifty 50 (top 50 companies), Sensex (top 30 companies), Nifty 500 (500 companies across market capitalizations).

- Sectoral Indices: Track specific sectors like Nifty Bank, Nifty IT, Nifty Pharma, Nifty Auto.

- Market Cap Indices: Nifty Midcap 150, Nifty Smallcap 250 for mid and small-sized companies.

- ETFs (Exchange-Traded Funds): Trade on stock exchanges like individual stocks. Can buy/sell anytime during market hours.

- Index Mutual Funds: Bought directly from fund houses at NAV (Net Asset Value) calculated at day's end.

4.3 Market Returns Matching

Index funds aim to deliver returns that closely track the underlying index performance.

- Tracking Error: Small difference between fund return and index return. Lower tracking error indicates better fund management. Formula: Tracking Error = Standard Deviation of (Fund Return - Index Return).

- Expected Returns: Historically, broad market indices deliver 10-12% annual returns over long periods (15-20+ years), though with significant year-to-year variation.

- Market Efficiency Theory: Most active fund managers fail to consistently beat market indices after fees, supporting passive approach validity.

- No Underperformance Risk: Cannot significantly underperform market, unlike active funds that may make poor stock selections.

- No Outperformance Either: Cannot beat market returns. Trade-off for guaranteed average performance is giving up possibility of above-average gains.

4.4 Lower Costs

Cost advantage is the most significant benefit of index investing compared to active management.

- Expense Ratio: Annual fee charged by fund. Formula: Expense Ratio = (Annual Fund Operating Expenses ÷ Total Fund Assets) × 100.

- Index Fund Fees: Typically 0.1% to 0.5% annually. Some ultra-low-cost funds charge as little as 0.05%.

- Active Fund Fees: Usually 1.5% to 2.5% annually. Higher fees to pay for research teams, fund managers, and trading costs.

- Cost Impact Example: On ₹10 lakh investment, 2% annual fee costs ₹20,000 yearly versus ₹2,000 for 0.2% index fund fee.

- Compounding Effect: Lower fees compound positively over decades. Saving 1.5-2% annually adds significantly to final wealth.

- No Transaction Costs: Minimal buying and selling means lower brokerage and tax costs from portfolio turnover.

- Performance Drag: High fees are major reason most active funds underperform indices over long periods.

4.5 Systematic Investment (SIP) with Index Funds

- Systematic Investment Plan (SIP): Investing fixed amount regularly (monthly/quarterly) regardless of market levels.

- Rupee Cost Averaging: SIP buys more units when markets are low, fewer when high, reducing average purchase cost over time.

- Discipline: Automatic investment removes emotion and timing concerns from investment process.

- Long-Term Wealth: Combining index investing with SIP is powerful strategy for beginners building wealth over 10-20+ years.

4.6 Common Student Mistakes

- Timing the Market: Trying to buy index funds only when markets seem "cheap." This defeats the passive approach and often reduces returns.

- Sector Index Concentration: Investing heavily in sectoral indices (banking, IT) without understanding concentration risk. Lacks diversification of broad indices.

- Short-Term Focus: Selling index funds after 1-2 years of underperformance. Index investing requires minimum 5-10 year horizon.

- Ignoring Expense Ratios: Not comparing expense ratios between similar index funds. Even 0.3% difference matters significantly over decades.

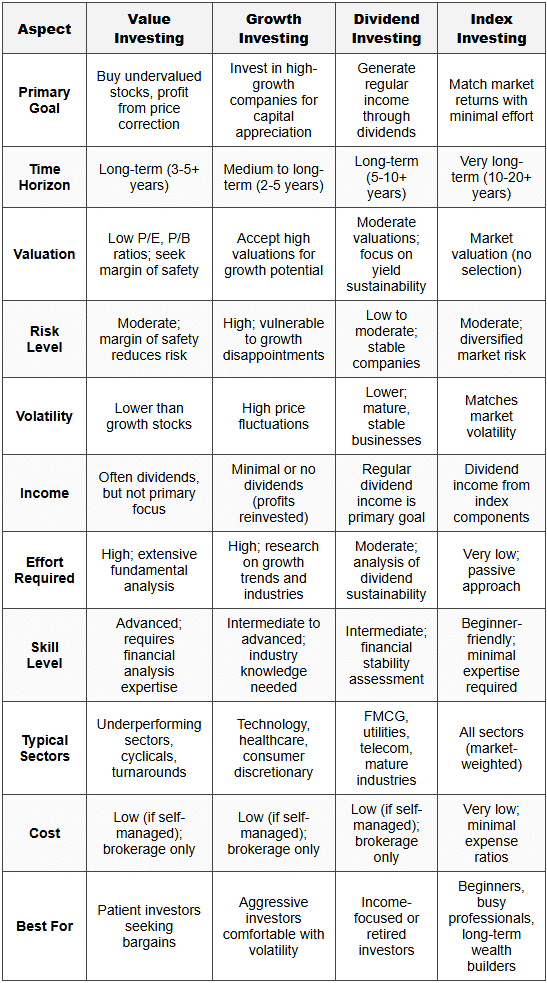

5. Comparing Investment Strategies

6. Choosing the Right Strategy

Selecting an investment strategy depends on multiple personal factors. No single strategy is universally "best."

6.1 Key Factors to Consider

- Investment Goals: Capital appreciation (growth/value), regular income (dividend), or steady wealth building (index).

- Risk Tolerance: Your ability and willingness to handle portfolio volatility. Growth investing requires high tolerance; dividend and index investing suit lower tolerance.

- Time Horizon: Longer horizons (10+ years) suit all strategies. Shorter horizons (under 5 years) favor dividend or index approaches.

- Available Time: Active strategies (value, growth, dividend) need research time. Index investing requires minimal time commitment.

- Knowledge Level: Beginners should start with index investing, gradually exploring other strategies as expertise grows.

- Income Needs: If you need portfolio income for expenses, dividend investing is appropriate. Accumulation phase favors growth or index strategies.

- Market Conditions: Different strategies perform better in different market cycles (bull markets favor growth; bear markets favor value).

6.2 Combining Strategies (Hybrid Approach)

Many successful investors combine multiple strategies rather than using just one.

- Core-Satellite Approach: Majority of portfolio (70-80%) in index funds (core), smaller portion (20-30%) in individual stock strategies (satellite).

- Life Stage Adjustment: Emphasize growth/index investing when young, gradually shift toward dividend investing as retirement approaches.

- Diversification Benefit: Different strategies perform well in different market conditions, reducing overall portfolio volatility.

- Example Allocation: 50% index funds, 25% dividend stocks, 25% growth stocks provides balanced exposure.

Understanding these four core investment strategies provides a strong foundation for building a personalized investment approach. Value investing emphasizes buying quality assets at bargain prices with a margin of safety. Growth investing focuses on companies with strong expansion potential, accepting higher valuations. Dividend investing prioritizes regular income from stable, profitable companies. Index investing offers a simple, low-cost path to match market returns through passive diversification. Your optimal strategy depends on your financial goals, risk capacity, time horizon, and personal circumstances. Many investors successfully combine elements from multiple strategies to create a balanced portfolio suited to their needs. As you gain experience, you can refine your approach, but starting with index investing provides an excellent beginner-friendly foundation while you develop deeper market knowledge.