Bank Exams Exam > Bank Exams Notes > Banking Awareness for Banking Exams > Cheatsheet: Non-Performing Assets (NPA)

Cheatsheet: Non-Performing Assets (NPA)

1. Definition and Classification

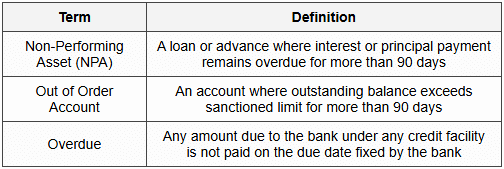

1.1 NPA Definition

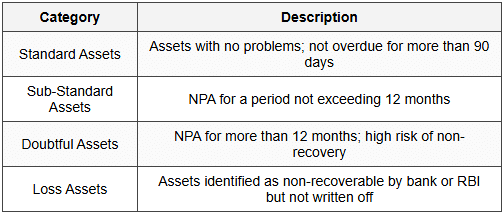

1.2 Asset Classification Categories

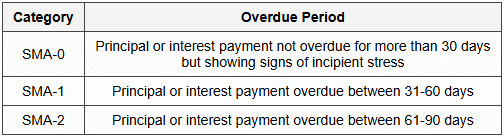

1.3 Special Mention Accounts (SMA)

2. NPA Recognition Norms

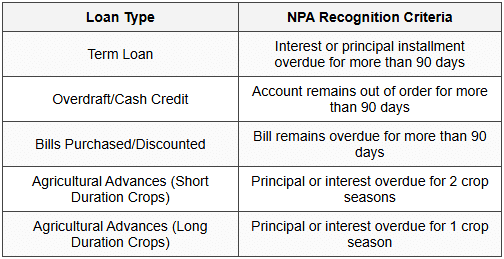

2.1 Different Loan Types

2.2 Important Time Periods

- 90 days: Standard period for NPA recognition across most loan categories

- 180 days: Previous NPA recognition period (changed in 2004)

- 12 months: Threshold for sub-standard to doubtful asset classification

- 31-60 days: SMA-1 classification

- 61-90 days: SMA-2 classification

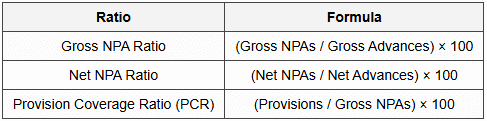

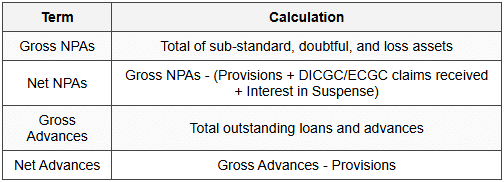

3. NPA Ratios and Calculations

3.1 Key NPA Ratios

3.2 Calculation Components

3.3 Acceptable Norms

- Ideal Gross NPA Ratio: Below 3%

- Ideal Net NPA Ratio: Below 1%

- Minimum PCR recommended by RBI: 70%

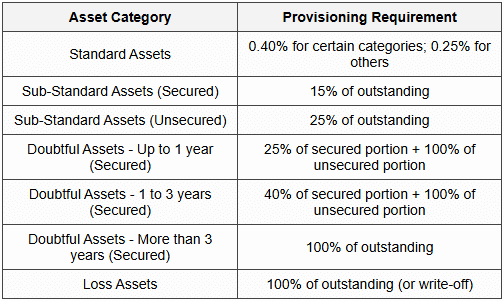

4. Provisioning Norms

4.1 Provisioning Requirements

4.2 Specific Provisioning Requirements

- Agriculture Advances: 0.25% for standard assets

- SME Advances: 0.25% for standard assets

- Commercial Real Estate: 1.00% for standard assets

- Restructured Standard Assets: Additional 5% provision for 2 years

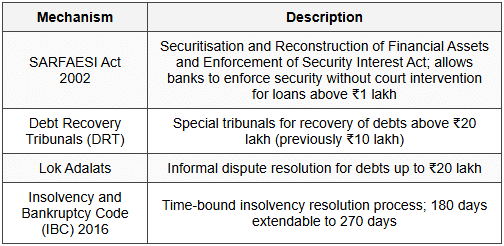

5. NPA Management and Resolution

5.1 Resolution Mechanisms

5.2 Asset Reconstruction Companies (ARCs)

- Established under SARFAESI Act 2002

- Purchase NPAs from banks at discounted prices

- Issue Security Receipts (SRs) to banks

- First ARC: Asset Reconstruction Company (India) Limited (ARCIL) - 2002

- Minimum Net Owned Funds: ₹2 crore initially, ₹100 crore within 3 years

5.3 National Asset Reconstruction Company (NARC/NARCL)

- Established: 2021

- Also known as Bad Bank

- 51% owned by Public Sector Banks

- Focus on resolution of stressed assets above ₹500 crore

- Complemented by India Debt Resolution Company Limited (IDRCL) for asset management

5.4 One-Time Settlement (OTS)

- Compromise settlement between bank and borrower

- Available for NPAs in sub-standard and doubtful categories

- Requires approval from competent authority based on amount

- Cannot be offered to wilful defaulters

5.5 Write-off

- Removal of NPA from balance sheet

- Does not mean waiver; recovery efforts continue

- Improves gross NPA ratio

- Full provision required before write-off

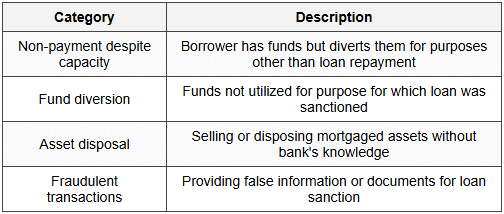

6. Wilful Defaulters

6.1 Definition and Categories

6.2 Consequences for Wilful Defaulters

- No additional credit facility from any bank

- Initiation of criminal proceedings under IPC Section 420

- Promoters cannot establish new ventures for 5 years

- Name published in public domain by RBI

- Debarred from accessing capital markets

- Cannot be appointed as directors in other companies

6.3 Wilful Defaulter Identification

- Minimum default amount: ₹25 lakh

- Identification Committee formed by banks

- Show cause notice issued before declaring as wilful defaulter

- Information shared with Credit Information Companies (CICs)

7. Restructuring and Relief Measures

7.1 Corporate Debt Restructuring (CDR)

- Voluntary mechanism for restructuring corporate debts above ₹10 crore

- CDR Cell: 3-tier structure (Standing Forum, Core Group, Empowered Group)

- Time limit: 90 days for restructuring decision after reference

- Discontinued in 2018; replaced by IBC route

7.2 Strategic Debt Restructuring (SDR)

- Allowed conversion of debt into equity (51% or more)

- Change in management control

- Implemented for accounts above ₹500 crore

- Discontinued in 2018 following RBI circular on revised framework

7.3 5/25 Refinancing Scheme

- For infrastructure and core industry projects

- Allowed extension of loan repayment period up to 25 years

- Refinancing every 5 or 7 years

- Discontinued in 2018

7.4 Resolution Framework for COVID-19 Related Stress

- Resolution plans for corporate and personal loans

- Invocation window for eligible borrowers

- Financial parameters: debt-equity ratio, liquidity coverage ratio

- Aggregate exposure threshold: ₹50 crore for corporate borrowers (later extended)

7.5 Prudential Framework on Resolution (June 2019)

- Inter-Creditor Agreement (ICA) for accounts above ₹50 crore (later ₹100 crore)

- 75% of creditors by value can enforce resolution plan

- 30-day review period for lenders

- 180-day resolution period after review

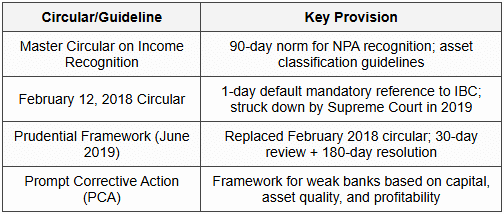

8. RBI Guidelines and Circulars

8.1 Key RBI Circulars

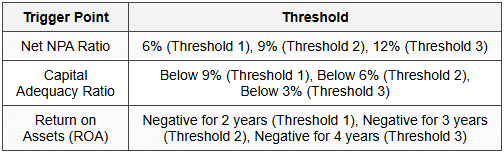

8.2 Prompt Corrective Action (PCA) Framework

8.3 PCA Restrictions

- Restriction on dividend distribution

- Prohibition on branch expansion

- Reduction in compensation to directors and senior executives

- Restrictions on lending to risky borrowers

- Mandatory capital infusion plan

9. Impact and Consequences of NPAs

9.1 Impact on Banks

- Reduced profitability due to provisioning requirements

- Lower Return on Assets (ROA) and Return on Equity (ROE)

- Reduced lending capacity and credit creation

- Increased Cost of Advances

- Impact on Capital Adequacy Ratio (CAR)

- Deterioration of asset quality indicators

9.2 Impact on Economy

- Reduced credit availability for productive sectors

- Lower economic growth due to credit crunch

- Increased interest rates for new borrowers

- Loss of depositor confidence

- Burden on government for recapitalization of PSBs

9.3 Recapitalization of Banks

- Indradhanush Plan (2015): ₹70,000 crore over 4 years

- Recapitalization Bonds (2017): ₹1,35,000 crore

- Regular budgetary allocations for PSB capital infusion

10. Preventive Measures and Best Practices

10.1 Preventive Measures

- Robust credit appraisal and risk assessment

- Regular monitoring of SMA accounts

- Early Warning Signals (EWS) system implementation

- Strengthening of credit rating and credit information systems

- Improved recovery mechanisms and dedicated recovery cells

- Technology adoption for credit monitoring

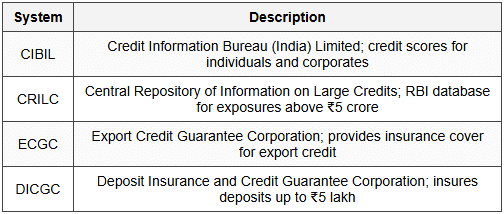

10.2 Credit Information Systems

10.3 Governance and Compliance

- Board-level oversight of asset quality

- Independent Credit Risk Management Department

- Regular asset quality review by internal and statutory auditors

- Compliance with RBI's Asset Classification and Provisioning norms

- Implementation of Basel III norms for capital adequacy

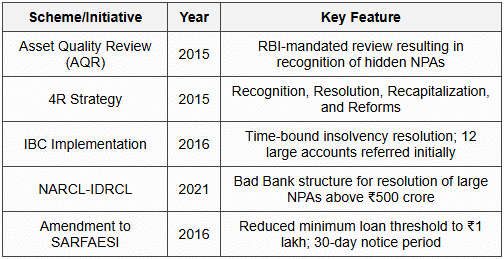

11. Recent Developments and Schemes

11.1 Key Schemes and Initiatives

11.2 Banking Regulation Amendments

- Banking Regulation (Amendment) Act 2017: RBI authorized to direct banks for insolvency proceedings

- Banking Regulation (Amendment) Act 2020: RBI powers extended to cooperative banks

- Fugitive Economic Offenders Act 2018: Confiscation of property of economic offenders

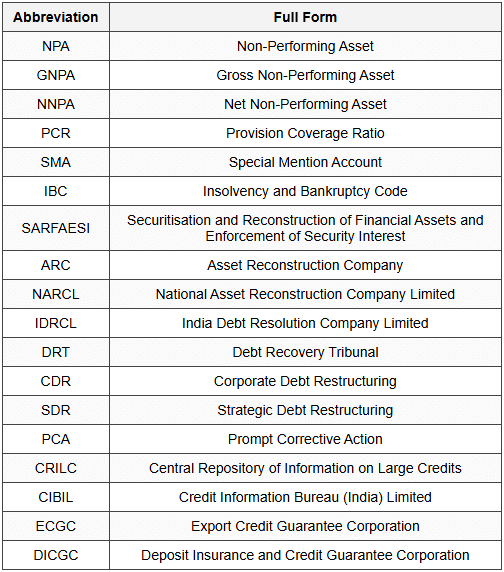

12. Important Terms and Abbreviations

12.1 Key Abbreviations

The document Cheatsheet: Non-Performing Assets (NPA) is a part of the Bank Exams Course Banking Awareness for Banking Exams.

All you need of Bank Exams at this link: Bank Exams

About this Document

4.66/5 Rating

Apr 18, 2026 Last updated

Related Exams

Document Description: Cheatsheet: Non-Performing Assets (NPA) for Bank Exams 2026 is part of Banking Awareness for Banking Exams preparation. The notes and questions for Cheatsheet: Non-Performing Assets (NPA) have been prepared according to the Bank Exams exam syllabus. Information about Cheatsheet: Non-Performing Assets (NPA) covers topics like and Cheatsheet: Non-Performing Assets (NPA) Example, for Bank Exams 2026 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Cheatsheet: Non-Performing Assets (NPA).

Introduction of Cheatsheet: Non-Performing Assets (NPA) in English is available as part of our Banking Awareness for Banking Exams for Bank Exams & Cheatsheet: Non-Performing Assets (NPA) in Hindi for Banking Awareness for Banking Exams course. Download more important topics related with notes, lectures and mock test series for Bank Exams Exam by signing up for free. Bank Exams: Cheatsheet: Non-Performing Assets (NPA)

Description

Cheatsheet: Non of Banking Awareness to help you remember important concepts with short tricks. Start learning for Bank Exams exam & improve retention with EduRev.

Information about Cheatsheet: Non-Performing Assets (NPA)

In this doc you can find the meaning of Cheatsheet: Non-Performing Assets (NPA) defined & explained in the simplest way possible. Besides explaining types of Cheatsheet: Non-Performing Assets (NPA) theory, EduRev gives you an ample number of questions to practice Cheatsheet: Non-Performing Assets (NPA) tests, examples and also practice Bank Exams tests

Related Searches

Semester Notes, pdf , Sample Paper, study material, Cheatsheet: Non-Performing Assets (NPA), Previous Year Questions with Solutions, ppt, Free, Viva Questions, shortcuts and tricks, mock tests for examination, Summary, past year papers, practice quizzes, Cheatsheet: Non-Performing Assets (NPA), Cheatsheet: Non-Performing Assets (NPA), MCQs, Exam, video lectures, Objective type Questions, Important questions, Extra Questions;