Currency Exchange Rates

Currency exchange rates represent the price of one currency expressed in terms of another currency. They are fundamental to international trade, capital flows, and investment decisions. For portfolio managers and analysts, understanding exchange rate mechanisms, parity conditions, and forecasting methods is crucial for managing currency risk and exploiting international investment opportunities. This topic integrates economics, finance, and quantitative methods to explain how currencies are priced and how they behave in different market conditions.

1. Exchange Rate Basics

1.1 Exchange Rate Quotation Conventions

- Spot Exchange Rate: Current market price for immediate delivery (typically T+2 settlement). Denoted as S(A/B) = units of currency A per unit of currency B.

- Base Currency vs. Price Currency: In quotation A/B, B is the base currency (denominator), A is the price currency (numerator). Example: USD/EUR = 1.20 means 1.20 USD per 1 EUR.

- Direct Quotation (Price Quotation): Domestic currency per unit of foreign currency. From US perspective, USD/EUR = 1.20 is direct.

- Indirect Quotation (Volume Quotation): Foreign currency per unit of domestic currency. From US perspective, EUR/USD = 0.8333 is indirect.

- Cross Rate: Exchange rate between two currencies calculated from their exchange rates against a third currency (usually USD). Formula: S(A/B) = S(A/C) × S(C/B).

1.2 Bid-Offer Spreads

- Bid Rate: Price at which dealer buys the base currency (sells the price currency). Always lower than offer rate.

- Offer (Ask) Rate: Price at which dealer sells the base currency (buys the price currency). Always higher than bid rate.

- Spread Calculation: % Spread = [(Offer - Bid) / Offer] × 100. Wider spreads indicate less liquid currency pairs or higher volatility.

- Transaction Rule: When buying base currency, use offer rate. When selling base currency, use bid rate. Dealer always profits from the spread.

- Cross Rate with Spreads: Use offer rates when buying and bid rates when selling to compute worst-case cross rates for transactions.

1.3 Currency Appreciation and Depreciation

- Currency Appreciation: Base currency strengthens; exchange rate increases (more price currency per base currency). Example: USD/EUR rises from 1.20 to 1.25, EUR appreciated.

- Currency Depreciation: Base currency weakens; exchange rate decreases (less price currency per base currency). Example: USD/EUR falls from 1.20 to 1.15, EUR depreciated.

- Percentage Change Formula: % Change = [(S₁ - S₀) / S₀] × 100, where S₁ is ending rate, S₀ is beginning rate.

- Reciprocal Relationship: If S(A/B) increases by X%, then S(B/A) decreases by approximately X/(1+X)%, not exactly X%.

1.4 Mark-to-Market Value of Currency Positions

- Long Position in Base Currency: Profits when base currency appreciates. Value = Contract Size × (Current Rate - Entry Rate).

- Short Position in Base Currency: Profits when base currency depreciates. Value = Contract Size × (Entry Rate - Current Rate).

- Home Currency Return: For foreign investments, total return = Foreign asset return + Currency return + (Foreign asset return × Currency return).

2. Forward Exchange Rates

2.1 Forward Contracts and Quotations

- Forward Contract: Agreement to exchange currencies at a specified future date at a rate agreed today (forward rate F). No money changes hands at initiation.

- Forward Points (Swap Points): Difference between forward and spot rate, quoted in basis points. Forward Rate = Spot Rate + Forward Points/10,000.

- Forward Premium: Forward rate > Spot rate (base currency trading at premium). Forward points are positive.

- Forward Discount: Forward rate < spot="" rate="" (base="" currency="" trading="" at="" discount).="" forward="" points="" are="">

- Percentage Forward Premium/Discount: (F - S) / S × 100. Annualized: [(F - S) / S] × (360/Days) × 100.

2.2 Forward Rate Calculation

Forward rates are determined by no-arbitrage conditions based on interest rate differentials between two currencies. This prevents covered interest arbitrage.

- Forward Rate Formula: F(A/B) = S(A/B) × [(1 + i_A × Days/360) / (1 + i_B × Days/360)]

- Where: F = Forward rate, S = Spot rate, i_A = Interest rate for currency A (price currency), i_B = Interest rate for currency B (base currency), Days = Forward contract period.

- Key Insight: Currency with higher interest rate trades at forward discount. Currency with lower interest rate trades at forward premium.

- Approximation Formula: (F - S) / S ≈ (i_A - i_B) × (Days/360). Forward premium/discount approximately equals interest rate differential.

- Trap Alert: Always match currency positions correctly-price currency interest rate in numerator, base currency interest rate in denominator.

2.3 Covered Interest Rate Parity (CIRP)

- Definition: No-arbitrage condition ensuring forward rates prevent riskless profit from covered interest arbitrage. Must hold in efficient markets.

- CIRP Formula: F(A/B) / S(A/B) = (1 + i_A) / (1 + i_B). This is the fundamental forward pricing equation.

- Covered Interest Arbitrage: If CIRP violated, arbitrageurs borrow in low-rate currency, convert spot, invest in high-rate currency, sell forward proceeds, lock riskless profit.

- Arbitrage Steps: (1) Borrow currency with lower interest rate, (2) Convert to currency with higher rate at spot, (3) Invest at higher rate, (4) Enter forward contract to convert back, (5) Repay loan and keep profit.

- CIRP Holding: In practice, CIRP holds very tightly for major currency pairs due to active arbitrageurs and liquid markets.

2.4 Forward Contract Settlement and Value

- At Initiation (t=0): Value = 0 (no money exchanges hands). Both parties agree to future exchange rate F.

- During Life of Contract (t): Value = (F_new - F_original) × Contract Size × [1 / (1 + i × Remaining Days/360)]. Discount using price currency interest rate.

- At Maturity (T): Value = (S_T - F) × Contract Size. This is the payoff from the forward position.

- Long Forward Position: Obligation to buy base currency at F. Profits if spot at maturity S_T > F.

- Short Forward Position: Obligation to sell base currency at F. Profits if spot at maturity S_T <>

3. Interest Rate Parity Conditions

3.1 Covered Interest Rate Parity (CIRP) - Detailed

- Exact Formula: (1 + i_A)^t = [F(A/B) / S(A/B)] × (1 + i_B)^t, where t is time period as fraction of year.

- Rearranged Form: F(A/B) = S(A/B) × [(1 + i_A)^t / (1 + i_B)^t]. This shows forward rate as function of spot rate and interest rate differential.

- Linear Approximation: (F - S) / S ≈ (i_A - i_B) × t. Useful for quick calculations; accurate for small interest rate differences and short periods.

- Empirical Evidence: CIRP holds very well for major currencies with no capital controls. Deviations are typically within transaction costs.

- Violation Conditions: Capital controls, political risk, differing tax treatments, or transaction costs can cause CIRP deviations.

3.2 Uncovered Interest Rate Parity (UIRP)

- Definition: Expected spot exchange rate at time T equals the forward rate for time T. E[S_T(A/B)] = F_T(A/B).

- UIRP Formula: E[%ΔS(A/B)] ≈ i_A - i_B. Expected percentage change in spot rate equals interest rate differential.

- Interpretation: Currency with higher interest rate expected to depreciate by the interest rate differential. Currency with lower rate expected to appreciate.

- Relationship to CIRP: UIRP assumes forward rate is unbiased predictor of future spot rate. CIRP + Unbiased Forward Rate → UIRP.

- Empirical Evidence: UIRP performs poorly in practice. High interest rate currencies often appreciate rather than depreciate (forward rate bias or carry trade premium).

- Carry Trade Implication: UIRP violations enable profitable carry trades-borrow low-rate currency, invest in high-rate currency.

3.3 Forward Rate Parity Relationships Summary

- CIRP (Covered): Links spot rate, forward rate, and interest rates. No arbitrage condition. Holds in practice.

- UIRP (Uncovered): Links expected future spot rate and current interest rates. Behavioral prediction. Often violated in practice.

- Key Difference: CIRP is risk-free arbitrage relationship (must hold). UIRP is expected relationship involving risk (often fails).

- Trap Alert: Don't confuse CIRP with UIRP. CIRP is about forward pricing (arbitrage-free). UIRP is about expectations (often wrong).

4. Purchasing Power Parity (PPP)

4.1 Law of One Price

- Definition: Identical goods should trade at same price across countries when expressed in common currency, assuming no transaction costs or barriers.

- Formula: P_A = S(A/B) × P_B, where P_A is price in currency A, P_B is price in currency B, S(A/B) is spot exchange rate.

- Example: If iPad costs $500 in US and €400 in Europe, law of one price implies USD/EUR = 500/400 = 1.25.

- Arbitrage Mechanism: If violated, buy in cheap market, sell in expensive market until prices converge.

- Limitations: Transaction costs, tariffs, non-tradable goods, and different product specifications prevent law from holding exactly.

4.2 Absolute Purchasing Power Parity

- Definition: Exchange rate between two currencies equals ratio of price levels (general baskets of goods).

- Formula: S(A/B) = CPI_A / CPI_B, where CPI is consumer price index (or general price level).

- Implication: A currency's value is determined by its purchasing power. Exchange rates adjust to equalize purchasing power across countries.

- Empirical Evidence: Absolute PPP fails in short and medium run due to structural factors, different consumption baskets, and non-tradable goods.

- Trap Alert: Absolute PPP is theoretical benchmark. Don't expect exact holding in practice.

4.3 Relative Purchasing Power Parity

- Definition: Change in exchange rate over time equals difference in inflation rates between two countries.

- Formula: %ΔS(A/B) ≈ Inflation_A - Inflation_B, where %ΔS is percentage change in spot rate.

- Exact Formula: [S₁(A/B) / S₀(A/B)] = [(1 + Inflation_A) / (1 + Inflation_B)].

- Interpretation: Currency of country with higher inflation depreciates. Currency of country with lower inflation appreciates.

- Time Horizon: Relative PPP works better over long periods (5-10 years) than short periods. Short-run deviations can be substantial.

- Empirical Evidence: Relative PPP holds reasonably well in long run, especially for countries with large inflation differentials. Poor predictor in short run.

4.4 Ex-Ante vs. Ex-Post PPP

- Ex-Ante PPP: Uses expected inflation rates. E[%ΔS(A/B)] = E[Inflation_A] - E[Inflation_B]. Forward-looking relationship.

- Ex-Post PPP: Uses realized inflation rates. Actual %ΔS(A/B) compared to actual inflation differential. Backward-looking verification.

- Real Exchange Rate: RER = S(A/B) × (CPI_B / CPI_A). Adjusts nominal rate for relative price levels. Constant RER implies PPP holds.

- Real Exchange Rate Change: %ΔRER ≈ %ΔS(A/B) - (Inflation_A - Inflation_B). If PPP holds, real rate is constant (%ΔRER = 0).

5. International Fisher Effect (IFE)

5.1 Fisher Effect (Domestic)

- Definition: Nominal interest rate equals real interest rate plus expected inflation.

- Formula: (1 + Nominal Rate) = (1 + Real Rate) × (1 + Expected Inflation).

- Linear Approximation: Nominal Rate ≈ Real Rate + Expected Inflation.

- Implication: If real rates constant across time, changes in nominal rates reflect changes in inflation expectations.

5.2 International Fisher Effect

- Definition: Difference in nominal interest rates between two countries equals expected change in exchange rate.

- Formula: E[%ΔS(A/B)] ≈ i_A - i_B, where i_A and i_B are nominal interest rates.

- Exact Formula: [E(S₁) / S₀] = [(1 + i_A) / (1 + i_B)].

- Derivation Logic: If real rates equal across countries and PPP holds, then Fisher Effect + PPP → IFE.

- Interpretation: Currency with higher nominal interest rate expected to depreciate. Currency with lower rate expected to appreciate.

- Relationship to UIRP: IFE is equivalent to UIRP. Both predict high interest rate currencies depreciate.

- Empirical Evidence: Like UIRP, IFE fails in practice. High interest rate currencies often appreciate (carry trade anomaly).

5.3 Real Interest Rate Parity

- Definition: Real interest rates are equal across countries (after adjusting for expected currency changes).

- Formula: Real Rate_A = Real Rate_B. Equivalently: (i_A - Expected Inflation_A) = (i_B - Expected Inflation_B).

- Capital Mobility Implication: With perfect capital mobility, investors shift capital until real returns equalize globally.

- Trap Alert: Real interest rate parity assumes perfect capital mobility and no risk differences-often unrealistic.

6. Parity Relationships - Big Picture Integration

6.1 Complete Parity Framework

Four parity conditions interrelate spot rates, forward rates, interest rates, inflation rates, and expected exchange rate changes. They form an integrated framework:

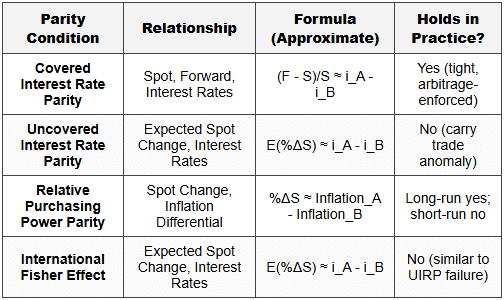

- Covered Interest Rate Parity (CIRP): Links spot rate, forward rate, and interest rates. Formula: F/S = (1 + i_A) / (1 + i_B). Arbitrage-enforced.

- Uncovered Interest Rate Parity (UIRP): Links expected spot rate and interest rates. Formula: E(S₁)/S₀ = (1 + i_A) / (1 + i_B). Expectational.

- Relative Purchasing Power Parity (PPP): Links expected spot rate change and inflation differential. Formula: E(S₁)/S₀ = (1 + Inflation_A) / (1 + Inflation_B).

- International Fisher Effect (IFE): Links interest rate differential and expected exchange rate change. Formula: (1 + i_A) / (1 + i_B) = E(S₁)/S₀.

6.2 Parity Condition Interconnections

- CIRP + Unbiased Forward Rate Hypothesis → UIRP: If forward rate equals expected future spot rate [F = E(S₁)], then CIRP implies UIRP.

- PPP + Domestic Fisher Effect → IFE: If PPP holds and Fisher Effect holds domestically in both countries, then IFE must hold.

- UIRP = IFE: These are mathematically equivalent expressions. Both state: E[%ΔS] = i_A - i_B.

- Common Thread: All conditions assume no arbitrage, perfect capital mobility, and rational expectations. Real-world frictions cause deviations.

6.3 Parity Relationships Summary Table

6.4 Practical Implications for Currency Analysis

- Forward Rates as Predictors: CIRP ensures forward rates are arbitrage-free, but they are biased predictors of future spot rates (UIRP fails).

- Inflation and Currency: High inflation countries see currency depreciation over long periods (PPP works), but short-run disconnection is common.

- Interest Rates and Currency: High interest rate currencies often appreciate short-term (carry trade), violating UIRP/IFE, but may depreciate long-term.

- Real vs. Nominal Rates: Real interest rate differentials (not just nominal) matter for capital flows and currency movements.

7. Currency Carry Trade

7.1 Carry Trade Mechanics

- Definition: Strategy borrowing in low interest rate currency (funding currency) and investing in high interest rate currency (target currency).

- Profit Source: Interest rate differential (carry). Trader earns positive carry if target currency rate > funding currency rate.

- Uncovered Position: Carry trade does not hedge currency risk (no forward contract). Exposed to spot rate movements.

- Carry Trade Return: Return ≈ (i_High - i_Low) + %ΔS(High/Low). Profit if interest differential exceeds currency depreciation.

7.2 Why Carry Trades Can Be Profitable

- UIRP Violation: If UIRP held perfectly, expected currency depreciation would offset interest differential (zero expected profit). Empirically, UIRP fails.

- Forward Rate Bias: High interest rate currencies depreciate less than forward discount implies (forward rate overpredicts depreciation).

- Risk Premium Explanation: Carry trade earns risk premium for bearing crash risk. High interest rate currencies can depreciate sharply during crises.

- Volatility Patterns: Carry trades profitable in low-volatility, risk-on environments. Suffer losses during high-volatility, risk-off periods (sudden unwinding).

7.3 Carry Trade Risks

- Currency Depreciation: If high interest rate currency depreciates more than interest differential, carry trade loses money.

- Crash Risk: Carry trades exhibit negative skewness (small gains most of time, large losses occasionally). "Picking up nickels in front of steamroller."

- Funding Currency Appreciation: If funding currency (low rate) sharply appreciates, carry trade unwinds with losses (e.g., JPY carry trades in 2008).

- Liquidity Risk: During stress, traders rush to unwind carry positions simultaneously, causing sharp reversals and liquidity problems.

- Volatility Spikes: Carry trades perform poorly when FX volatility rises suddenly. Often correlate with equity market crashes.

7.4 Carry Trade Implementation and Monitoring

- Currency Pair Selection: Choose currencies with large, stable interest rate differentials. Historically: Borrow JPY/CHF, invest in AUD/NZD/BRL.

- Leverage: Carry trades often use leverage to amplify returns. Increases both gains and losses.

- Risk Management: Use stop-loss orders, position limits, and volatility monitoring to manage downside risk.

- Market Conditions: Favor carry trades in stable, low-volatility, risk-on environments. Avoid or hedge during uncertain, high-volatility periods.

8. Currency Risk in Portfolio Management

8.1 Currency Risk Exposure

- Definition: Risk that foreign currency movements affect portfolio value when converted to domestic currency (base currency).

- Sources: Foreign equity investments, foreign bond investments, foreign direct investments, receivables/payables in foreign currency.

- Return Decomposition: Total Return (Domestic) = Foreign Asset Return + Currency Return + Cross-Product Term.

- Formula: R_DC = R_FC + R_FX + (R_FC × R_FX), where R_DC = domestic currency return, R_FC = foreign currency return, R_FX = currency return.

- Approximation: For small returns, R_DC ≈ R_FC + R_FX (cross-product negligible).

8.2 Strategic vs. Tactical Currency Management

- Strategic (Passive) Hedging: Setting benchmark hedge ratio based on long-term policy. Typically 0% (unhedged), 50%, or 100% (fully hedged) based on risk tolerance.

- Tactical (Active) Hedging: Deviating from benchmark hedge ratio based on currency views and market conditions to add value.

- Discretionary Approach: Portfolio manager actively decides hedge ratios based on forecasts and judgment.

- Rules-Based Approach: Systematic rules adjust hedge ratios based on quantitative signals (e.g., valuation, momentum, carry).

8.3 Currency Hedging Instruments

- Forward Contracts: Most common hedging tool. Lock in exchange rate for future date. Customizable, OTC, counterparty risk.

- Currency Futures: Standardized exchange-traded forwards. Liquid for major currencies. Daily mark-to-market, margin requirements.

- Currency Options: Provide asymmetric payoff (hedge downside, retain upside). Cost = premium paid. Useful when directional view uncertain.

- Currency Swaps: Exchange principal and interest in different currencies. Used for longer-term hedging of bond portfolios or liabilities.

8.4 Hedging Effectiveness and Costs

- Roll Yield: Gain or loss from rolling forward contracts at maturity. Equals forward premium/discount. Currency with higher interest rate has negative roll yield (cost).

- Hedging Cost Formula: Hedging Cost ≈ (i_Foreign - i_Domestic). Hedging high interest rate currency to low interest rate currency incurs cost.

- Basis Risk: Imperfect correlation between hedging instrument and underlying exposure. Arises from maturity mismatch, contract size mismatch, or cross-hedging.

- Rebalancing Frequency: More frequent rebalancing improves hedge effectiveness but increases transaction costs. Trade-off between precision and cost.

8.5 Factors Influencing Hedge Ratio Decision

- Currency Volatility: Higher volatility increases potential currency impact, favoring higher hedge ratios for risk-averse investors.

- Correlation with Domestic Assets: If foreign currency negatively correlates with domestic assets (natural hedge), lower hedge ratio optimal.

- Hedging Costs: High costs (large interest rate differential) may justify lower hedge ratios if expected currency gain insufficient.

- Investment Horizon: Longer horizons see currency movements mean-revert (PPP), potentially reducing need for hedging.

- Risk Tolerance: Risk-averse investors prefer higher hedge ratios (minimize volatility). Risk-seeking investors may leave positions unhedged or underhedged.

9. Forecasting Exchange Rates

9.1 Challenges in Exchange Rate Forecasting

- Random Walk Hypothesis: Exchange rates follow random walk in short run. Future spot rate's best predictor is current spot rate. Hard to beat statistically.

- Meese-Rogoff Puzzle: Empirical finding that economic models fail to outperform random walk in forecasting exchange rates at short horizons (less than 1 year).

- Multiple Influences: Exchange rates affected by interest rates, inflation, capital flows, current account, political factors, market sentiment-complex interactions.

- Regime Changes: Currency markets shift between regimes (carry, momentum, risk-off). Models working in one regime fail in another.

9.2 Fundamental Analysis Approach

- PPP-Based Models: Use relative inflation rates and price levels to estimate long-run equilibrium exchange rate. Currencies overvalued/undervalued vs PPP.

- Interest Rate Parity Models: Use interest rate differentials to forecast based on UIRP/IFE. Limited short-run accuracy due to UIRP failure.

- Balance of Payments Approach: Analyze current account and capital flows. Persistent current account deficits suggest currency depreciation pressure over time.

- Monetary Models: Link exchange rates to money supply, output, interest rates. Flexible-price monetary model: S(A/B) = (M_A/M_B) × (Y_B/Y_A) × f(i_A, i_B).

- Portfolio Balance Approach: Focus on capital flows and asset demand. Currency appreciates if foreign demand for domestic assets increases.

9.3 Technical Analysis Approach

- Definition: Use past price patterns, trends, and trading volumes to forecast future exchange rate movements. Assumes past patterns repeat.

- Trend Following: Identify and follow trends (uptrends, downtrends). Use moving averages, breakouts, support/resistance levels.

- Momentum Indicators: RSI (Relative Strength Index), MACD (Moving Average Convergence Divergence), stochastic oscillators identify overbought/oversold conditions.

- Chart Patterns: Head and shoulders, double tops/bottoms, triangles, flags signal potential reversals or continuations.

- Empirical Evidence: Technical analysis can add value in short-term trading (days to weeks). Less useful for long-term forecasting.

9.4 Order Flow and Market Microstructure

- Order Flow Analysis: Examines actual buy/sell orders in currency markets. Large order flows can predict short-term price movements.

- Customer Order Flow: Central banks and dealers observe retail vs institutional flows. Persistent one-way flows signal momentum.

- Market Depth and Liquidity: Thin markets with low liquidity show larger price impacts from orders. Major currency pairs have deep liquidity.

- High-Frequency Data: Intraday patterns, bid-ask spreads, transaction volumes provide signals for very short-term (minutes to hours) forecasting.

9.5 Forecasting Effectiveness by Time Horizon

- Short-Term (Days to Weeks): Technical analysis, order flow, and momentum strategies moderately effective. Random walk hard to beat consistently.

- Medium-Term (Months to 1 Year): Fundamental models perform poorly (Meese-Rogoff puzzle). Carry trade signals (interest differentials) have some predictive power.

- Long-Term (Multi-Year): Fundamental models (PPP, productivity differentials) gain traction. Real exchange rates mean-revert to fundamentals over long periods.

- Trap Alert: No single model consistently forecasts accurately across all horizons. Combine models and judgment for best results.

10. Exchange Rate Regimes

10.1 Fixed (Pegged) Exchange Rate Regime

- Definition: Country's central bank commits to maintain exchange rate at specific level (peg) vs another currency or basket.

- Mechanism: Central bank intervenes by buying/selling foreign currency to maintain peg. Uses foreign exchange reserves.

- Advantages: Reduces exchange rate uncertainty, facilitates trade/investment, imposes monetary discipline, anchors inflation expectations.

- Disadvantages: Loss of independent monetary policy (Impossible Trinity), vulnerable to speculative attacks, requires large reserves.

- Examples: Hong Kong Dollar (HKD) pegged to USD. Historically, many countries pegged to USD or gold standard.

- Currency Board: Strict form of fixed regime. Monetary base fully backed by foreign reserves. No discretionary monetary policy (e.g., Hong Kong).

10.2 Floating (Flexible) Exchange Rate Regime

- Definition: Exchange rate determined by market forces (supply and demand). No central bank intervention commitment.

- Pure Float: Completely market-determined. Central bank never intervenes (rare in practice).

- Managed (Dirty) Float: Exchange rate mostly market-determined, but central bank intervenes occasionally to smooth volatility or influence level.

- Advantages: Independent monetary policy, automatic adjustment mechanism for external imbalances, no reserve depletion risk.

- Disadvantages: Exchange rate volatility and uncertainty, may amplify economic shocks, risk of overshooting.

- Examples: US Dollar (USD), Euro (EUR), Japanese Yen (JPY), British Pound (GBP) are major floating currencies.

10.3 Intermediate (Hybrid) Regimes

- Crawling Peg: Exchange rate adjusted periodically in small amounts (e.g., based on inflation differential). Combines stability with gradual adjustment.

- Target Zone (Band): Exchange rate allowed to fluctuate within a band around central parity. Central bank intervenes at band edges. (e.g., ERM before Euro).

- Managed Float with Implicit Target: Central bank has undisclosed target range and intervenes to keep rate within it. Lacks transparency.

10.4 The Impossible Trinity (Trilemma)

- Definition: A country cannot simultaneously maintain: (1) Fixed exchange rate, (2) Independent monetary policy, (3) Free capital flows. Must sacrifice one.

- Fixed Rate + Free Capital Flows → No Independent Policy: Monetary policy must defend peg. Interest rates determined by anchor currency (e.g., Eurozone members).

- Fixed Rate + Independent Policy → Capital Controls: Must restrict capital flows to prevent speculative attacks (e.g., China historically).

- Independent Policy + Free Capital Flows → Floating Rate: Exchange rate adjusts freely, allowing policy independence (e.g., US, UK).

- Policy Implication: Countries choose regime based on priorities (stability vs autonomy vs openness).

10.5 Factors Influencing Regime Choice

- Economic Size and Diversification: Large, diversified economies better able to handle floating rates. Small, specialized economies may prefer pegs for stability.

- Trade Patterns: Countries with trade concentrated with single partner often peg to partner's currency (reduce transaction costs).

- Inflation History: Countries with poor inflation credibility may use fixed rate as commitment device (import credibility from anchor country).

- Capital Mobility: High capital mobility makes fixed rates harder to maintain (vulnerable to attacks). Floating more sustainable.

- Shock Nature: If shocks mainly real (productivity, terms of trade), floating better. If shocks mainly monetary, fixed may be better.

11. Currency Crises

11.1 Balance of Payments Crisis (First-Generation Models)

- Mechanism: Government runs persistent fiscal deficits financed by money creation (monetization). Inflation rises, eroding competitiveness.

- Speculative Attack: Investors anticipate central bank will run out of reserves defending peg. Rush to convert domestic currency before devaluation.

- Crisis Trigger: Reserves depleted, central bank abandons peg, sharp devaluation occurs. Often sudden and predictable collapse.

- Fundamental Cause: Inconsistent macroeconomic policies (expansionary fiscal/monetary policy incompatible with fixed rate).

- Historical Example: Latin American crises in 1970s-1980s (Argentina, Mexico). Excessive money printing led to reserve depletion.

11.2 Self-Fulfilling Crisis (Second-Generation Models)

- Mechanism: Even without poor fundamentals, market expectations can trigger crisis. Multiple equilibria possible (peg survives or collapses).

- Expectation Shift: If market expects devaluation, interest rates spike to defend peg. Higher rates cause recession, making devaluation optimal.

- Policy Trade-Off: Government weighs cost of defending peg (high interest rates, recession) vs cost of devaluation (inflation, credibility loss).

- Crisis Dynamics: If market believes government will abandon peg, attack becomes self-fulfilling. Speculative attack forces devaluation even if fundamentals moderate.

- Historical Example: European Exchange Rate Mechanism (ERM) crisis 1992-93. UK, Italy forced to exit despite reasonable fundamentals. George Soros' famous attack on British Pound.

11.3 Financial Sector and Currency Crisis (Third-Generation Models)

- Twin Crises: Banking crisis and currency crisis occur together. Weak banking system amplifies currency pressures.

- Mechanism: Banks have currency mismatches (borrow foreign currency, lend domestic). Devaluation causes bank losses and failures.

- Moral Hazard: Implicit government guarantees encourage excessive risk-taking (foreign currency borrowing). When crisis hits, government faces bank bailouts or currency collapse.

- Contagion: Crisis in one country spreads to others with similar vulnerabilities (regional contagion through capital flows and sentiment).

- Historical Example: Asian Financial Crisis 1997-98 (Thailand, Indonesia, South Korea). Currency pegs collapsed alongside banking system failures.

11.4 Warning Indicators of Currency Crises

- Current Account Deficit: Large, persistent deficits signal external imbalance. Deficit > 5% of GDP is warning sign.

- Foreign Exchange Reserve Depletion: Rapid decline in reserves indicates central bank struggling to defend peg. Low reserves relative to short-term debt critical.

- Real Exchange Rate Overvaluation: Currency significantly overvalued vs PPP or historical averages. Loss of competitiveness, exports decline.

- Credit Boom and Asset Bubbles: Rapid credit growth, rising property/stock prices suggest unsustainable lending. Often precedes twin crises.

- Short-Term Debt and Maturity Mismatch: High short-term foreign currency debt relative to reserves. Refinancing risk if capital flows reverse.

- Political Instability: Elections, political uncertainty, weak institutions increase crisis risk. Market questions government commitment to peg.

11.5 Policy Responses to Currency Crises

- Devaluation (Float): Abandon peg, allow currency to depreciate. Restores competitiveness, but may trigger inflation and capital flight.

- Interest Rate Defense: Raise interest rates sharply to make holding currency attractive. Defends peg but causes recession.

- Capital Controls: Restrict outflows to stop speculative attack. May work short-term, damages long-term credibility and investment (Malaysia 1998).

- International Assistance: IMF loans provide reserves to defend currency and finance adjustment. Conditional on policy reforms (austerity, structural changes).

- Preemptive Adjustment: Implement fiscal consolidation, structural reforms, and gradual rate adjustment before crisis hits. Requires political will.

11.6 Contagion and Spillover Effects

- Trade Linkages: Devaluation in one country makes its exports cheaper, hurting competitiveness of trading partners (competitive devaluation pressure).

- Financial Linkages: Banks and investors with exposure to crisis country face losses. Pull capital from similar countries (indiscriminate selling).

- Wake-Up Call Effect: Crisis in one country alerts markets to vulnerabilities elsewhere. Reassessment of risk spreads crisis regionally.

- Herd Behavior: Investors follow crowd during crisis, selling emerging market assets broadly regardless of fundamentals.

- Historical Examples: Asian Financial Crisis spread from Thailand to Indonesia, Korea, Malaysia. Tequila Crisis (Mexico 1994) affected Argentina, Brazil.

12. Exam-Relevant Practice Application

12.1 Sample Problem: Forward Rate Calculation

Question: Spot EUR/USD = 1.2000. Eurozone 1-year interest rate = 2%. US 1-year interest rate = 4%. Calculate 1-year forward EUR/USD rate and determine if EUR is at forward premium or discount.

Solution:

- Formula: F = S × [(1 + i_USD) / (1 + i_EUR)]

- F = 1.2000 × [(1.04) / (1.02)] = 1.2000 × 1.0196 = 1.2235

- EUR is at forward premium (F > S). EUR strengthens because US rate higher (USD depreciates vs EUR per CIRP).

- Forward premium % = [(1.2235 - 1.2000) / 1.2000] × 100 = 1.96% ≈ interest differential (4% - 2%).

12.2 Sample Problem: Currency Return Calculation

Question: A US investor invests in German bonds. German bond returns 5% in EUR. EUR/USD spot rate moves from 1.2000 to 1.2600. Calculate total return in USD.

Solution:

- Foreign asset return (EUR) = 5%

- Currency return = (1.2600 - 1.2000) / 1.2000 = 0.05 = 5%

- Total USD return = (1 + 0.05) × (1 + 0.05) - 1 = 1.1025 - 1 = 0.1025 = 10.25%

- Approximation: 5% + 5% = 10% (close, but exact is 10.25% due to compounding).

12.3 Sample Problem: Covered vs. Uncovered Returns

Question: A Japanese investor can invest domestically at 0.5% or in Australia at 3.5%. Spot JPY/AUD = 80. 1-year forward = 82.36. Should investor hedge currency risk? What is return in each scenario if spot in 1 year is 81?

Solution:

- Covered (Hedged): Lock in forward rate 82.36. Return = Australian rate + forward premium/discount. Forward discount = (82.36 - 80)/80 = 2.95%. Total ≈ 3.5% + (-2.95%) ≈ 0.55% (approximately domestic rate, CIRP holds).

- Uncovered (Unhedged): Actual spot = 81. Currency loss = (81 - 80)/80 = 1.25%. Total return ≈ 3.5% + (-1.25%) ≈ 2.25% (better than domestic 0.5%, but took currency risk).

- Decision: Hedging eliminates currency risk, return ≈ domestic rate. Unhedged depends on actual spot rate (risky but potentially higher return).

12.4 Common Exam Mistakes (Trap Alerts)

- Confusing Base and Price Currency: In A/B quotation, B is base (denominator). If B appreciates, A/B increases (more A per B). Review quotation conventions carefully.

- Bid-Offer Confusion: When buying base currency, use offer rate (higher). When selling base currency, use bid rate (lower). Always unfavorable to customer.

- CIRP vs. UIRP: CIRP is arbitrage-free (always holds). UIRP is expectational (frequently violated). Don't assume UIRP holds when forecasting.

- PPP Time Horizon: PPP fails short-term, works long-term. Don't apply PPP for 1-month forecast; better for 5-10 year horizon.

- Forward Premium Sign: Currency with higher interest rate trades at forward discount (F < s),="" not="" premium.="" interest="" parity="">

- Carry Trade Risk: Carry trades earn positive carry but face crash risk. Not "free money"-compensates for tail risk.

- Hedging Cost Direction: Hedging from high-rate to low-rate currency incurs cost (negative roll yield). Hedging from low-rate to high-rate currency earns roll yield (benefit).

12.5 Key Formulas Summary for Quick Reference

- Forward Rate: F(A/B) = S(A/B) × [(1 + i_A × t) / (1 + i_B × t)] or F/S = (1 + i_A) / (1 + i_B) annualized.

- Forward Premium/Discount %: [(F - S) / S] × 100 ≈ (i_A - i_B) × 100.

- Covered Interest Rate Parity: (F - S) / S = (i_A - i_B) / (1 + i_B) ≈ i_A - i_B for small rates.

- Currency Return Contribution: Total Return = R_Foreign + R_FX + (R_Foreign × R_FX). Approximation: R_Foreign + R_FX.

- Relative PPP: %ΔS(A/B) ≈ Inflation_A - Inflation_B. Or S₁/S₀ = (1 + Inflation_A) / (1 + Inflation_B).

- International Fisher Effect: E[%ΔS(A/B)] ≈ i_A - i_B. Equivalent to UIRP.

- Real Exchange Rate: RER = S(A/B) × (CPI_B / CPI_A). %ΔRER = %ΔS - (Inflation_A - Inflation_B).

- Carry Trade Return: Return ≈ (i_Target - i_Funding) + %ΔS(Target/Funding).

- Cross Rate: S(A/B) = S(A/C) × S(C/B). With spreads, use bid and offer appropriately.

Currency exchange rates are central to international finance and portfolio management. Mastery requires understanding quotation conventions, no-arbitrage pricing (CIRP), long-run equilibrium relationships (PPP), and the practical failures of expectational parity conditions (UIRP/IFE). Successful currency management integrates these theoretical frameworks with practical considerations of carry trades, hedging strategies, forecasting limitations, and crisis risks. For CFA Level I, focus on precise formula application, understanding when parity conditions hold vs. fail, and recognizing common traps in exam questions. Always clarify base vs. price currency, apply bid-offer spreads correctly, and distinguish arbitrage relationships (must hold) from expected relationships (often violated).