Intangible Assets

Intangible Assets are non-physical, identifiable assets that provide economic benefits to an entity over multiple periods. Unlike tangible assets, they lack physical substance but hold significant value through legal rights, competitive advantages, or contractual benefits. Understanding their classification, measurement, and amortization is critical for accurate financial reporting and compliance with US GAAP standards.

1. Definition and Recognition Criteria

An Intangible Asset is an identifiable non-monetary asset without physical substance. Recognition requires meeting specific criteria to ensure assets are properly recorded on the balance sheet.

1.1 Recognition Criteria

- Identifiability: The asset must be separable (can be sold, transferred, licensed) OR arise from contractual/legal rights regardless of separability.

- Control: The entity must have power to obtain future economic benefits and restrict others' access to those benefits.

- Future Economic Benefits: The asset must be expected to generate revenues, cost savings, or other economic benefits.

- Measurability: The cost of the asset can be reliably measured at acquisition or creation date.

1.2 Common Examples of Intangible Assets

- Patents: Legal rights to exclude others from making, using, or selling an invention (typically 20 years protection).

- Trademarks: Distinctive signs, symbols, or names identifying products or services from competitors.

- Copyrights: Exclusive rights to reproduce, distribute, or display creative works (author's life plus 70 years).

- Franchises: Contractual rights to operate a business using another entity's brand and business model.

- Customer Lists: Databases containing customer information with economic value through repeat business.

- Non-compete Agreements: Contractual restrictions preventing parties from competing in specific markets/timeframes.

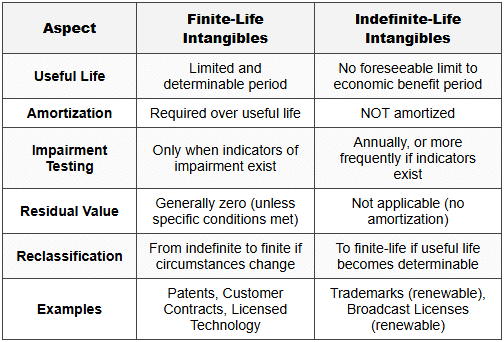

2. Finite Life vs Indefinite Life Intangibles

The classification of intangible assets as finite-lived or indefinite-lived determines their subsequent accounting treatment. This distinction directly impacts amortization requirements and impairment testing frequency.

2.1 Finite-Life Intangible Assets

A finite-life intangible has a limited useful life that can be reasonably estimated based on legal, regulatory, contractual, competitive, economic, or other factors.

- Definition: Intangibles with foreseeable limit to the period of expected cash flow generation or legal protection.

- Useful Life Determination: Based on the shorter of legal life, contractual life, or economic useful life estimated by management.

- Accounting Treatment: Subject to systematic amortization over useful life and impairment testing when indicators exist.

- Residual Value: Generally assumed to be zero unless a third party commits to purchase the asset at end of useful life OR active market exists for the asset.

2.1.1 Common Finite-Life Examples

- Patents: Legal life typically 20 years, but economic life may be shorter due to technological obsolescence.

- Copyrights: Author's life plus 70 years legally, but economic life often much shorter based on market demand.

- Customer Contracts: Limited to the specific contract term with determinable expiration date.

- Licensed Technology: Restricted to the license agreement period with defined termination date.

2.2 Indefinite-Life Intangible Assets

An indefinite-life intangible has no foreseeable limit to the period over which the asset is expected to generate net cash inflows for the entity.

- Definition: Intangibles where no legal, regulatory, contractual, competitive, economic, or other factors limit the useful life.

- Key Characteristic: "Indefinite" does NOT mean "infinite" - it means no reasonably determinable endpoint exists at initial recognition.

- Accounting Treatment: NOT amortized, but tested for impairment annually (or more frequently if indicators exist).

- Reassessment Required: Management must review the indefinite classification each reporting period; reclassification to finite-life is possible if circumstances change.

2.2.1 Common Indefinite-Life Examples

- Trademarks: Can be renewed indefinitely with minimal cost and no foreseeable abandonment planned.

- Broadcast Licenses: Renewable indefinitely if regulatory conditions met, with no technological obsolescence expected.

- Taxi Medallions: Perpetual licenses in certain jurisdictions with no expiration (though economic factors may change this classification).

2.3 Comparison: Finite vs Indefinite Life Intangibles

2.4 Trap Alert: Common Classification Mistakes

- Trademark Confusion: Trademarks are indefinite-life ONLY if renewable at minimal cost and the entity intends to renew indefinitely. If renewal is uncertain or cost-prohibitive, classify as finite-life.

- Legal vs Economic Life: Use the SHORTER of legal life or economic useful life. A 20-year patent may have only 5-year economic usefulness due to rapid technology changes.

- Indefinite ≠ Infinite: Students often confuse "indefinite" with "permanent." Indefinite means "not currently determinable," not "lasts forever."

- Goodwill Exception: Goodwill is indefinite-life but follows different impairment rules (tested at reporting unit level, not individually).

3. Amortization of Finite-Life Intangible Assets

Amortization is the systematic allocation of the amortizable amount (cost minus residual value) of a finite-life intangible asset over its useful life. This process matches the asset's cost to the periods benefiting from its use.

3.1 Amortization Requirements and Methods

- Amortizable Amount Formula: Amortizable Amount = Cost of Intangible Asset - Residual Value

- Commencement: Amortization begins when the asset is available for use (i.e., when it is in the location and condition necessary for operation).

- Method Selection: Use the pattern in which economic benefits are consumed. If pattern cannot be reliably determined, use straight-line method as default.

- Residual Value Default: Assumed to be zero unless specific conditions are met (third-party purchase commitment or active market exists).

3.2 Amortization Methods

3.2.1 Straight-Line Method (Most Common)

Allocates equal expense amounts to each period over the useful life. This is the default method when consumption pattern is uncertain.

Formula: Annual Amortization Expense = (Cost - Residual Value) ÷ Useful Life in Years

Example: Patent acquired for $100,000, 10-year useful life, zero residual value.

- Annual Amortization = ($100,000 - $0) ÷ 10 = $10,000 per year

- Journal Entry: Debit Amortization Expense $10,000; Credit Accumulated Amortization $10,000

3.2.2 Units-of-Production Method

Allocates amortization based on actual usage, output, or activity level. Use when consumption pattern directly correlates with production volume or usage units.

Formula: Amortization Expense = (Cost - Residual Value) × (Units Produced in Period ÷ Total Estimated Units)

Example: Patent for manufacturing process, $200,000 cost, expected to produce 500,000 units total, 50,000 units produced this year.

- Amortization = ($200,000 - $0) × (50,000 ÷ 500,000) = $20,000

3.2.3 Accelerated Methods (Rare for Intangibles)

Methods like declining balance are permitted if they better reflect the consumption pattern. Rarely used for intangibles unless clear evidence exists that benefits decline rapidly in early years.

3.3 Useful Life Determination Factors

Management must consider multiple factors to estimate the useful life of finite-life intangibles:

- Legal/Contractual Provisions: Statutory or contractual expiration dates provide maximum useful life limits.

- Expected Use: Anticipated period the entity will use the asset based on operational plans.

- Technological Obsolescence: Rate of innovation in the industry that may render the intangible obsolete.

- Competitive Factors: Actions by competitors that could reduce the asset's economic benefits.

- Maintenance/Renewal: Costs and feasibility of maintaining or renewing the asset's benefits.

- Demand Changes: Expected stability or decline in demand for products/services the intangible supports.

3.4 Amortization Presentation and Disclosure

- Balance Sheet Presentation: Intangible assets shown at cost minus accumulated amortization (net carrying amount). Can present using direct reduction OR accumulated amortization contra-account.

- Income Statement: Amortization expense included in operating expenses, typically within administrative or general expenses.

- Required Disclosures: Gross carrying amount, accumulated amortization, amortization method, useful lives or rates, aggregate amortization expense for the period.

- Future Amortization: Must disclose estimated amortization expense for each of the next five years and total thereafter.

3.5 Changes in Amortization Estimates

Changes in useful life or residual value estimates are changes in accounting estimate (NOT restatements). Apply prospectively from the change date.

Revised Amortization Formula: Revised Annual Amortization = (Current Carrying Amount - Revised Residual Value) ÷ Revised Remaining Useful Life

Example: Patent with $80,000 carrying amount, originally 10-year life with 5 years remaining. Management revises remaining life to 8 years.

- Revised Annual Amortization = ($80,000 - $0) ÷ 8 = $10,000 (instead of $16,000 under original estimate)

- No retroactive adjustment; apply new rate going forward only.

3.6 Trap Alert: Amortization Common Errors

- Residual Value Assumption: Students often forget residual value is typically ZERO unless specific conditions exist. Don't assume market value at end of life.

- Amortization Start Date: Begins when asset is "ready for use," NOT necessarily the purchase date. If additional setup/development needed, delay amortization start.

- Method Selection: Straight-line is default, but you MUST use consumption pattern method if reliably determinable. Units-of-production may be required for certain assets.

- Indefinite-Life Confusion: Remember: indefinite-life intangibles are NEVER amortized, only tested for impairment annually. Don't apply amortization formulas to trademarks or goodwill.

- Estimate Changes: Changes in useful life are prospective only; do NOT restate prior periods or adjust accumulated amortization retroactively.

4. Special Amortization Considerations

4.1 Intangibles with Legal vs Economic Life Differences

When legal life differs from economic useful life, use the shorter period for amortization purposes.

- Patent Example: 20-year legal life but technology becomes obsolete in 5 years → Amortize over 5 years.

- Franchise Example: 30-year contractual term but entity plans to exit market in 10 years → Amortize over 10 years.

4.2 Renewable Intangibles

For intangibles subject to renewal (e.g., broadcast licenses, certain franchises), determine if indefinite or finite classification applies:

- Indefinite Classification Criteria: Renewal expected at minimal cost, no legal/regulatory/economic factors limit useful life, entity intends to renew indefinitely.

- Finite Classification: If renewal uncertain, costly, or limited number of renewals permitted, classify as finite-life and amortize over initial term plus expected renewal periods.

4.3 Intangibles Used in Research and Development

Acquired intangibles used in R&D activities follow specific rules:

- Acquired in Asset Acquisition: If the intangible has no alternative future use beyond a specific R&D project, expense immediately as R&D cost.

- Alternative Future Use Exists: Capitalize and amortize over useful life if the intangible can be used in other projects or sold.

- IPR&D (In-Process R&D): Acquired in business combinations, initially measured at fair value as indefinite-life asset, then reclassified to finite-life when project completes or abandoned (written off).

4.4 Software Development Costs

Software for internal use follows specific capitalization and amortization rules:

- Preliminary Stage: Expense all costs (planning, evaluating alternatives, vendor selection).

- Application Development Stage: Capitalize costs (design, coding, testing) until software ready for intended use.

- Post-Implementation Stage: Expense all costs (training, maintenance, minor upgrades).

- Amortization: Begin when software is ready for use; amortize over estimated useful life using straight-line unless another method better reflects usage pattern.

5. Impairment of Intangible Assets

Intangible assets must be tested for impairment when indicators suggest carrying amount may not be recoverable (finite-life) or annually (indefinite-life).

5.1 Impairment Testing for Finite-Life Intangibles

Apply the two-step impairment test when impairment indicators exist:

- Recoverability Test: Compare carrying amount to sum of undiscounted future cash flows from the asset. If carrying amount exceeds undiscounted cash flows, proceed to Step 2.

- Measurement Step: Impairment Loss = Carrying Amount - Fair Value. Record loss as expense; reduce carrying amount to fair value (new cost basis).

Impairment Indicators: Significant decline in market value, adverse legal/regulatory changes, technological obsolescence, loss of key customer relationships.

Key Rule: Impairment losses on finite-life intangibles are NOT reversible under US GAAP once recorded.

5.2 Impairment Testing for Indefinite-Life Intangibles

- Frequency: Test annually at same time each year, or more frequently if impairment indicators arise.

- Simplified Approach Allowed: Entity may perform qualitative assessment first. If more-likely-than-not (>50%) that fair value exceeds carrying amount, no quantitative test needed.

- Quantitative Test: If qualitative assessment fails or entity chooses to skip it, compare carrying amount directly to fair value. Record impairment loss if carrying amount exceeds fair value.

- No Recoverability Test: Unlike finite-life intangibles, indefinite-life assets skip the undiscounted cash flow step.

5.3 Trap Alert: Impairment vs Amortization Confusion

- Amortization vs Impairment: Amortization is systematic allocation; impairment is a loss recognition event. They are separate processes with different triggers and calculations.

- Indefinite-Life Assets: Never amortized, always tested for impairment annually. Students often incorrectly apply amortization to trademarks.

- Loss Reversal: Under US GAAP, impairment losses on intangibles are NEVER reversed (even if fair value recovers later). This differs from inventory or certain other asset classes.

- Fair Value Measurement: Use the price that would be received to sell the asset in orderly transaction (exit price), not replacement cost or value-in-use.

6. Acquisition and Initial Measurement

6.1 Acquisition Methods and Initial Recognition

Intangible assets are initially measured based on acquisition method:

- Purchased Separately: Record at cost, including purchase price, legal fees, registration costs, and other directly attributable expenditures to prepare asset for use.

- Acquired in Business Combination: Record at fair value at acquisition date, separate from goodwill if identifiability criteria met.

- Internally Generated: Generally expensed as incurred (R&D costs), except specific items like software development costs (after technological feasibility) or website development costs (application stage).

- Government Grants: May receive intangibles at no cost or nominal cost; measure at fair value or nominal amount per entity's accounting policy election.

6.2 Internal Development Prohibition

Under US GAAP, internally generated intangibles are generally NOT capitalized:

- Research and Development: Expensed as incurred; cannot capitalize internal R&D costs even if project successful.

- Brands/Mastheads/Customer Lists (Internal): Cannot be capitalized when internally developed; only recognize if acquired externally.

- Start-up Costs: All organization and start-up costs expensed as incurred.

- Exception - Software/Website Costs: Specific guidance allows capitalization during application development stage for internal-use software and websites.

6.3 Basket Purchase Allocation

When multiple intangibles acquired in single transaction, allocate total cost based on relative fair values:

Formula: Allocated Cost = Total Purchase Price × (Fair Value of Individual Asset ÷ Total Fair Value of All Assets)

Example: Acquire trademark (FV $60,000) and patent (FV $40,000) for combined $90,000.

- Trademark Allocation = $90,000 × ($60,000 ÷ $100,000) = $54,000

- Patent Allocation = $90,000 × ($40,000 ÷ $100,000) = $36,000

7. Disposal and Derecognition

7.1 Disposal Accounting

Remove intangible asset from books upon disposal (sale, abandonment, exchange) or when no future economic benefits expected.

Gain/Loss Calculation: Gain or Loss on Disposal = Proceeds Received - Carrying Amount (Cost - Accumulated Amortization)

- Journal Entry for Sale: Debit Cash (proceeds), Debit Accumulated Amortization, Credit Intangible Asset (cost), Credit/Debit Gain/Loss on Disposal (balancing amount).

- Abandonment: Write off entire carrying amount as loss; no proceeds received.

- Income Statement: Gains/losses typically reported in "Other Income/Expense" section, not operating income (unless disposal part of ordinary activities).

7.2 Exchange Transactions

Exchanges of intangible assets follow nonmonetary exchange rules:

- Commercial Substance Exists: Measure acquired asset at fair value; recognize gain or loss on exchange.

- No Commercial Substance: Measure acquired asset at carrying amount of asset given up (no gain recognized; losses recognized).

- Boot (Cash) Received: May trigger partial gain recognition even without commercial substance if boot exceeds 25% threshold.

Intangible assets represent a critical component of modern business valuation and financial reporting. Proper classification as finite or indefinite-life drives the accounting treatment, determining whether systematic amortization or annual impairment testing applies. Mastery of amortization methods, useful life estimation, and impairment rules ensures accurate financial statement presentation and compliance with US GAAP requirements. Understanding the distinctions between purchased and internally developed intangibles, along with disposal accounting, completes the comprehensive framework necessary for professional accounting practice.