Double Entry Bookkeeping and the Accounting Equation

Welcome to the Language of Business: Double Entry Bookkeeping

Imagine you're managing a lemonade stand. You buy lemons for £10 cash, and now you have lemons worth £10 but £10 less cash. Something came in, something went out, but your overall wealth hasn't changed-you've just swapped one thing for another. This simple observation is the heartbeat of double entry bookkeeping, a system so elegant that it has remained virtually unchanged since an Italian monk named Luca Pacioli first documented it in 1494.

Double entry bookkeeping isn't just about recording transactions-it's about understanding the dual nature of every business event. Every action creates an equal and opposite reaction in your accounts. When you understand this, you unlock the ability to track, analyze, and communicate the financial story of any organization, from a corner shop to multinational corporations like Apple or Shell.

The Accounting Equation: The Foundation of Everything

Before we dive into double entry, we need to understand the accounting equation. This is the bedrock formula that describes the financial position of any business at any moment in time:

\[ \text{Assets} = \text{Liabilities} + \text{Equity} \]Let's break this down into plain English.

Assets: What the Business Owns

Assets are resources controlled by the business that are expected to bring future economic benefits. Think of them as anything valuable the business owns or has a right to.

Assets come in many forms:

- Cash - money in the bank or in a till

- Inventory - goods held for sale (like bottles of Coca-Cola in a warehouse)

- Receivables - money owed to you by customers who bought on credit

- Equipment - machinery, computers, delivery vans

- Buildings - offices, factories, retail stores

- Intellectual property - patents, trademarks, brand names

Consider Amazon. Its assets include massive warehouses, sophisticated computer servers, delivery trucks, inventory in stock, and the cash in its bank accounts. Each of these helps Amazon generate revenue.

Liabilities: What the Business Owes

Liabilities are obligations-amounts the business owes to outsiders. These are claims against the business's assets by people or organizations other than the owners.

Common liabilities include:

- Payables - money owed to suppliers for goods bought on credit

- Loans - bank borrowings that must be repaid

- Accrued expenses - bills not yet paid (electricity, wages earned by staff but not yet paid)

- Deferred revenue - money received from customers before you've delivered the service

When Tesla borrows money from a bank to build a new factory, that loan is a liability. Tesla has an obligation to repay that money with interest.

Equity: The Owners' Claim

Equity (also called capital or owners' equity) represents the owners' claim on the business assets after all liabilities have been settled. It's what would be left for the owners if the business sold everything it owned and paid off all its debts.

Equity can come from:

- Capital introduced - money or assets the owner puts into the business

- Retained profits - earnings the business has made and kept rather than distributing to owners

You can also rearrange the accounting equation to highlight equity:

\[ \text{Equity} = \text{Assets} - \text{Liabilities} \]This version makes it crystal clear: equity is the residual interest-what's left after deducting what you owe from what you own.

Why Must the Equation Always Balance?

Here's the beautiful logic: every asset a business has must have come from somewhere. Either it was funded by the owners (equity) or by borrowing from others (liabilities). There's no third source of funding-it's logically impossible.

If a business has £100,000 in assets, those assets were financed by some combination of owner investment and borrowings. The equation must balance because it's describing the same pool of resources from two perspectives:

- Left side (Assets): What form does the value take? Cash? Buildings? Inventory?

- Right side (Liabilities + Equity): Where did that value come from? Owners or creditors?

Let's see this in action with a simple example.

Example: Starting a Business

Sarah starts a graphic design business and contributes £5,000 of her own money. Let's analyze this transaction:

- The business now has £5,000 cash (an asset)

- This came from the owner, so equity increases by £5,000

- No liabilities exist yet

The accounting equation after this transaction:

\[ £5,000 \text{ (Assets)} = £0 \text{ (Liabilities)} + £5,000 \text{ (Equity)} \]Now Sarah buys a computer for £1,200 in cash. What happens?

- Cash decreases by £1,200 (one asset goes down)

- Equipment increases by £1,200 (another asset goes up)

- Liabilities and equity remain unchanged

The equation after the computer purchase:

\[ £3,800 \text{ (Cash)} + £1,200 \text{ (Equipment)} = £0 \text{ (Liabilities)} + £5,000 \text{ (Equity)} \] \[ £5,000 = £5,000 \]Notice that total assets remain £5,000-we've simply changed the composition. The equation still balances.

Next, Sarah takes a £2,000 loan from the bank. Now:

- Cash increases by £2,000 (asset up)

- Loan payable increases by £2,000 (liability up)

The equation becomes:

\[ £5,800 \text{ (Cash)} + £1,200 \text{ (Equipment)} = £2,000 \text{ (Loan)} + £5,000 \text{ (Equity)} \] \[ £7,000 = £7,000 \]The equation still balances. Every single transaction affects at least two items in the accounting equation, which brings us naturally to double entry bookkeeping.

Double Entry Bookkeeping: The Dual Aspect Concept

Double entry bookkeeping is built on a simple but powerful principle: every transaction affects at least two accounts. For every debit entry, there must be an equal and opposite credit entry. This isn't arbitrary-it reflects the dual nature of business transactions.

Think back to our lemonade stand. When you buy lemons for cash, two things happen simultaneously:

- You gain inventory (lemons)

- You lose cash

Both effects must be recorded to capture the complete picture.

Debits and Credits: Understanding the Mechanism

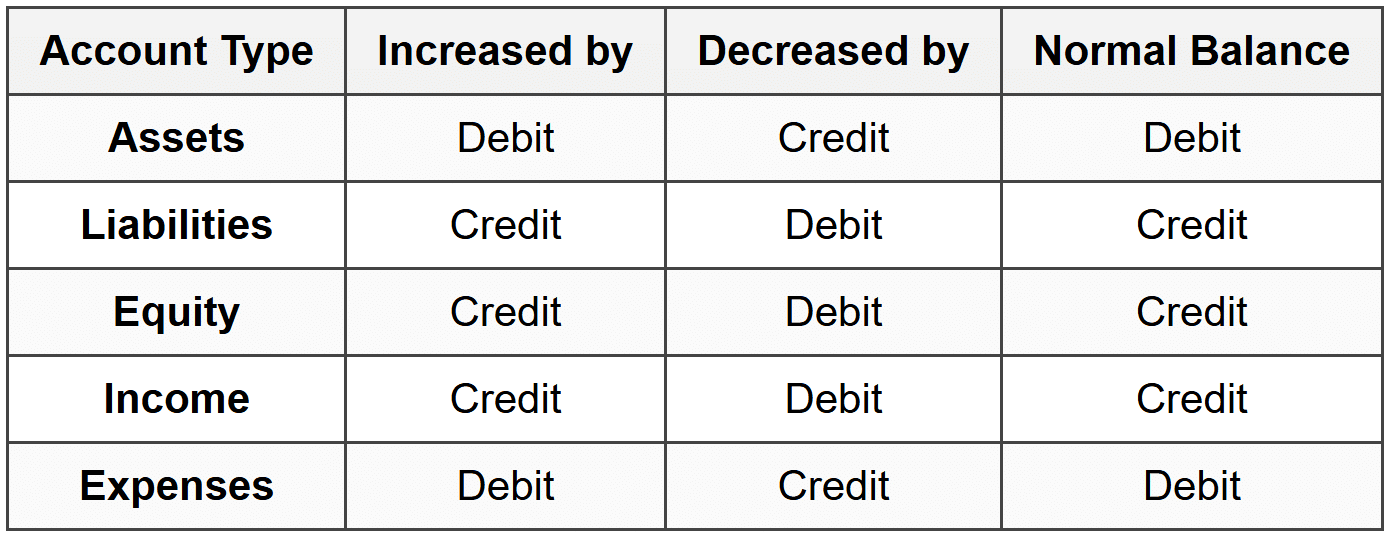

Here's where many beginners get confused. In everyday language, "debit" might mean money leaving your bank account, and "credit" might mean money coming in. Forget those meanings immediately. In accounting, debits and credits are simply the left side and right side of accounts-nothing more, nothing less.

Every account in your accounting system has two sides:

- Debit side - the left side

- Credit side - the right side

Whether an increase is recorded as a debit or credit depends entirely on what type of account it is. Here are the rules:

This might seem arbitrary, but there's logic here. Remember the accounting equation:

\[ \text{Assets} = \text{Liabilities} + \text{Equity} \]Assets are on the left side of the equation, so they increase with debits (left side entries). Liabilities and equity are on the right side, so they increase with credits (right side entries). This keeps the equation balanced.

Why Do Income and Expenses Follow These Rules?

Income (also called revenue) increases the business's wealth, which ultimately increases equity. Since equity increases with credits, income also increases with credits.

Expenses decrease the business's wealth, reducing equity. Since equity decreases with debits, expenses increase with debits. (Yes, it sounds odd-expenses "increase" as you spend more, but they're negative for your equity, so they follow the opposite rule.)

Let's expand the accounting equation to include income and expenses:

\[ \text{Assets} = \text{Liabilities} + \text{Equity} + \text{Income} - \text{Expenses} \]Or rearranged:

\[ \text{Assets} + \text{Expenses} = \text{Liabilities} + \text{Equity} + \text{Income} \]Now you can see why assets and expenses both increase with debits (they're on the left side), while liabilities, equity, and income all increase with credits (they're on the right side).

The Golden Rule: Debits Must Equal Credits

In every transaction, the total debits must equal the total credits. This is non-negotiable. If they don't match, you've made an error.

This golden rule ensures the accounting equation always stays in balance.

Recording Transactions: Step-by-Step Process

Let's walk through how to actually record transactions using double entry bookkeeping. We'll follow a systematic five-step process.

Step 1: Identify the Transaction

What business event has occurred? Has money changed hands? Have goods been bought or sold? Has a service been provided?

Step 2: Identify Which Accounts Are Affected

Every transaction touches at least two accounts. Ask yourself:

- What did we receive?

- What did we give up?

- What type of account is each one? (Asset, liability, equity, income, expense?)

Step 3: Determine the Direction of Change

For each affected account, did it increase or decrease?

Step 4: Apply Debit and Credit Rules

Using the table above, determine whether each change should be recorded as a debit or credit.

Step 5: Record the Journal Entry

Write the entry in the journal (the book of first entry) with debits listed first and credits indented below. Ensure total debits equal total credits.

Detailed Example: Multiple Transactions

Let's follow James, who starts a consulting business called Bright Ideas Ltd.

Transaction 1: James invests £10,000 cash into the business.

- Identify: Owner contributes capital

- Accounts affected: Cash (asset) and Capital (equity)

- Direction: Cash increases, Capital increases

- Debit/Credit: Cash increases → Debit Cash. Capital increases → Credit Capital

- Journal entry:

Debit: Cash £10,000

Credit: Capital £10,000

(Being capital introduced by owner)

Transaction 2: The business buys office furniture for £2,500 cash.

- Identify: Purchase of asset for cash

- Accounts affected: Furniture (asset) and Cash (asset)

- Direction: Furniture increases, Cash decreases

- Debit/Credit: Furniture increases → Debit Furniture. Cash decreases → Credit Cash

- Journal entry:

Debit: Furniture £2,500

Credit: Cash £2,500

(Being purchase of office furniture)

Transaction 3: The business provides consulting services for £3,000 cash.

- Identify: Revenue earned and received

- Accounts affected: Cash (asset) and Consulting Income (income)

- Direction: Cash increases, Income increases

- Debit/Credit: Cash increases → Debit Cash. Income increases → Credit Income

- Journal entry:

Debit: Cash £3,000

Credit: Consulting Income £3,000

(Being income from consulting services)

Transaction 4: The business pays £800 for advertising expenses.

- Identify: Expense incurred and paid

- Accounts affected: Advertising Expense (expense) and Cash (asset)

- Direction: Expense increases, Cash decreases

- Debit/Credit: Expense increases → Debit Advertising Expense. Cash decreases → Credit Cash

- Journal entry:

Debit: Advertising Expense £800

Credit: Cash £800

(Being advertising costs paid)

Transaction 5: The business purchases £1,500 of supplies on credit from a supplier.

- Identify: Purchase on credit (not immediate payment)

- Accounts affected: Supplies (asset) and Accounts Payable (liability)

- Direction: Supplies increases, Accounts Payable increases

- Debit/Credit: Supplies increases → Debit Supplies. Accounts Payable increases → Credit Accounts Payable

- Journal entry:

Debit: Supplies £1,500

Credit: Accounts Payable £1,500

(Being supplies purchased on credit)

Transaction 6: The business takes a £5,000 bank loan.

- Identify: Borrowing from bank

- Accounts affected: Cash (asset) and Bank Loan (liability)

- Direction: Cash increases, Bank Loan increases

- Debit/Credit: Cash increases → Debit Cash. Bank Loan increases → Credit Bank Loan

- Journal entry:

Debit: Cash £5,000

Credit: Bank Loan £5,000

(Being loan received from bank)

Transaction 7: The business pays £600 toward the accounts payable.

- Identify: Payment of liability

- Accounts affected: Accounts Payable (liability) and Cash (asset)

- Direction: Accounts Payable decreases, Cash decreases

- Debit/Credit: Accounts Payable decreases → Debit Accounts Payable. Cash decreases → Credit Cash

- Journal entry:

Debit: Accounts Payable £600

Credit: Cash £600

(Being partial payment to supplier)

T-Accounts: Visualizing the Flow

A T-account is a visual representation of an individual account, shaped like the letter T. The account name sits on top, debits go on the left side, and credits go on the right side.

Let's create T-accounts for the Cash account from James's business above:

Cash ------------------------------- Debit | Credit ------------------------------- £10,000 (1) | £2,500 (2) £3,000 (3) | £800 (4) £5,000 (6) | £600 (7) ------------------------------- £18,000 | £3,900 ------------------------------- Balance: £14,100 (Debit)

The numbers in parentheses refer to the transaction numbers. We add up each side, and the difference gives us the balance. Since Cash is an asset with a normal debit balance, a debit balance of £14,100 means the business has £14,100 in cash.

Let's also look at the Capital account:

Capital ------------------------------- Debit | Credit ------------------------------- | £10,000 (1) ------------------------------- | £10,000 ------------------------------- Balance: £10,000 (Credit)

Capital has a normal credit balance. A credit balance of £10,000 represents the owner's initial investment.

The Trial Balance: Checking Your Work

After recording all transactions and posting them to individual accounts, you prepare a trial balance. This is simply a list of all accounts and their balances at a specific date, separated into debit and credit columns.

The trial balance serves two purposes:

- Error detection: If total debits don't equal total credits, you know there's a mistake somewhere

- Preparation for financial statements: It provides a convenient summary of all account balances

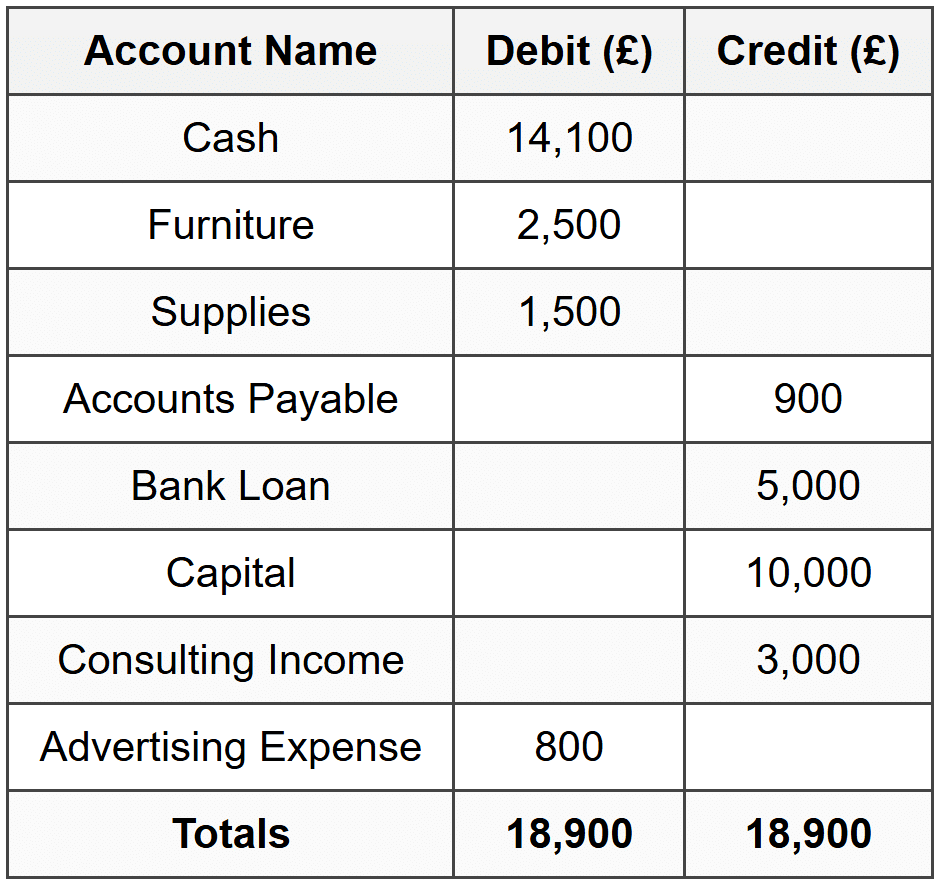

Here's the trial balance for Bright Ideas Ltd after the seven transactions:

Notice that the totals match: £18,900 on each side. This confirms that our debits equal our credits, suggesting the accounting equation is in balance.

Does a Balanced Trial Balance Guarantee No Errors?

Unfortunately, no. A trial balance only confirms that debits equal credits-it won't catch certain errors:

- Errors of omission - forgetting to record a transaction entirely

- Errors of commission - recording the correct amount in the wrong account (e.g., debiting Rent Expense instead of Insurance Expense)

- Errors of principle - recording a transaction that violates accounting principles (e.g., treating an asset purchase as an expense)

- Compensating errors - two errors that cancel each other out

- Errors of original entry - recording the wrong amount in both debit and credit

Still, a balanced trial balance is an excellent first checkpoint.

Real-World Example: How Tesco Uses Double Entry

Tesco, one of the world's largest retailers, uses double entry bookkeeping to track billions of transactions annually. Let's consider a simplified scenario:

Tesco purchases £50 million of groceries from suppliers on 30-day credit terms. The double entry would be:

Debit: Inventory £50,000,000

Credit: Accounts Payable £50,000,000

This increases Tesco's inventory (an asset-goods they'll sell) and increases accounts payable (a liability-money owed to suppliers).

When customers buy £70 million of groceries for cash, Tesco records:

Debit: Cash £70,000,000

Credit: Sales Revenue £70,000,000

This increases cash (an asset) and recognizes revenue (increasing equity through income).

Tesco also needs to account for the cost of the inventory sold. If those groceries cost Tesco £50 million, they record:

Debit: Cost of Sales £50,000,000

Credit: Inventory £50,000,000

This increases an expense (reducing equity) and decreases inventory (the asset has been sold).

When Tesco pays its suppliers:

Debit: Accounts Payable £50,000,000

Credit: Cash £50,000,000

The liability decreases (debit) and cash decreases (credit).

Through this chain of double entries, Tesco maintains a precise, balanced record of its financial position. Every transaction is captured from both perspectives, creating an audit trail and ensuring accuracy.

The Books of Account: From Journal to Ledger

In a complete accounting system, transactions flow through several books:

The Journal (Book of First Entry)

The journal is where transactions are first recorded in chronological order. Each entry shows:

- Date of the transaction

- Accounts affected

- Debit and credit amounts

- A brief description (called a narration)

For large businesses, there might be specialized journals for common transactions:

- Sales journal - for credit sales only

- Purchases journal - for credit purchases

- Cash receipts journal - for all cash received

- Cash payments journal - for all cash paid out

- General journal - for everything else (adjustments, corrections, unusual items)

The Ledger (Book of Final Entry)

The ledger contains individual accounts (like the T-accounts we saw earlier). Information from the journal is posted (transferred) to the relevant ledger accounts.

The ledger organizes information by account rather than by date, making it easy to see the complete history and current balance of any account.

Large businesses subdivide the ledger:

- General ledger - contains all the main accounts (cash, capital, sales, expenses, etc.)

- Subsidiary ledgers - contain detailed records supporting general ledger control accounts (e.g., individual customer accounts that feed into the total Accounts Receivable figure)

Different Types of Accounts in Detail

Let's explore the main categories of accounts more deeply.

Personal Accounts

Personal accounts record transactions with people or organizations. These include:

- Customer accounts (people who owe you money)

- Supplier accounts (people you owe money to)

- Owner's capital account

The traditional rule for personal accounts is: Debit the receiver, credit the giver.

If a customer buys goods on credit, they're receiving goods, so you debit their account. When they pay you back, you're receiving cash, so you debit Cash and credit the customer's account (they've given you cash).

Real Accounts

Real accounts relate to assets and liabilities-things that have a continuing existence. Examples include:

- Land and buildings

- Machinery

- Inventory

- Bank loans

These accounts are permanent-their balances carry forward from one accounting period to the next.

The traditional rule for real accounts: Debit what comes in, credit what goes out.

Nominal Accounts

Nominal accounts relate to income and expenses-items connected to running the business. Examples include:

- Sales revenue

- Rent expense

- Salaries expense

- Interest income

These accounts are temporary-they're reset to zero at the start of each accounting period (usually a year). Their balances are transferred to the equity section via the profit or loss calculation.

The traditional rule for nominal accounts: Debit all expenses and losses, credit all income and gains.

Balancing Accounts at Period End

At the end of an accounting period, each account in the ledger must be balanced-meaning we calculate the closing balance to carry forward to the next period.

Balancing Process

Let's balance the Cash account we looked at earlier:

Cash Account ------------------------------------------- Date Detail £ | Date Detail £ ------------------------------------------- Jan 1 Capital 10,000 | Jan 5 Furniture 2,500 Jan 10 Income 3,000 | Jan 15 Advertising 800 Jan 20 Loan 5,000 | Jan 28 Payable 600 ----------- | ----------- Total 18,000 | Total 3,900 ----------- | Jan 31 Balance c/d 14,100 | ----------- Total 18,000 | Total 18,000 ═══════════ | ═══════════ Feb 1 Balance b/d 14,100|

The steps are:

- Total both the debit and credit sides

- Insert a balancing figure on the smaller side, labeled Balance c/d (carried down)

- Draw totals that match on both sides

- Bring down the balance on the opposite side, labeled Balance b/d (brought down), dated the first day of the next period

This creates a clear closing balance (£14,100) that becomes the opening balance for the next period.

The Expanded Accounting Equation and Profit

Remember that income and expenses ultimately affect equity. When a business earns income, equity increases. When it incurs expenses, equity decreases.

We can expand the accounting equation to explicitly show this relationship:

\[ \text{Assets} = \text{Liabilities} + \text{Capital} + \text{Income} - \text{Expenses} - \text{Drawings} \]Drawings (also called withdrawals) represent amounts taken out of the business by the owner for personal use. These reduce equity but aren't expenses-they're distributions of profit.

Profit is calculated as:

\[ \text{Profit} = \text{Income} - \text{Expenses} \]Profit increases equity. Loss (when expenses exceed income) decreases equity.

At the end of each period, income and expense accounts are closed (zeroed out), and their net effect (profit or loss) is transferred to equity. This is called the closing process.

Example: Calculating Profit and Its Effect on Equity

Let's return to Bright Ideas Ltd. From the trial balance, we had:

- Consulting Income: £3,000 (credit)

- Advertising Expense: £800 (debit)

Profit calculation:

\[ \text{Profit} = £3,000 - £800 = £2,200 \]This £2,200 profit is added to James's capital. His total equity becomes:

\[ \text{Total Equity} = £10,000 \text{ (original capital)} + £2,200 \text{ (profit)} = £12,200 \]If James had withdrawn £500 for personal expenses (drawings), equity would be:

\[ \text{Total Equity} = £10,000 + £2,200 - £500 = £11,700 \]Practical Application: Common Business Transactions

Let's look at a variety of common transactions and their double entries.

Transaction: Cash Sales

The business sells goods for £500 cash.

Debit: Cash £500

Credit: Sales £500

Transaction: Credit Sales

The business sells goods for £500 on credit to Customer A.

Debit: Accounts Receivable-Customer A £500

Credit: Sales £500

Later, when Customer A pays:

Debit: Cash £500

Credit: Accounts Receivable-Customer A £500

Transaction: Cash Purchases

The business buys inventory for £300 cash.

Debit: Purchases £300

Credit: Cash £300

Transaction: Credit Purchases

The business buys inventory for £300 on credit from Supplier B.

Debit: Purchases £300

Credit: Accounts Payable-Supplier B £300

When paying Supplier B:

Debit: Accounts Payable-Supplier B £300

Credit: Cash £300

Transaction: Paying Wages

The business pays £1,200 in employee wages.

Debit: Wages Expense £1,200

Credit: Cash £1,200

Transaction: Receiving Interest

The business receives £50 interest on its bank savings account.

Debit: Cash £50

Credit: Interest Income £50

Transaction: Paying Insurance Premium

The business pays £600 for annual insurance.

Debit: Insurance Expense £600

Credit: Cash £600

Note: If the insurance covers future periods, it might be recorded as a prepaid expense (an asset), then gradually expensed over time. For now, we're keeping it simple.

Transaction: Owner Introduces Additional Capital

The owner contributes an additional £2,000 to the business.

Debit: Cash £2,000

Credit: Capital £2,000

Transaction: Owner Withdraws Cash (Drawings)

The owner takes £400 for personal use.

Debit: Drawings £400

Credit: Cash £400

Drawings reduce equity but are kept in a separate account from expenses because they're not business costs.

Transaction: Returning Goods to Supplier

The business returns £150 of faulty goods previously purchased on credit from Supplier C.

Debit: Accounts Payable-Supplier C £150

Credit: Purchases Returns £150

This reduces the liability (you owe less) and reduces the net purchases.

Transaction: Customer Returns Goods

Customer D returns £100 of goods previously sold on credit.

Debit: Sales Returns £100

Credit: Accounts Receivable-Customer D £100

This reduces the amount the customer owes and reduces net sales.

Understanding Contra Accounts

A contra account is an account that offsets another account. For example:

- Sales Returns is a contra account to Sales. Instead of directly reducing Sales, we track returns separately for better information

- Purchases Returns is a contra account to Purchases

- Accumulated Depreciation is a contra account to fixed assets (we'll encounter this in later studies)

Contra accounts help maintain detail while still showing the net effect.

Why Double Entry Works: The Built-In Self-Checking Mechanism

Double entry bookkeeping is remarkably resilient. Because every transaction affects at least two accounts equally, and because debits must always equal credits, the system has a built-in error-detection mechanism.

If you make a single-sided entry (forget either the debit or credit), the trial balance won't balance. If you record different amounts for the debit and credit, the trial balance won't balance.

This is why double entry has survived over 500 years-it provides both detailed information and mathematical certainty. Luca Pacioli, the Franciscan monk who documented this system in 1494, created something so elegant that even modern computerized accounting systems follow the exact same principles.

Companies like Shell, which operates in over 70 countries, process millions of transactions every day. Without the discipline of double entry, tracking the flow of resources, profits, and obligations would be virtually impossible.

From Double Entry to Financial Statements

The ultimate purpose of double entry bookkeeping is to produce financial statements-the documents that summarize a business's financial performance and position.

The three main financial statements are:

- Statement of Profit or Loss (Income Statement): Shows income and expenses for a period, calculating profit or loss

- Statement of Financial Position (Balance Sheet): Shows assets, liabilities, and equity at a specific point in time

- Statement of Cash Flows: Shows cash inflows and outflows during a period

The trial balance feeds directly into these statements:

- Income and expense balances go into the Statement of Profit or Loss

- Asset, liability, and equity balances go into the Statement of Financial Position

Double entry ensures that all the information for these statements is accurate, complete, and interconnected.

Key Terms Recap

- Accounting Equation - Assets = Liabilities + Equity; the fundamental relationship describing a business's financial position

- Assets - Resources owned or controlled by the business that provide future economic benefits

- Liabilities - Obligations owed to external parties

- Equity - The owners' residual claim on assets after liabilities are deducted; also called capital or owners' equity

- Double Entry Bookkeeping - A system where every transaction affects at least two accounts, with equal debits and credits

- Debit - An entry on the left side of an account; increases assets and expenses, decreases liabilities, equity, and income

- Credit - An entry on the right side of an account; increases liabilities, equity, and income, decreases assets and expenses

- Income - Revenue earned by the business, increasing equity

- Expenses - Costs incurred in running the business, decreasing equity

- Drawings - Amounts withdrawn by the owner for personal use, reducing equity but not considered expenses

- T-Account - A visual representation of an account showing debits on the left and credits on the right

- Journal - The book of first entry where transactions are recorded chronologically with debits and credits

- Ledger - The book of final entry containing individual accounts organized by account name

- Posting - Transferring entries from the journal to the ledger

- Trial Balance - A list of all ledger account balances at a point in time, separated into debit and credit columns, used to check that total debits equal total credits

- Personal Accounts - Accounts for individuals or organizations (customers, suppliers, owners)

- Real Accounts - Permanent accounts for assets and liabilities

- Nominal Accounts - Temporary accounts for income and expenses, reset each period

- Balance c/d - Balance carried down; the closing balance of an account

- Balance b/d - Balance brought down; the opening balance of an account in the next period

- Contra Account - An account that offsets another account (e.g., Sales Returns offsets Sales)

- Accounts Receivable - Money owed to the business by customers; an asset

- Accounts Payable - Money owed by the business to suppliers; a liability

- Profit - Income minus Expenses; increases equity

- Loss - When expenses exceed income; decreases equity

Common Mistakes and Misconceptions

- Mistake: Thinking "debit" always means decrease and "credit" always means increase.

Reality: The effect depends on the account type. Debits increase assets and expenses but decrease liabilities, equity, and income. Credits do the opposite. - Mistake: Recording only one side of a transaction.

Reality: Every transaction must have at least one debit and one credit. Single-entry recording is incomplete and will cause the trial balance to fail. - Mistake: Believing that a balanced trial balance proves there are no errors.

Reality: A balanced trial balance only confirms debits equal credits. It won't detect omitted transactions, entries in wrong accounts, or conceptual errors. - Mistake: Confusing drawings with expenses.

Reality: Drawings are not business expenses-they're personal withdrawals by the owner. They reduce equity directly and are not included in the profit calculation. - Mistake: Thinking assets must equal equity.

Reality: Assets equal liabilities plus equity. Equity is only one source of funding for assets; the other source is borrowed money (liabilities). - Mistake: Recording revenue when cash is received rather than when it's earned.

Reality: Under the accrual basis of accounting (which is standard), revenue is recognized when earned, regardless of when cash is received. The same applies to expenses-they're recognized when incurred, not necessarily when paid. - Mistake: Posting to the wrong side of a T-account.

Reality: Always refer back to the rules: assets and expenses increase on the debit (left) side; liabilities, equity, and income increase on the credit (right) side. - Mistake: Forgetting to balance accounts at period end.

Reality: Accounts must be formally balanced to determine closing balances that carry forward. Simply adding up both sides isn't sufficient-you must show the balance carried down and brought down. - Mistake: Treating all purchases as expenses immediately.

Reality: If you purchase inventory (goods for resale), it's an asset until sold. If you purchase supplies or services consumed immediately, those are expenses. The nature of what you buy determines the account. - Mistake: Using everyday banking terminology for accounting terms.

Reality: When your bank statement shows a "credit," it means the bank owes you money (from their perspective, you're a liability). In your business books, that same transaction is a debit to your Cash account (an asset increase). Always think from your business's perspective, not the bank's.

Summary

- The accounting equation (Assets = Liabilities + Equity) is the foundation of all accounting, describing the financial position of any entity at any time. Every transaction affects this equation, but it must always remain in balance.

- Double entry bookkeeping requires that every transaction affects at least two accounts with equal debits and credits. This dual recording reflects the dual aspect of every business event-something received and something given up.

- Debits and credits are simply left-side and right-side entries. Assets and expenses increase with debits; liabilities, equity, and income increase with credits. The rules ensure the accounting equation stays balanced.

- The journal is where transactions are first recorded chronologically, and the ledger contains individual accounts organized by name. Information flows from journal to ledger through the posting process.

- A trial balance lists all account balances at a point in time and checks that total debits equal total credits. While it detects many errors, it won't catch all types of mistakes.

- Personal accounts relate to people/organizations, real accounts relate to assets and liabilities (permanent accounts), and nominal accounts relate to income and expenses (temporary accounts reset each period).

- Profit equals income minus expenses and increases equity. Drawings are owner withdrawals that reduce equity but aren't expenses.

- Double entry bookkeeping provides a self-checking mechanism and detailed information trail, enabling the preparation of accurate financial statements that show performance and position.

- The system has remained fundamentally unchanged for over 500 years because it elegantly captures the dual nature of transactions, maintains mathematical balance, and provides comprehensive information for decision-making.

- Understanding double entry is not just about following rules-it's about understanding the logic of how resources flow through a business, creating a complete, balanced picture of financial reality.

Practice Questions

Question 1: Recall

State the accounting equation and explain what each component represents.

Question 2: Application

A business has the following assets and liabilities:

Cash: £8,000

Inventory: £12,000

Equipment: £25,000

Accounts Payable: £5,000

Bank Loan: £15,000

Calculate the owner's equity.

Question 3: Application

Record the following transactions in journal entry format (show debits and credits):

- Owner invests £20,000 cash into the business

- Business purchases a vehicle for £8,000 cash

- Business sells goods for £3,500 on credit to Customer X

- Business pays £1,200 for rent expense

- Customer X pays £3,500 owed

Question 4: Analytical

A trial balance shows total debits of £156,000 and total credits of £157,500. What does this indicate? List three possible errors that could cause this imbalance.

Question 5: Application

Complete the following T-account for the Accounts Payable account and determine the closing balance:

Transactions:

1. Purchased goods on credit from Supplier A: £4,000

2. Purchased goods on credit from Supplier B: £2,500

3. Paid Supplier A: £2,000

4. Returned faulty goods to Supplier B: £300

Question 6: Analytical

Explain why drawings are not treated as expenses and describe the correct accounting treatment for owner withdrawals.

Question 7: Application

A business starts the year with £30,000 equity. During the year, it earns £50,000 in sales revenue and incurs £35,000 in expenses. The owner withdraws £8,000 for personal use and introduces additional capital of £5,000. Calculate the closing equity.

Question 8: Analytical

Why does a balanced trial balance not guarantee that all transactions have been recorded correctly? Give examples of errors that would not prevent the trial balance from balancing.