Sales, Purchases, and Cash Transactions

What Are Sales, Purchases, and Cash Transactions?

Imagine you run a small bakery. Every day, you sell bread to customers, buy flour from suppliers, and handle cash coming in and going out. These activities are the lifeblood of your business, and in the world of accounting, we call them sales, purchases, and cash transactions. Understanding how to record these properly is absolutely fundamental to keeping accurate financial records.

Here's something surprising: every single business transaction, whether it's Apple selling an iPhone or your local corner shop selling a chocolate bar, follows the same basic recording principles you're about to learn. The amounts might differ wildly, but the method stays consistent.

Let's break this down from absolute scratch. A transaction is simply an exchange of value between a business and another party. When you record these transactions, you're creating a permanent, systematic record that tells the story of what happened to the business's money and resources.

The Three Main Types of Transactions

- Sales transactions - when your business sells goods or services to customers (money or promises of money coming IN)

- Purchases transactions - when your business buys goods or services from suppliers (money or promises of money going OUT)

- Cash transactions - when actual money (or bank transfers) changes hands immediately, regardless of whether it's a sale or purchase

Notice something important: sales and purchases can happen with or without immediate cash exchange. This is where things get interesting and where many beginners get confused.

Sales Transactions: Recording Revenue

When your business sells something, you need to record it properly. But there are two fundamentally different types of sales that require different recording approaches.

Cash Sales vs Credit Sales

A cash sale happens when the customer pays immediately. This doesn't necessarily mean physical banknotes and coins - it includes card payments, bank transfers, and digital payments like PayPal. The key feature is: you get the money right away.

A credit sale (also called a sale "on account") happens when you let the customer take the goods or services now but pay later. You've made the sale, but you haven't received the cash yet. Instead, the customer becomes your debtor or receivable - someone who owes you money.

Real-world example: When you buy groceries at Tesco and pay with your debit card at the checkout, that's a cash sale for Tesco (they receive the money immediately through the electronic payment system). But when Tesco supplies products to a restaurant and invoices them with "payment due in 30 days," that's a credit sale - Tesco has made the sale but won't receive cash for a month.

Recording a Cash Sale

Let's say your bakery sells bread for £50 cash on 5th January. Here's what you need to record:

- The business has more cash (an asset increases by £50)

- The business has earned sales revenue (income increases by £50)

In accounting terms, we record this using the double-entry principle. Every transaction affects at least two accounts. For this cash sale:

Debit: Cash £50

Credit: Sales £50

Think of it this way: "debit" means the left side of an account, and "credit" means the right side. For assets like cash, a debit means an increase. For income like sales, a credit means an increase. Don't worry if this feels backwards at first - everyone finds it strange initially!

Recording a Credit Sale

Now imagine your bakery supplies £200 worth of bread to a local café on 8th January, and the café will pay in 30 days. Here's what changes:

- The business has more receivables (an asset increases by £200 - someone owes you money)

- The business has earned sales revenue (income increases by £200)

The recording looks like this:

Debit: Receivables (or Debtors) £200

Credit: Sales £200

Notice something crucial: you record the sale when it happens, not when you receive the cash. This is called the accruals principle or revenue recognition principle - a foundational concept in accounting.

What Happens When the Customer Pays Later?

When the café pays you the £200 on 7th February, that's a separate transaction:

Debit: Cash £200

Credit: Receivables £200

Notice that sales aren't involved in this second entry. Why? Because you already recorded the sale back on 8th January. Now you're just converting one asset (receivables) into another asset (cash). The total value of your assets stays the same - you're just changing the form.

Sales Returns and Allowances

Sometimes customers return goods or you give them a discount because something wasn't quite right. Suppose a customer returns £30 worth of bread because it was stale. You need to reverse part of the original sale:

Debit: Sales Returns £30

Credit: Receivables (or Cash) £30

The Sales Returns account (sometimes called Returns Inwards) is a contra-revenue account - it reduces your total sales figure. At the end of the accounting period, you subtract sales returns from gross sales to get net sales.

The formula looks like this:

\[ \text{Net Sales} = \text{Gross Sales} - \text{Sales Returns} - \text{Sales Allowances} \]Purchases Transactions: Recording Costs

Just as your business makes sales, it also buys things it needs to operate. These are purchases. In accounting, we typically use "purchases" specifically to mean goods bought for resale (inventory) or raw materials used to make products.

Cash Purchases vs Credit Purchases

The same logic that applies to sales applies here, but in reverse.

A cash purchase means you pay the supplier immediately when you receive the goods or services.

A credit purchase means you take the goods now but pay the supplier later. The supplier becomes your creditor or payable - someone you owe money to.

Real-world example: When Amazon buys products from manufacturers in China, they typically don't pay immediately. They might have payment terms of 60 or 90 days, meaning they receive the inventory now but pay later. These are credit purchases. Amazon's suppliers become creditors in Amazon's accounting records.

Recording a Cash Purchase

Your bakery buys £100 worth of flour, paying cash immediately on 10th January:

Debit: Purchases £100

Credit: Cash £100

Here's what's happening:

- The business has more inventory/purchases (an expense or asset increases by £100)

- The business has less cash (an asset decreases by £100)

For expenses and costs like purchases, a debit means an increase. For assets like cash, a credit means a decrease.

Recording a Credit Purchase

On 12th January, your bakery orders £300 worth of sugar from a supplier with 30-day payment terms:

Debit: Purchases £300

Credit: Payables (or Creditors) £300

You've acquired the goods (purchases increase), and you've created an obligation to pay (payables increase - which is a liability).

What Happens When You Pay the Supplier Later?

On 11th February, you pay the supplier the £300:

Debit: Payables £300

Credit: Cash £300

You're reducing what you owe (payables decrease with a debit) and reducing your cash (cash decreases with a credit).

Purchase Returns and Allowances

Sometimes you return goods to suppliers - maybe the flour you ordered was contaminated. If you return £40 worth of flour:

Debit: Payables (or Cash) £40

Credit: Purchase Returns £40

The Purchase Returns account (sometimes called Returns Outwards) reduces your total purchases. The formula is:

\[ \text{Net Purchases} = \text{Gross Purchases} - \text{Purchase Returns} - \text{Purchase Allowances} \]Cash Transactions: The Movement of Money

Cash transactions deserve special attention because cash is the most liquid asset - it's what keeps your business alive day-to-day. In accounting, "cash" includes actual currency, coins, checks received, and money in bank accounts.

Cash Receipts

Cash receipts are all the ways money comes INTO your business. These include:

- Cash sales to customers

- Payments received from credit customers (receivables collected)

- Loans received from banks

- Capital invested by owners

- Interest received on savings

- Sale of fixed assets for cash

Let's look at a few examples:

Example 1: You receive £500 cash from a customer who bought goods on credit last month:

Debit: Cash £500

Credit: Receivables £500

Example 2: The business owner invests an additional £2,000 of personal money into the business:

Debit: Cash £2,000

Credit: Capital £2,000

Capital represents the owner's investment in the business.

Cash Payments

Cash payments are all the ways money goes OUT of your business:

- Cash purchases from suppliers

- Payments to credit suppliers (payables settled)

- Payments for expenses (rent, utilities, salaries)

- Loan repayments to banks

- Owner withdrawals (drawings)

- Purchase of fixed assets for cash

Example 1: You pay £800 to a supplier you owed money to:

Debit: Payables £800

Credit: Cash £800

Example 2: You pay £300 rent for your bakery premises:

Debit: Rent Expense £300

Credit: Cash £300

Example 3: The owner withdraws £150 cash for personal use:

Debit: Drawings £150

Credit: Cash £150

Drawings (sometimes called withdrawals) represent money the owner takes out of the business for personal use. It's not an expense - it reduces the owner's equity in the business.

Petty Cash System

Most businesses maintain a petty cash fund - a small amount of physical cash kept on premises for minor expenses like coffee, postage stamps, or emergency supplies.

Here's how it typically works:

- You establish the fund with a fixed amount (say £100)

- As small expenses occur, you pay from petty cash and keep receipts

- When the cash runs low, you "top up" the fund back to £100

This is called the imprest system. Let's see it in action:

Step 1 - Establishing the fund:

Debit: Petty Cash £100

Credit: Cash £100

Step 2 - During the month: You spend £60 from petty cash on various small items (stationery £25, coffee £20, postage £15). You don't record each tiny transaction immediately - you just keep the receipts.

Step 3 - Replenishing the fund: At month-end, you count the petty cash and find £40 remaining. You had £100, spent £60, so you restore it to £100 by adding £60:

Debit: Stationery Expense £25

Debit: Refreshments Expense £20

Debit: Postage Expense £15

Credit: Cash £60

Notice that petty cash itself doesn't change - it stays at £100. You only record the actual expenses and the cash used to replenish the fund.

Trade Discounts vs Cash Discounts

Businesses often offer discounts, but there are two completely different types that beginners frequently mix up.

Trade Discounts

A trade discount is a reduction in the list price offered to certain customers, usually based on their type (wholesalers, regular customers, bulk buyers). It's deducted BEFORE you record the transaction.

Example: A supplier's catalog shows flour at £100 per bag, but they give you a 20% trade discount because you're a regular customer. You actually buy at £80 per bag.

You simply record the purchase at the net amount:

Debit: Purchases £80

Credit: Payables £80

The £20 discount is never shown in your accounting records. The transaction happened at £80, period.

Cash Discounts (Settlement Discounts)

A cash discount or settlement discount is a reduction offered for paying quickly - typically within 7 or 10 days instead of the usual 30 days. This IS recorded in the accounts.

Common terms look like "2/10, n/30" which means:

- Take a 2% discount if you pay within 10 days

- Otherwise, pay the net (full) amount within 30 days

Example: You buy £1,000 of goods on credit with terms 2/10, n/30.

Initial purchase on 1st March:

Debit: Purchases £1,000

Credit: Payables £1,000

If you pay on 8th March (within 10 days):

Discount = £1,000 × 2% = £20

Amount paid = £1,000 - £20 = £980

Debit: Payables £1,000

Credit: Cash £980

Credit: Discount Received £20

Discount Received is income for your business - you've saved money by paying early.

If you pay on 25th March (after 10 days):

Debit: Payables £1,000

Credit: Cash £1,000

No discount - you pay the full amount.

Offering Discounts to Your Customers

When you're the seller offering early payment discounts, the account name changes to Discount Allowed, which is an expense for your business.

Example: You sell £500 of goods on credit with terms 3/10, n/30. The customer pays within 10 days.

Initial sale on 5th April:

Debit: Receivables £500

Credit: Sales £500

Payment received on 12th April:

Discount = £500 × 3% = £15

Cash received = £500 - £15 = £485

Debit: Cash £485

Debit: Discount Allowed £15

Credit: Receivables £500

Sales Tax (VAT) Considerations

In many countries, businesses must charge Value Added Tax (VAT) or similar sales taxes. This adds another layer to recording transactions.

Let's say VAT is 20% and you make a sale of goods worth £100. The customer actually pays £120 (£100 + £20 VAT). Here's the crucial point: the £20 VAT isn't your money - you're just collecting it on behalf of the government.

Recording a sale with VAT:

Debit: Cash (or Receivables) £120

Credit: Sales £100

Credit: VAT Payable £20

You've increased cash by the full amount paid (£120), recorded sales revenue at the net amount (£100), and created a liability to pay VAT to the government (£20).

Recording a purchase with VAT:

You buy goods for £200 plus 20% VAT = £240 total.

Debit: Purchases £200

Debit: VAT Recoverable £40

Credit: Cash (or Payables) £240

You've recorded the purchase at the net amount (£200), created an asset for VAT you can claim back (£40), and decreased cash by the full amount paid (£240).

Periodically (monthly or quarterly), you calculate:

\[ \text{VAT to pay} = \text{VAT collected from customers} - \text{VAT paid to suppliers} \]If VAT Payable is £500 and VAT Recoverable is £300, you owe the government £200.

The Document Trail: Source Documents

In the real world, you don't just randomly record transactions. Each entry must be supported by evidence - these are called source documents. They provide the proof that a transaction actually occurred.

Sales-Related Documents

- Sales Invoice - You send this to the customer when you make a credit sale. It shows what was sold, the quantity, price, VAT, and payment terms. This is THE source document for recording a sale.

- Cash Register Receipt - For cash sales, the till receipt or POS (point of sale) printout serves as evidence.

- Credit Note - You issue this when a customer returns goods or you grant an allowance. It reduces the amount the customer owes you. This supports recording sales returns.

- Delivery Note - Proves that goods were physically delivered to the customer.

Purchases-Related Documents

- Purchase Invoice - Received from your supplier when you buy on credit. This is THE source document for recording a purchase.

- Debit Note - You send this to a supplier when you return goods or dispute a charge. It reduces what you owe them.

- Goods Received Note (GRN) - Internal document confirming you actually received the goods ordered.

- Purchase Order - Your written order to the supplier (created before the goods arrive).

Cash-Related Documents

- Bank Statement - Shows all money in and out of your bank account.

- Receipt - Proof that you paid cash for something.

- Cheque Stub/Counterfoil - Your record of cheques you've written.

- Paying-in Slip - Proof of cash or cheques deposited into the bank.

Real-world insight: The 2001 Enron scandal, one of the biggest corporate frauds in history, involved creating fake transactions without proper source documents. This is why auditors always demand to see original invoices, bank statements, and other supporting evidence. No document = no proof = potential fraud.

Books of Prime Entry (Day Books)

Imagine trying to record every single transaction directly into your main accounts - it would be chaotic! Instead, businesses use books of prime entry (also called day books or journals) as an intermediate step.

Think of these as organized lists where you initially record transactions by type, before transferring the totals to your main accounting records (the ledger).

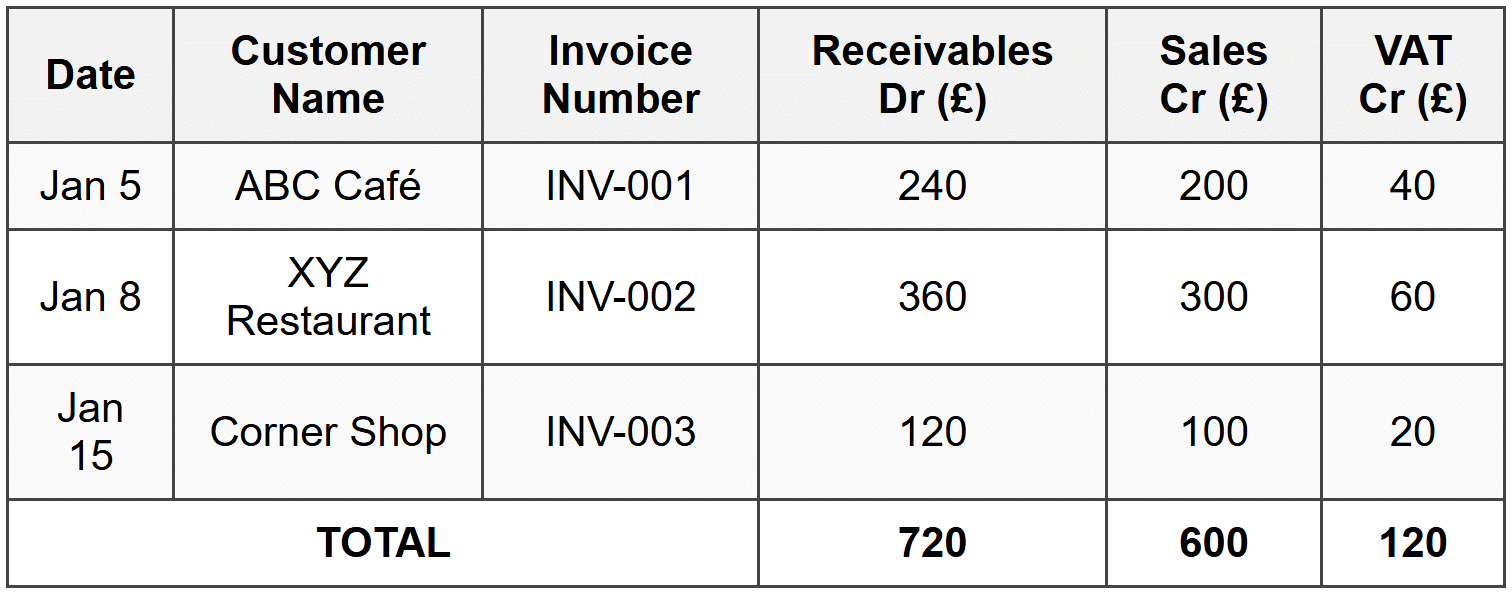

The Sales Day Book

The Sales Day Book (or Sales Journal) records all credit sales. Cash sales are NOT recorded here - they go straight into the cash book.

Here's what a typical sales day book looks like:

At the end of the period (week, month), you transfer these totals to the ledger with one combined entry:

Debit: Receivables £720

Credit: Sales £600

Credit: VAT Payable £120

This saves you from making three separate ledger entries. The sales day book has done the organizing work for you.

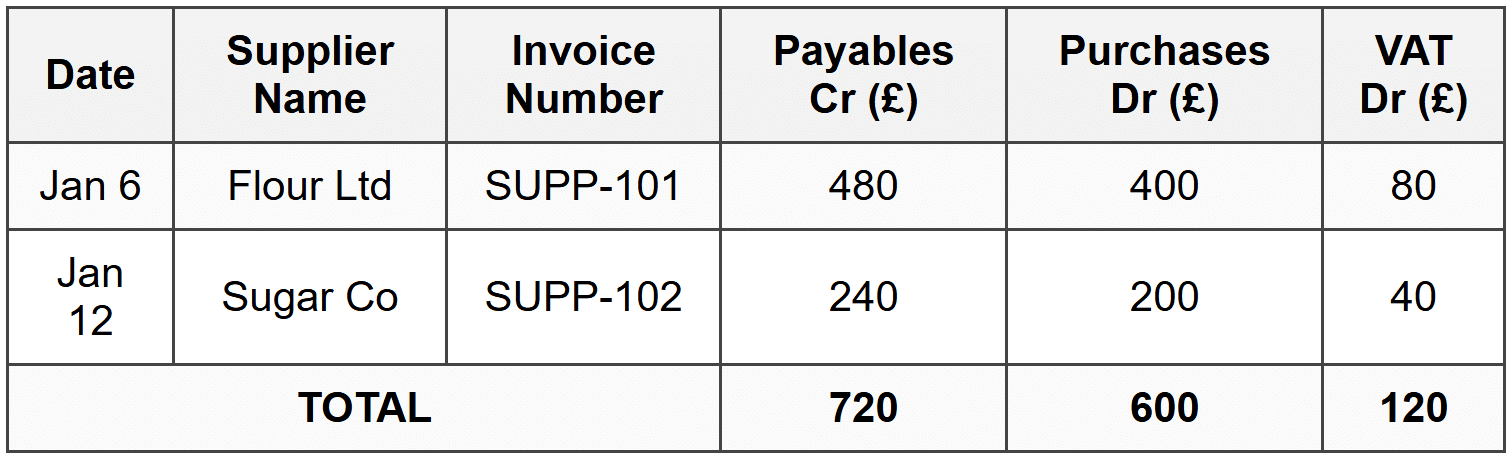

The Purchases Day Book

The Purchases Day Book (or Purchases Journal) records all credit purchases.

Monthly posting to ledger:

Debit: Purchases £600

Debit: VAT Recoverable £120

Credit: Payables £720

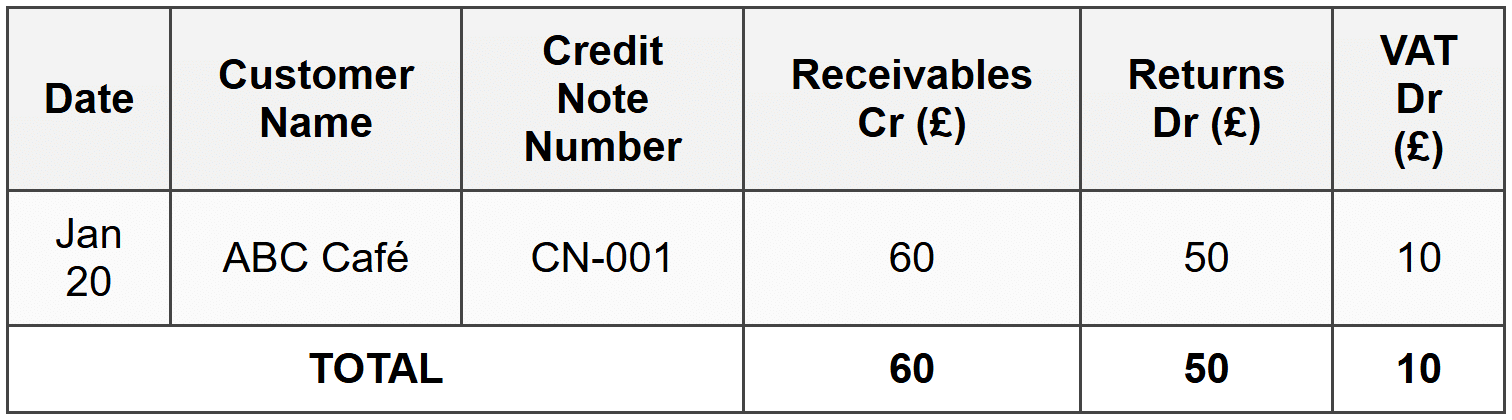

Sales Returns Day Book

Records all goods returned by customers (returns inwards).

Monthly posting:

Debit: Sales Returns £50

Debit: VAT Payable £10

Credit: Receivables £60

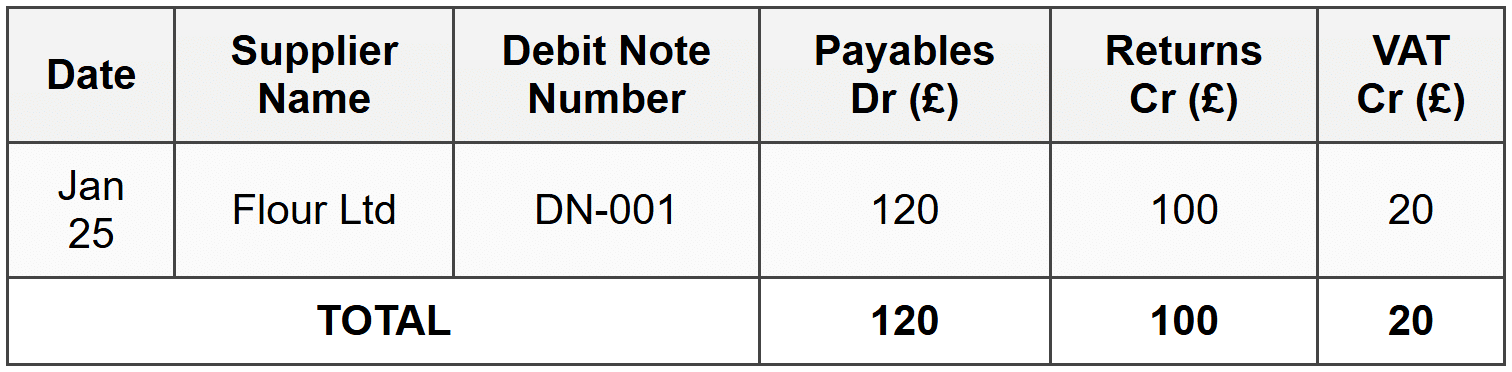

Purchases Returns Day Book

Records all goods you return to suppliers (returns outwards).

Monthly posting:

Debit: Payables £120

Credit: Purchase Returns £100

Credit: VAT Recoverable £20

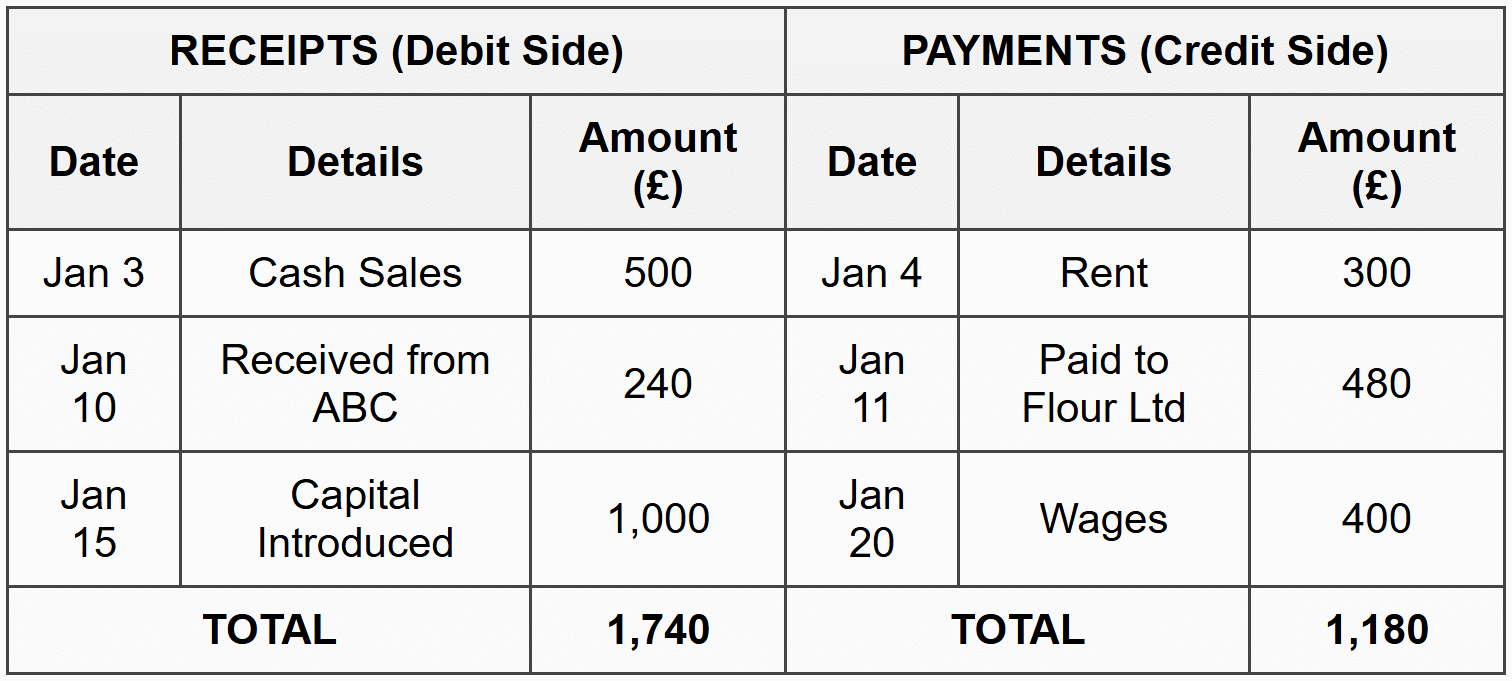

The Cash Book

The Cash Book is special - it's both a book of prime entry AND part of the ledger. It records all cash receipts and payments.

A basic cash book has two sides:

Balance = £1,740 - £1,180 = £560 (cash on hand)

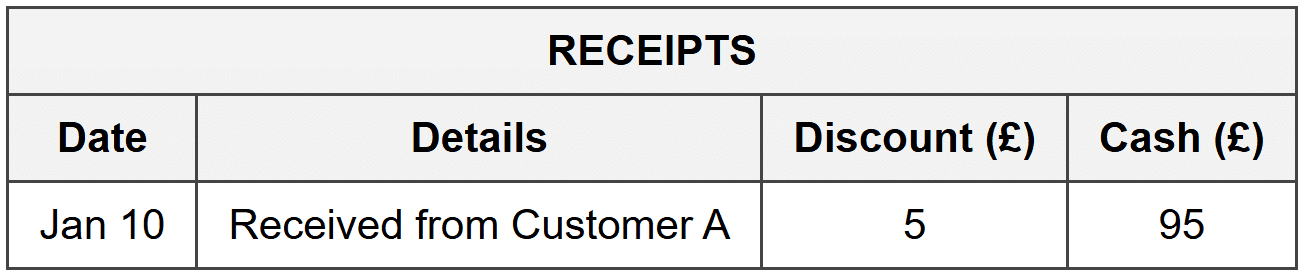

Many businesses use a three-column cash book that also tracks discounts:

This shows the customer owed £100, you allowed £5 discount, and received £95 cash.

Linking Everything Together: From Transaction to Financial Statements

Let's trace a complete journey to see how everything connects:

- Transaction occurs: You sell £1,000 of goods on credit to a customer

- Source document created: You issue invoice INV-123

- Book of prime entry: You record it in the Sales Day Book

- Ledger posting: At month-end, you post totals to the Sales Account and Receivables Account in the ledger

- Trial balance: These ledger balances appear in your trial balance

- Financial statements: Sales appears on the Income Statement, Receivables appears on the Balance Sheet

This systematic flow ensures nothing gets lost and everything can be traced back to original evidence.

Control Accounts: Keeping Track of Many Customers and Suppliers

As your business grows, you might have hundreds of customers and suppliers. Imagine having separate ledger accounts for each - it becomes unwieldy. The solution is control accounts.

The Receivables Control Account

Instead of checking every individual customer account, the Receivables Control Account (also called Sales Ledger Control Account) summarizes all customer balances in one place.

Here's what goes into it:

Increases (Debits):

- Credit sales (from Sales Day Book)

- Dishonored cheques from customers

- Interest charged on overdue accounts

Decreases (Credits):

- Cash received from customers

- Sales returns

- Discounts allowed

- Bad debts written off

The formula for the receivables control account:

\[ \text{Closing Balance} = \text{Opening Balance} + \text{Credit Sales} - \text{Cash Received} - \text{Returns} - \text{Discounts} - \text{Bad Debts} \]Example:

Opening balance of receivables: £5,000

Credit sales for the month: £12,000

Cash received from customers: £9,000

Sales returns: £500

Discounts allowed: £300

Bad debts written off: £200

This £7,000 should match the sum of all individual customer balances in your detailed records.

The Payables Control Account

The Payables Control Account (also called Purchases Ledger Control Account) does the same for suppliers.

Increases (Credits):

- Credit purchases (from Purchases Day Book)

Decreases (Debits):

- Cash paid to suppliers

- Purchase returns

- Discounts received

Example:

Opening balance of payables: £3,000

Credit purchases for the month: £8,000

Cash paid to suppliers: £7,000

Purchase returns: £400

Discounts received: £100

Bank Reconciliation: Making Sure Your Records Match Reality

Your cash book shows what you THINK is in your bank account. But the bank statement shows what the bank THINKS is in your account. These often don't match! This isn't necessarily an error - there are legitimate timing differences.

Common Differences Between Cash Book and Bank Statement

- Unpresented cheques - You wrote cheques that haven't been cashed yet, so they're in your cash book but not on the bank statement

- Outstanding deposits - You deposited money that hasn't cleared yet

- Bank charges - The bank deducted fees you didn't know about yet

- Direct debits - Automatic payments you forgot to record

- Standing orders - Regular automatic payments

- Interest earned - The bank added interest you didn't know about

- Errors - Mistakes in either your records or the bank's

Real-world example: You write a cheque for £500 to a supplier on January 28th and record it in your cash book immediately, reducing your balance to £2,000. But the supplier doesn't deposit the cheque until February 3rd. On January 31st, your cash book shows £2,000, but the bank statement shows £2,500. Neither is wrong - it's a timing difference.

Performing a Bank Reconciliation

Let's work through a complete example:

Your cash book balance on 31st January: £3,200

Bank statement balance on 31st January: £4,100

Additional information:

- Cheques written but not yet presented: £650

- Deposits made but not yet on statement: £400

- Bank charges on statement not in cash book: £50

- Direct debit payment not recorded: £200

- Customer payment via bank transfer not recorded: £600

Step 1: Update the cash book for items you didn't know about

Starting cash book balance: £3,200

Add: Customer payment: +£600

Less: Bank charges: -£50

Less: Direct debit: -£200

Revised cash book balance: £3,550

Step 2: Reconcile the revised cash book to the bank statement

Bank statement balance: £4,100

Add: Outstanding deposits: +£400

Less: Unpresented cheques: -£650

Less: Bank error (if any): £0

Adjusted bank balance: £3,850

Wait - these still don't match! This means there's likely an error somewhere. You'd need to investigate further. But if they DID match, the reconciliation would be complete.

Here's the proper format when they do match:

Bank Reconciliation Statement as at 31st January

Balance per bank statement: £3,850

Add: Outstanding deposits: £400

Total: £4,250

Less: Unpresented cheques: £650

Balance per cash book: £3,600

(This is a corrected example where figures would match)

Real-World Business Examples

Amazon's Transaction Processing

Amazon processes millions of transactions daily. When you order a book for £10:

- Amazon records a sale of £10 (credit sales)

- Your credit card payment creates a receivable that clears within days

- Amazon has already purchased that book from a publisher on credit (purchases on account)

- They might have 60-90 day payment terms with the publisher

- Meanwhile, they've received cash from you within 2-3 days

This creates positive cash flow - receiving cash before paying suppliers. It's one reason Amazon grew so successfully despite early unprofitability.

Starbucks' Cash Sales Model

When you buy a coffee at Starbucks for £3.50, that's a cash sale (even if you pay by card - remember, "cash" includes electronic payments). Starbucks receives money immediately, but they bought the coffee beans on credit weeks earlier. This cash-intensive model means Starbucks has excellent working capital - they have cash on hand before they need to pay suppliers.

Tesla's Deposit System

When Tesla launches a new car model, customers pay deposits (sometimes £1,000 or more) years before delivery. How is this recorded?

When deposit received:

Debit: Cash £1,000

Credit: Customer Deposits (Liability) £1,000

It's NOT sales revenue yet because they haven't delivered the car. It's a liability - they owe the customer a car or must return the money.

When car delivered:

Debit: Customer Deposits £1,000

Debit: Receivables £39,000 (remaining balance)

Credit: Sales £40,000

Now it becomes a sale because they've fulfilled their obligation.

Key Terms Recap

- Transaction - An exchange of value between a business and another party

- Cash Sale - Sale where payment is received immediately (including electronic payments)

- Credit Sale - Sale where payment will be received later

- Receivables (Debtors) - Customers who owe money to the business

- Cash Purchase - Purchase where payment is made immediately

- Credit Purchase - Purchase where payment will be made later

- Payables (Creditors) - Suppliers whom the business owes money

- Double-Entry - System where every transaction affects at least two accounts

- Debit - Left side of an account; increases assets and expenses, decreases liabilities and income

- Credit - Right side of an account; decreases assets and expenses, increases liabilities and income

- Sales Returns (Returns Inwards) - Goods returned by customers

- Purchase Returns (Returns Outwards) - Goods returned to suppliers

- Trade Discount - Reduction in list price, not recorded in accounts

- Cash Discount (Settlement Discount) - Reduction for early payment, recorded in accounts

- Discount Allowed - Early payment discount given to customers (expense)

- Discount Received - Early payment discount received from suppliers (income)

- Drawings - Money withdrawn by business owner for personal use

- Capital - Owner's investment in the business

- VAT (Value Added Tax) - Sales tax collected on behalf of government

- Source Document - Original evidence supporting a transaction (invoice, receipt, etc.)

- Sales Invoice - Document sent to customer for credit sales

- Credit Note - Document issued when customer returns goods

- Debit Note - Document sent to supplier when returning goods

- Books of Prime Entry (Day Books) - Journals where transactions are first recorded before posting to ledger

- Sales Day Book - Records all credit sales

- Purchases Day Book - Records all credit purchases

- Cash Book - Records all cash receipts and payments

- Petty Cash - Small amount of cash kept for minor expenses

- Imprest System - Method of maintaining petty cash at a fixed amount

- Control Account - Summary account showing total of all individual customer or supplier balances

- Bank Reconciliation - Process of matching cash book balance with bank statement

- Unpresented Cheques - Cheques written but not yet cashed

- Outstanding Deposits - Deposits made but not yet shown on bank statement

Common Mistakes and Misconceptions

Mistake 1: Thinking "Cash" Only Means Physical Money

Wrong thinking: "A customer paid by card, so it's not a cash sale."

Correct understanding: In accounting, "cash" includes any immediate payment method - physical currency, cheques, card payments, bank transfers, PayPal, etc. If payment happens right away, it's a cash transaction. The key is TIMING, not the physical form of payment.

Mistake 2: Recording Sales When You Send an Invoice

Wrong thinking: "I sent the invoice on Monday, so I record the sale on Monday, even though I won't ship the goods until Wednesday."

Correct understanding: Sales are recorded when you deliver the goods or perform the service, not when you send an invoice or receive an order. The critical event is the transfer of ownership or fulfillment of obligation.

Mistake 3: Confusing Drawings with Expenses

Wrong thinking: "The owner took £500 from the business for groceries. That's an expense."

Correct understanding: Drawings are NOT expenses. Expenses are costs incurred to run the business (rent, salaries, utilities). Drawings reduce the owner's equity but don't appear on the income statement. The entry is: Debit Drawings, Credit Cash.

Mistake 4: Recording Trade Discounts in the Accounts

Wrong thinking: "The supplier gave me a 10% trade discount on a £100 purchase. I'll record Purchases £100, Discount Received £10, Payables £90."

Correct understanding: Trade discounts are deducted BEFORE recording. You simply record: Debit Purchases £90, Credit Payables £90. The discount never appears in your books because the transaction happened at the net price.

Mistake 5: Treating VAT as Revenue or Expense

Wrong thinking: "I sold goods for £100 plus £20 VAT, so my sales are £120."

Correct understanding: VAT isn't your money - you're just collecting it for the government. Sales revenue is £100. The £20 is a liability you owe to the tax authorities. Similarly, VAT you pay on purchases isn't an expense - it's recoverable (an asset).

Mistake 6: Not Updating the Cash Book During Bank Reconciliation

Wrong thinking: "My cash book shows £1,000, the bank statement shows £1,200, so I'll just note the difference."

Correct understanding: When reconciling, you must UPDATE your cash book for items that appear on the bank statement but not in your records (bank charges, direct debits, interest, etc.). Only THEN do you reconcile for timing differences like unpresented cheques.

Mistake 7: Recording Both Sides of a Transaction in the Same Book of Prime Entry

Wrong thinking: "I'll record both the debit and credit in the Sales Day Book."

Correct understanding: Each book of prime entry captures ONE aspect of similar transactions. The Sales Day Book only records the credit sales part. The double-entry is completed when you POST from the day book to the ledger. The day book itself isn't double-entry - it's a list.

Mistake 8: Forgetting That Payment of Receivables Doesn't Affect Sales

Wrong thinking: "A customer paid £500 they owed me. I'll record: Debit Cash £500, Credit Sales £500."

Correct understanding: When a customer pays, you're converting one asset (receivables) into another (cash). Sales were already recorded when you made the original sale. The correct entry is: Debit Cash £500, Credit Receivables £500.

Summary

- Three transaction types: Sales (revenue coming in), Purchases (costs going out), and Cash (immediate money movement). Each can be either immediate (cash) or delayed (credit).

- Double-entry foundation: Every transaction affects at least two accounts. Debits must equal credits. This creates a self-balancing system that helps catch errors.

- Credit sales create receivables: When you sell on credit, you record sales revenue immediately (even though you haven't received cash) and create an asset called receivables. When the customer pays later, you convert receivables to cash - no new sales recorded.

- Credit purchases create payables: When you buy on credit, you record the purchase immediately (even though you haven't paid cash) and create a liability called payables. When you pay later, you reduce payables and cash - no additional purchase recorded.

- Two types of discounts: Trade discounts are never recorded (you record the net amount), while cash/settlement discounts ARE recorded (as Discount Allowed or Discount Received) because they're conditional on payment timing.

- VAT is not revenue or expense: VAT collected from customers is a liability (you owe it to the government). VAT paid to suppliers is an asset (you can reclaim it). Only the net amount goes to/from the tax authorities.

- Source documents provide proof: Every transaction must be supported by evidence - invoices for sales/purchases, receipts for cash, credit notes for returns. No document = potential fraud or error.

- Books of prime entry organize transactions: Instead of recording directly into main accounts, transactions are first listed in day books (Sales Day Book, Purchases Day Book, etc.), then totals are posted to the ledger periodically.

- Control accounts summarize multiple balances: Rather than check hundreds of individual customer accounts, the Receivables Control Account shows the total owed by all customers in one place. Same for Payables Control Account.

- Bank reconciliation resolves differences: Your cash book and bank statement rarely match due to timing differences (unpresented cheques, outstanding deposits) and items you didn't know about (bank charges, direct debits). Update your cash book first, then reconcile timing differences.

Practice Questions

Question 1 (Recall)

Define the following terms and explain the difference between them:

- Cash sale vs Credit sale

- Trade discount vs Cash discount

- Receivables vs Payables

Question 2 (Application)

On 1st March, you sold goods worth £2,000 to Customer A on credit with terms 2/10, n/30. On 8th March, Customer A paid the invoice in full.

Required: Prepare the journal entries for:

- The sale on 1st March

- The payment on 8th March

Question 3 (Application)

Your business purchased inventory listed at £5,000 from Supplier B. You receive a 15% trade discount and the payment terms are 3/10, n/30. You paid within 10 days to take advantage of the cash discount.

Required: Calculate:

- The amount at which you record the purchase

- The cash discount amount

- The actual cash paid

- Prepare journal entries for the purchase and the payment

Question 4 (Analytical)

The following information relates to your business for January:

- Opening Receivables: £8,000

- Credit sales for the month: £25,000

- Cash received from customers: £22,000

- Sales returns: £1,500

- Discounts allowed: £600

- Bad debts written off: £400

Required: Calculate the closing balance on the Receivables Control Account. Show your workings.

Question 5 (Analytical)

Your cash book shows a balance of £4,500 on 31st May. The bank statement shows £5,200. Investigation reveals:

- Cheques written but not yet presented: £1,200

- Deposits made on 31st May not yet on statement: £800

- Bank charges of £50 on statement, not in cash book

- Direct debit payment of £150 on statement, not in cash book

- Standing order receipt of £200 on statement, not in cash book

Required:

- Calculate the revised cash book balance after adjustments

- Prepare a bank reconciliation statement

- List the journal entries needed to update the cash book

Question 6 (Application)

On 10th April, you sold goods for £600 plus VAT at 20%. The customer paid by bank transfer immediately.

Required: Prepare the journal entry to record this transaction.

Question 7 (Analytical)

Explain why a business might have positive cash flow (lots of cash in the bank) but still show low profit on the income statement. Use the concepts of credit sales, credit purchases, and timing to support your answer.