Provisions and Contingencies (IAS 37)

What Are Provisions and Why Should You Care?

Imagine you run a car manufacturing company, and one of your models has been in the news because its brakes occasionally fail. You haven't been sued yet, but let's be honest-it's probably coming. Should your financial statements pretend everything is rosy? Or should they show that a storm might be brewing?

This is exactly what provisions are about. They're amounts you set aside in your financial statements for liabilities that are uncertain in timing or amount, but likely to happen. Think of them as financial umbrellas you carry when dark clouds gather, even if it hasn't started raining yet.

IAS 37 Provisions, Contingent Liabilities and Contingent Assets is the accounting standard that tells us when to recognise these "maybe" liabilities, when to just mention them in notes, and when to ignore them completely. It's all about being honest with investors and stakeholders about what might go wrong-without crying wolf every time there's a tiny risk.

The Three Categories: Provisions, Contingent Liabilities, and Contingent Assets

Before diving deep, let's understand the three siblings in the IAS 37 family:

- Provisions: Liabilities of uncertain timing or amount that you recognise (record) in your financial statements because they're probable and you can estimate them reliably

- Contingent Liabilities: Possible obligations that you don't recognise in the financial statements but disclose in the notes because they're either not probable enough or you can't measure them reliably

- Contingent Assets: Possible assets that you don't recognise but might disclose in notes if they're probable (accounting is cautious about counting your chickens before they hatch)

The key distinction? Recognition versus disclosure. Provisions make it onto the balance sheet. Contingent items stay in the notes-they're acknowledged but not counted yet.

What Exactly Is a Provision?

According to IAS 37, a provision is a liability of uncertain timing or amount. But it's not just any uncertainty-it must meet three strict criteria before you can recognise it:

- Present obligation: The entity has a present obligation (legal or constructive) as a result of a past event

- Probable outflow: It is probable that an outflow of resources embodying economic benefits will be required to settle the obligation

- Reliable estimate: A reliable estimate can be made of the amount of the obligation

All three must be ticked off. Miss one? No provision for you.

Present Obligation: It's Already Happened

The obligation must exist now, arising from a past event. This past event is called an obligating event-one that creates a legal or constructive obligation that leaves the entity with no realistic alternative to settling it.

Legal obligations are straightforward-they come from contracts, legislation, or other operations of law. If you sign a contract promising to restore a mining site after extraction, you have a legal obligation.

Constructive obligations are trickier. They arise when:

- The entity has indicated to other parties (through established patterns of past practice, published policies, or a sufficiently specific current statement) that it will accept certain responsibilities, AND

- As a result, the entity has created a valid expectation in those other parties that it will discharge those responsibilities

Real example: For years, a supermarket chain has had a policy of refunding customers who are dissatisfied with products, even without legal obligation. Customers expect this. At year-end, even though the supermarket doesn't know exactly who will return what, it has a constructive obligation to provide refunds and should recognise a provision.

Probable Outflow: More Likely Than Not

Probable means "more likely than not" to occur. In practical terms, this means a probability greater than 50%. If there's only a 40% chance you'll have to pay, it's not probable-you have a contingent liability instead, not a provision.

This threshold matters enormously. It's the difference between recording a liability on your balance sheet (which affects your ratios, your borrowing capacity, your share price) and merely mentioning it in a note that many investors might skim over.

Reliable Estimate: You Can Put a Number on It

You must be able to estimate the amount reliably. Notice the word isn't "perfectly" or "exactly"-it's reliably. Provisions are estimates by nature. You're dealing with uncertainty, but that uncertainty must be quantifiable.

The standard acknowledges that in extremely rare cases, no reliable estimate can be made. In such cases, you can't recognise a provision-you disclose it as a contingent liability instead.

Measurement: How Much Should You Recognise?

Once you've decided a provision is needed, you need to figure out how much to record. IAS 37 provides clear guidance:

Best Estimate

The amount recognised should be the best estimate of the expenditure required to settle the present obligation at the end of the reporting period. This is the amount the entity would rationally pay to settle the obligation or to transfer it to a third party at that date.

Think of it as: "If someone offered to take this problem off your hands right now, what would you reasonably pay them?"

Single Obligation vs. Large Population

The estimation method depends on what you're dealing with:

- Single obligation: Use the most likely outcome. If there's a lawsuit and your lawyers say there's a 60% chance you'll pay £1 million and a 40% chance you'll pay nothing, the most likely outcome is £1 million-that's your provision.

- Large population of items: Use the expected value method (weighted average of all possible outcomes). This is particularly relevant for warranties, refunds, or similar obligations affecting many transactions.

Expected Value Example

A company sells 10,000 products with a one-year warranty. Based on past experience:

- 80% will have no defects (cost = £0)

- 15% will have minor defects (repair cost = £50 per unit)

- 5% will have major defects (repair cost = £200 per unit)

Expected value calculation:

\[ \text{Expected cost per unit} = (0.80 \times £0) + (0.15 \times £50) + (0.05 \times £200) \] \[ = £0 + £7.50 + £10 = £17.50 \]Total provision = 10,000 × £17.50 = £175,000

Notice we didn't just pick the "most likely" outcome (£0) for each individual product. When dealing with large populations, the expected value smooths out the uncertainty across all items.

Discounting to Present Value

When the effect of the time value of money is material, provisions should be discounted to their present value. This applies when:

- The outflow will occur significantly in the future (typically more than one year away)

- The difference between the nominal amount and present value is material

The discount rate should be a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability. It should not reflect risks already considered in estimating future cash flows.

Discounting Example

A company operates a nuclear power station. It has a legal obligation to decommission the facility in 20 years. The estimated cost at that time is £50 million. The appropriate pre-tax discount rate is 5%.

Present value calculation:

\[ \text{Present Value} = \frac{\text{Future Value}}{(1 + r)^n} \] \[ = \frac{£50,000,000}{(1.05)^{20}} = \frac{£50,000,000}{2.6533} = £18,843,000 \]The company recognises a provision of approximately £18.84 million now, not £50 million. Each year, the provision will increase as the present value "unwinds"-this increase is recognised as a finance cost (sometimes called unwinding the discount).

Risks and Uncertainties

The estimate should take into account risks and uncertainties. However, uncertainty doesn't justify creating excessive provisions or deliberately overstating liabilities (that would violate the principle of prudence/conservatism without becoming imprudent).

Future Events

Future events that may affect the amount required to settle an obligation should be reflected in the provision where there is sufficient objective evidence that they will occur.

Example: A provision for environmental cleanup costs might consider new technology that will reduce costs, but only if there's objective evidence (not just hope) that this technology will be available and used.

Recognition Timing: When Does the Obligation Arise?

This is where things get interesting. The obligating event is the trigger. Let's explore common scenarios:

Restructuring Provisions

Imagine your company announces it's closing a factory and laying off 500 workers. Do you immediately recognise a provision for redundancy costs?

Not necessarily. A restructuring is a programme planned and controlled by management that materially changes either the scope of a business or the manner in which it's conducted.

You can only recognise a restructuring provision when you have a constructive obligation, which requires:

- A detailed formal plan identifying at least:

- The business or part of business concerned

- Principal locations affected

- Location, function, and approximate number of employees who will be compensated for termination

- Expenditures that will be undertaken

- When the plan will be implemented

- Valid expectation in those affected that the restructuring will be carried out, either by:

- Starting to implement the plan, OR

- Announcing the main features to those affected in a sufficiently specific manner

Just having a board decision isn't enough. Just announcing vague "efficiency improvements" isn't enough. You need a detailed plan and to have raised valid expectations.

What to Include in Restructuring Provisions

Include only direct expenditures arising from the restructuring, not costs associated with ongoing activities. This means:

- Include: Employee termination costs, lease termination penalties, costs of closing facilities

- Exclude: Retraining or relocating continuing staff, marketing costs, investment in new systems, future operating losses

The exclusion of future operating losses is crucial. Provisions aren't created for normal business activities, even if they're expected to be loss-making. If a factory will lose money until it closes, those future losses don't go into the provision. Only the direct costs of closing do.

Onerous Contracts

An onerous contract is one in which the unavoidable costs of meeting the obligations exceed the economic benefits expected to be received. "Unavoidable costs" are the lower of the cost of fulfilling the contract and any compensation or penalties from failure to fulfill it.

When you have an onerous contract, recognise a provision for the present obligation under the contract.

Example: You've signed a three-year lease for £100,000 per year for a retail space. After one year, you decide to close that location permanently. You try to sublet it but can only find a tenant willing to pay £60,000 per year. The remaining two years will cost you £40,000 per year more than you'll receive.

You have an onerous contract. You should recognise a provision for the unavoidable net cost:

\[ \text{Provision} = 2 \text{ years} \times (£100,000 - £60,000) = £80,000 \](This would typically be discounted to present value if material.)

Warranties

When you sell products with warranties, the obligating event is the sale. At the point of sale, you've created an obligation-even though you don't know which specific products will fail or when.

This is a classic case for using the expected value method across a large population, as we demonstrated earlier.

Environmental and Decommissioning Obligations

These often arise from legal requirements or constructive obligations to clean up contamination or restore sites.

The obligating event is the action that causes the damage or creates the legal obligation-often the extraction of resources or the operation of facilities.

Real-world example: BP's Deepwater Horizon oil spill in 2010 created massive environmental obligations. The obligating event was the spill itself. BP ultimately recognised provisions exceeding $60 billion for cleanup costs, fines, and compensation-one of the largest provisions in corporate history.

Contingent Liabilities: The "Maybe" Obligations

A contingent liability is either:

- A possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of uncertain future events not wholly within the entity's control, OR

- A present obligation that arises from past events but is not recognised because:

- It is not probable that an outflow of resources will be required to settle it, OR

- The amount cannot be measured with sufficient reliability

Key Difference from Provisions

The critical distinctions:

- Provisions: Present obligations, probable outflow, reliably measurable → Recognise on balance sheet

- Contingent liabilities: Possible obligations OR present obligations that aren't probable or reliably measurable → Disclose in notes only

There's one exception: if the possibility of outflow is remote, you don't even need to disclose a contingent liability.

Common Examples

- Lawsuit with uncertain outcome: Your company is being sued for £5 million. Your lawyers say there's a 30% chance you'll lose. This is a contingent liability (not probable), disclosed but not recognised.

- Guarantee of another entity's debt: You've guaranteed a loan for a subsidiary. If the subsidiary is healthy and unlikely to default, it's a contingent liability.

- Possible tax assessments: The tax authority is reviewing a filing, and there's a chance of additional assessment, but the outcome is uncertain.

Disclosure Requirements

For each class of contingent liability (unless the possibility of outflow is remote), disclose:

- Brief description of the nature of the contingent liability

- An estimate of its financial effect (if practicable)

- An indication of uncertainties relating to amount or timing

- The possibility of any reimbursement

Contingent Assets: Don't Count Your Chickens

A contingent asset is a possible asset that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of uncertain future events not wholly within the entity's control.

Examples include:

- A claim through legal processes where the outcome is uncertain

- Potential tax refunds under negotiation

- Insurance claims where recovery is probable but not certain

Recognition Rules: Very Conservative

Contingent assets are never recognised on the balance sheet. This reflects the prudence principle-don't count income until it's virtually certain.

However, when the inflow of economic benefits is probable, disclose the contingent asset in the notes (with similar details as for contingent liabilities).

When the realisation becomes virtually certain, it's no longer contingent-it becomes a real asset (typically a receivable) and should be recognised.

The Decision Tree: Provision, Contingent Liability, or Nothing?

Here's how to work through any scenario:

- Is there a present obligation from a past event?

- No → Possible obligation → Contingent liability (disclose unless remote)

- Yes → Go to step 2

- Is an outflow of resources probable (>50%)?

- No → Contingent liability (disclose unless remote)

- Yes → Go to step 3

- Can you make a reliable estimate?

- No → Contingent liability (disclose with explanation)

- Yes → Provision (recognise on balance sheet)

Journal Entries: Recording Provisions

Understanding the accounting mechanics helps cement the concepts. Here's how provisions move through the books.

Initial Recognition

When you first recognise a provision:

Dr Expense (or relevant cost category) £XXX

Cr Provision £XXX

Example: Recognising a warranty provision of £175,000:

Dr Warranty Expense £175,000

Cr Warranty Provision £175,000

The expense hits the profit or loss statement (reducing profit), and the provision appears as a liability on the balance sheet.

Utilising the Provision

When you actually incur the costs the provision was created for:

Dr Provision £XXX

Cr Cash/Payables £XXX

Example: During the year, warranty repairs costing £120,000 are performed:

Dr Warranty Provision £120,000

Cr Cash/Inventory/Payables £120,000

Notice: this does not go through the income statement again. You already recognised the expense when you created the provision. Now you're just settling the liability.

Year-End Review and Adjustment

At each reporting date, review provisions and adjust to reflect the current best estimate.

If the estimate increases:

Dr Expense £XXX

Cr Provision £XXX

If the estimate decreases:

Dr Provision £XXX

Cr Income/Reduction in expense £XXX

Unwinding the Discount

For discounted provisions, the carrying amount increases each period as you get closer to the payment date. This is called unwinding the discount.

Dr Finance Cost £XXX

Cr Provision £XXX

Using our earlier decommissioning example where we recognised £18.84 million for a £50 million obligation in 20 years at 5%:

After year 1, the provision increases by £18.84m × 5% = £942,000

Dr Finance Cost £942,000

Cr Decommissioning Provision £942,000

After year 1, the provision stands at £18.84m + £0.942m = £19.782m. This continues each year until, by year 20, it reaches the full £50m needed.

Specific Applications: Common Scenarios in Detail

Legal Claims and Litigation

When your company faces a lawsuit, the accounting treatment depends entirely on likelihood and measurability:

- Virtually certain to lose and amount estimable: Provision required

- Probable loss (>50%) and amount estimable: Provision required

- Possible but not probable (<> Contingent liability, disclose in notes

- Remote possibility: No recognition, no disclosure

Lawyers often resist giving definitive probability assessments, which creates challenges. Management must make informed judgments based on all available evidence.

Real-world example: When Volkswagen's emissions scandal broke in 2015, the company initially recognised provisions of approximately €6.7 billion in September 2015. By December 2015, this increased to €16.2 billion as the scale became clearer. The provisions covered vehicle refits, legal costs, and fines-all meeting the criteria of present obligation, probable outflow, and reliable estimate (even though the exact amounts were uncertain).

Environmental Rehabilitation

Mining, oil and gas, and chemical companies face significant obligations to rehabilitate sites after operations cease.

The obligating event typically occurs when:

- The extraction or contamination happens (the damage is done), AND

- There's a legal or constructive obligation to remediate

These provisions are usually:

- Recognised over the operational life of the site (as extraction occurs)

- Discounted because payment is far in the future

- Reviewed regularly as cost estimates, timing, and discount rates change

Example scenario: A mining company begins operations in January 2024. The mine will operate for 15 years. Legal requirements mandate site restoration when operations cease. Estimated restoration cost: £30 million in 2039. Discount rate: 6%.

Present value in 2024:

\[ PV = \frac{£30,000,000}{(1.06)^{15}} = \frac{£30,000,000}{2.3966} = £12,518,000 \]The company recognises a provision of £12.518 million and typically capitalises this as part of the cost of the mine asset (rather than expensing immediately). The asset is then depreciated over the mine's life, and the provision is unwound each year through finance costs.

Product Recalls

When a company discovers a product defect that requires recall, the obligating event is either:

- The legal requirement to recall (if mandated by regulators), OR

- The public announcement of the recall (if voluntary, creating a constructive obligation)

Before announcement, even if the defect is known internally, there may be no constructive obligation if the company hasn't committed to a recall.

Once the recall is announced, recognise a provision for:

- Cost of notifying customers

- Cost of collecting and destroying defective products

- Cost of replacement or refund

- Associated administrative costs

Reimbursements: When Someone Else Helps Pay

Sometimes when you have an obligation, a third party will reimburse some or all of the expenditure. Common examples:

- Insurance coverage for warranty claims

- Contractual indemnities where a supplier compensates you for defects

- Government grants for environmental cleanup

Accounting Treatment

When reimbursement is virtually certain to be received:

- Recognise the reimbursement as a separate asset (not offset against the provision)

- The amount recognised shouldn't exceed the provision amount

- In the income statement, the expense may be presented net of the reimbursement

Example: A company recognises a £500,000 provision for legal settlement. Insurance will reimburse £300,000 (virtually certain).

Journal entries:

Dr Legal Expense £500,000

Cr Legal Provision £500,000

Dr Insurance Receivable £300,000

Cr Legal Expense £300,000

Net effect on profit: £500,000 - £300,000 = £200,000 expense

Balance sheet shows:

- Asset: Insurance Receivable £300,000

- Liability: Legal Provision £500,000

If the reimbursement is only probable but not virtually certain, disclose it as a contingent asset but don't recognise it.

Changes in Provisions Over Time

Provisions aren't "set and forget." IAS 37 requires reviewing them at each reporting date and adjusting to the current best estimate.

Reasons for Changes

- New information: Better understanding of costs or probabilities

- Passage of time: Unwinding of discount

- Changes in estimates: Revised cost projections, changed discount rates

- Partial settlement: Some obligations are met

- Change in circumstances: The obligation increases, decreases, or is eliminated

Accounting for Changes

Increases in provisions are recognised as expenses (unless capitalised as part of an asset, such as with decommissioning costs).

Decreases reverse previous expenses or create income.

Where a provision is no longer required (the obligation is cancelled or expires), reverse it entirely:

Dr Provision £XXX

Cr Income £XXX

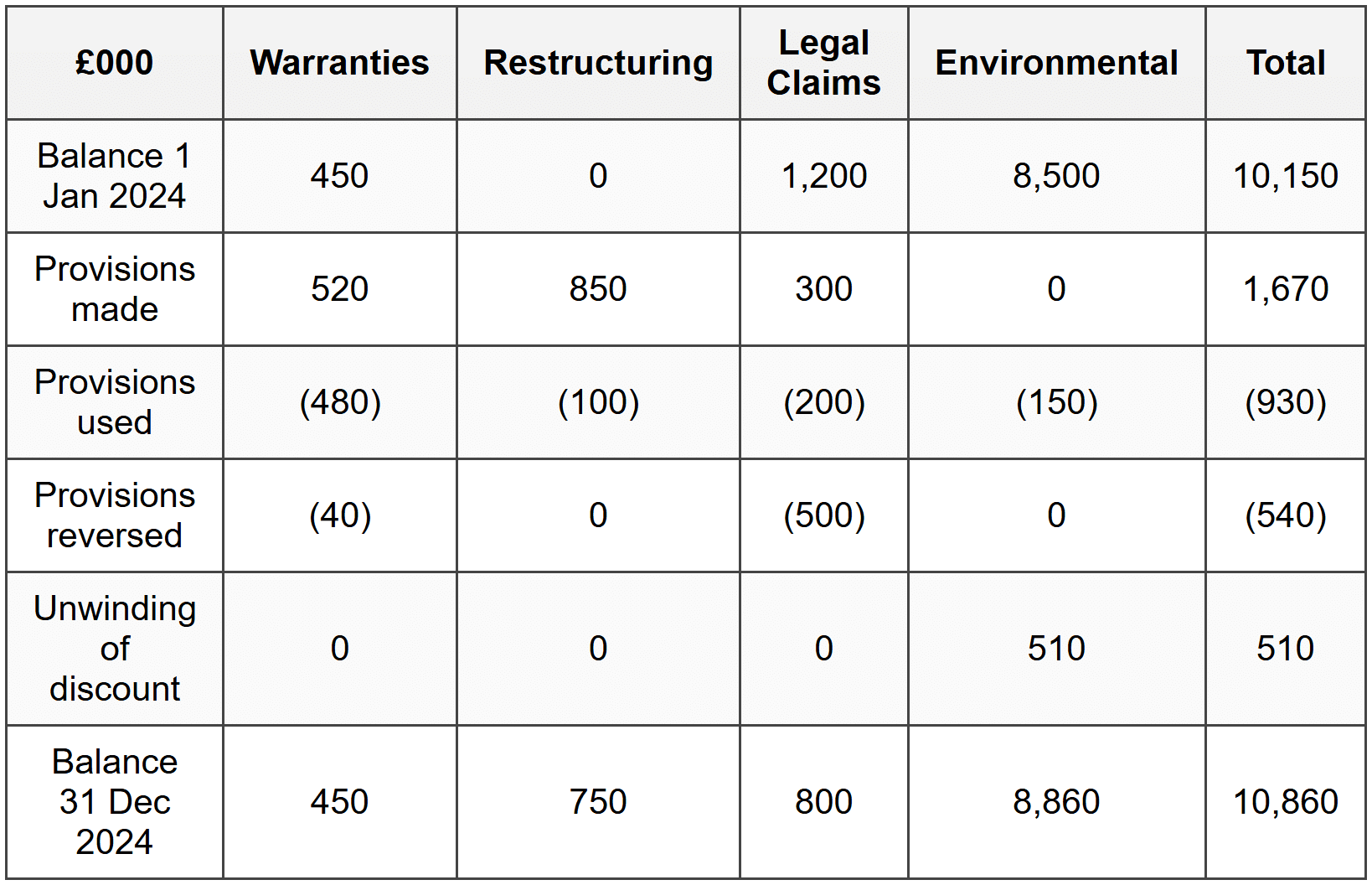

Disclosure Requirements: Transparency Is Key

IAS 37 has extensive disclosure requirements. For each class of provision, disclose:

- Carrying amount at beginning and end of period

- Additional provisions made during the period, including increases to existing provisions

- Amounts used (incurred and charged against the provision)

- Unused amounts reversed during the period

- Increase during the period in discounted amount arising from passage of time (unwinding)

- Brief description of nature of obligation and expected timing of outflows

- Indication of uncertainties about amount or timing

- Amount of any expected reimbursement

This reconciliation (often presented as a table) helps users understand how provisions evolved during the year.

Sample Disclosure Table

Each class would be accompanied by narrative explaining the nature, timing, and uncertainties.

What IAS 37 Does NOT Cover

It's important to know the boundaries. IAS 37 does not apply to:

- Financial instruments within the scope of IFRS 9

- Executory contracts (unless they're onerous-then IAS 37 applies)

- Insurance contracts within the scope of IFRS 17

- Provisions covered by other standards:

- Employee benefits (IAS 19)

- Income taxes (IAS 12)

- Leases (IFRS 16)

- Construction contracts (IFRS 15)

So when you see pensions, deferred tax, or lease obligations, remember: different standards apply.

Executory Contracts: The Balanced Exchange

An executory contract is one where neither party has performed their obligations, or both have partially performed their obligations to an equal extent.

Example: You sign a contract to purchase £100,000 of inventory in three months. Until you receive the goods or pay, it's executory-equally unperformed on both sides.

Generally, executory contracts don't create provisions because the obligations are balanced. However, if the contract becomes onerous, IAS 37 kicks in and you recognise a provision for the unavoidable net loss.

Prudence vs. Manipulation: Walking the Tightrope

IAS 37 embodies the prudence principle: recognise losses when probable, but don't recognise gains until virtually certain. This prevents over-optimistic reporting.

However, prudence must not become an excuse for creating "hidden reserves"-deliberately overstating provisions in good years to smooth profits by releasing them in bad years. This is earnings manipulation and violates the faithful representation principle.

The best estimate should be exactly that: your best judgment of the actual obligation, not a "rainy day fund" or a profit-smoothing tool.

Real-World Example: The Tobacco Industry

Tobacco companies face massive litigation over health impacts. For decades, these companies disclosed contingent liabilities for lawsuits but often didn't recognise provisions, arguing outcomes weren't probable or reliably measurable.

As judgments accumulated and settlement patterns emerged, some companies began recognising substantial provisions. Philip Morris USA, for instance, recognised provisions for certain state settlements once the terms became sufficiently certain.

This illustrates the judgment required: at what point does a "possible" liability become "probable"? When do you have enough information to estimate reliably? Different companies, faced with similar lawsuits, sometimes reached different conclusions-all within the framework of IAS 37, but reflecting different interpretations of the facts.

Key Terms Recap

- Provision - A liability of uncertain timing or amount that is recognised on the balance sheet because it represents a present obligation, a probable outflow of resources, and can be reliably estimated.

- Contingent Liability - Either a possible obligation whose existence will be confirmed by uncertain future events, or a present obligation that isn't probable or reliably measurable; disclosed in notes but not recognised on the balance sheet.

- Contingent Asset - A possible asset arising from past events whose existence will be confirmed by uncertain future events; disclosed if probable but never recognised until virtually certain.

- Obligating Event - A past event that creates a legal or constructive obligation, leaving the entity with no realistic alternative to settling it.

- Legal Obligation - An obligation that derives from a contract, legislation, or other operation of law.

- Constructive Obligation - An obligation arising from an entity's actions that create a valid expectation in other parties that it will accept and discharge certain responsibilities.

- Probable - More likely than not to occur; practically interpreted as greater than 50% probability.

- Best Estimate - The amount an entity would rationally pay to settle the obligation or transfer it to a third party at the reporting date.

- Expected Value - The weighted average of all possible outcomes, used for measuring provisions involving a large population of items.

- Most Likely Outcome - The single most probable scenario, used for measuring provisions involving a single obligation.

- Discount Rate - The pre-tax rate reflecting current market assessments of the time value of money and risks specific to the liability, used to calculate present value of long-term provisions.

- Unwinding the Discount - The periodic increase in a discounted provision as time passes and the payment date approaches, recognised as a finance cost.

- Restructuring - A programme planned and controlled by management that materially changes the scope of a business or the manner in which it's conducted.

- Onerous Contract - A contract in which the unavoidable costs of meeting obligations exceed the economic benefits expected to be received.

- Executory Contract - A contract where neither party has performed, or both have partially performed to an equal extent; generally doesn't create provisions unless it becomes onerous.

- Reimbursement - Amounts expected to be received from third parties to settle an obligation; recognised as a separate asset when virtually certain.

- Virtually Certain - A very high threshold of certainty, higher than probable; used for recognising contingent assets and reimbursements.

Common Mistakes and Misconceptions

- Mistake: Recognising provisions for future operating losses.

Reality: Provisions are for present obligations from past events, not future business activities. Expected future losses from continuing operations shouldn't be provided for (though an onerous contract creating those losses would require a provision). - Mistake: Creating provisions based on management's intention or budgets alone.

Reality: Intention isn't enough. There must be a present obligation-you can't recognise a provision just because you've decided to do something (like a restructuring) unless you've created a valid expectation in others through announcement or action. - Mistake: Confusing provisions with accruals.

Reality: Accruals are liabilities for goods/services received but not yet invoiced-they're certain in principle, just awaiting documentation. Provisions involve much greater uncertainty about timing or amount (or both). - Mistake: Offsetting provisions against related assets.

Reality: Provisions are shown as liabilities. Even when reimbursement is virtually certain, it's recognised as a separate asset, not netted against the provision on the balance sheet. - Mistake: Using the most likely outcome for large populations.

Reality: For large populations (like warranties), use expected value (weighted average), not the most likely outcome for individual items. - Mistake: Recognising contingent assets when probable.

Reality: Contingent assets are disclosed when probable but only recognised when virtually certain. The threshold for recognition is much higher than for liabilities (prudence in action). - Mistake: Failing to discount long-term provisions.

Reality: When the time value of money is material, provisions must be discounted to present value. A £50 million obligation in 20 years isn't worth £50 million today. - Mistake: Including all restructuring costs in the provision.

Reality: Only direct costs of restructuring go in the provision-not retraining, marketing, systems, or future operating costs. The scope is narrower than many assume. - Mistake: Treating "possible" and "probable" as the same thing.

Reality: "Probable" means >50% likely (recognise a provision); "possible" means somewhere between remote and probable (disclose as contingent liability but don't recognise). - Mistake: Forgetting to review provisions at each year-end.

Reality: Provisions must be reviewed and adjusted to the current best estimate at each reporting date. They're not one-time entries that sit unchanged for years.

Summary

- IAS 37 governs uncertain obligations, requiring provisions to be recognised when there's a present obligation from a past event, a probable outflow of resources, and a reliable estimate-all three criteria must be met.

- Provisions appear on the balance sheet as liabilities, while contingent liabilities are disclosed in notes only, and contingent assets are disclosed only when probable but recognised only when virtually certain.

- The measurement of provisions uses best estimate, applying the most likely outcome for single obligations and expected value for large populations, with discounting to present value when the time effect is material.

- Restructuring provisions require both a detailed formal plan and raised valid expectations, and they include only direct restructuring costs, excluding future operating losses and ongoing activity costs.

- Onerous contracts require provisions for the unavoidable net loss when obligations exceed expected benefits, but ordinary executory contracts don't create provisions.

- Provisions must be reviewed and adjusted at each reporting date, with increases charged to expense and decreases reversing previous charges, plus unwinding of discount recognised as finance cost.

- Reimbursements are recognised as separate assets when virtually certain, never offset against the provision on the balance sheet, though the income statement expense may be shown net.

- Disclosure requirements are extensive, including reconciliations showing opening balances, additions, uses, reversals, and closing balances for each class of provision.

- The obligating event is crucial-the timing of when a provision is recognised depends on when the past event creates the obligation with no realistic alternative to settlement.

- Prudence guides IAS 37, recognising probable losses but not gains until virtually certain, though this shouldn't justify creating hidden reserves or manipulating earnings.

Practice Questions

Question 1: Recognition Decision (Recall)

Alpha Ltd is being sued by a customer for £2 million. Alpha's lawyers assess there is a 45% chance Alpha will lose the case. Should Alpha recognise a provision, a contingent liability, or nothing? Explain your answer.

Question 2: Measurement Calculation (Application)

Beta Ltd sells 5,000 smartphones with a one-year warranty. Based on experience:

- 90% will require no repairs (cost £0)

- 8% will require minor repairs (cost £40 per unit)

- 2% will require major repairs (cost £150 per unit)

Calculate the total warranty provision Beta should recognise at the point of sale.

Question 3: Discounting Application (Application)

Gamma plc has a legal obligation to restore a quarry site in 10 years. The estimated restoration cost at that time is £5 million. The appropriate discount rate is 4% per annum. Calculate the provision that should be recognised now. (You may use the formula or approximation method.)

Question 4: Restructuring Timing (Analytical)

On 20 November 2024, Delta Ltd's board approved a restructuring plan to close a division, resulting in 200 redundancies and estimated costs of £3 million. The board decided to announce this to employees in January 2025. Delta's year-end is 31 December 2024. Should Delta recognise a restructuring provision in the 2024 financial statements? Explain your reasoning with reference to IAS 37 requirements.

Question 5: Onerous Contract (Application)

Epsilon Ltd signed a non-cancellable three-year contract on 1 January 2023 to lease office space for £120,000 per year. On 1 January 2024, Epsilon relocated and no longer uses this space. Despite efforts, Epsilon can only sublet the space for £70,000 per year for the remaining two years. The discount rate is 5%. Calculate the provision Epsilon should recognise on 1 January 2024. Show your workings.

Question 6: Contingent Asset Recognition (Analytical)

Zeta Ltd is claiming £800,000 from an insurance company for fire damage. Zeta's lawyers assess the claim as follows:

- 20% chance of receiving nothing

- 30% chance of receiving £400,000

- 50% chance of receiving the full £800,000

What amount, if any, should Zeta recognise as an asset? What disclosure, if any, should be made? Justify your answer.

Question 7: Provision Reconciliation (Application)

The following information relates to Theta Ltd's legal provisions:

- Balance at 1 January 2024: £450,000

- New provision created during 2024: £300,000

- Cash paid to settle claims during 2024: £200,000

- Provision no longer required reversed: £80,000

Calculate the provision balance at 31 December 2024 and show the journal entries for each transaction during the year.