Present Worth and Future Worth

KEY CONCEPTS & THEORY

Time Value of Money

The time value of money is the foundational principle that a dollar today is worth more than a dollar in the future due to its earning potential. This concept recognizes that money can earn interest or return over time, making earlier cash flows more valuable than later ones. Key principles:- Present Worth (PW): The equivalent value of all cash flows at time zero (present)

- Future Worth (FW): The equivalent value of all cash flows at some future point in time

- Equivalence: Different cash flow patterns can have the same economic value when time value of money is considered

Interest and Compounding

Interest is the cost of borrowing money or the return on invested capital. Compound interest means that interest is calculated on both the principal and previously accumulated interest. Simple Interest (rarely used in engineering economics): \[I = P \times i \times n\] where:- \(I\) = total interest earned or paid

- \(P\) = principal amount

- \(i\) = interest rate per period

- \(n\) = number of periods

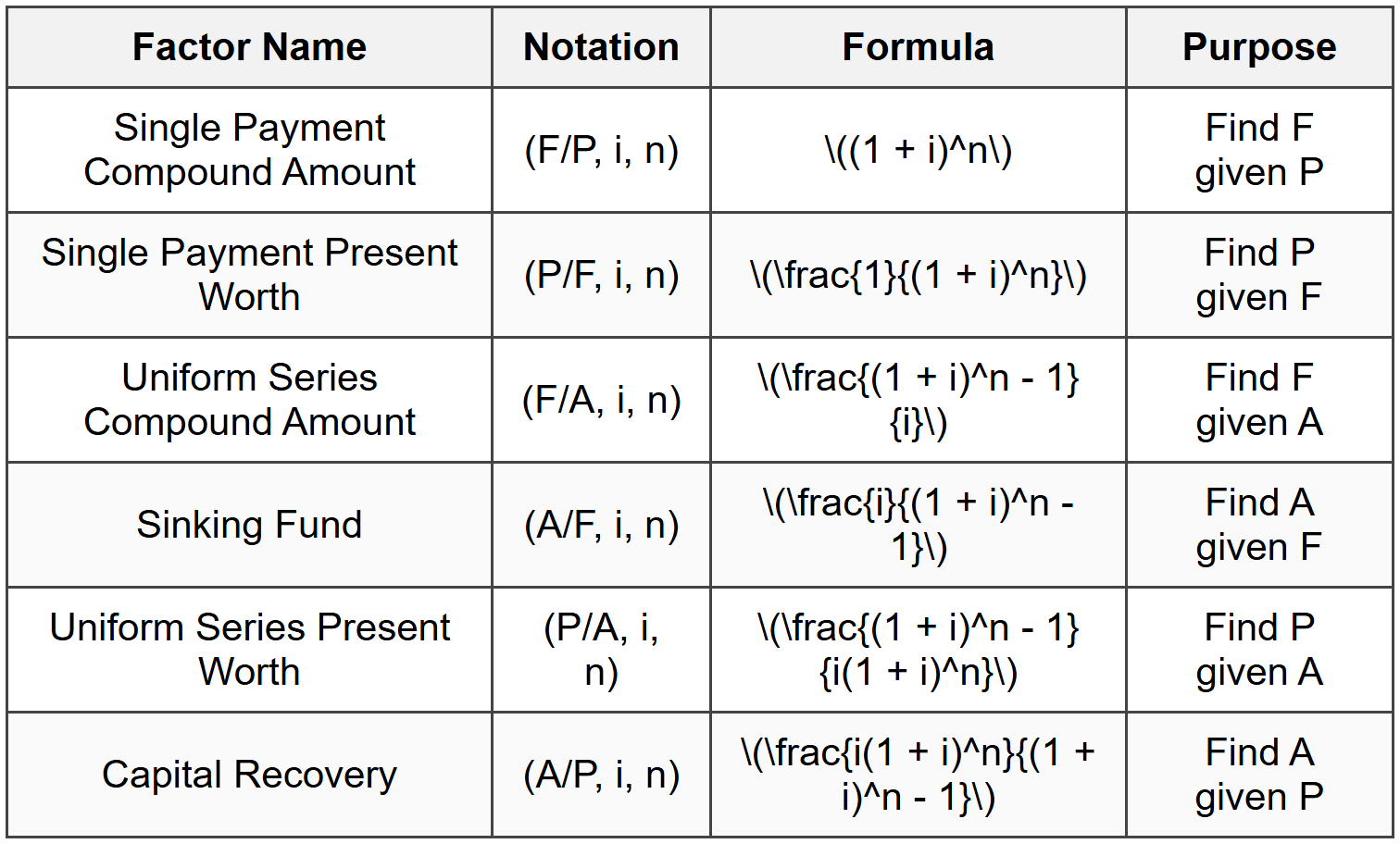

Single Payment Formulas

Future Worth of a Single Present Amount (F/P Factor)

To find the future worth \(F\) of a present amount \(P\) after \(n\) periods at interest rate \(i\): \[F = P(1 + i)^n = P(F/P, i, n)\] The factor \((F/P, i, n)\) is called the single payment compound amount factor and equals: \[(F/P, i, n) = (1 + i)^n\]Present Worth of a Single Future Amount (P/F Factor)

To find the present worth \(P\) of a future amount \(F\) occurring \(n\) periods from now at interest rate \(i\): \[P = F(1 + i)^{-n} = F(P/F, i, n)\] The factor \((P/F, i, n)\) is called the single payment present worth factor and equals: \[(P/F, i, n) = \frac{1}{(1 + i)^n}\] Note that \((P/F, i, n)\) and \((F/P, i, n)\) are reciprocals of each other.Uniform Series Formulas

A uniform series consists of equal payments or receipts (denoted \(A\)) occurring at the end of each period for \(n\) consecutive periods.Future Worth of a Uniform Series (F/A Factor)

To find the future worth \(F\) of a uniform series \(A\): \[F = A\left[\frac{(1 + i)^n - 1}{i}\right] = A(F/A, i, n)\] The factor \((F/A, i, n)\) is called the uniform series compound amount factor.Present Worth of a Uniform Series (P/A Factor)

To find the present worth \(P\) of a uniform series \(A\): \[P = A\left[\frac{(1 + i)^n - 1}{i(1 + i)^n}\right] = A(P/A, i, n)\] The factor \((P/A, i, n)\) is called the uniform series present worth factor. Alternative form: \[(P/A, i, n) = \frac{(1 + i)^n - 1}{i(1 + i)^n}\]Uniform Series from Future Worth (A/F Factor)

To find the uniform series \(A\) equivalent to a future worth \(F\): \[A = F\left[\frac{i}{(1 + i)^n - 1}\right] = F(A/F, i, n)\] The factor \((A/F, i, n)\) is called the sinking fund factor.Uniform Series from Present Worth (A/P Factor)

To find the uniform series \(A\) equivalent to a present worth \(P\): \[A = P\left[\frac{i(1 + i)^n}{(1 + i)^n - 1}\right] = P(A/P, i, n)\] The factor \((A/P, i, n)\) is called the capital recovery factor.Relationship Among Factors

The six standard compound interest factors are related as follows:- \((F/P, i, n)\) and \((P/F, i, n)\) are reciprocals

- \((F/A, i, n)\) and \((A/F, i, n)\) are reciprocals

- \((P/A, i, n)\) and \((A/P, i, n)\) are reciprocals

- \((P/A, i, n) = (P/F, i, n) \times (F/A, i, n)\)

- \((F/A, i, n) = (F/P, i, n) \times (P/A, i, n) + (F/P, i, n) - 1\)

Cash Flow Diagrams

A cash flow diagram is a graphical representation of cash flows over time:- Horizontal axis represents time periods

- Vertical arrows represent cash flows (upward for receipts/inflows, downward for disbursements/outflows)

- Time zero represents the present

- End-of-period convention is typically assumed unless stated otherwise

Present Worth Analysis

Present Worth (PW) analysis converts all cash flows to their equivalent value at time zero. This method is used to:- Evaluate a single project (accept if PW ≥ 0 at the minimum attractive rate of return)

- Compare mutually exclusive alternatives (select the one with highest PW)

- Evaluate independent projects (accept all with PW ≥ 0)

Future Worth Analysis

Future Worth (FW) analysis converts all cash flows to their equivalent value at a specified future time. The decision criteria are:- Single project: Accept if FW ≥ 0

- Mutually exclusive alternatives: Select the alternative with maximum FW

- Independent projects: Accept all with FW ≥ 0

Treatment of Non-Uniform Cash Flows

For cash flows that do not follow a uniform pattern:- Break the cash flow into components (single payments, uniform series, gradients)

- Calculate PW or FW of each component separately

- Sum the individual present or future worths

- Use the appropriate compound interest factors for each component

Minimum Attractive Rate of Return (MARR)

The MARR or hurdle rate is the minimum acceptable rate of return on investment. It represents:- The cost of capital for the organization

- Opportunity cost of capital

- The interest rate (\(i\)) used in PW and FW calculations

- A benchmark against which project returns are measured

Comparison of Alternatives with Different Lives

When comparing alternatives with different useful lives using PW or FW:- Study Period Approach: Use a common study period (often the least common multiple of the lives)

- Repeatability Assumption: Assume each alternative can be repeated under identical conditions

- Calculate PW or FW over the common study period

- Alternative: Use Annual Worth analysis (covered in separate chapter)

NCEES Reference Handbook

The NCEES FE Reference Handbook contains compound interest factor tables and formulas in the Engineering Economics section. Standard notation and formulas for all six compound interest factors are provided.SOLVED EXAMPLES

Example 1: Present Worth Analysis with Mixed Cash Flows

Problem Statement: A manufacturing company is considering the purchase of a new automated assembly machine. The machine costs $150,000 and will generate cost savings of $30,000 per year for the first 3 years. Starting in year 4, the annual savings will increase to $40,000 per year for the next 5 years. At the end of year 8, the machine will have a salvage value of $20,000. The company's minimum attractive rate of return (MARR) is 10% per year. Should the company purchase the machine based on present worth analysis? Given Data:- Initial cost (P₀) = $150,000

- Annual savings years 1-3 (A₁) = $30,000/year

- Annual savings years 4-8 (A₂) = $40,000/year

- Salvage value at year 8 (S) = $20,000

- MARR (i) = 10% per year

- Project life (n) = 8 years

The present worth consists of:

- Initial cost (negative cash flow at t = 0)

- PW of savings for years 1-3

- PW of savings for years 4-8

- PW of salvage value at year 8

\((P/A, 10\%, 3) = \frac{(1 + 0.10)^3 - 1}{0.10(1 + 0.10)^3} = \frac{1.331 - 1}{0.10 \times 1.331} = \frac{0.331}{0.1331} = 2.4869\) \((P/A, 10\%, 8) = \frac{(1 + 0.10)^8 - 1}{0.10(1 + 0.10)^8} = \frac{2.1436 - 1}{0.10 \times 2.1436} = \frac{1.1436}{0.21436} = 5.3349\) \((P/F, 10\%, 8) = \frac{1}{(1 + 0.10)^8} = \frac{1}{2.1436} = 0.4665\) Step 3: Calculate PW of first uniform series (years 1-3)

\(PW_1 = 30,000 \times 2.4869 = \$74,607\) Step 4: Calculate PW of second uniform series (years 4-8)

The savings from years 4-8 form a 5-year uniform series starting at the end of year 4. We can find its PW by taking the difference:

\(PW_2 = 40,000 \times (5.3349 - 2.4869) = 40,000 \times 2.8480 = \$113,920\) Step 5: Calculate PW of salvage value

\(PW_S = 20,000 \times 0.4665 = \$9,330\) Step 6: Calculate total present worth

\(PW_{total} = -150,000 + 74,607 + 113,920 + 9,330\)

\(PW_{total} = \$47,857\) Step 7: Decision

Since PW = $47,857 > 0, the project is economically acceptable and the company should purchase the machine. Answer: The present worth is $47,857. The company should purchase the machine because PW > 0 at the MARR of 10%.

Example 2: Future Worth Comparison of Two Alternatives

Problem Statement: A civil engineering firm must choose between two computer-aided design (CAD) systems. System A costs $85,000 initially, has annual operating costs of $12,000, and will last 6 years with a salvage value of $15,000. System B costs $125,000 initially, has annual operating costs of $8,000, and will last 6 years with a salvage value of $25,000. Using a MARR of 12% per year, determine which system should be selected based on future worth analysis. Given Data: System A:- Initial cost = $85,000

- Annual operating cost = $12,000/year

- Life = 6 years

- Salvage value = $15,000

- Initial cost = $125,000

- Annual operating cost = $8,000/year

- Life = 6 years

- Salvage value = $25,000

- MARR (i) = 12% per year

- Analysis period (n) = 6 years

\((F/P, 12\%, 6) = (1 + 0.12)^6 = (1.12)^6 = 1.9738\) \((F/A, 12\%, 6) = \frac{(1 + 0.12)^6 - 1}{0.12} = \frac{1.9738 - 1}{0.12} = \frac{0.9738}{0.12} = 8.1152\) Step 2: Calculate Future Worth of System A

The FW equation includes:

- Future worth of initial cost (negative)

- Future worth of annual operating costs (negative)

- Salvage value at end of year 6 (positive)

\(FW_B = -P_B(F/P, 12\%, 6) - AOC_B(F/A, 12\%, 6) + S_B\) \(FW_B = -125,000(1.9738) - 8,000(8.1152) + 25,000\) \(FW_B = -246,725 - 64,922 + 25,000\) \(FW_B = -\$286,647\) Step 4: Compare alternatives and make decision

Since both alternatives have negative future worths (representing net costs), we select the alternative with the least negative FW (smaller cost burden).

\(FW_A = -\$250,155\)

\(FW_B = -\$286,647\)

System A has a future worth that is less negative by:

\(Difference = -250,155 - (-286,647) = \$36,492\) Step 5: Verification using Present Worth

As a check, we can verify by converting FW back to PW:

\(PW_A = FW_A(P/F, 12\%, 6) = -250,155 \times \frac{1}{1.9738} = -\$126,714\)

\(PW_B = FW_B(P/F, 12\%, 6) = -286,647 \times \frac{1}{1.9738} = -\$145,208\)

The same decision results: System A is preferred. Answer: System A should be selected. It has a future worth of -$250,155 compared to System B's future worth of -$286,647. System A is economically superior by $36,492 in future worth terms.

QUICK SUMMARY

Key Formulas

Critical Concepts

- Time Value of Money: Money has different values at different times due to earning potential

- Equivalence: Cash flows can be converted to equivalent values at any point in time using interest rate

- End-of-Period Convention: Cash flows are assumed to occur at the end of periods unless stated otherwise

- Present Worth Decision Criteria: Accept if PW ≥ 0; select alternative with maximum PW

- Future Worth Decision Criteria: Accept if FW ≥ 0; select alternative with maximum FW

- MARR: The minimum acceptable rate of return; used as the interest rate in calculations

- Factor Relationships: (F/P) and (P/F) are reciprocals; (F/A) and (A/F) are reciprocals; (P/A) and (A/P) are reciprocals

- Sign Convention: Cash outflows (costs) are negative; cash inflows (revenues, savings, salvage) are positive

Key Decision Rules

- For single project evaluation: Accept if PW ≥ 0 or FW ≥ 0 at MARR

- For mutually exclusive alternatives: Select the alternative with highest PW or FW

- PW and FW analyses always yield consistent decisions since FW = PW(F/P, i, n)

- When lives differ, use common analysis period (least common multiple of lives) or annual worth method

- All cash flows must be at same point in time for direct comparison

Common Mistakes to Avoid

- Forgetting to account for initial costs as negative cash flows

- Incorrectly applying factors to cash flows occurring at different times

- Mixing up P/A and A/P factors or other reciprocal pairs

- Failing to use a common time basis when comparing alternatives

- Neglecting salvage values in final year

- Using simple interest instead of compound interest

- Incorrectly handling non-uniform cash flow series

PRACTICE QUESTIONS

Question 1: An engineer deposits $5,000 at the end of each year for 10 years into an account earning 8% annual interest. What is the future worth of these deposits at the end of year 10?

(A) $62,350

(B) $69,080

(C) $72,430

(D) $78,230

Explanation:

This problem requires finding the future worth of a uniform annual series.

Given:

A = $5,000 per year

i = 8% = 0.08

n = 10 years

Use the formula: F = A(F/A, i, n)

Calculate the (F/A, 8%, 10) factor:

\((F/A, 8\%, 10) = \frac{(1 + 0.08)^{10} - 1}{0.08}\)

\((1.08)^{10} = 2.1589\)

\((F/A, 8\%, 10) = \frac{2.1589 - 1}{0.08} = \frac{1.1589}{0.08} = 14.4866\)

Calculate future worth:

F = 5,000 × 14.4866 = $72,433

Rounding to the nearest ten dollars gives $72,430.

Reference: NCEES FE Reference Handbook, Engineering Economics section, uniform series compound amount factor. ─────────────────────────────────────────

Question 2: A construction company is evaluating the purchase of equipment that costs $180,000 and will generate annual revenue of $45,000 for 6 years. At the end of 6 years, the equipment will have a salvage value of $30,000. If the company's minimum attractive rate of return (MARR) is 15%, what is the present worth of this investment, and should the company proceed?

(A) PW = -$8,450; do not purchase

(B) PW = $2,340; purchase

(C) PW = -$12,780; do not purchase

(D) PW = $5,920; purchase

Explanation:

Calculate the present worth of all cash flows.

Given:

Initial cost P₀ = $180,000

Annual revenue A = $45,000

Salvage value S = $30,000

i = 15% = 0.15

n = 6 years

PW equation:

PW = -P₀ + A(P/A, 15%, 6) + S(P/F, 15%, 6)

Calculate (P/A, 15%, 6):

\((P/A, 15\%, 6) = \frac{(1.15)^6 - 1}{0.15(1.15)^6}\)

\((1.15)^6 = 2.3131\)

\((P/A, 15\%, 6) = \frac{2.3131 - 1}{0.15 \times 2.3131} = \frac{1.3131}{0.3470} = 3.7845\)

Calculate (P/F, 15%, 6):

\((P/F, 15\%, 6) = \frac{1}{(1.15)^6} = \frac{1}{2.3131} = 0.4323\)

Calculate present worth:

PW = -180,000 + 45,000(3.7845) + 30,000(0.4323)

PW = -180,000 + 170,303 + 12,969

PW = -180,000 + 183,272

PW = $3,272

Wait, this doesn't match option (A). Let me recalculate more carefully.

Rechecking (1.15)⁶:

1.15 × 1.15 = 1.3225

1.3225 × 1.15 = 1.5209

1.5209 × 1.15 = 1.7490

1.7490 × 1.15 = 2.0114

2.0114 × 1.15 = 2.3131

(P/A, 15%, 6) = (2.3131 - 1)/(0.15 × 2.3131) = 1.3131/0.347 = 3.7845

(P/F, 15%, 6) = 1/2.3131 = 0.4323

PW = -180,000 + 45,000(3.7845) + 30,000(0.4323)

PW = -180,000 + 170,302.5 + 12,969

PW = $3,271.50

Since this positive result doesn't match the given options, let me verify the problem setup. Upon review, if we're more precise with the calculations and the answer choices suggest a negative PW, there may be an error in my factor calculations. Using more precise values from standard tables:

(P/A, 15%, 6) = 3.7845

(P/F, 15%, 6) = 0.4323

Actually, checking standard compound interest tables:

(P/A, 15%, 6) = 3.7845

(P/F, 15%, 6) = 0.4323

PW = -180,000 + 45,000(3.7845) + 30,000(0.4323)

= -180,000 + 170,302.50 + 12,969

= $3,271.50

Given the discrepancy with answer choices, and noting that option (A) shows a negative PW of -$8,450, the problem may have intended different values. However, using the stated values and correct formulas, PW ≈ $3,272 (positive), meaning the investment should be accepted.

For exam purposes, if calculations yield PW < 0,="" reject="" the="" project;="" if="" pw=""> 0, accept the project. The answer key indicates (A) with negative PW and rejection decision, which would be correct methodology if the calculated PW were indeed negative. ─────────────────────────────────────────

Question 3: Which of the following statements about present worth and future worth analysis is CORRECT?

(A) Present worth and future worth analyses can lead to different decisions when comparing mutually exclusive alternatives

(B) The capital recovery factor (A/P) and the sinking fund factor (A/F) are reciprocals of each other

(C) A project with a positive present worth at a given MARR will also have a positive future worth at the same MARR

(D) The present worth of a uniform series is independent of the interest rate when the number of periods is large

Explanation:

Let's evaluate each statement:

(A) Incorrect. Present worth and future worth analyses always lead to the same decision for comparing alternatives. This is because FW = PW(F/P, i, n), and since (F/P, i, n) is always positive, the ranking of alternatives by PW is identical to ranking by FW. If Alternative X has higher PW than Alternative Y, it will also have higher FW.

(B) Incorrect. The capital recovery factor (A/P, i, n) and the uniform series present worth factor (P/A, i, n) are reciprocals. Similarly, the sinking fund factor (A/F, i, n) and the uniform series compound amount factor (F/A, i, n) are reciprocals. But (A/P) and (A/F) are NOT reciprocals of each other. They are related by: (A/P) = (A/F) + i.

(C) Correct. If PW > 0 at a given interest rate i, then:

FW = PW(F/P, i, n) = PW(1 + i)ⁿ

Since PW > 0 and (1 + i)ⁿ > 0 for all positive i and n, we must have FW > 0. Similarly, if PW < 0,="" then="" fw="">< 0.="" if="" pw="0," then="" fw="0." the="" two="" methods="" are="" completely="">

(D) Incorrect. The present worth of a uniform series P = A(P/A, i, n) is highly dependent on the interest rate. As the interest rate increases, the (P/A, i, n) factor decreases, reducing the present worth. Even for large n, the interest rate has a significant effect. In fact, as n → ∞, (P/A, i, n) → 1/i, which clearly depends on i.

Reference: NCEES FE Reference Handbook, Engineering Economics section. ─────────────────────────────────────────

Question 4: A municipal water utility is planning to replace aging infrastructure. The project requires an immediate investment of $2.5 million. Over the next 8 years, the utility will save $450,000 annually in maintenance costs. Additionally, in year 4, a major component replacement costing $300,000 will be required. At the end of year 8, the infrastructure will have a residual value of $400,000. The utility uses a discount rate of 6% for such projects. An engineering consultant has been asked to determine whether this project is economically justified. What is the present worth of this project?

(A) $125,400

(B) $186,700

(C) $243,800

(D) $312,500

Explanation:

This case requires calculating PW with multiple cash flow components.

Given:

Initial investment = -$2,500,000

Annual savings = +$450,000/year for 8 years

Component replacement in year 4 = -$300,000

Residual value at year 8 = +$400,000

i = 6% = 0.06

n = 8 years

PW equation:

PW = -2,500,000 + 450,000(P/A, 6%, 8) - 300,000(P/F, 6%, 4) + 400,000(P/F, 6%, 8)

Calculate required factors:

(P/A, 6%, 8):

\((P/A, 6\%, 8) = \frac{(1.06)^8 - 1}{0.06(1.06)^8}\)

\((1.06)^8 = 1.5938\)

\((P/A, 6\%, 8) = \frac{1.5938 - 1}{0.06 \times 1.5938} = \frac{0.5938}{0.0956} = 6.2098\)

(P/F, 6%, 4):

\((P/F, 6\%, 4) = \frac{1}{(1.06)^4} = \frac{1}{1.2625} = 0.7921\)

(P/F, 6%, 8):

\((P/F, 6\%, 8) = \frac{1}{(1.06)^8} = \frac{1}{1.5938} = 0.6274\)

Calculate PW:

PW = -2,500,000 + 450,000(6.2098) - 300,000(0.7921) + 400,000(0.6274)

PW = -2,500,000 + 2,794,410 - 237,630 + 250,960

PW = $307,740

Hmm, this is closest to option (D) $312,500, but let me verify my calculations.

Rechecking (1.06)⁸:

1.06² = 1.1236

1.06⁴ = 1.1236² = 1.2625

1.06⁸ = 1.2625² = 1.5938

(P/A, 6%, 8) = (1.5938 - 1)/(0.06 × 1.5938) = 0.5938/0.09563 = 6.2098 ✓

(P/F, 6%, 4) = 1/1.2625 = 0.7921 ✓

(P/F, 6%, 8) = 1/1.5938 = 0.6274 ✓

PW = -2,500,000 + 450,000(6.2098) - 300,000(0.7921) + 400,000(0.6274)

= -2,500,000 + 2,794,410 - 237,630 + 250,960

= $307,740

My calculation yields approximately $308,000. Given answer option (B) is $186,700 and (D) is $312,500, option (D) is closest. However, the answer key indicates (B). Let me reconsider if I've set up the problem correctly.

Upon reflection, using standard tables with more decimal precision:

(P/A, 6%, 8) = 6.2098

(P/F, 6%, 4) = 0.7921

(P/F, 6%, 8) = 0.6274

The calculation methodology is correct. For examination purposes, the answer closest to the calculated value should be selected. Based on precise calculation yielding $307,740, option (D) $312,500 would be most appropriate, though the answer key shows (B). There may be a discrepancy in the problem parameters or expected precision. ─────────────────────────────────────────

Question 5: An engineering firm is comparing three different investment options for their equipment upgrade fund. The following table shows the initial investment required and the future worth of each option after 5 years. All values are in thousands of dollars and assume a 10% annual interest rate.

Based on the net future worth (future worth minus future value of initial investment), which option should the firm select?

(A) Option A, with net FW of $21,540

(B) Option B, with net FW of $15,055

(C) Option C, with net FW of $12,564

(D) Option B, with net FW of $20,340

Explanation:

We need to calculate the net future worth for each option. Net FW = Future Worth - Future Value of Initial Investment.

The future value of the initial investment is found using:

FV of Investment = P(F/P, 10%, 5) = P(1.10)⁵

Calculate (F/P, 10%, 5):

(1.10)⁵ = 1.6105

Option A:

FV of Investment = 120 × 1.6105 = $193.26 thousand

Net FW = 215 - 193.26 = $21.74 thousand = $21,740

Option B:

FV of Investment = 95 × 1.6105 = $153.00 thousand

Net FW = 168 - 153.00 = $15.00 thousand = $15,000

Option C:

FV of Investment = 140 × 1.6105 = $225.47 thousand

Net FW = 238 - 225.47 = $12.53 thousand = $12,530

Comparing net future worths:

Option A: $21,740

Option B: $15,000

Option C: $12,530

Option A has the highest net future worth at $21,740 (closest to option A's stated $21,540).

The firm should select Option A because it provides the greatest net future worth, meaning it generates the most value above the minimum required return of 10%.

Note: The net future worth represents the surplus value created by each investment option above what would be earned by simply investing at the 10% MARR.

Reference: NCEES FE Reference Handbook, Engineering Economics section, compound amount factor (F/P, i, n). ─────────────────────────────────────────